Taxation Law and Practice: Assessment on Taxation Law Concepts

VerifiedAdded on 2020/03/04

|11

|3099

|44

Homework Assignment

AI Summary

This assignment on Taxation Law and Practice covers various aspects of Australian taxation. Part A explores the sources of taxation law, residency definitions, Medicare levy, specific deductions, and the valuation of stock. Part B analyzes the deductibility of expenses, including tax advisor fees and solicitor fees for objections. Part C examines the residency status of an international student. Part D calculates assessable income, including income from employment, tips, and gifts. Part E discusses deductible outgoings for a mortgage broker working from home. The assignment provides a comprehensive overview of key concepts such as assessable income, deductions, and residency, using examples to illustrate the practical application of tax laws.

Running head: TAXATION LAW AND PRACTICE

Taxation Law and Practice

Student’s Name:

University Name:

Author Note

Taxation Law and Practice

Student’s Name:

University Name:

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW AND PRACTICE

Table of Contents

Part A.........................................................................................................................................2

Part B..........................................................................................................................................4

Part C..........................................................................................................................................5

Part D.........................................................................................................................................6

Part E..........................................................................................................................................7

References:.................................................................................................................................9

Table of Contents

Part A.........................................................................................................................................2

Part B..........................................................................................................................................4

Part C..........................................................................................................................................5

Part D.........................................................................................................................................6

Part E..........................................................................................................................................7

References:.................................................................................................................................9

2TAXATION LAW AND PRACTICE

Part A

1. The primary source of the Commonwealth Parliament’s Taxation can be found under

section 51(ii) of the Australian Constitution (Chordia, Lynch, & Williams, 2013).

2. The primary source of Australia’s taxation laws is roughly, the parliament, courts and

government departments or statutory authorities. The taxation laws are derived from

the Commonwealth Constitution and the rules and regulations of its international

treaties, as well as many Double Tax Agreements (DTAs) done with foreign countries

(Whait, 2012).

3. Taxation Ruling TR 98/17 discusses essentially the meaning of the word resides, in

respect to the definition of the word resident in the Income Tax Assessment Act, 1936

under subsection 6(1). This ruling applies to probably all the individuals visiting

Australia including students living in Australia for academic purposes or migrants

residing in Australia or contractual employees. The ruling however is not applicable

for residents of Australia who have been living overseas for a temporary period of

time. The word resides generally means a person dwelling in a particular place for a

considerable amount of time (Kobetsky et al., 2012). However under the definition of

this ruling, the period of stay of a single individual is not the determining factor in

regards of he or she being the resident of Australia. An individual is considered a

resident of Australia on the grounds of quality, character, behavior and habit of that

particular individual. Furthermore the living and social standards, business links,

location and preservation of assets, are also monitored and evaluated. The consistent

maintenance of behavior along with the residing status is the determining factor for an

individual to gain residential status of the country. Now to explain the meaning of the

term resident or resident of Australia in legal terms, a resident is a person who is

Part A

1. The primary source of the Commonwealth Parliament’s Taxation can be found under

section 51(ii) of the Australian Constitution (Chordia, Lynch, & Williams, 2013).

2. The primary source of Australia’s taxation laws is roughly, the parliament, courts and

government departments or statutory authorities. The taxation laws are derived from

the Commonwealth Constitution and the rules and regulations of its international

treaties, as well as many Double Tax Agreements (DTAs) done with foreign countries

(Whait, 2012).

3. Taxation Ruling TR 98/17 discusses essentially the meaning of the word resides, in

respect to the definition of the word resident in the Income Tax Assessment Act, 1936

under subsection 6(1). This ruling applies to probably all the individuals visiting

Australia including students living in Australia for academic purposes or migrants

residing in Australia or contractual employees. The ruling however is not applicable

for residents of Australia who have been living overseas for a temporary period of

time. The word resides generally means a person dwelling in a particular place for a

considerable amount of time (Kobetsky et al., 2012). However under the definition of

this ruling, the period of stay of a single individual is not the determining factor in

regards of he or she being the resident of Australia. An individual is considered a

resident of Australia on the grounds of quality, character, behavior and habit of that

particular individual. Furthermore the living and social standards, business links,

location and preservation of assets, are also monitored and evaluated. The consistent

maintenance of behavior along with the residing status is the determining factor for an

individual to gain residential status of the country. Now to explain the meaning of the

term resident or resident of Australia in legal terms, a resident is a person who is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW AND PRACTICE

living in Australia continuously or intermittently for a part or half of the income year

and has an intention to take up resident status in Australia. An individual’s purpose or

reason of stay in Australia also acts as a determining factor in ensuring whether he or

she resides in Australia or not (Harding, 2012).

4. Medicare levy is a service provided by the government of Australia which lies in the

domain of public health care. A resident, who pays the taxes regularly and has an

annual income of $26,668 per year, he or she has to pay a Medicare levy of two

percent which is always calculated on the respective taxable income of the taxpayer.

For an instance if the total taxable income of an individual is $60000, then the

Medicare levy of two percent that is $1200 will be payable by him. Therefore any

resident having taxable income that is greater than or equal to $26,668 will have to

Medicare levy will be reduced and earnings below the minimum level will have zero

Medicare pay a Medicare levy of two percent. In case the taxable income is below the

limit then the levy applied on it (Taylor, 2012).

5. The Division of the Income Tax Assessment Act 1997 that denies a company that has

been fined under Commonwealth consumer legislation for engaging in misleading and

deceptive conduct from deducting the costs of the fine is 3(G)5 (Taylor & Richardson,

2012).

6. A specific deduction is an expense or loss which can be deducted under a specific or a

particular provision of the Tax Acts except section 8-1 of the ITAA 1997. Now

Section 25-45 ITAA97 specifically involves deduction in respect to a loss due to

events such as embezzlements, theft, larceny or defalcation on the part of the

stakeholders or taxpayers. Thus the deduction under Section 25-45 ITAA97 is a

specific deduction (Boccabella, 2012).

living in Australia continuously or intermittently for a part or half of the income year

and has an intention to take up resident status in Australia. An individual’s purpose or

reason of stay in Australia also acts as a determining factor in ensuring whether he or

she resides in Australia or not (Harding, 2012).

4. Medicare levy is a service provided by the government of Australia which lies in the

domain of public health care. A resident, who pays the taxes regularly and has an

annual income of $26,668 per year, he or she has to pay a Medicare levy of two

percent which is always calculated on the respective taxable income of the taxpayer.

For an instance if the total taxable income of an individual is $60000, then the

Medicare levy of two percent that is $1200 will be payable by him. Therefore any

resident having taxable income that is greater than or equal to $26,668 will have to

Medicare levy will be reduced and earnings below the minimum level will have zero

Medicare pay a Medicare levy of two percent. In case the taxable income is below the

limit then the levy applied on it (Taylor, 2012).

5. The Division of the Income Tax Assessment Act 1997 that denies a company that has

been fined under Commonwealth consumer legislation for engaging in misleading and

deceptive conduct from deducting the costs of the fine is 3(G)5 (Taylor & Richardson,

2012).

6. A specific deduction is an expense or loss which can be deducted under a specific or a

particular provision of the Tax Acts except section 8-1 of the ITAA 1997. Now

Section 25-45 ITAA97 specifically involves deduction in respect to a loss due to

events such as embezzlements, theft, larceny or defalcation on the part of the

stakeholders or taxpayers. Thus the deduction under Section 25-45 ITAA97 is a

specific deduction (Boccabella, 2012).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW AND PRACTICE

7. The significance of the High Court case, W Thomas & Co Pty Ltd v FC of T (1965)

115 CLR 58, in the topic of deductions is that in this case as it can be observed,

deductions regarding repair of walls, roof and floor of the building, was considered a

capital expenditure. The entire point of the case law lies in determining whether a

particular renovation is a repair or maintenance, meaning whether a particular repair

is required for the property to function properly or is it just needed for the

maintenance of the appearance of the property. Thus the expenditure incurred in this

situation is of a capital nature. It therefore will be not deductible under subsection

53(1) (Maples, 2012).

8. The three ways that a taxpayer can choose to value each item of stock on hand at the

end of the income year are the cost price method, market selling value method and the

replacement value method. The cost price method roughly involves bringing the stock

to its present location and value. The market selling value method involves usage of

the current stock when it is sold normally, in a particular financial year. The

replacement value method involves the cost of the stock to retrieve an almost identical

item on the ending day of the financial year.

9. The applicable tax rate for a taxpayer whose taxable income is $45000 is $3572 plus

32.5c for each $1 over $37000. Therefore the tax rate would be [$3572 +

32.5c*($45000 - $37000)] $6172.

10. PAYG stands for pay as you go. PAYG tax collection system refers to the process

where an employer helps his employees or payees in meeting up to their tax liabilities

at the end of the financial year by withholding some amount of their respective

payments (Kaganovich & Zilcha, 2012).

7. The significance of the High Court case, W Thomas & Co Pty Ltd v FC of T (1965)

115 CLR 58, in the topic of deductions is that in this case as it can be observed,

deductions regarding repair of walls, roof and floor of the building, was considered a

capital expenditure. The entire point of the case law lies in determining whether a

particular renovation is a repair or maintenance, meaning whether a particular repair

is required for the property to function properly or is it just needed for the

maintenance of the appearance of the property. Thus the expenditure incurred in this

situation is of a capital nature. It therefore will be not deductible under subsection

53(1) (Maples, 2012).

8. The three ways that a taxpayer can choose to value each item of stock on hand at the

end of the income year are the cost price method, market selling value method and the

replacement value method. The cost price method roughly involves bringing the stock

to its present location and value. The market selling value method involves usage of

the current stock when it is sold normally, in a particular financial year. The

replacement value method involves the cost of the stock to retrieve an almost identical

item on the ending day of the financial year.

9. The applicable tax rate for a taxpayer whose taxable income is $45000 is $3572 plus

32.5c for each $1 over $37000. Therefore the tax rate would be [$3572 +

32.5c*($45000 - $37000)] $6172.

10. PAYG stands for pay as you go. PAYG tax collection system refers to the process

where an employer helps his employees or payees in meeting up to their tax liabilities

at the end of the financial year by withholding some amount of their respective

payments (Kaganovich & Zilcha, 2012).

5TAXATION LAW AND PRACTICE

Part B

According to the question, the first cost is payment to tax advisor to complete

previous year’s income tax return ($1000) which will be deductible as it is included in the

preparation and lodging of the tax return and related activities. The next cost is the amount

paid by Ram to his solicitor to draft an objection to an ATO assessment that he received two

years ago, which will not be deductible as the maximum time limit within which the

objection should be registered with the ATO has passed. Had the payment been done by Ram

within the prescribed time limit then the transaction would have been counted under the

deductions (De Mooij, 2012). The third cost is the total income tax paid by Ram that is

$50000. As nothing is mentioned in the question, it may be assumed that the income tax paid

by Ram is of the current financial year. Thus after reducing the total assessable income by the

deductions, the amount of tax payable or income tax is arrived at. Therefore no deduction

will be applicable for the third cost (Harding, 2013).

Part C

According to the given question, on November 11 Tina a twenty year old international

student arrives in Brisbane to study at university. Here the key points vital for arriving at a

decision in regards to the residency status of Tina is that she is more than eighteen years old

and arrives in Australia. Then the next statement mentioned in the question is that she works

part time in a local supermarket to help with living expenses and study fees. Her earnings to

30 June are $12,000. Hence the key points that can be inferred from this statement is that she

has visited Australia for academic purposes and in order to support her expenses, she has

taken up a part time job that which has fetched her $12,000 on 30th June (Shaw, 2012). The

last statement is that she does not do well in the assignments and exams and fails all subjects

and therefore she returns to her home country. Thus the only key point in the last statement is

Part B

According to the question, the first cost is payment to tax advisor to complete

previous year’s income tax return ($1000) which will be deductible as it is included in the

preparation and lodging of the tax return and related activities. The next cost is the amount

paid by Ram to his solicitor to draft an objection to an ATO assessment that he received two

years ago, which will not be deductible as the maximum time limit within which the

objection should be registered with the ATO has passed. Had the payment been done by Ram

within the prescribed time limit then the transaction would have been counted under the

deductions (De Mooij, 2012). The third cost is the total income tax paid by Ram that is

$50000. As nothing is mentioned in the question, it may be assumed that the income tax paid

by Ram is of the current financial year. Thus after reducing the total assessable income by the

deductions, the amount of tax payable or income tax is arrived at. Therefore no deduction

will be applicable for the third cost (Harding, 2013).

Part C

According to the given question, on November 11 Tina a twenty year old international

student arrives in Brisbane to study at university. Here the key points vital for arriving at a

decision in regards to the residency status of Tina is that she is more than eighteen years old

and arrives in Australia. Then the next statement mentioned in the question is that she works

part time in a local supermarket to help with living expenses and study fees. Her earnings to

30 June are $12,000. Hence the key points that can be inferred from this statement is that she

has visited Australia for academic purposes and in order to support her expenses, she has

taken up a part time job that which has fetched her $12,000 on 30th June (Shaw, 2012). The

last statement is that she does not do well in the assignments and exams and fails all subjects

and therefore she returns to her home country. Thus the only key point in the last statement is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW AND PRACTICE

the total time period for which she stays in Australia that is 11th November to 30th June (8

months and 19 days). Though there are many perks of being a resident in Australia like

applying for an Australian passport and to travel in and out of Australia without being applied

for a resident return visa, participating in elections, and applying for a job in armed forces.

But unfortunately Tina will not be able to be a resident of Australia because in order to be a

permanent resident of Australia the person applying for being a resident in Australia should

stay in Australia for four consecutive years immediately before applying for the same. The

person should also be a permanent resident of Australia for twelve months and must not be

absent from Australia for a period not more than twelve months before applying. Thus Tina

cannot be a resident of Australia because her total stay in Australia is only for 8 months and

19 days. Neither does she satisfy any of the conditions in terms of tenure of stay in Australia

nor does she have any intent of continuing her association with Australia as unfortunately she

has failed her subjects and returned to her home country. Tina will also have to pay foreign

tax as she has earned a certain sum of money in Brisbane (Mabaso, 2012).

Part D

In this question, it has been asked to calculate the assessable income of Jimmy who is

an Australian single full-time university student and works part time in a restaurant. It has

been asked in the question to calculate the assessable income of Jimmy.

Assessable income is any income which is obtained through business or service, even

foreign income is also included in assessable income. Essentially assessable income is the

income or amount that is considered while calculating taxable income payable by an

individual for a particular financial year (Higgins & Sinning, 2013).

Now the first point that has been given about Jimmy’s income is that the income

earned from working in restaurant is $27,000. This entire amount will be counted in

the total time period for which she stays in Australia that is 11th November to 30th June (8

months and 19 days). Though there are many perks of being a resident in Australia like

applying for an Australian passport and to travel in and out of Australia without being applied

for a resident return visa, participating in elections, and applying for a job in armed forces.

But unfortunately Tina will not be able to be a resident of Australia because in order to be a

permanent resident of Australia the person applying for being a resident in Australia should

stay in Australia for four consecutive years immediately before applying for the same. The

person should also be a permanent resident of Australia for twelve months and must not be

absent from Australia for a period not more than twelve months before applying. Thus Tina

cannot be a resident of Australia because her total stay in Australia is only for 8 months and

19 days. Neither does she satisfy any of the conditions in terms of tenure of stay in Australia

nor does she have any intent of continuing her association with Australia as unfortunately she

has failed her subjects and returned to her home country. Tina will also have to pay foreign

tax as she has earned a certain sum of money in Brisbane (Mabaso, 2012).

Part D

In this question, it has been asked to calculate the assessable income of Jimmy who is

an Australian single full-time university student and works part time in a restaurant. It has

been asked in the question to calculate the assessable income of Jimmy.

Assessable income is any income which is obtained through business or service, even

foreign income is also included in assessable income. Essentially assessable income is the

income or amount that is considered while calculating taxable income payable by an

individual for a particular financial year (Higgins & Sinning, 2013).

Now the first point that has been given about Jimmy’s income is that the income

earned from working in restaurant is $27,000. This entire amount will be counted in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW AND PRACTICE

assessable income as this is the direct income earned by Jimmy. As mentioned in the question

Jimmy also has received tips from customers for $750 cash which will also be included in the

assessable income calculations. The third point is that Jimmy gets a bottle of alcohol as a gift

from one of the customers worth $250 but Jimmy does not drink so he gives away the bottle

to Eva. Now this income will not fall under assessable income as the item of income that is

the bottle is passed on to Eva. Had Jimmy accepted the bottle of scotch, then the income

would have been included in assessable income because it is a gift related to the work that

Jimmy does. The fourth point is that Jimmy receives a gift worth $15,000 for Christmas from

his parents. This will not be included in assessable income because the nature of the gift

received by Jimmy from his parents is personal (Rahman & Harding, 2014). A personal

income is not included in assessable income. The last point is that each month Jimmy’s

employer at the restaurant takes all staff including Jimmy out for dinner and the total expense

of the food that Jimmy eats on these nights is $645. This will not be included in assessable

income because there is no mention of payment of $645 as an allowance to Jimmy by his

employer. Therefore without any recorded bill or receipt this income cannot be included in

assessable income (Menezes, 2012).

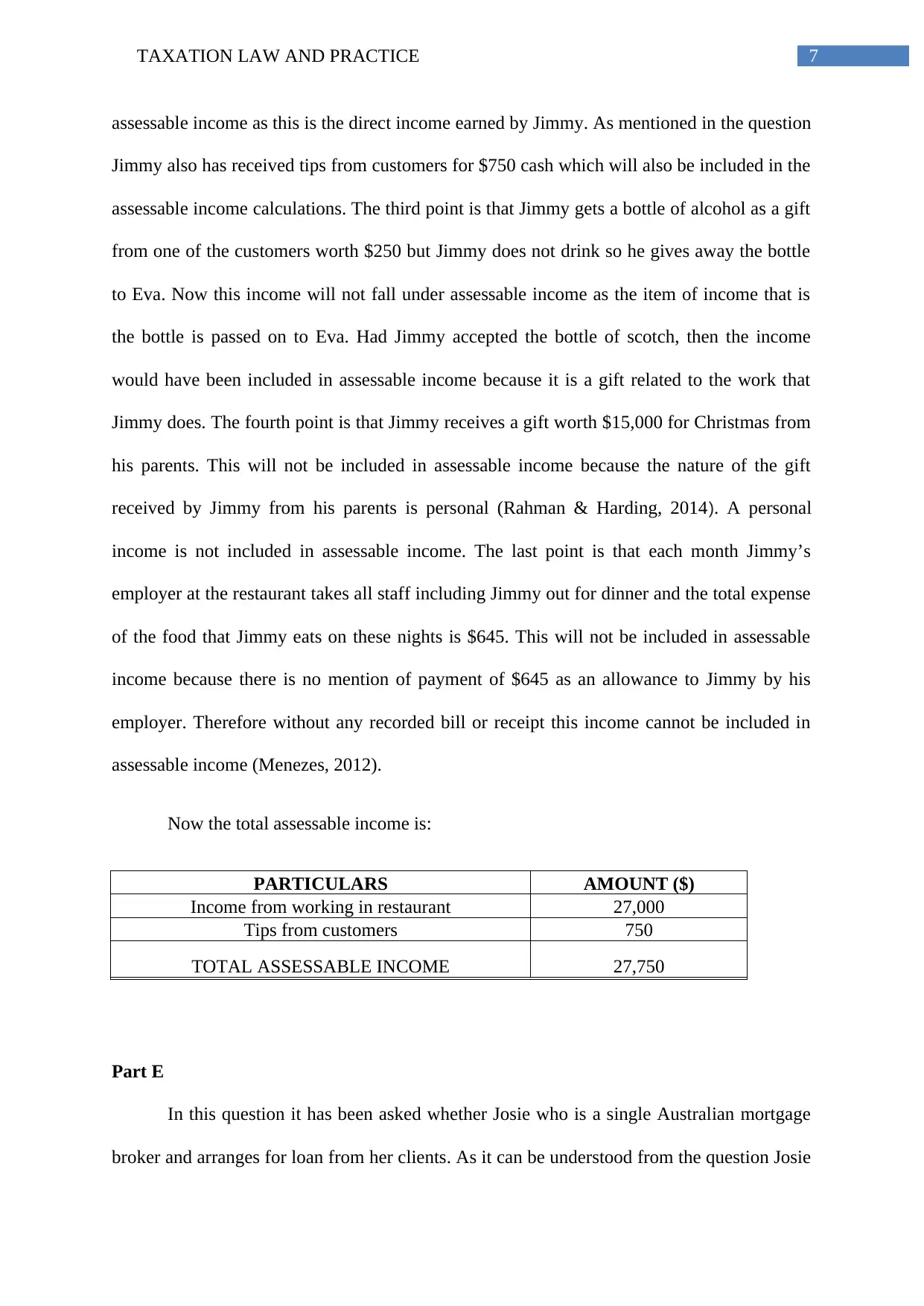

Now the total assessable income is:

PARTICULARS AMOUNT ($)

Income from working in restaurant 27,000

Tips from customers 750

TOTAL ASSESSABLE INCOME 27,750

Part E

In this question it has been asked whether Josie who is a single Australian mortgage

broker and arranges for loan from her clients. As it can be understood from the question Josie

assessable income as this is the direct income earned by Jimmy. As mentioned in the question

Jimmy also has received tips from customers for $750 cash which will also be included in the

assessable income calculations. The third point is that Jimmy gets a bottle of alcohol as a gift

from one of the customers worth $250 but Jimmy does not drink so he gives away the bottle

to Eva. Now this income will not fall under assessable income as the item of income that is

the bottle is passed on to Eva. Had Jimmy accepted the bottle of scotch, then the income

would have been included in assessable income because it is a gift related to the work that

Jimmy does. The fourth point is that Jimmy receives a gift worth $15,000 for Christmas from

his parents. This will not be included in assessable income because the nature of the gift

received by Jimmy from his parents is personal (Rahman & Harding, 2014). A personal

income is not included in assessable income. The last point is that each month Jimmy’s

employer at the restaurant takes all staff including Jimmy out for dinner and the total expense

of the food that Jimmy eats on these nights is $645. This will not be included in assessable

income because there is no mention of payment of $645 as an allowance to Jimmy by his

employer. Therefore without any recorded bill or receipt this income cannot be included in

assessable income (Menezes, 2012).

Now the total assessable income is:

PARTICULARS AMOUNT ($)

Income from working in restaurant 27,000

Tips from customers 750

TOTAL ASSESSABLE INCOME 27,750

Part E

In this question it has been asked whether Josie who is a single Australian mortgage

broker and arranges for loan from her clients. As it can be understood from the question Josie

8TAXATION LAW AND PRACTICE

does most of her work from home. It is also mentioned that home office occupies only 15

percent of the total space in her home (Taylor & Richardson, 2013). The outgoings incurred

by Josie are council rates which is a deductible item. The next outgoing is interest on her

home loan for 18,900$ which is also a deductible item but not totally, that is, as Josie works

from home and only fifteen percent of the total space in her home is occupied by her home

office that is why only fifteen percent of 18,900$ will be deductible (Tran-Nam & Evans,

2012). The next outgoing is electricity and heating costs for $6,800 of which only fifteen

percent will be taken into account. The daily wages for cleaning lady will also be deductible

but again only fifteen percent of it will be taken into account as only fifteen percent of the

total home space constitutes of her office (Kobetsky., 2012). The next outgoings are home

telephone and mobile bill, percentages of which are given as to how much are the phone used

for business purposes (Whait, 2012).

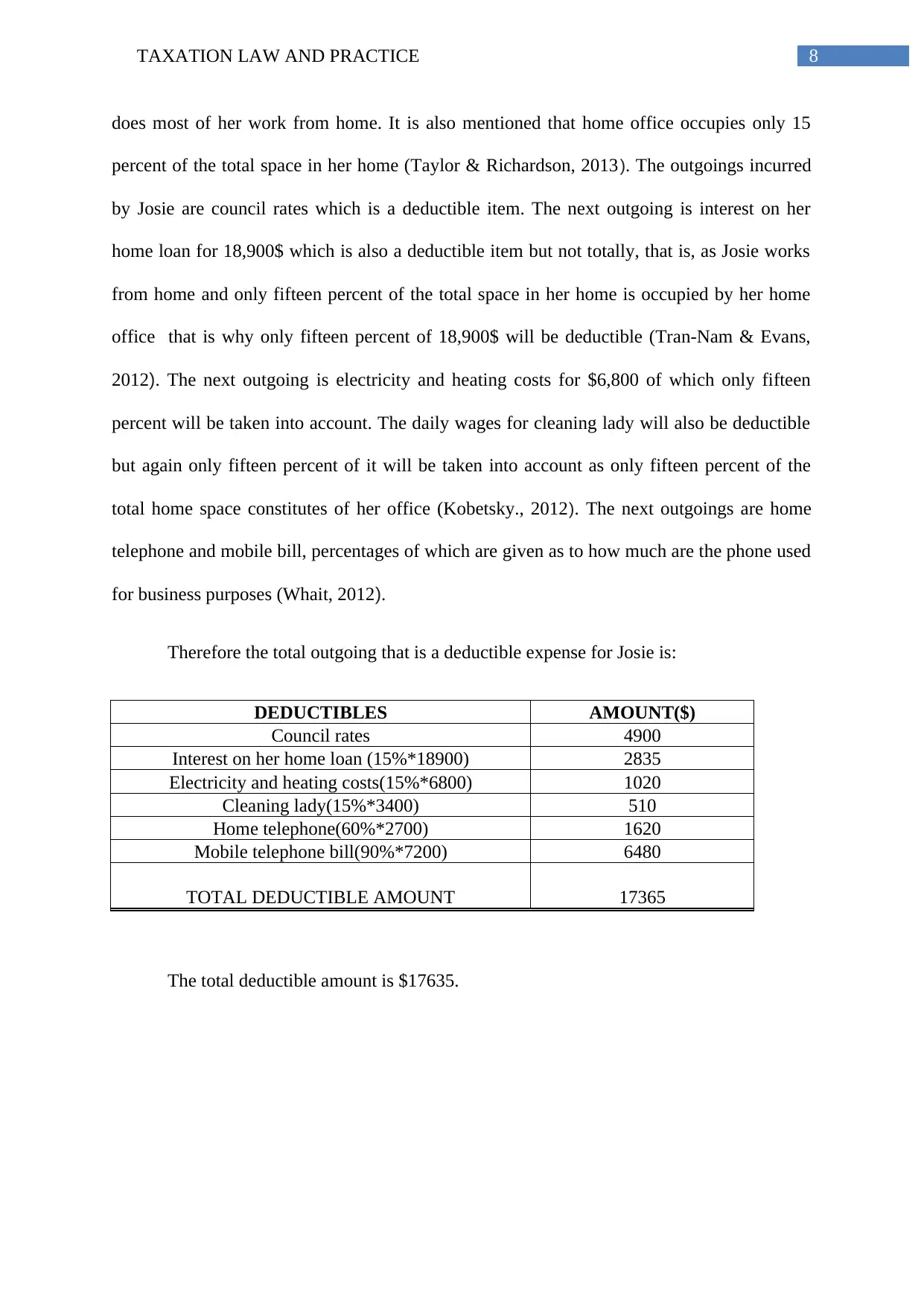

Therefore the total outgoing that is a deductible expense for Josie is:

DEDUCTIBLES AMOUNT($)

Council rates 4900

Interest on her home loan (15%*18900) 2835

Electricity and heating costs(15%*6800) 1020

Cleaning lady(15%*3400) 510

Home telephone(60%*2700) 1620

Mobile telephone bill(90%*7200) 6480

TOTAL DEDUCTIBLE AMOUNT 17365

The total deductible amount is $17635.

does most of her work from home. It is also mentioned that home office occupies only 15

percent of the total space in her home (Taylor & Richardson, 2013). The outgoings incurred

by Josie are council rates which is a deductible item. The next outgoing is interest on her

home loan for 18,900$ which is also a deductible item but not totally, that is, as Josie works

from home and only fifteen percent of the total space in her home is occupied by her home

office that is why only fifteen percent of 18,900$ will be deductible (Tran-Nam & Evans,

2012). The next outgoing is electricity and heating costs for $6,800 of which only fifteen

percent will be taken into account. The daily wages for cleaning lady will also be deductible

but again only fifteen percent of it will be taken into account as only fifteen percent of the

total home space constitutes of her office (Kobetsky., 2012). The next outgoings are home

telephone and mobile bill, percentages of which are given as to how much are the phone used

for business purposes (Whait, 2012).

Therefore the total outgoing that is a deductible expense for Josie is:

DEDUCTIBLES AMOUNT($)

Council rates 4900

Interest on her home loan (15%*18900) 2835

Electricity and heating costs(15%*6800) 1020

Cleaning lady(15%*3400) 510

Home telephone(60%*2700) 1620

Mobile telephone bill(90%*7200) 6480

TOTAL DEDUCTIBLE AMOUNT 17365

The total deductible amount is $17635.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW AND PRACTICE

References:

Boccabella, D. (2012). An ordered approach to the tax rules for problem solving in a first

Australian income taxation law course can improve student performance. eJournal of

Tax Research, 10(3), 621.

Chordia, S., Lynch, A., & Williams, G. (2013). Williams v. Commonwealth: Commonwealth

Executive Power and Australian Federalism. Melb. UL Rev., 37, 189.

De Mooij, R. A. (2012). Tax biases to debt finance: Assessing the problem, finding solutions.

Fiscal Studies, 33(4), 489-512.

Harding, C. (2012). Who is a resident of Australia?. Concise Collection of Tax

Fundamentals, A, 181.

Harding, M. (2013). Taxation of dividend, interest, and capital gain income.

Higgins, T., & Sinning, M. (2013). Modeling income dynamics for public policy design: An

application to income contingent student loans. Economics of Education Review, 37,

273-285.

Kaganovich, M., & Zilcha, I. (2012). Pay-as-you-go or funded social security? A general

equilibrium comparison. Journal of Economic Dynamics and Control, 36(4), 455-467.

Kobetsky, M., O'Connell, A., Brown, C., Fisher, R., & Peacock, C. (2012). Income Tax: Text,

Materials and Essential Cases. The Federation Press.

Mabaso, N. D. (2012). An international comparative study of the effect of personal income

tax on labour migration (Doctoral dissertation).

References:

Boccabella, D. (2012). An ordered approach to the tax rules for problem solving in a first

Australian income taxation law course can improve student performance. eJournal of

Tax Research, 10(3), 621.

Chordia, S., Lynch, A., & Williams, G. (2013). Williams v. Commonwealth: Commonwealth

Executive Power and Australian Federalism. Melb. UL Rev., 37, 189.

De Mooij, R. A. (2012). Tax biases to debt finance: Assessing the problem, finding solutions.

Fiscal Studies, 33(4), 489-512.

Harding, C. (2012). Who is a resident of Australia?. Concise Collection of Tax

Fundamentals, A, 181.

Harding, M. (2013). Taxation of dividend, interest, and capital gain income.

Higgins, T., & Sinning, M. (2013). Modeling income dynamics for public policy design: An

application to income contingent student loans. Economics of Education Review, 37,

273-285.

Kaganovich, M., & Zilcha, I. (2012). Pay-as-you-go or funded social security? A general

equilibrium comparison. Journal of Economic Dynamics and Control, 36(4), 455-467.

Kobetsky, M., O'Connell, A., Brown, C., Fisher, R., & Peacock, C. (2012). Income Tax: Text,

Materials and Essential Cases. The Federation Press.

Mabaso, N. D. (2012). An international comparative study of the effect of personal income

tax on labour migration (Doctoral dissertation).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW AND PRACTICE

Maples, A. J. (2012). A Super Massive Black Hole: The Tax Treatment of Seismic

Strengthening Costs. J. Australasian Tax Tchrs. Ass'n, 7, 123.

Menezes, F. M. (2012). The Business Tax Reform Agenda. Economic Papers: A journal of

applied economics and policy, 31(1), 3-7.

Rahman, A., & Harding, A. (2014). Spatial analysis of housing stress estimation in Australia

with statistical validation. Australasian Journal of Regional Studies, 20(3), 452.

Shaw, A. (2012). 'Tax files: Wherever I lay my hat': That's my place of domicile. Bulletin

(Law Society of South Australia), 34(2), 16.

Taylor, G., & Richardson, G. (2012). International corporate tax avoidance practices:

evidence from Australian firms. The International Journal of Accounting, 47(4), 469-

496.

Taylor, G., & Richardson, G. (2013). The determinants of thinly capitalized tax avoidance

structures: Evidence from Australian firms. Journal of International Accounting,

Auditing and Taxation, 22(1), 12-25.

Taylor, M. (2012). Is it a levy, or is it a tax, or both?. Revenue Law Journal, 22(1), 188.

Tran-Nam, B., & Evans, C. (2012). Tax policy simplification: An evaluation of the proposal

for a standard deduction for work related expenses.

Whait, R. B. (2012). Developing risk management strategies in tax administration: the

evolution of the Australian Taxation Office's compliance model. eJournal of Tax

Research, 10(2), 436.

Maples, A. J. (2012). A Super Massive Black Hole: The Tax Treatment of Seismic

Strengthening Costs. J. Australasian Tax Tchrs. Ass'n, 7, 123.

Menezes, F. M. (2012). The Business Tax Reform Agenda. Economic Papers: A journal of

applied economics and policy, 31(1), 3-7.

Rahman, A., & Harding, A. (2014). Spatial analysis of housing stress estimation in Australia

with statistical validation. Australasian Journal of Regional Studies, 20(3), 452.

Shaw, A. (2012). 'Tax files: Wherever I lay my hat': That's my place of domicile. Bulletin

(Law Society of South Australia), 34(2), 16.

Taylor, G., & Richardson, G. (2012). International corporate tax avoidance practices:

evidence from Australian firms. The International Journal of Accounting, 47(4), 469-

496.

Taylor, G., & Richardson, G. (2013). The determinants of thinly capitalized tax avoidance

structures: Evidence from Australian firms. Journal of International Accounting,

Auditing and Taxation, 22(1), 12-25.

Taylor, M. (2012). Is it a levy, or is it a tax, or both?. Revenue Law Journal, 22(1), 188.

Tran-Nam, B., & Evans, C. (2012). Tax policy simplification: An evaluation of the proposal

for a standard deduction for work related expenses.

Whait, R. B. (2012). Developing risk management strategies in tax administration: the

evolution of the Australian Taxation Office's compliance model. eJournal of Tax

Research, 10(2), 436.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.