LAWS19033 Taxation Law: Comprehensive Analysis of Income Tax

VerifiedAdded on 2023/06/07

|16

|4121

|238

Homework Assignment

AI Summary

This assignment provides a detailed analysis of individual income tax within the Australian legal framework, referencing the Income Tax Assessment Act 1997 and relevant taxation rulings. It addresses key aspects such as the functions of taxation, equity in the tax system, taxable income calculation, and progressive tax systems. The assignment includes case studies involving foreign residents and assesses their tax obligations, along with calculations of assessable income, tax deductions, and payable tax for individuals. Furthermore, it examines the deductibility of asset depreciation and outlines the requirements for starting a new business in Australia, emphasizing compliance with various legal and regulatory standards. This comprehensive overview is intended to provide a clear understanding of the complexities of individual income tax in Australia.

Running head: TAX

Tax

Name of the Student:

Name of the University:

Authors Note:

Tax

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAX

Table of Contents

Answer to Question 1.................................................................................................................2

Answer to Question 2.................................................................................................................3

Answer to Question 3.................................................................................................................5

Answer to Question 4.................................................................................................................7

Answer to Question 5.................................................................................................................8

Answer to Question 6.................................................................................................................9

Reference..................................................................................................................................13

Table of Contents

Answer to Question 1.................................................................................................................2

Answer to Question 2.................................................................................................................3

Answer to Question 3.................................................................................................................5

Answer to Question 4.................................................................................................................7

Answer to Question 5.................................................................................................................8

Answer to Question 6.................................................................................................................9

Reference..................................................................................................................................13

2TAX

Answer to Question 1

a)

The primary functions of taxation in Australia are to administer over the taxes,

superannuation and excise duty in order to affect the revenue system of Australia. Regulating

the aggressive tax planning, persistent tax debtors, globalisation and the cash economy1 is

considered as the primary function of taxation in Australia.

b)

Equity in a good tax system means that everybody irrespective of personnel influence

should pay a fair share of taxes as long as the individual is regarded as the residence of

Australia. The equity can be divided into horizontal equity and vertical equity.

c)

It is required to deduct the taxable deductions from the assessable income in order to

get the taxable income2 in accordance with the section 4/15 of the Income Tax Assessment

Act 1997.

d)

The aim of a progressive tax system is to implement the corresponding effect of

reducing the burden on low income, and to achieve the goal of income equality. Another goal

of a progressive tax system is to provide educational attainment for the families with lower

income in order to increase the opportunity for educational attainment for those families.

e)

The value of allowances in the assessable income is included in the Section 15-2 of

the Income Tax Assessment Act 1997.

1Parker, Hermione. Instead of the Dole: an enquiry into integration of the tax and benefit systems. Routledge,

2018.

2Thayer, Carlyle A., and David G. Marr. Vietnam and the Rule of Law. Canberra, ACT: Dept. of Political and

Social Change, Research School of Pacific and Asian Studies, The Australian National University., 2017.

Answer to Question 1

a)

The primary functions of taxation in Australia are to administer over the taxes,

superannuation and excise duty in order to affect the revenue system of Australia. Regulating

the aggressive tax planning, persistent tax debtors, globalisation and the cash economy1 is

considered as the primary function of taxation in Australia.

b)

Equity in a good tax system means that everybody irrespective of personnel influence

should pay a fair share of taxes as long as the individual is regarded as the residence of

Australia. The equity can be divided into horizontal equity and vertical equity.

c)

It is required to deduct the taxable deductions from the assessable income in order to

get the taxable income2 in accordance with the section 4/15 of the Income Tax Assessment

Act 1997.

d)

The aim of a progressive tax system is to implement the corresponding effect of

reducing the burden on low income, and to achieve the goal of income equality. Another goal

of a progressive tax system is to provide educational attainment for the families with lower

income in order to increase the opportunity for educational attainment for those families.

e)

The value of allowances in the assessable income is included in the Section 15-2 of

the Income Tax Assessment Act 1997.

1Parker, Hermione. Instead of the Dole: an enquiry into integration of the tax and benefit systems. Routledge,

2018.

2Thayer, Carlyle A., and David G. Marr. Vietnam and the Rule of Law. Canberra, ACT: Dept. of Political and

Social Change, Research School of Pacific and Asian Studies, The Australian National University., 2017.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAX

f)

In Taxation Ruling 2004-15, the residential status of the companies that are not

incorporated in Australia is stated. The requirements of carrying on business in Australia and

the duties and structure of the central and control management are also stated in this taxation

ruling3.

g)

The deductions for the capital expenditure are stated in section 40 and section 25-5 of

the Income Tax Assessment Act 1997,

h)

The fixed taxation rate over the taxable income of $37,000 is $3572. After that, 32.5%

will be deducted over the income of $37,000. Therefore, by using this rate, the tax rate for the

taxpayer with an income of $80,000 will be $17,547 in 2017/18.

i)

Section 11-55 lists the provisions that treat amounts as Non Assessable Non Exempt

income as stated in the Income Tax Assessment Act 1997.

j)

According to Tax Determination TD 2017/4, the rate which is applicable for 2500cc

and above motor vehicles is 63 percent.

Answer to Question 2

It is stated in the section 6-5(3) of Income Tax Assessment Act 1997, how a foreign

resident can be eligible and liable for paying the taxes to the Australian Government. In this

case, Martelle has come to Australia from France in order to complete her assignment of

creating colourful designs based on the vibrant colours of the Great Barrier Reef. She is

3Wilkins, Roger. "Measuring income inequality in Australia." Australian Economic Review 48, no. 1 (2015): 93-

102.

f)

In Taxation Ruling 2004-15, the residential status of the companies that are not

incorporated in Australia is stated. The requirements of carrying on business in Australia and

the duties and structure of the central and control management are also stated in this taxation

ruling3.

g)

The deductions for the capital expenditure are stated in section 40 and section 25-5 of

the Income Tax Assessment Act 1997,

h)

The fixed taxation rate over the taxable income of $37,000 is $3572. After that, 32.5%

will be deducted over the income of $37,000. Therefore, by using this rate, the tax rate for the

taxpayer with an income of $80,000 will be $17,547 in 2017/18.

i)

Section 11-55 lists the provisions that treat amounts as Non Assessable Non Exempt

income as stated in the Income Tax Assessment Act 1997.

j)

According to Tax Determination TD 2017/4, the rate which is applicable for 2500cc

and above motor vehicles is 63 percent.

Answer to Question 2

It is stated in the section 6-5(3) of Income Tax Assessment Act 1997, how a foreign

resident can be eligible and liable for paying the taxes to the Australian Government. In this

case, Martelle has come to Australia from France in order to complete her assignment of

creating colourful designs based on the vibrant colours of the Great Barrier Reef. She is

3Wilkins, Roger. "Measuring income inequality in Australia." Australian Economic Review 48, no. 1 (2015): 93-

102.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAX

expected to stay in the country for six and a half months. The salary of Martelle is paid to an

Australian bank4. Apart from the income that Martelle is getting from here, she has also

rented a boat for her personnel use.

According to section 6-5, there are four methods of deciding the residential status of

any individual living in Australia, which are, ordinary concepts, domicile test, 183-day test

and superannuation test. The legislation that is most relevant for Martelle is the 183-day test.

According to this legislation, if a person whose permanent residential status is outside of

Australia, will be considered as the resident of Australia if the person is living in this country

for more than 6 months and there is some taxable earning that the person is getting from

here. As the contract of Martelle has exceeded the time period of 6 months, she will surely be

regarded as the resident of Australia for the whole year. The income of Martelle will be

considered as taxable if she has managed to gain an assessable income of over $18,200. This

assessable income will be considered as a total of the ordinary income and statutory income

of Martelle. The income that is being generated from her properties and investments in

France will not be included in the taxable income of Australian legislation as only the

permanent residents of Australia needs to pay taxes even if they earn the income from outside

of Australia. As Martelle has a permanent domicile of France, she is not liable to pay taxes

for her properties in France5. As of her properties in Australia, the boat and the residential

place of Martelle will also not be included for taxation as these are not the sources of income

for Martelle.

Answer to Question 3

As far as the transaction gained by Ellen for the fiscal year 2017-18 is concerned, the

deductibility of tax needs to be decided under the Income Tax Assessment Act 1997

4Braithwaite, Valerie. Taxing democracy: Understanding tax avoidance and evasion. Routledge, 2017.

5Basu, Subhajit. Global perspectives on e-commerce taxation law. Routledge, 2016.

expected to stay in the country for six and a half months. The salary of Martelle is paid to an

Australian bank4. Apart from the income that Martelle is getting from here, she has also

rented a boat for her personnel use.

According to section 6-5, there are four methods of deciding the residential status of

any individual living in Australia, which are, ordinary concepts, domicile test, 183-day test

and superannuation test. The legislation that is most relevant for Martelle is the 183-day test.

According to this legislation, if a person whose permanent residential status is outside of

Australia, will be considered as the resident of Australia if the person is living in this country

for more than 6 months and there is some taxable earning that the person is getting from

here. As the contract of Martelle has exceeded the time period of 6 months, she will surely be

regarded as the resident of Australia for the whole year. The income of Martelle will be

considered as taxable if she has managed to gain an assessable income of over $18,200. This

assessable income will be considered as a total of the ordinary income and statutory income

of Martelle. The income that is being generated from her properties and investments in

France will not be included in the taxable income of Australian legislation as only the

permanent residents of Australia needs to pay taxes even if they earn the income from outside

of Australia. As Martelle has a permanent domicile of France, she is not liable to pay taxes

for her properties in France5. As of her properties in Australia, the boat and the residential

place of Martelle will also not be included for taxation as these are not the sources of income

for Martelle.

Answer to Question 3

As far as the transaction gained by Ellen for the fiscal year 2017-18 is concerned, the

deductibility of tax needs to be decided under the Income Tax Assessment Act 1997

4Braithwaite, Valerie. Taxing democracy: Understanding tax avoidance and evasion. Routledge, 2017.

5Basu, Subhajit. Global perspectives on e-commerce taxation law. Routledge, 2016.

5TAX

provisions. In section, 15-17 of the act the assessable income of an individual is stated. In

accordance with this legislation, the salary of Ellen will be regarded as taxable income and

thus the annual salary of Ellen will be regarded as the taxable income as a whole of $10800.

In the section 6-5 of ITAA 1997, the provision about the incomes according to the ordinary

concept is discussed. According to this provision, the bank interest, prize winnings and

termination contracts for Ellen will be included in this section6. The total amount of income

according to the ordinary concept for Ellen is $16925. Thus it can be said that the total

amount of Assessable income for Ellen is $124925.

The payable tax is calculated by deducting the tax deductions from the assessable

income in accordance the Income Tax Assessment Act 1997. It is stated in the previous

paragraph that the assessable income of Ellen is $124925 for the fiscal year 2017-18. The tax

deduction amount for Ellen is calculated as $of Ellen is $124925 for the fiscal year 2017-18.

The tax deduction amount for Ellen is calculated as $500 as a cost of the health insurance of

Ellen. Thus the taxable amount for Ellen is $124425. The static rate of taxation for earning

over $18,200 is $3572. For earning over $37,000, additional rate of 32.5% will be included in

the payable tax amount7. The total additional rate of this is measured as $16249.68 as

measured from the amount calculated for the taxation. For earning over $87,000, a tax will be

deducted with a rate of 37% from the total taxable amount. Thus the amount calculated for

Ellen is $13847.25 in this present year. So far as, the total tax which will be deducted from

the total income of Ellen is $33668.93 as per stated in the legislations related to taxation of

Australia.

Calculation of the Income for Ellen

6Thayer, Carlyle A., and David G. Marr. Vietnam and the Rule of Law. Canberra, ACT: Dept. of Political and

Social Change, Research School of Pacific and Asian Studies, The Australian National University., 2017.

7Endres, Dieter, and ChristophSpengel, eds. International company taxation and tax planning. Alphen aanDen

Rijn: Kluwer Law International, 2015.

provisions. In section, 15-17 of the act the assessable income of an individual is stated. In

accordance with this legislation, the salary of Ellen will be regarded as taxable income and

thus the annual salary of Ellen will be regarded as the taxable income as a whole of $10800.

In the section 6-5 of ITAA 1997, the provision about the incomes according to the ordinary

concept is discussed. According to this provision, the bank interest, prize winnings and

termination contracts for Ellen will be included in this section6. The total amount of income

according to the ordinary concept for Ellen is $16925. Thus it can be said that the total

amount of Assessable income for Ellen is $124925.

The payable tax is calculated by deducting the tax deductions from the assessable

income in accordance the Income Tax Assessment Act 1997. It is stated in the previous

paragraph that the assessable income of Ellen is $124925 for the fiscal year 2017-18. The tax

deduction amount for Ellen is calculated as $of Ellen is $124925 for the fiscal year 2017-18.

The tax deduction amount for Ellen is calculated as $500 as a cost of the health insurance of

Ellen. Thus the taxable amount for Ellen is $124425. The static rate of taxation for earning

over $18,200 is $3572. For earning over $37,000, additional rate of 32.5% will be included in

the payable tax amount7. The total additional rate of this is measured as $16249.68 as

measured from the amount calculated for the taxation. For earning over $87,000, a tax will be

deducted with a rate of 37% from the total taxable amount. Thus the amount calculated for

Ellen is $13847.25 in this present year. So far as, the total tax which will be deducted from

the total income of Ellen is $33668.93 as per stated in the legislations related to taxation of

Australia.

Calculation of the Income for Ellen

6Thayer, Carlyle A., and David G. Marr. Vietnam and the Rule of Law. Canberra, ACT: Dept. of Political and

Social Change, Research School of Pacific and Asian Studies, The Australian National University., 2017.

7Endres, Dieter, and ChristophSpengel, eds. International company taxation and tax planning. Alphen aanDen

Rijn: Kluwer Law International, 2015.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAX

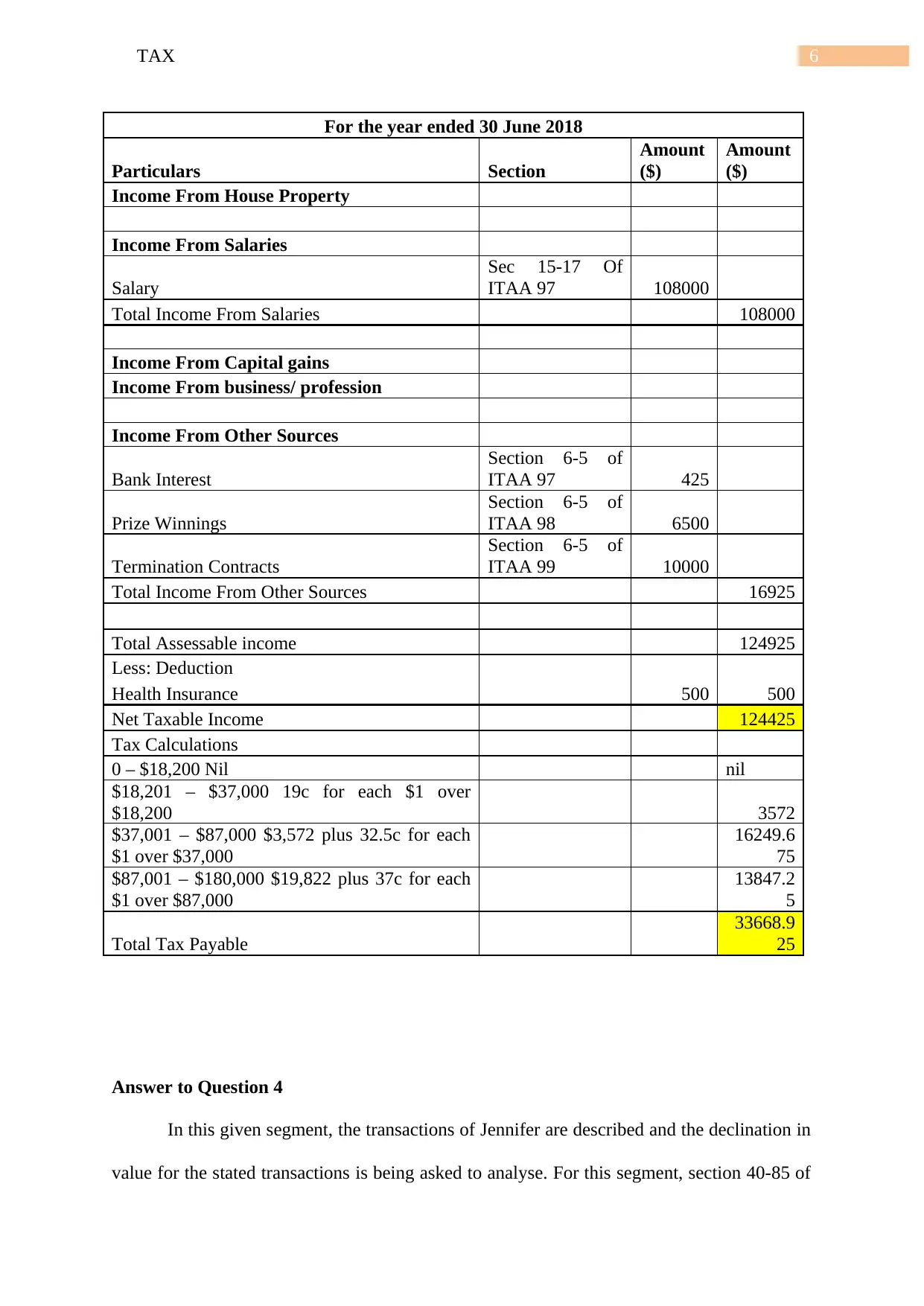

For the year ended 30 June 2018

Particulars Section

Amount

($)

Amount

($)

Income From House Property

Income From Salaries

Salary

Sec 15-17 Of

ITAA 97 108000

Total Income From Salaries 108000

Income From Capital gains

Income From business/ profession

Income From Other Sources

Bank Interest

Section 6-5 of

ITAA 97 425

Prize Winnings

Section 6-5 of

ITAA 98 6500

Termination Contracts

Section 6-5 of

ITAA 99 10000

Total Income From Other Sources 16925

Total Assessable income 124925

Less: Deduction

Health Insurance 500 500

Net Taxable Income 124425

Tax Calculations

0 – $18,200 Nil nil

$18,201 – $37,000 19c for each $1 over

$18,200 3572

$37,001 – $87,000 $3,572 plus 32.5c for each

$1 over $37,000

16249.6

75

$87,001 – $180,000 $19,822 plus 37c for each

$1 over $87,000

13847.2

5

Total Tax Payable

33668.9

25

Answer to Question 4

In this given segment, the transactions of Jennifer are described and the declination in

value for the stated transactions is being asked to analyse. For this segment, section 40-85 of

For the year ended 30 June 2018

Particulars Section

Amount

($)

Amount

($)

Income From House Property

Income From Salaries

Salary

Sec 15-17 Of

ITAA 97 108000

Total Income From Salaries 108000

Income From Capital gains

Income From business/ profession

Income From Other Sources

Bank Interest

Section 6-5 of

ITAA 97 425

Prize Winnings

Section 6-5 of

ITAA 98 6500

Termination Contracts

Section 6-5 of

ITAA 99 10000

Total Income From Other Sources 16925

Total Assessable income 124925

Less: Deduction

Health Insurance 500 500

Net Taxable Income 124425

Tax Calculations

0 – $18,200 Nil nil

$18,201 – $37,000 19c for each $1 over

$18,200 3572

$37,001 – $87,000 $3,572 plus 32.5c for each

$1 over $37,000

16249.6

75

$87,001 – $180,000 $19,822 plus 37c for each

$1 over $87,000

13847.2

5

Total Tax Payable

33668.9

25

Answer to Question 4

In this given segment, the transactions of Jennifer are described and the declination in

value for the stated transactions is being asked to analyse. For this segment, section 40-85 of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAX

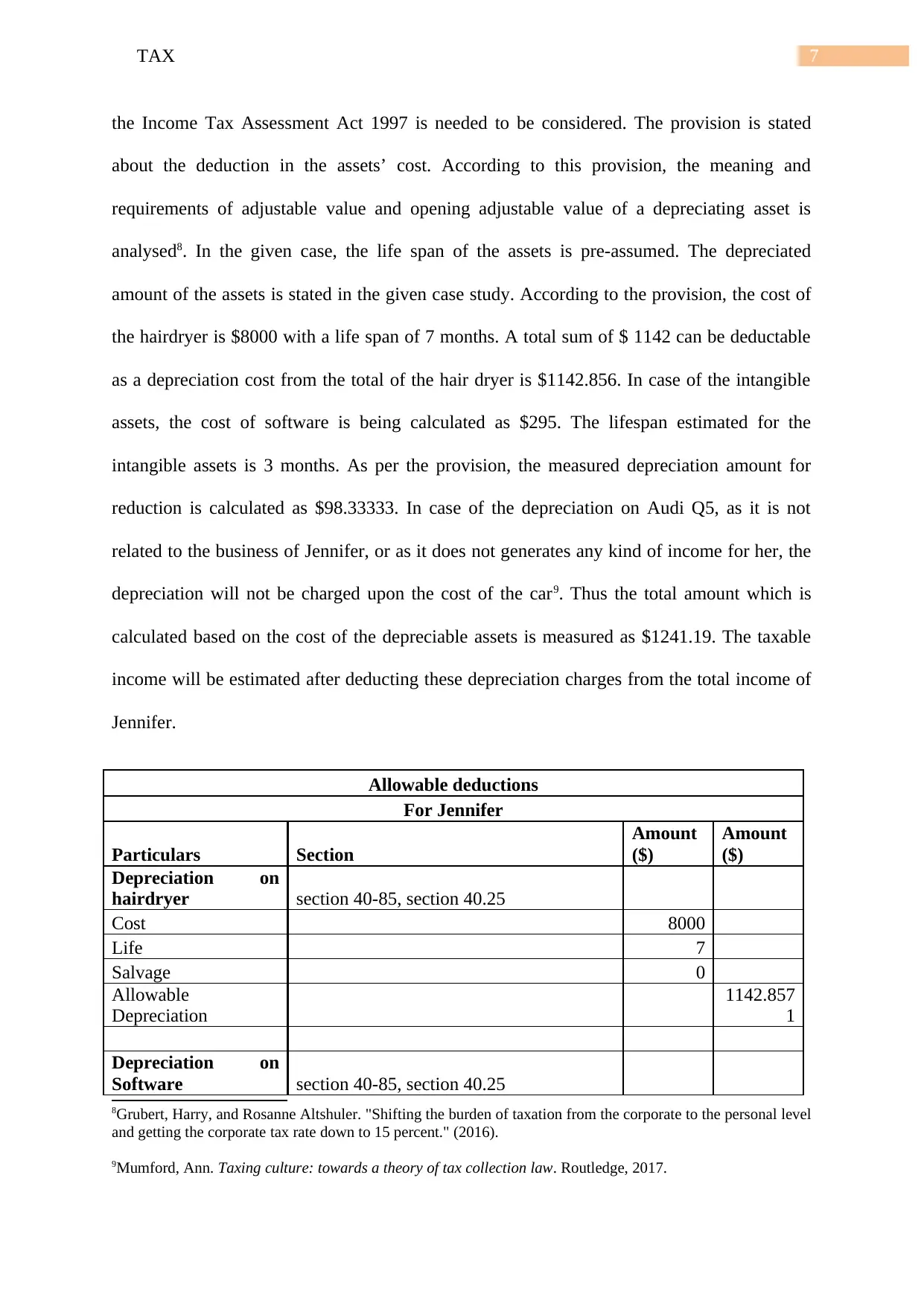

the Income Tax Assessment Act 1997 is needed to be considered. The provision is stated

about the deduction in the assets’ cost. According to this provision, the meaning and

requirements of adjustable value and opening adjustable value of a depreciating asset is

analysed8. In the given case, the life span of the assets is pre-assumed. The depreciated

amount of the assets is stated in the given case study. According to the provision, the cost of

the hairdryer is $8000 with a life span of 7 months. A total sum of $ 1142 can be deductable

as a depreciation cost from the total of the hair dryer is $1142.856. In case of the intangible

assets, the cost of software is being calculated as $295. The lifespan estimated for the

intangible assets is 3 months. As per the provision, the measured depreciation amount for

reduction is calculated as $98.33333. In case of the depreciation on Audi Q5, as it is not

related to the business of Jennifer, or as it does not generates any kind of income for her, the

depreciation will not be charged upon the cost of the car9. Thus the total amount which is

calculated based on the cost of the depreciable assets is measured as $1241.19. The taxable

income will be estimated after deducting these depreciation charges from the total income of

Jennifer.

Allowable deductions

For Jennifer

Particulars Section

Amount

($)

Amount

($)

Depreciation on

hairdryer section 40-85, section 40.25

Cost 8000

Life 7

Salvage 0

Allowable

Depreciation

1142.857

1

Depreciation on

Software section 40-85, section 40.25

8Grubert, Harry, and Rosanne Altshuler. "Shifting the burden of taxation from the corporate to the personal level

and getting the corporate tax rate down to 15 percent." (2016).

9Mumford, Ann. Taxing culture: towards a theory of tax collection law. Routledge, 2017.

the Income Tax Assessment Act 1997 is needed to be considered. The provision is stated

about the deduction in the assets’ cost. According to this provision, the meaning and

requirements of adjustable value and opening adjustable value of a depreciating asset is

analysed8. In the given case, the life span of the assets is pre-assumed. The depreciated

amount of the assets is stated in the given case study. According to the provision, the cost of

the hairdryer is $8000 with a life span of 7 months. A total sum of $ 1142 can be deductable

as a depreciation cost from the total of the hair dryer is $1142.856. In case of the intangible

assets, the cost of software is being calculated as $295. The lifespan estimated for the

intangible assets is 3 months. As per the provision, the measured depreciation amount for

reduction is calculated as $98.33333. In case of the depreciation on Audi Q5, as it is not

related to the business of Jennifer, or as it does not generates any kind of income for her, the

depreciation will not be charged upon the cost of the car9. Thus the total amount which is

calculated based on the cost of the depreciable assets is measured as $1241.19. The taxable

income will be estimated after deducting these depreciation charges from the total income of

Jennifer.

Allowable deductions

For Jennifer

Particulars Section

Amount

($)

Amount

($)

Depreciation on

hairdryer section 40-85, section 40.25

Cost 8000

Life 7

Salvage 0

Allowable

Depreciation

1142.857

1

Depreciation on

Software section 40-85, section 40.25

8Grubert, Harry, and Rosanne Altshuler. "Shifting the burden of taxation from the corporate to the personal level

and getting the corporate tax rate down to 15 percent." (2016).

9Mumford, Ann. Taxing culture: towards a theory of tax collection law. Routledge, 2017.

8TAX

Cost 295

Life 3

Salvage 0

Allowable

Depreciation

98.33333

3

Depreciation on

Audi Q5

section 40-85, section 40.25 ( not related

to business)

Cost 85000

Life 6

Salvage 0

Allowable

Depreciation 0

Total allowable

Deductions

1241.190

5

Answer to Question 5

Julie, an enthusiastic photographer is willing to start her own business in Australia. As

photography was her hobby, she does not know much about the provisions which are needed

to be considered in order to start a new business in Australia. Certain criteria needed to be

followed in order to start the business in accordance with the legislations of Australia. At

first, the business structure and the trademark of the business need to be decided. It is

required for Julie to registere for Australian Business Number, Pay as you go withholding,

Tax File Number and Goods and Service tax10. The proper preparation for tax is also required

in order to carry on the business. The legislations which are required for starting a fair trade

in Australia are Australian standards, Australian Consumer Law, Fair Trading Laws,

Competition and Consumer Act, and codes of practice. For selling a certain service,

following legislations are needed to be considered, such as pricing regulations, displaying

prices, warranties and refunds, Australian trade measurement laws, , product labelling, and

selling goods and services. The privacy act, contract act and anti bullying laws are also

10Dixon, J. M., and Jason Nassios. Modelling the impacts of a cut to company tax in Australia. Centre for Policy

Studies, Victoria University, 2016.

Cost 295

Life 3

Salvage 0

Allowable

Depreciation

98.33333

3

Depreciation on

Audi Q5

section 40-85, section 40.25 ( not related

to business)

Cost 85000

Life 6

Salvage 0

Allowable

Depreciation 0

Total allowable

Deductions

1241.190

5

Answer to Question 5

Julie, an enthusiastic photographer is willing to start her own business in Australia. As

photography was her hobby, she does not know much about the provisions which are needed

to be considered in order to start a new business in Australia. Certain criteria needed to be

followed in order to start the business in accordance with the legislations of Australia. At

first, the business structure and the trademark of the business need to be decided. It is

required for Julie to registere for Australian Business Number, Pay as you go withholding,

Tax File Number and Goods and Service tax10. The proper preparation for tax is also required

in order to carry on the business. The legislations which are required for starting a fair trade

in Australia are Australian standards, Australian Consumer Law, Fair Trading Laws,

Competition and Consumer Act, and codes of practice. For selling a certain service,

following legislations are needed to be considered, such as pricing regulations, displaying

prices, warranties and refunds, Australian trade measurement laws, , product labelling, and

selling goods and services. The privacy act, contract act and anti bullying laws are also

10Dixon, J. M., and Jason Nassios. Modelling the impacts of a cut to company tax in Australia. Centre for Policy

Studies, Victoria University, 2016.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAX

essential for the proper interpretation by Australian Taxation Office11. There are legal

obligations of marketing which is also needed to be considered before starting a business.

Proper financial plans in accordance with the legislations of ATO are also required. Security

and insurance of the business can also be helpful for Julie to start with.

Answer to Question 6

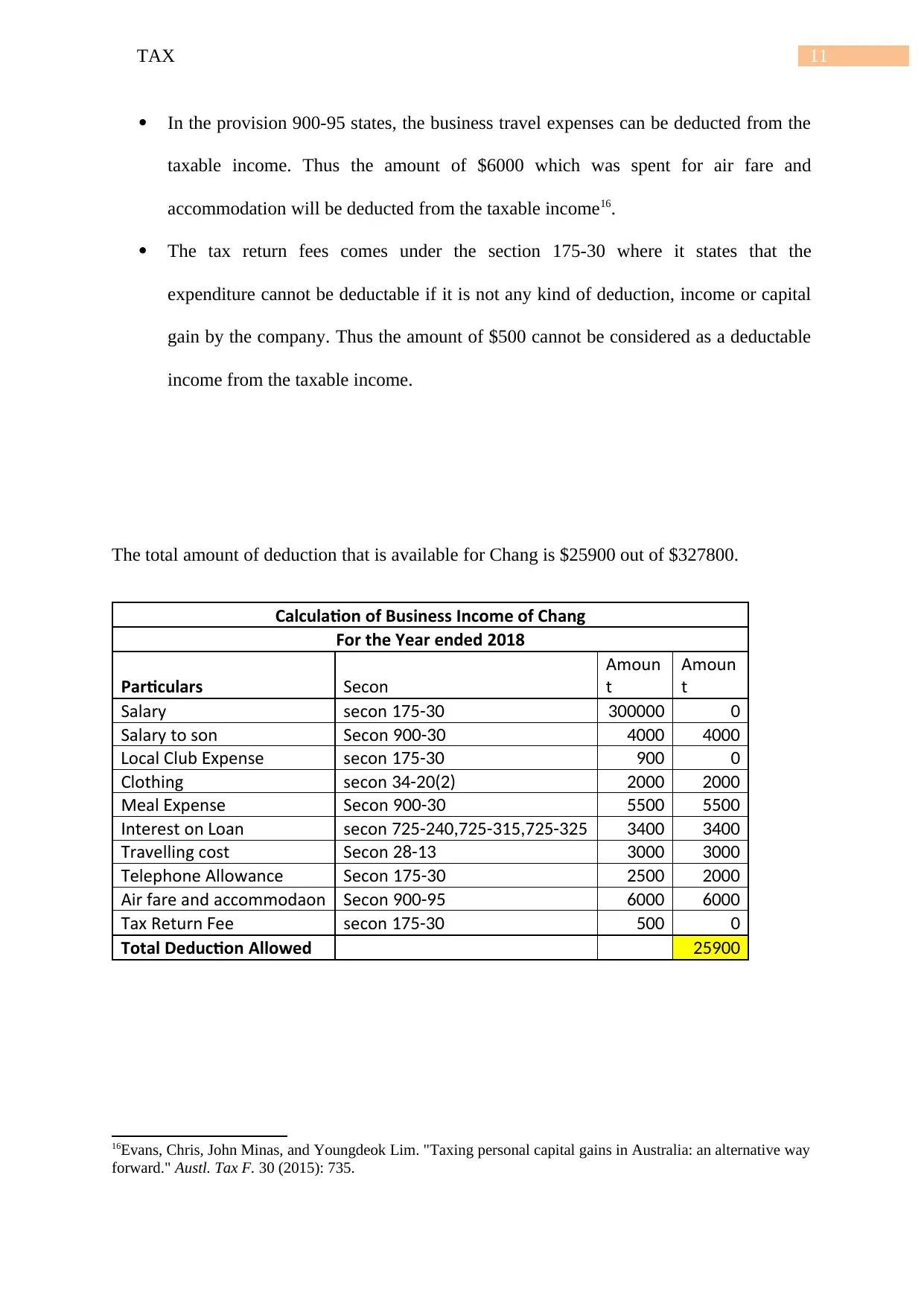

In the given case, Chang runs a marketing business. Some of the transactions occurred

in the current financial year has been given in order to evaluate the possible deductibility of

the expenses over the taxability of the overall amount. Thus the amounts that are likely to be

deductable is given below:

According to section 175-30, an amount cannot be deducted unless it is not regarded

as an income or capital gain which is incurred by someone else. Thus, the salary

earned by Chang cannot be deducted and thus, the whole amount of the salary will be

included in the measurement of taxable income12.

For the next transaction, Chang has paid a sum of $4000 to his son for doing some

graphic designing for him. This particular case comes under the section 900-30 where

the work expenses have been described. According to this legislation, a work expense

is a loss or an outgoing from the income and it is deductable for taxation. Thus the

total amount given by Chang to his son will be totally deducted from the payable tax.

According to the section 175-30, an individual can gain a benefit of tax deduction if

there is any kind of deduction, income or capital gain available to the company. But in

the given case, the expenses cannot be considered as any of such criteria. Thus the

local club expenses cannot be deducted from the taxable income.

11Davis, Angela K., David A. Guenther, Linda K. Krull, and Brian M. Williams. "Do socially responsible firms

pay more taxes?." The accounting review 91, no. 1 (2015): 47-68.

12Emery, Joel. "Decoding the regulatory enigma: how Australian regulators should respond to the tax challenges

presented by bitcoin." (2016).

essential for the proper interpretation by Australian Taxation Office11. There are legal

obligations of marketing which is also needed to be considered before starting a business.

Proper financial plans in accordance with the legislations of ATO are also required. Security

and insurance of the business can also be helpful for Julie to start with.

Answer to Question 6

In the given case, Chang runs a marketing business. Some of the transactions occurred

in the current financial year has been given in order to evaluate the possible deductibility of

the expenses over the taxability of the overall amount. Thus the amounts that are likely to be

deductable is given below:

According to section 175-30, an amount cannot be deducted unless it is not regarded

as an income or capital gain which is incurred by someone else. Thus, the salary

earned by Chang cannot be deducted and thus, the whole amount of the salary will be

included in the measurement of taxable income12.

For the next transaction, Chang has paid a sum of $4000 to his son for doing some

graphic designing for him. This particular case comes under the section 900-30 where

the work expenses have been described. According to this legislation, a work expense

is a loss or an outgoing from the income and it is deductable for taxation. Thus the

total amount given by Chang to his son will be totally deducted from the payable tax.

According to the section 175-30, an individual can gain a benefit of tax deduction if

there is any kind of deduction, income or capital gain available to the company. But in

the given case, the expenses cannot be considered as any of such criteria. Thus the

local club expenses cannot be deducted from the taxable income.

11Davis, Angela K., David A. Guenther, Linda K. Krull, and Brian M. Williams. "Do socially responsible firms

pay more taxes?." The accounting review 91, no. 1 (2015): 47-68.

12Emery, Joel. "Decoding the regulatory enigma: how Australian regulators should respond to the tax challenges

presented by bitcoin." (2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAX

According to the section 34-20, if there is any expenditure made for purchasing the

occupation specific clothing, the amount can be deductable from the taxable income.

Thus, the amount spent for purchasing the cloths will be deducted from the taxable

income of Chang13.

The expenses made by Chang for buying meal comes under section 900-30 of ITAA

1997 where it is stated that if any work expenses is spent as a loss or outgoing from

the income of an individual, the amount spent will be deducted from the taxable

income14. Thus amount $5500 will be deducted from the taxable income of Chang.

According to the provisions stated in 725-315 and 725-325, the interest on loan will

be deducted from the taxable income as it would be measured upon its adjustable

value. Thus the amount of $3400 given for the interest on loan will be deducted from

the taxable income.

In accordance with the section 28-13 of IITA 1997, the car expenses can be regarded

as deductable taxation income. The travelling cost made by Chang can be deductable

from the taxable income and $3000 will be reduced15.

The telephone allowances can be considered under section 175-30 where it states, an

individual can gain a benefit of tax deduction if there is any kind of deduction, income

or capital gain available to the company. According to this provision, the allowances

spent can be regarded as a capital deduction from the business and thus it can be

deducted from the taxable income.

13Schenk, Alan, Victor Thuronyi, and Wei Cui. Value added tax. Cambridge University Press, 2015.

14Schneider, Friedrich. "Size and development of the shadow economy of 31 European and 5 other OECD

countries from 2003 to 2014: different developments?." Journal of Self-Governance & Management

Economics 3, no. 4 (2015).

15Dowling, Grahame R. "The curious case of corporate tax avoidance: Is it socially irresponsible?." Journal of

Business Ethics 124, no. 1 (2014): 173-184.

According to the section 34-20, if there is any expenditure made for purchasing the

occupation specific clothing, the amount can be deductable from the taxable income.

Thus, the amount spent for purchasing the cloths will be deducted from the taxable

income of Chang13.

The expenses made by Chang for buying meal comes under section 900-30 of ITAA

1997 where it is stated that if any work expenses is spent as a loss or outgoing from

the income of an individual, the amount spent will be deducted from the taxable

income14. Thus amount $5500 will be deducted from the taxable income of Chang.

According to the provisions stated in 725-315 and 725-325, the interest on loan will

be deducted from the taxable income as it would be measured upon its adjustable

value. Thus the amount of $3400 given for the interest on loan will be deducted from

the taxable income.

In accordance with the section 28-13 of IITA 1997, the car expenses can be regarded

as deductable taxation income. The travelling cost made by Chang can be deductable

from the taxable income and $3000 will be reduced15.

The telephone allowances can be considered under section 175-30 where it states, an

individual can gain a benefit of tax deduction if there is any kind of deduction, income

or capital gain available to the company. According to this provision, the allowances

spent can be regarded as a capital deduction from the business and thus it can be

deducted from the taxable income.

13Schenk, Alan, Victor Thuronyi, and Wei Cui. Value added tax. Cambridge University Press, 2015.

14Schneider, Friedrich. "Size and development of the shadow economy of 31 European and 5 other OECD

countries from 2003 to 2014: different developments?." Journal of Self-Governance & Management

Economics 3, no. 4 (2015).

15Dowling, Grahame R. "The curious case of corporate tax avoidance: Is it socially irresponsible?." Journal of

Business Ethics 124, no. 1 (2014): 173-184.

11TAX

In the provision 900-95 states, the business travel expenses can be deducted from the

taxable income. Thus the amount of $6000 which was spent for air fare and

accommodation will be deducted from the taxable income16.

The tax return fees comes under the section 175-30 where it states that the

expenditure cannot be deductable if it is not any kind of deduction, income or capital

gain by the company. Thus the amount of $500 cannot be considered as a deductable

income from the taxable income.

The total amount of deduction that is available for Chang is $25900 out of $327800.

Calculation of Business Income of Chang

For the Year ended 2018

Particulars Section

Amoun

t

Amoun

t

Salary section 175-30 300000 0

Salary to son Section 900-30 4000 4000

ocal Club penseL Ex section 175-30 900 0

Clothing section 34-20(2) 2000 2000

Meal penseEx Section 900-30 5500 5500

nterest on oanI L section 725-240,725-315,725-325 3400 3400

ravelling costT Section 28-13 3000 3000

elephone AllowanceT Section 175-30 2500 2000

Air fare and accommodation Section 900-95 6000 6000

a Return eeT x F section 175-30 500 0

Total Deduction Allowed 25900

16Evans, Chris, John Minas, and Youngdeok Lim. "Taxing personal capital gains in Australia: an alternative way

forward." Austl. Tax F. 30 (2015): 735.

In the provision 900-95 states, the business travel expenses can be deducted from the

taxable income. Thus the amount of $6000 which was spent for air fare and

accommodation will be deducted from the taxable income16.

The tax return fees comes under the section 175-30 where it states that the

expenditure cannot be deductable if it is not any kind of deduction, income or capital

gain by the company. Thus the amount of $500 cannot be considered as a deductable

income from the taxable income.

The total amount of deduction that is available for Chang is $25900 out of $327800.

Calculation of Business Income of Chang

For the Year ended 2018

Particulars Section

Amoun

t

Amoun

t

Salary section 175-30 300000 0

Salary to son Section 900-30 4000 4000

ocal Club penseL Ex section 175-30 900 0

Clothing section 34-20(2) 2000 2000

Meal penseEx Section 900-30 5500 5500

nterest on oanI L section 725-240,725-315,725-325 3400 3400

ravelling costT Section 28-13 3000 3000

elephone AllowanceT Section 175-30 2500 2000

Air fare and accommodation Section 900-95 6000 6000

a Return eeT x F section 175-30 500 0

Total Deduction Allowed 25900

16Evans, Chris, John Minas, and Youngdeok Lim. "Taxing personal capital gains in Australia: an alternative way

forward." Austl. Tax F. 30 (2015): 735.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.