Taxation Law Assignment: Exploring Australian Taxation Laws

VerifiedAdded on 2021/06/17

|17

|3460

|86

Homework Assignment

AI Summary

This Taxation Law assignment provides comprehensive answers to several key questions. The assignment begins by outlining the main functions of taxation in Australia, the principles of equity in a good tax system, and the process of calculating taxable income. It delves into progressive tax systems and the inclusion of allowances in assessable income. The assignment then addresses residency status in Australia, exploring how an individual's behavior, intentions, and connections influence their residency status. It also examines what constitutes assessable income, including income from personal exertion, prize winnings, and the treatment of restrictive covenants. Furthermore, it analyzes the tax implications of private health insurance rebates. The assignment then covers depreciation deductions, comparing diminishing value and prime cost methods. Finally, it discusses the distinction between a hobby and a business in the context of photography and taxation. This assignment provides a thorough overview of various aspects of Australian taxation law.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer A:..............................................................................................................................2

Answer B:...............................................................................................................................2

Answer C:...............................................................................................................................2

Answer D:..............................................................................................................................3

Answer E:...............................................................................................................................3

Answer F:...............................................................................................................................3

Answer G:..............................................................................................................................4

Answer H:..............................................................................................................................4

Answer I:................................................................................................................................4

Answer J:................................................................................................................................4

Answer to question 2:.................................................................................................................4

Answer to question 3:.................................................................................................................6

Answer to question 4:.................................................................................................................8

Answer to question 5:...............................................................................................................10

Answer to question 6:...............................................................................................................11

References:...............................................................................................................................15

Table of Contents

Answer to question 1:.................................................................................................................2

Answer A:..............................................................................................................................2

Answer B:...............................................................................................................................2

Answer C:...............................................................................................................................2

Answer D:..............................................................................................................................3

Answer E:...............................................................................................................................3

Answer F:...............................................................................................................................3

Answer G:..............................................................................................................................4

Answer H:..............................................................................................................................4

Answer I:................................................................................................................................4

Answer J:................................................................................................................................4

Answer to question 2:.................................................................................................................4

Answer to question 3:.................................................................................................................6

Answer to question 4:.................................................................................................................8

Answer to question 5:...............................................................................................................10

Answer to question 6:...............................................................................................................11

References:...............................................................................................................................15

2TAXATION LAW

Answer to question 1:

Answer A:

The main functions of taxation in Australia is to administer and shape the taxation,

excise and superannuation system that helps in funding the services for the Australians,

providing effects to the social and economic policy1. The main functions of taxation in

Australia is to manage the legislations for taxation, superannuation and excise. By doing this

the taxation system addresses the wide issues that impacts the revenue system of Australia.

Answer B:

While designing the good tax system equity consists of distributing the burden of

taxation fairly among the populations. The principles of equity consists of two basic elements

namely the horizontal and vertical equity2. Horizontal equity represents that the taxpayers

must pay the similar amount of tax while vertical equity represents that taxpayers that are in

different position must pay different sum of tax.

Answer C:

“Section 4-15” requires an individual to work out their assessable income during the

income year

Taxable Income = Assessable Income – Deductions

Step 1 – The taxpayer should add up all the taxable income for the income year

Step 2 – The taxpayer must add the deduction for the income year

1 Barkoczy, Stephen, Australian Tax Casebook 2018 14E Ebook (OUPANZ, 2018)

2 Oishi, Shigehiro, Kostadin Kushlev, and Ulrich Schimmack. "Progressive taxation, income

inequality, and happiness." American Psychologist 73.2 (2018): 157.

Answer to question 1:

Answer A:

The main functions of taxation in Australia is to administer and shape the taxation,

excise and superannuation system that helps in funding the services for the Australians,

providing effects to the social and economic policy1. The main functions of taxation in

Australia is to manage the legislations for taxation, superannuation and excise. By doing this

the taxation system addresses the wide issues that impacts the revenue system of Australia.

Answer B:

While designing the good tax system equity consists of distributing the burden of

taxation fairly among the populations. The principles of equity consists of two basic elements

namely the horizontal and vertical equity2. Horizontal equity represents that the taxpayers

must pay the similar amount of tax while vertical equity represents that taxpayers that are in

different position must pay different sum of tax.

Answer C:

“Section 4-15” requires an individual to work out their assessable income during the

income year

Taxable Income = Assessable Income – Deductions

Step 1 – The taxpayer should add up all the taxable income for the income year

Step 2 – The taxpayer must add the deduction for the income year

1 Barkoczy, Stephen, Australian Tax Casebook 2018 14E Ebook (OUPANZ, 2018)

2 Oishi, Shigehiro, Kostadin Kushlev, and Ulrich Schimmack. "Progressive taxation, income

inequality, and happiness." American Psychologist 73.2 (2018): 157.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Step 3 – The taxpayer should subtract from the taxable income the total deductions to get the

taxable income3.

Answer D:

A progressive tax refers to the rate which increases the assessable value. It is

generally segmented in the tax brackets that progress successively into the higher rates.

Progressive tax system aims in achieving stronger purchasing power. Under this tax system

the demand for certain commodities are either subsidized or a portion of the basic

commodities are increased. Progressive tax system aims in promoting growth and

development in those areas which could have been difficult without the intervention of

government.

Answer E:

“Section 15-2 of the ITAA 1997” includes the value of the allowances into the

assessable income.

Answer F:

The “taxation ruling of TR 2004/15” provides guidance in ascertaining whether the

company that is not incorporated in Australia will be considered as the Australian occupant

under the second statutory test of the meaning of “Resident of Australia” stated in

“subsection 6(1) of the ITAA 1936”4.

3 Grange, Janet, Geralyn A Jover-Ledesma and Gary L Maydew, 2014 Principles Of Business

Taxation

4 James, Simon, The Economics Of Taxation 2014

Step 3 – The taxpayer should subtract from the taxable income the total deductions to get the

taxable income3.

Answer D:

A progressive tax refers to the rate which increases the assessable value. It is

generally segmented in the tax brackets that progress successively into the higher rates.

Progressive tax system aims in achieving stronger purchasing power. Under this tax system

the demand for certain commodities are either subsidized or a portion of the basic

commodities are increased. Progressive tax system aims in promoting growth and

development in those areas which could have been difficult without the intervention of

government.

Answer E:

“Section 15-2 of the ITAA 1997” includes the value of the allowances into the

assessable income.

Answer F:

The “taxation ruling of TR 2004/15” provides guidance in ascertaining whether the

company that is not incorporated in Australia will be considered as the Australian occupant

under the second statutory test of the meaning of “Resident of Australia” stated in

“subsection 6(1) of the ITAA 1936”4.

3 Grange, Janet, Geralyn A Jover-Ledesma and Gary L Maydew, 2014 Principles Of Business

Taxation

4 James, Simon, The Economics Of Taxation 2014

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Answer G:

Two division of ITAA 1997 that provides deductions for capital outlay are;

a. Division 40 Uniform capital allowances

b. Division 43 Capital works allowances

Answer H:

The appropriate tax rate for the taxpayer that has the assessable earnings of $80,000 in

2017/18 is stated below;

Taxable Income = 80,000 (Marginal tax rate 32.5% with 3,572 plus 32.5 cents for every

dollar over $37,000)

Answer I:

“Sub-Division 11-B of the ITAA 1997” list down the provision for treating the

amounts as the Non Assessable Non Exempt Income.

Answer J:

Under the “Tax Determination TD 2017/4”, 53 cents per kilometre is applicable for

motor vehicles with the engine capacity of 2500 cc.

Answer to question 2:

The “taxation ruling of TR 98/17” is related with the residency status of a individual

that arrives to Australia5. The ruling provides the taxation commissioner with the

understanding regarding the ordinary meaning of the word resides inside the meaning of the

“subsection 6(1) of the ITAA 1936”. The ruling is mainly applied on individuals that enters

to Australia.

5 Jover-Ledesma, Geralyn, Principles Of Business Taxation 2015 (Cch Incorporated, 2014)

Answer G:

Two division of ITAA 1997 that provides deductions for capital outlay are;

a. Division 40 Uniform capital allowances

b. Division 43 Capital works allowances

Answer H:

The appropriate tax rate for the taxpayer that has the assessable earnings of $80,000 in

2017/18 is stated below;

Taxable Income = 80,000 (Marginal tax rate 32.5% with 3,572 plus 32.5 cents for every

dollar over $37,000)

Answer I:

“Sub-Division 11-B of the ITAA 1997” list down the provision for treating the

amounts as the Non Assessable Non Exempt Income.

Answer J:

Under the “Tax Determination TD 2017/4”, 53 cents per kilometre is applicable for

motor vehicles with the engine capacity of 2500 cc.

Answer to question 2:

The “taxation ruling of TR 98/17” is related with the residency status of a individual

that arrives to Australia5. The ruling provides the taxation commissioner with the

understanding regarding the ordinary meaning of the word resides inside the meaning of the

“subsection 6(1) of the ITAA 1936”. The ruling is mainly applied on individuals that enters

to Australia.

5 Jover-Ledesma, Geralyn, Principles Of Business Taxation 2015 (Cch Incorporated, 2014)

5TAXATION LAW

The current case study is based on advising Martelle regarding her residency status

while present in Australia. She arrived in Australia for work-purpose though she intends to

return to country of her domicile. When an individual that comes to Australia with no

intention of residing here on permanent basis, then all the factors regarding the person’s

presence should be considered in ascertaining the residency status. The quality and an

individual’s behaviour while in Australia aids in determining whether an individual resides in

Australia. The following factors that are considered by ATO in determining the residency

status includes;

a. The intention or the objective of existence

b. Family and service or business relations

c. Maintenance as well as location of assets

d. Societal and living arrangements

When an individual’s behaviour is consistent with that living in Australia over the

considerable time, then the person would be held as the Australian resident. The viewpoint of

commissioner is that the time of six months is sufficient to decide whether an individual

behaviour is constant with existing in Australia. The meaning of the term reside was

considered in “Reid v The commissioner of Inland Revenue (1926)” where the quality of

existence as well as the time are considered in ascertaining whether the person lives in the

place where they spend a portion of their lives6. However, the court in “Miesegaes v

Commissioner of Inland Revenue (1957)” held that a person that enters to Australia to take

up the pre-arranged service opportunities may be held as occupant given their stay complies

with residing in Australia.

6 Kenny, Paul, Michael Blissenden and Sylvia Villios, Australian Tax 2018

The current case study is based on advising Martelle regarding her residency status

while present in Australia. She arrived in Australia for work-purpose though she intends to

return to country of her domicile. When an individual that comes to Australia with no

intention of residing here on permanent basis, then all the factors regarding the person’s

presence should be considered in ascertaining the residency status. The quality and an

individual’s behaviour while in Australia aids in determining whether an individual resides in

Australia. The following factors that are considered by ATO in determining the residency

status includes;

a. The intention or the objective of existence

b. Family and service or business relations

c. Maintenance as well as location of assets

d. Societal and living arrangements

When an individual’s behaviour is consistent with that living in Australia over the

considerable time, then the person would be held as the Australian resident. The viewpoint of

commissioner is that the time of six months is sufficient to decide whether an individual

behaviour is constant with existing in Australia. The meaning of the term reside was

considered in “Reid v The commissioner of Inland Revenue (1926)” where the quality of

existence as well as the time are considered in ascertaining whether the person lives in the

place where they spend a portion of their lives6. However, the court in “Miesegaes v

Commissioner of Inland Revenue (1957)” held that a person that enters to Australia to take

up the pre-arranged service opportunities may be held as occupant given their stay complies

with residing in Australia.

6 Kenny, Paul, Michael Blissenden and Sylvia Villios, Australian Tax 2018

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

As evident Martelle opened an Australian bank account that stipulated her salary to be

paid in that account. She even bought a boat to use it for enjoying the Island during the

weekends with her friends. This additionally adds to the weight that Martelle has established

behaviour which is consistent with residing here. Martelle exhibits the characteristics of

residing in Australia over the entire period. With reference to the judgement made in “Reid v

The commissioner of Inland Revenue (1926)” Martelle will be regarded as Australian

resident inside the connotation of “subsection 6(1) of the ITAA 1936”7. Therefore, the salary

income that is paid into Martelle’s bank account in Australia will held liable for taxation

since she is an Australian within the sense of the Act.

Answer to question 3:

“Section 6-1 of the ITAA 1936” explains that income from person exertion represents

the income that is obtained from salaries, wages, fees, allowances or gratuities that is

received in the capacity of employee in respect of any services provided. A taxpayer that

receives receipts from employment would be subjected to income tax. “Section 6-5 of the

ITAA 1997” states that customarily, majority of the income that is received by the taxpayer is

treated as the ordinary income. The law court in “Scott v CT (1395)” held that receipts must

be considered as income based on ordinary concepts8. Similarly the receipts of salary by

Ellen constitutes income from personal services or employment. The receipts would be

taxable under the ordinary concepts of “section 6-5 of the ITAA 1997” as ordinary income.

7 McCouat, Philip, Australian Master GST Guide 2018

8 Burton, Mark. "A Review of Judicial References to the Dictum of Jordan CJ, Expressed in

Scott v. Commissioner of Taxation, in Elaborating the Meaning of Income for the Purposes

of the Australian Income Tax." J. Austl. Tax'n 19 (2017): 50.

As evident Martelle opened an Australian bank account that stipulated her salary to be

paid in that account. She even bought a boat to use it for enjoying the Island during the

weekends with her friends. This additionally adds to the weight that Martelle has established

behaviour which is consistent with residing here. Martelle exhibits the characteristics of

residing in Australia over the entire period. With reference to the judgement made in “Reid v

The commissioner of Inland Revenue (1926)” Martelle will be regarded as Australian

resident inside the connotation of “subsection 6(1) of the ITAA 1936”7. Therefore, the salary

income that is paid into Martelle’s bank account in Australia will held liable for taxation

since she is an Australian within the sense of the Act.

Answer to question 3:

“Section 6-1 of the ITAA 1936” explains that income from person exertion represents

the income that is obtained from salaries, wages, fees, allowances or gratuities that is

received in the capacity of employee in respect of any services provided. A taxpayer that

receives receipts from employment would be subjected to income tax. “Section 6-5 of the

ITAA 1997” states that customarily, majority of the income that is received by the taxpayer is

treated as the ordinary income. The law court in “Scott v CT (1395)” held that receipts must

be considered as income based on ordinary concepts8. Similarly the receipts of salary by

Ellen constitutes income from personal services or employment. The receipts would be

taxable under the ordinary concepts of “section 6-5 of the ITAA 1997” as ordinary income.

7 McCouat, Philip, Australian Master GST Guide 2018

8 Burton, Mark. "A Review of Judicial References to the Dictum of Jordan CJ, Expressed in

Scott v. Commissioner of Taxation, in Elaborating the Meaning of Income for the Purposes

of the Australian Income Tax." J. Austl. Tax'n 19 (2017): 50.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Ellen reported a receipt of $425 from the Westpac bank account. The receipt should be

characterised as income which is assessable within the ordinary sense of “section 6-5 of the

ITAA 1997”.

The court of law in “Moore v Griffiths (1972)” held that mere winning from prize is

not an income. However, the prize winnings might be considered as income if an adequate

“nexus” exists with the taxpayer’s income generating activities. As held in “Kelly v FC of T

(1985)” the skilled footballer was awarded as the best and fairest player9. The amount that

was received as award will be held taxable since it was incidental with the taxpayer work and

employment which was also related to his use of skills. Denoting the above judgement, the

receipt of $6,500 by Ellen for “Queensland Designer of the Year” will be held as taxable

income since it incidental to the taxpayer work and employment.

Payments received for relinquishing or restricting right is not regarded as income. For

example, payments received for assenting not to do something are not classified as income.

Perhaps under “(section 104-35 (1)” relinquishing or restricting right results in CGT event

D1. A CGT event D1 occurs when the taxpayer creates any contractual right to another

entity. For examples restraint of trade where the taxpayer agrees of not operating any similar

business inside a particular radius or any exclusive trade agreements. As held in “Higgs v

Oliver (1951)” the taxpayer was paid a lump sum for agreeing not produce, act or direct any

films for a period of eighteen months was not held as income10. Similarly the receipt of

10,000 by Ellen for signing the restrictive covenants cannot be held as income. Instead under

“(section 104-35 (1)” the restrictive covenant constitutes CGT event D1.

9 Sadiq, Kerrie, Australian Taxation Law Cases 2018 (Thomson Reuters, 2018)

10 Taylor, C. J et al, Understanding Taxation Law 2018

Ellen reported a receipt of $425 from the Westpac bank account. The receipt should be

characterised as income which is assessable within the ordinary sense of “section 6-5 of the

ITAA 1997”.

The court of law in “Moore v Griffiths (1972)” held that mere winning from prize is

not an income. However, the prize winnings might be considered as income if an adequate

“nexus” exists with the taxpayer’s income generating activities. As held in “Kelly v FC of T

(1985)” the skilled footballer was awarded as the best and fairest player9. The amount that

was received as award will be held taxable since it was incidental with the taxpayer work and

employment which was also related to his use of skills. Denoting the above judgement, the

receipt of $6,500 by Ellen for “Queensland Designer of the Year” will be held as taxable

income since it incidental to the taxpayer work and employment.

Payments received for relinquishing or restricting right is not regarded as income. For

example, payments received for assenting not to do something are not classified as income.

Perhaps under “(section 104-35 (1)” relinquishing or restricting right results in CGT event

D1. A CGT event D1 occurs when the taxpayer creates any contractual right to another

entity. For examples restraint of trade where the taxpayer agrees of not operating any similar

business inside a particular radius or any exclusive trade agreements. As held in “Higgs v

Oliver (1951)” the taxpayer was paid a lump sum for agreeing not produce, act or direct any

films for a period of eighteen months was not held as income10. Similarly the receipt of

10,000 by Ellen for signing the restrictive covenants cannot be held as income. Instead under

“(section 104-35 (1)” the restrictive covenant constitutes CGT event D1.

9 Sadiq, Kerrie, Australian Taxation Law Cases 2018 (Thomson Reuters, 2018)

10 Taylor, C. J et al, Understanding Taxation Law 2018

8TAXATION LAW

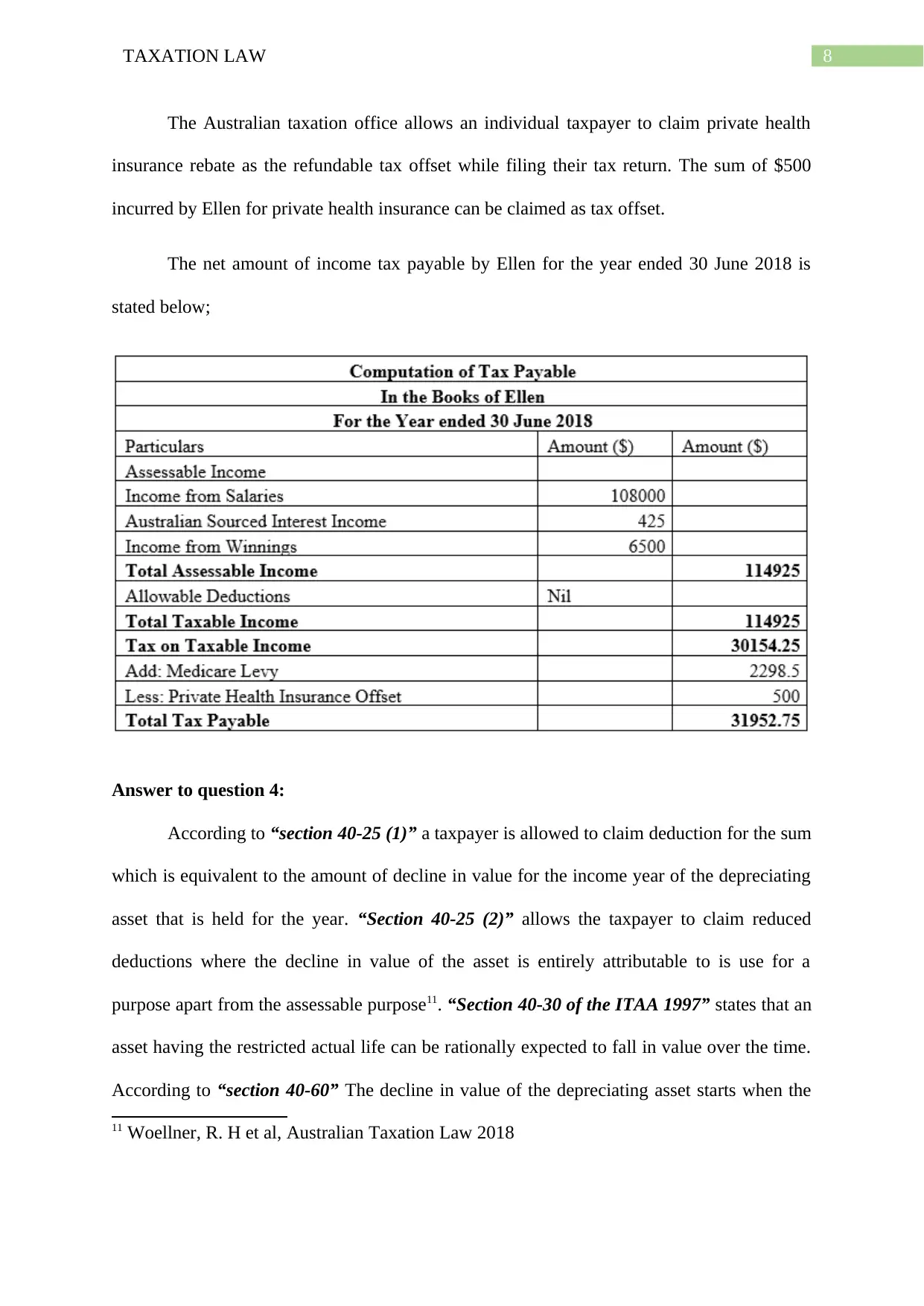

The Australian taxation office allows an individual taxpayer to claim private health

insurance rebate as the refundable tax offset while filing their tax return. The sum of $500

incurred by Ellen for private health insurance can be claimed as tax offset.

The net amount of income tax payable by Ellen for the year ended 30 June 2018 is

stated below;

Answer to question 4:

According to “section 40-25 (1)” a taxpayer is allowed to claim deduction for the sum

which is equivalent to the amount of decline in value for the income year of the depreciating

asset that is held for the year. “Section 40-25 (2)” allows the taxpayer to claim reduced

deductions where the decline in value of the asset is entirely attributable to is use for a

purpose apart from the assessable purpose11. “Section 40-30 of the ITAA 1997” states that an

asset having the restricted actual life can be rationally expected to fall in value over the time.

According to “section 40-60” The decline in value of the depreciating asset starts when the

11 Woellner, R. H et al, Australian Taxation Law 2018

The Australian taxation office allows an individual taxpayer to claim private health

insurance rebate as the refundable tax offset while filing their tax return. The sum of $500

incurred by Ellen for private health insurance can be claimed as tax offset.

The net amount of income tax payable by Ellen for the year ended 30 June 2018 is

stated below;

Answer to question 4:

According to “section 40-25 (1)” a taxpayer is allowed to claim deduction for the sum

which is equivalent to the amount of decline in value for the income year of the depreciating

asset that is held for the year. “Section 40-25 (2)” allows the taxpayer to claim reduced

deductions where the decline in value of the asset is entirely attributable to is use for a

purpose apart from the assessable purpose11. “Section 40-30 of the ITAA 1997” states that an

asset having the restricted actual life can be rationally expected to fall in value over the time.

According to “section 40-60” The decline in value of the depreciating asset starts when the

11 Woellner, R. H et al, Australian Taxation Law 2018

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

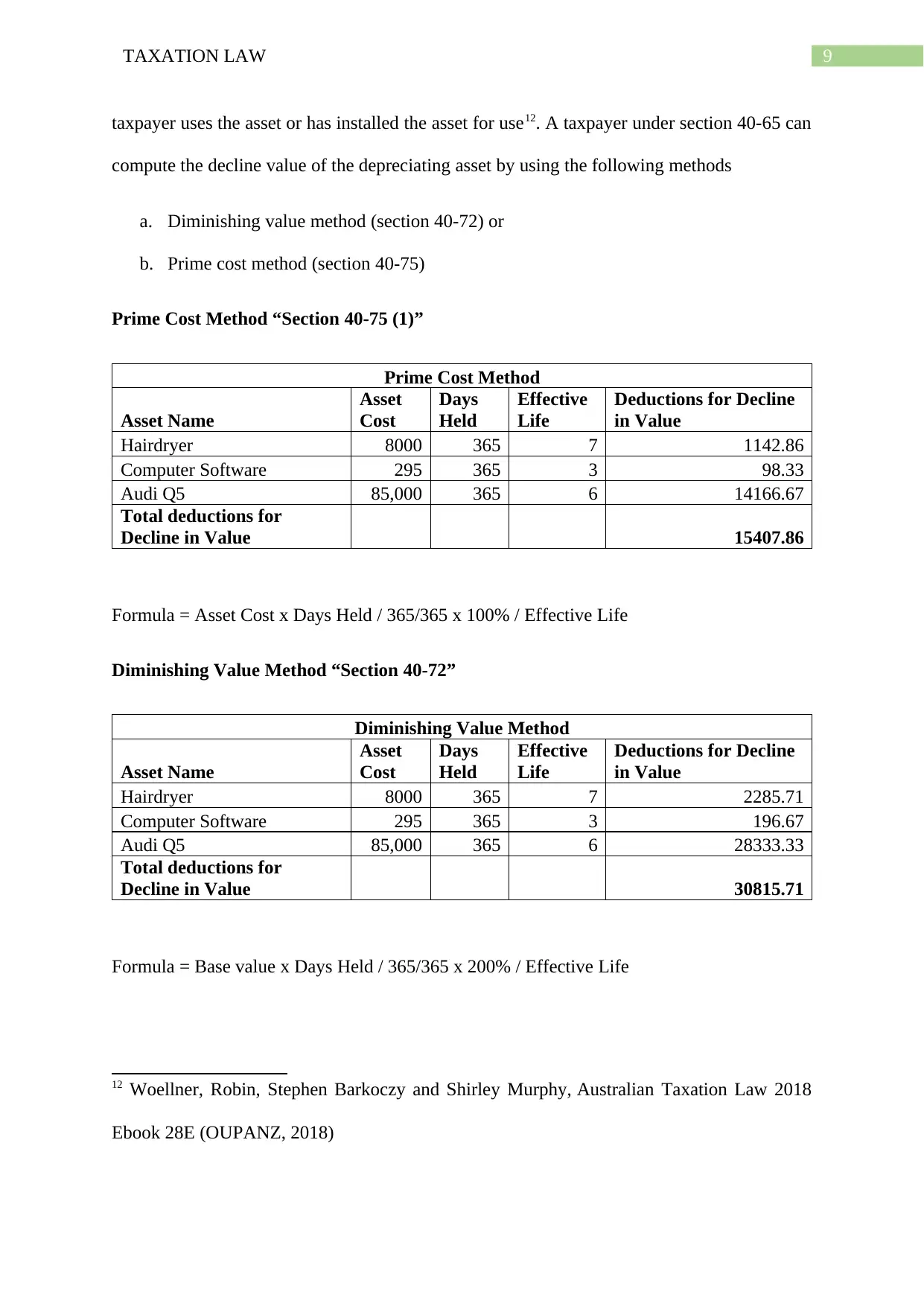

taxpayer uses the asset or has installed the asset for use12. A taxpayer under section 40-65 can

compute the decline value of the depreciating asset by using the following methods

a. Diminishing value method (section 40-72) or

b. Prime cost method (section 40-75)

Prime Cost Method “Section 40-75 (1)”

Prime Cost Method

Asset Name

Asset

Cost

Days

Held

Effective

Life

Deductions for Decline

in Value

Hairdryer 8000 365 7 1142.86

Computer Software 295 365 3 98.33

Audi Q5 85,000 365 6 14166.67

Total deductions for

Decline in Value 15407.86

Formula = Asset Cost x Days Held / 365/365 x 100% / Effective Life

Diminishing Value Method “Section 40-72”

Diminishing Value Method

Asset Name

Asset

Cost

Days

Held

Effective

Life

Deductions for Decline

in Value

Hairdryer 8000 365 7 2285.71

Computer Software 295 365 3 196.67

Audi Q5 85,000 365 6 28333.33

Total deductions for

Decline in Value 30815.71

Formula = Base value x Days Held / 365/365 x 200% / Effective Life

12 Woellner, Robin, Stephen Barkoczy and Shirley Murphy, Australian Taxation Law 2018

Ebook 28E (OUPANZ, 2018)

taxpayer uses the asset or has installed the asset for use12. A taxpayer under section 40-65 can

compute the decline value of the depreciating asset by using the following methods

a. Diminishing value method (section 40-72) or

b. Prime cost method (section 40-75)

Prime Cost Method “Section 40-75 (1)”

Prime Cost Method

Asset Name

Asset

Cost

Days

Held

Effective

Life

Deductions for Decline

in Value

Hairdryer 8000 365 7 1142.86

Computer Software 295 365 3 98.33

Audi Q5 85,000 365 6 14166.67

Total deductions for

Decline in Value 15407.86

Formula = Asset Cost x Days Held / 365/365 x 100% / Effective Life

Diminishing Value Method “Section 40-72”

Diminishing Value Method

Asset Name

Asset

Cost

Days

Held

Effective

Life

Deductions for Decline

in Value

Hairdryer 8000 365 7 2285.71

Computer Software 295 365 3 196.67

Audi Q5 85,000 365 6 28333.33

Total deductions for

Decline in Value 30815.71

Formula = Base value x Days Held / 365/365 x 200% / Effective Life

12 Woellner, Robin, Stephen Barkoczy and Shirley Murphy, Australian Taxation Law 2018

Ebook 28E (OUPANZ, 2018)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Based on the above stated calculation Jenifer should choose diminishing value

method as under this method she can claim a maximum deduction of $30,815.71 from her

assessable income.

Answer to question 5:

Gains that originates from the carrying on of the business is regarded as usual income

under “section 6-5 of the ITAA 1997”. However gains originating from the hobby or

pleasure are not treated as income unless the gains are specifically made taxable by the

legislation13. As understood in the present situation of Julie who is a keen photographer and

carried on the hobby of photography is now considering setting up her own business.

According to Australian Taxation Office it is necessary to understand the differences between

the hobby and business for taxation and other purpose. Similarly for Julie her tax obligations

commences soon when she is in the business of photography. It is essential to understand

when the hobby or recreational activities turns out to be business.

The legislative definition of “section 995-1” defines business as any profession, trade

or service but not in the capacity of employee. The court of law in “FC of T v Ferguson

(1979)” used numerous indicators that reflects the existence of business. The court of law in

“Stone v FC of T (2005)” have considered common indicators of business whether the profit

making intention is existent14. The extent of events together with the nature and kind of

capital are some of the factors that is considered by the ATO. As held in “JR Walker v FC of

13 Pinto, Dale. "State taxes." Australian Taxation Law. CCH Australia Limited, 2011. 1763-

1762.

14 Braithwaite, Valerie. Taxing democracy: Understanding tax avoidance and evasion.

Routledge, 2017.

Based on the above stated calculation Jenifer should choose diminishing value

method as under this method she can claim a maximum deduction of $30,815.71 from her

assessable income.

Answer to question 5:

Gains that originates from the carrying on of the business is regarded as usual income

under “section 6-5 of the ITAA 1997”. However gains originating from the hobby or

pleasure are not treated as income unless the gains are specifically made taxable by the

legislation13. As understood in the present situation of Julie who is a keen photographer and

carried on the hobby of photography is now considering setting up her own business.

According to Australian Taxation Office it is necessary to understand the differences between

the hobby and business for taxation and other purpose. Similarly for Julie her tax obligations

commences soon when she is in the business of photography. It is essential to understand

when the hobby or recreational activities turns out to be business.

The legislative definition of “section 995-1” defines business as any profession, trade

or service but not in the capacity of employee. The court of law in “FC of T v Ferguson

(1979)” used numerous indicators that reflects the existence of business. The court of law in

“Stone v FC of T (2005)” have considered common indicators of business whether the profit

making intention is existent14. The extent of events together with the nature and kind of

capital are some of the factors that is considered by the ATO. As held in “JR Walker v FC of

13 Pinto, Dale. "State taxes." Australian Taxation Law. CCH Australia Limited, 2011. 1763-

1762.

14 Braithwaite, Valerie. Taxing democracy: Understanding tax avoidance and evasion.

Routledge, 2017.

11TAXATION LAW

T (1985)” small operations undertaken by the taxpayer can still continue as the business

given there are sufficient other characteristics15. As evident in the current situations of Julie a

commercial approach has been taken to commence the business of photography which she

carried out as hobby for several years. As Julie intends to set up the business of photography

she must register the business name or obtain the ABN for her business. Other factors

includes;

a. Keeping the records of the business and accounts books

b. Having the separate business bank account

c. Having the registered name of business

d. Having necessary qualification or licence

The receipts that would be obtained by Julie from such business of photography

would be held as ordinary income under the normal proceeds of the business activity.

Answer to question 6:

As per “section 8-1” a person is permitted to claim deduction for expenditures that

are occurred in gaining the assessable income given the expenses are occurred in producing

the taxable earnings or occurred necessarily in making the taxable income16. In the present

situation Change runs a marketing business and incurs certain business costs for the income

year ended. A salary cost of $300,000 is occurred by Chang. He also reports a salary cost of

$4,000 that was paid to his son who carried out graphic design. “Section 8-1” has the

potential to be implemented on any taxpayer. The salary cost of $300,000 that is incurred by

15 Basu, Subhajit. Global perspectives on e-commerce taxation law. Routledge, 2016.

16 Saad, Natrah. "Tax knowledge, tax complexity and tax compliance: Taxpayers’

view." Procedia-Social and Behavioral Sciences 109 (2014): 1069-1075.

T (1985)” small operations undertaken by the taxpayer can still continue as the business

given there are sufficient other characteristics15. As evident in the current situations of Julie a

commercial approach has been taken to commence the business of photography which she

carried out as hobby for several years. As Julie intends to set up the business of photography

she must register the business name or obtain the ABN for her business. Other factors

includes;

a. Keeping the records of the business and accounts books

b. Having the separate business bank account

c. Having the registered name of business

d. Having necessary qualification or licence

The receipts that would be obtained by Julie from such business of photography

would be held as ordinary income under the normal proceeds of the business activity.

Answer to question 6:

As per “section 8-1” a person is permitted to claim deduction for expenditures that

are occurred in gaining the assessable income given the expenses are occurred in producing

the taxable earnings or occurred necessarily in making the taxable income16. In the present

situation Change runs a marketing business and incurs certain business costs for the income

year ended. A salary cost of $300,000 is occurred by Chang. He also reports a salary cost of

$4,000 that was paid to his son who carried out graphic design. “Section 8-1” has the

potential to be implemented on any taxpayer. The salary cost of $300,000 that is incurred by

15 Basu, Subhajit. Global perspectives on e-commerce taxation law. Routledge, 2016.

16 Saad, Natrah. "Tax knowledge, tax complexity and tax compliance: Taxpayers’

view." Procedia-Social and Behavioral Sciences 109 (2014): 1069-1075.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.