University Taxation Law: Residency and Tax Advice Report

VerifiedAdded on 2023/03/21

|9

|1370

|28

Report

AI Summary

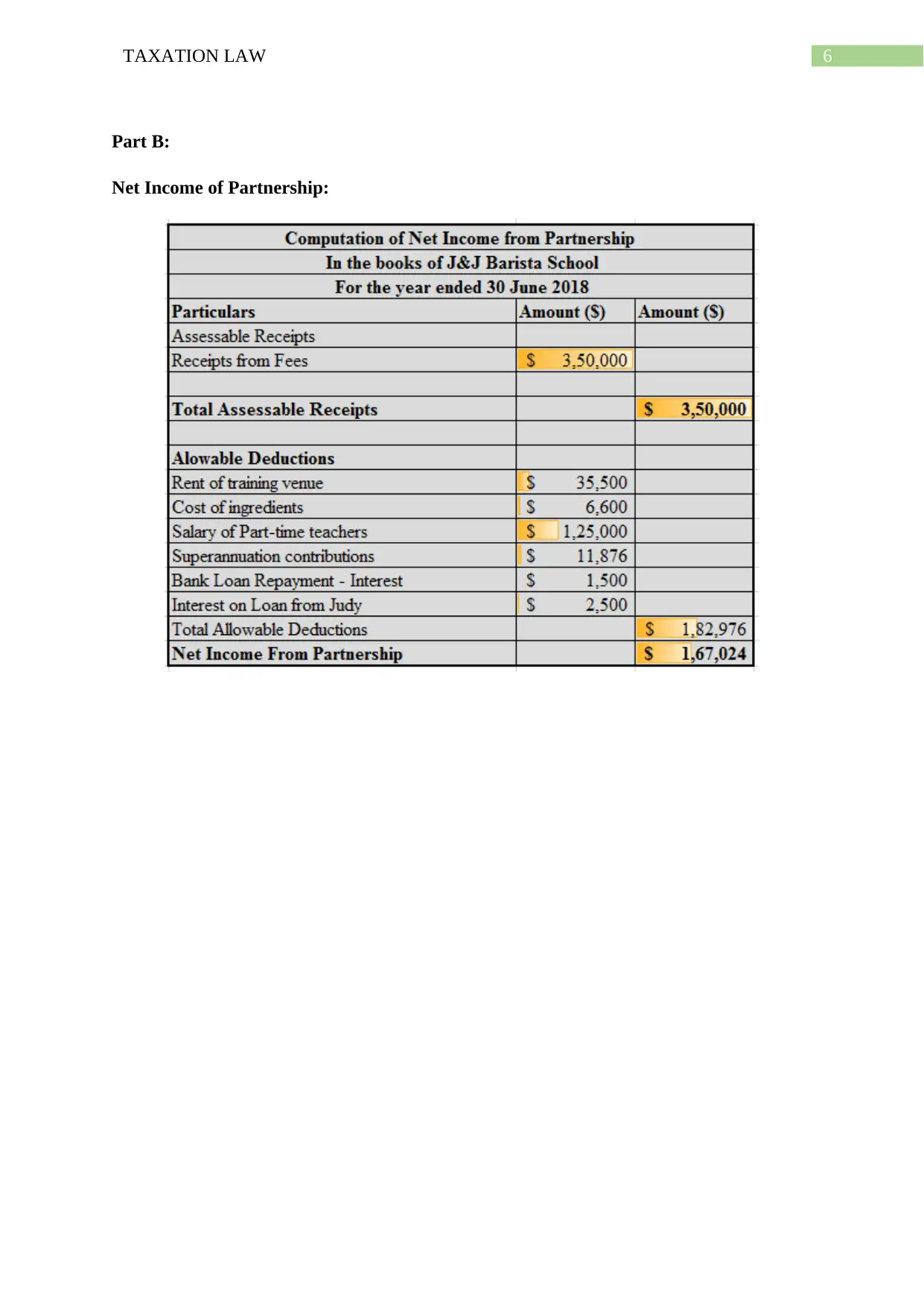

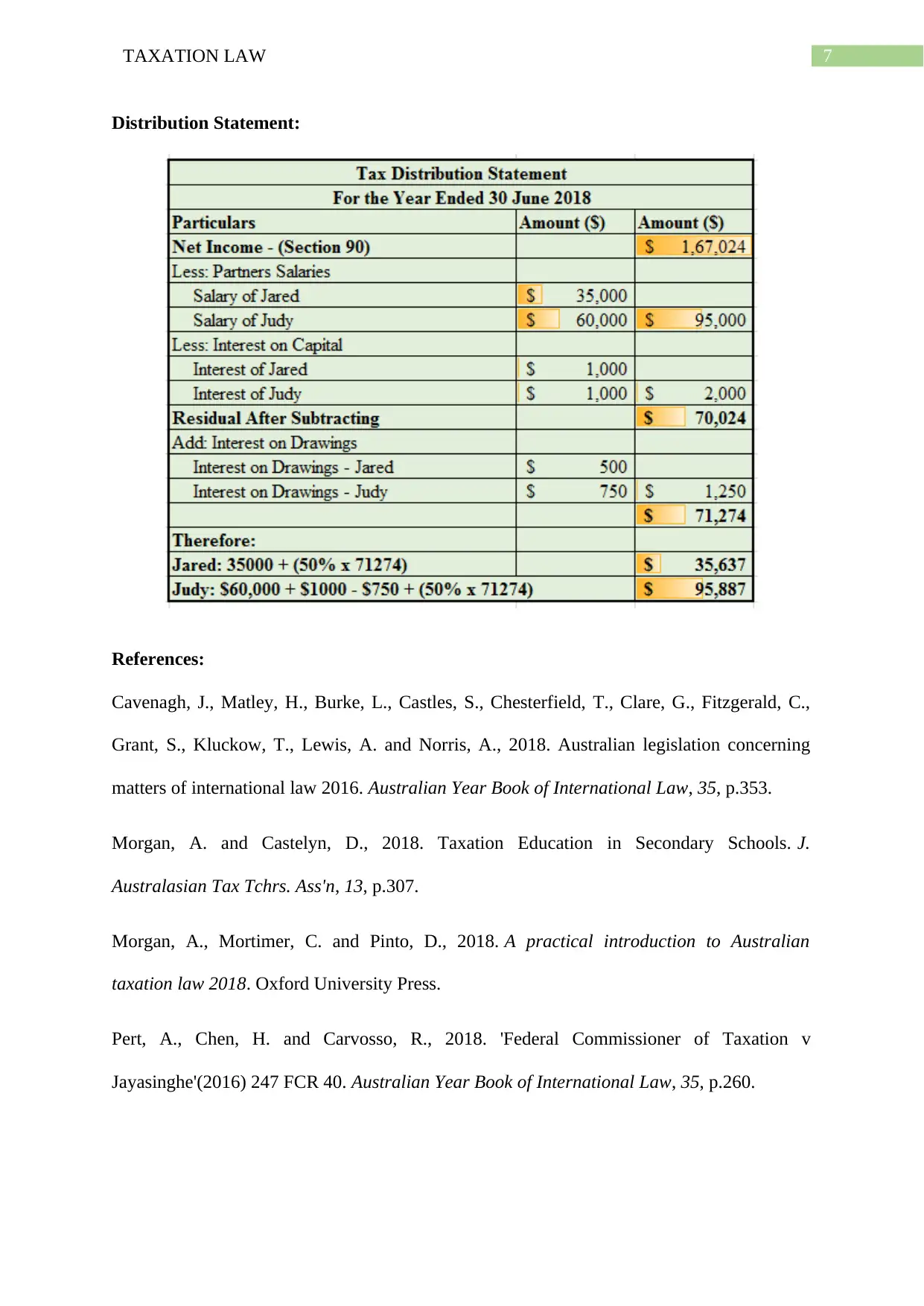

This report provides a comprehensive analysis of Australian taxation law, specifically addressing the residency status of an individual who has moved out of Australia. It includes a letter of advice to a taxpayer, Jack Johnson, detailing the application of various tests to determine residency, including the 'Resides in Australia Test,' 'Domicile Test,' '183-Day Test,' and 'Superannuation Test.' The report references relevant legislation, such as ITAA 1936 and ITAA 1997, and case law, such as IRC v Lysaght (1928) and Applegate v FCT (1979), to support its conclusions. The advice considers factors like time spent in Australia, domicile, and superannuation arrangements. The report concludes that based on the provided facts, the individual is considered a non-resident for tax purposes. The report also includes a distribution statement and references to relevant literature. This assignment is a tax practice assignment for ACC304 Taxation Law, requiring individual research and application of tax resources to synthesize an original piece of work.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.