Taxation Law Analysis: Manic Pty Ltd and Tax Compliance

VerifiedAdded on 2021/06/17

|12

|2770

|20

Report

AI Summary

This report analyzes the taxation law implications for Manic Pty Ltd, addressing assessable income, allowable deductions, and tax compliance. Part A examines specific financial transactions, including service fees, interest income, trading stock, bad debts, feasibility studies, repairs, loan interest, profit from sales of factory and shares, capital losses, depreciation, business entertainment expenses, compensation payments, and restrictive covenants. Each transaction is evaluated based on relevant sections of the ITAA 1997 and ITAA 1936, along with relevant case laws and taxation rulings, determining whether the expenses or income are taxable or deductible. Part B discusses the challenges of tax compliance for tax practitioners, considering the conflict between their professional purpose and societal expectations, the role of tax avoidance, and the ethical considerations involved in advising clients. The report concludes with a critique of corporate tax avoidance and its implications for society.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Part A:........................................................................................................................................2

Answer to requirement A:..........................................................................................................2

Answer to requirement B:..........................................................................................................7

Part B:.........................................................................................................................................7

Reference List:.........................................................................................................................10

Table of Contents

Part A:........................................................................................................................................2

Answer to requirement A:..........................................................................................................2

Answer to requirement B:..........................................................................................................7

Part B:.........................................................................................................................................7

Reference List:.........................................................................................................................10

2TAXATION LAW

Part A:

Answer to requirement A:

Memo

To Chief Financial Officer

Manic Pty Ltd

As defined under the “Section 6 of the ITAA 1997” an individual that derives income

through the private exertion is regarded as the income consisting of the earnings, salaries,

wages, bonus, fees, pension, superannuation’s or any form of business profits that is

performed by the taxpayer either individually or through the partnership (Woellner et al.

2016). Referring the definition of “Section 6-5 of the ITAA 1997” income that is generated

from the ordinary sources is held liable for taxation. Citing the reference of the court in the

case of “Scott v Commissioner of Taxation (1935)” receipts will be held as the taxable

income in compliance with the ordinary concepts (Barkoczy 2016). Denoting from the

current circumstances of Manic Pty Ltd the sum of $80,000 that are received from the service

fees forms the part of the taxable income as income derived from private exertion with

reference to “section 6 of the ITAA 1936”.

As stated under the “section 6-5 of the ITAA 1997” a person when beneficially

derives the income has the character of home coming for the taxpayer (Cao et al. 2015).

Additionally, income that are derived from the ordinary concept of mankind is considered

assessable. Evidently in the situation of Manic Pty Ltd the interest income will be included at

the time of filing for tax return.

According to the “section 8-1 of the ITAA 1997” an individual taxpayer is allowed to

claim deductions for the expenses that are incurred in generating the assessable income for

Part A:

Answer to requirement A:

Memo

To Chief Financial Officer

Manic Pty Ltd

As defined under the “Section 6 of the ITAA 1997” an individual that derives income

through the private exertion is regarded as the income consisting of the earnings, salaries,

wages, bonus, fees, pension, superannuation’s or any form of business profits that is

performed by the taxpayer either individually or through the partnership (Woellner et al.

2016). Referring the definition of “Section 6-5 of the ITAA 1997” income that is generated

from the ordinary sources is held liable for taxation. Citing the reference of the court in the

case of “Scott v Commissioner of Taxation (1935)” receipts will be held as the taxable

income in compliance with the ordinary concepts (Barkoczy 2016). Denoting from the

current circumstances of Manic Pty Ltd the sum of $80,000 that are received from the service

fees forms the part of the taxable income as income derived from private exertion with

reference to “section 6 of the ITAA 1936”.

As stated under the “section 6-5 of the ITAA 1997” a person when beneficially

derives the income has the character of home coming for the taxpayer (Cao et al. 2015).

Additionally, income that are derived from the ordinary concept of mankind is considered

assessable. Evidently in the situation of Manic Pty Ltd the interest income will be included at

the time of filing for tax return.

According to the “section 8-1 of the ITAA 1997” an individual taxpayer is allowed to

claim deductions for the expenses that are incurred in generating the assessable income for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

any loss or expenses incurred (Braithwaite 2017). The Australian taxation office provides that

expenditure related to trading stock is allowed for deduction. An increase in the value of the

trading stock constitute assessable income whereas a fall in the value of trading stock is

regarded as the permissible deduction. Taking into the consideration the value of trading

stock helps in assuring that in the ordinary business course the taxpayer relating to trading

stock purchased during the year reflects the cost of sales that is involved during the year.

Therefore, purchasing the trading stock from the Hong Kong forms the part of the deduction

as the accounting expenditure.

According to the “taxation ruling of 92/18” provides that there are situations where a

taxpayer can claim an allowable deductions relating to the bad debts (Davis et al. 2015).

According to the “section 51 (1)” any types of business losses that are in the nature of

outgoing or holding the characteristics of revenue is allowed for deductions when those

losses and outgoings are primarily incurred. The federal court in the case of “Crane Sales

Ltd v Federal Commissioner of Taxation (1971)” explained that the debt constitutes the

purpose in section “63 of the ITAA 1997” where a taxpayer is allowed to claim equal

deductions for the debt which is bad.

An individual taxpayer is only allowed to claim deductions for the bad debt which is

entirely written off as the bad debt during the year of income (Saad 2014). Ideally in the case

of Manic Pty Ltd the bad provision shall not be allowed as allowable deductions. The reason

for this is that the company did not recorded or suffered any form loss from bad debt.

Furthermore, there was no evidence of recording of transaction by the Manic Pty Ltd in the

income year where an appropriate bad debt deduction can be claimed.

The guidelines provided by the Australian taxation office provides that a person can

claim deductions relating to expenses that are in the nature of capital (Miller and Oats 2016).

any loss or expenses incurred (Braithwaite 2017). The Australian taxation office provides that

expenditure related to trading stock is allowed for deduction. An increase in the value of the

trading stock constitute assessable income whereas a fall in the value of trading stock is

regarded as the permissible deduction. Taking into the consideration the value of trading

stock helps in assuring that in the ordinary business course the taxpayer relating to trading

stock purchased during the year reflects the cost of sales that is involved during the year.

Therefore, purchasing the trading stock from the Hong Kong forms the part of the deduction

as the accounting expenditure.

According to the “taxation ruling of 92/18” provides that there are situations where a

taxpayer can claim an allowable deductions relating to the bad debts (Davis et al. 2015).

According to the “section 51 (1)” any types of business losses that are in the nature of

outgoing or holding the characteristics of revenue is allowed for deductions when those

losses and outgoings are primarily incurred. The federal court in the case of “Crane Sales

Ltd v Federal Commissioner of Taxation (1971)” explained that the debt constitutes the

purpose in section “63 of the ITAA 1997” where a taxpayer is allowed to claim equal

deductions for the debt which is bad.

An individual taxpayer is only allowed to claim deductions for the bad debt which is

entirely written off as the bad debt during the year of income (Saad 2014). Ideally in the case

of Manic Pty Ltd the bad provision shall not be allowed as allowable deductions. The reason

for this is that the company did not recorded or suffered any form loss from bad debt.

Furthermore, there was no evidence of recording of transaction by the Manic Pty Ltd in the

income year where an appropriate bad debt deduction can be claimed.

The guidelines provided by the Australian taxation office provides that a person can

claim deductions relating to expenses that are in the nature of capital (Miller and Oats 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

These deductions are only made available if the expenses are not occurred as the charge of

depreciating assets. An individual that occurs the expenses relating to the present business or

business which was previously executed or aspires to conduct, the expenditure will be

allowed for deduction to the extent the taxpayer aspires to carry on the business (Robin and

Barkoczy 2018). The Australian Taxation Office provides that a deduction is allowable

relating to the cost of feasibility studies, market research or setting up the business. The

expenses of $25,000 incurred by the Manic Pty Ltd associated to the viability of the entering

to the new market will be allowed for claiming deductions.

According to the “Section 25-10 of the ITAA 1997” a person is allowed to claim to

deductions for expenses relating to repairs that are performed on the premises or on the

depreciating assets which is held or completely used for the producing assessable income

(Robin 2017). Repairs constitutes restoring the asset to the earlier state without causing any

change in the asset character. “Section 25-10 of the ITAA 1997” defines that expenses which

is occurred for the purpose of repair are not allowed for deductions given the expenses are in

the nature of capital.

The federal court in the case of “Sun Newspaper Ltd v Federal Commissioner of

Taxation (1938)” differentiated between the capital and revenue outgoings. The

commissioner explained that expenses are incurred in producing the taxable income or

replacing the structure or the operating expenses is not allowed for deductions (Blakelock and

King 2017). A person is allowed to claim deductions only in the instances when the objective

of making deterioration good that is occurred through wear and tear. This usually comprises

of renewing or replacing the subsidiary portion but not completely the asset. Hence, the

expenses that are occurred in replacing the metal roof with the tiles is regarded as the capital

expenditure and as a result of this Manic Pty Ltd would not be allowed to claim an allowable

deduction under “subsection 25-10 (3) of the ITAA 1997”.

These deductions are only made available if the expenses are not occurred as the charge of

depreciating assets. An individual that occurs the expenses relating to the present business or

business which was previously executed or aspires to conduct, the expenditure will be

allowed for deduction to the extent the taxpayer aspires to carry on the business (Robin and

Barkoczy 2018). The Australian Taxation Office provides that a deduction is allowable

relating to the cost of feasibility studies, market research or setting up the business. The

expenses of $25,000 incurred by the Manic Pty Ltd associated to the viability of the entering

to the new market will be allowed for claiming deductions.

According to the “Section 25-10 of the ITAA 1997” a person is allowed to claim to

deductions for expenses relating to repairs that are performed on the premises or on the

depreciating assets which is held or completely used for the producing assessable income

(Robin 2017). Repairs constitutes restoring the asset to the earlier state without causing any

change in the asset character. “Section 25-10 of the ITAA 1997” defines that expenses which

is occurred for the purpose of repair are not allowed for deductions given the expenses are in

the nature of capital.

The federal court in the case of “Sun Newspaper Ltd v Federal Commissioner of

Taxation (1938)” differentiated between the capital and revenue outgoings. The

commissioner explained that expenses are incurred in producing the taxable income or

replacing the structure or the operating expenses is not allowed for deductions (Blakelock and

King 2017). A person is allowed to claim deductions only in the instances when the objective

of making deterioration good that is occurred through wear and tear. This usually comprises

of renewing or replacing the subsidiary portion but not completely the asset. Hence, the

expenses that are occurred in replacing the metal roof with the tiles is regarded as the capital

expenditure and as a result of this Manic Pty Ltd would not be allowed to claim an allowable

deduction under “subsection 25-10 (3) of the ITAA 1997”.

5TAXATION LAW

A person is entitled to claim an allowable deduction relating to the interest that is

paid on the borrowed amount to purchase the shares and investment related items. The

expenditure that are generally incurred are in the course of deriving taxable income (Fry

2017). As evident Manic incurred an expenditure on loan interest for the purchase of new

factory and the same will be considered as allowable deduction section 8-1 of the ITAA

1997. The expenses carries sufficient association with the positive limbs and the same is

allowed in case of Manic.

As evident Manic reported a profit from the sale of factory and also derived a profits

upon the sale of shares. The income will be included in the taxable earnings of “section 6-5

of the ITAA 1997”. Profits generated from the business is held as income based on the

realisable value (Murphy and Higgins 2016). To carry the characteristics of income the item

must be account as gain for the taxpayer that is beneficially obtained. Evidently in the

situations of sale of factory and sale of shares the amount derived from such transactions

represents gain for Manic Pty Ltd. As a consequence of this it would be held for assessment

at time of determining assessable income.

According to the Australian taxation office an individual experiencing loss upon the

sale investment items namely the shares and then the losses would constitute a capital loss

and the same is allowed to be set off only against the capital gains (Schenk 2017). Similarly

in case of Manic a capital loss was bought forward that comprised of $35,000. Manic in this

respect can set off the loss from the sale of shares.

According to the “Section 40-25 (1) of the ITAA 1997” a business entitled to claim

for deduction relating to the sum which is equal to the falling value during the income year of

the depreciating asset held by the entity (Hoffman et al. 2014). A depreciating asset refers to

those asset that has the restricted life and is expected to fall in value over the time period. As

A person is entitled to claim an allowable deduction relating to the interest that is

paid on the borrowed amount to purchase the shares and investment related items. The

expenditure that are generally incurred are in the course of deriving taxable income (Fry

2017). As evident Manic incurred an expenditure on loan interest for the purchase of new

factory and the same will be considered as allowable deduction section 8-1 of the ITAA

1997. The expenses carries sufficient association with the positive limbs and the same is

allowed in case of Manic.

As evident Manic reported a profit from the sale of factory and also derived a profits

upon the sale of shares. The income will be included in the taxable earnings of “section 6-5

of the ITAA 1997”. Profits generated from the business is held as income based on the

realisable value (Murphy and Higgins 2016). To carry the characteristics of income the item

must be account as gain for the taxpayer that is beneficially obtained. Evidently in the

situations of sale of factory and sale of shares the amount derived from such transactions

represents gain for Manic Pty Ltd. As a consequence of this it would be held for assessment

at time of determining assessable income.

According to the Australian taxation office an individual experiencing loss upon the

sale investment items namely the shares and then the losses would constitute a capital loss

and the same is allowed to be set off only against the capital gains (Schenk 2017). Similarly

in case of Manic a capital loss was bought forward that comprised of $35,000. Manic in this

respect can set off the loss from the sale of shares.

According to the “Section 40-25 (1) of the ITAA 1997” a business entitled to claim

for deduction relating to the sum which is equal to the falling value during the income year of

the depreciating asset held by the entity (Hoffman et al. 2014). A depreciating asset refers to

those asset that has the restricted life and is expected to fall in value over the time period. As

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

evident Manic incurred a depreciation expenditure of $120,000. By adhering to “section 40-

25 (1) of the ITAA 1997” Manic is entitled to claim for the allowable deduction.

According to the Australian taxation office expenditure that is incurred in as the

business entertainment purpose is allowed for deductions. These business expense constitute

for work purpose and are allowed for deduction under the provision of “section 8-1 of the

ITAA 1997” (Hill and Mancino 2014). According to “division 8 or section 40-880 of the

ITAA 1997” payments relating to compensation is allowed for deductions. An explanation

has been laid under the “section 25-50 of the ITAA 1997” and “subdivision 3AA of the

ITAA 1936” where a business is allowed to claim for deduction relating to specific payments.

Expenses that are occurred once and for all is usually regarded as the capital expenses

whereas expenses incurred often or regularly is held as revenue expenses. An expenses that

has the lasting benefit in bringing the asset into the existence is regarded as the capital

expenses. Referring to “division 8 of the ITAA 1997” capital expenses are not allowed for

deduction (Pope, Rupert and Anderson 2017). As held in “Sun Newspaper v Federal

Commissioner of Taxation” payments for restrictive covenants is not allowed for deductions

since the sum constitute capital in nature. Referring to the court of law verdict Manic incurred

an expenses on restrictive covenants and the expense constitute capital expenses which is not

allowed for deductions.

evident Manic incurred a depreciation expenditure of $120,000. By adhering to “section 40-

25 (1) of the ITAA 1997” Manic is entitled to claim for the allowable deduction.

According to the Australian taxation office expenditure that is incurred in as the

business entertainment purpose is allowed for deductions. These business expense constitute

for work purpose and are allowed for deduction under the provision of “section 8-1 of the

ITAA 1997” (Hill and Mancino 2014). According to “division 8 or section 40-880 of the

ITAA 1997” payments relating to compensation is allowed for deductions. An explanation

has been laid under the “section 25-50 of the ITAA 1997” and “subdivision 3AA of the

ITAA 1936” where a business is allowed to claim for deduction relating to specific payments.

Expenses that are occurred once and for all is usually regarded as the capital expenses

whereas expenses incurred often or regularly is held as revenue expenses. An expenses that

has the lasting benefit in bringing the asset into the existence is regarded as the capital

expenses. Referring to “division 8 of the ITAA 1997” capital expenses are not allowed for

deduction (Pope, Rupert and Anderson 2017). As held in “Sun Newspaper v Federal

Commissioner of Taxation” payments for restrictive covenants is not allowed for deductions

since the sum constitute capital in nature. Referring to the court of law verdict Manic incurred

an expenses on restrictive covenants and the expense constitute capital expenses which is not

allowed for deductions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

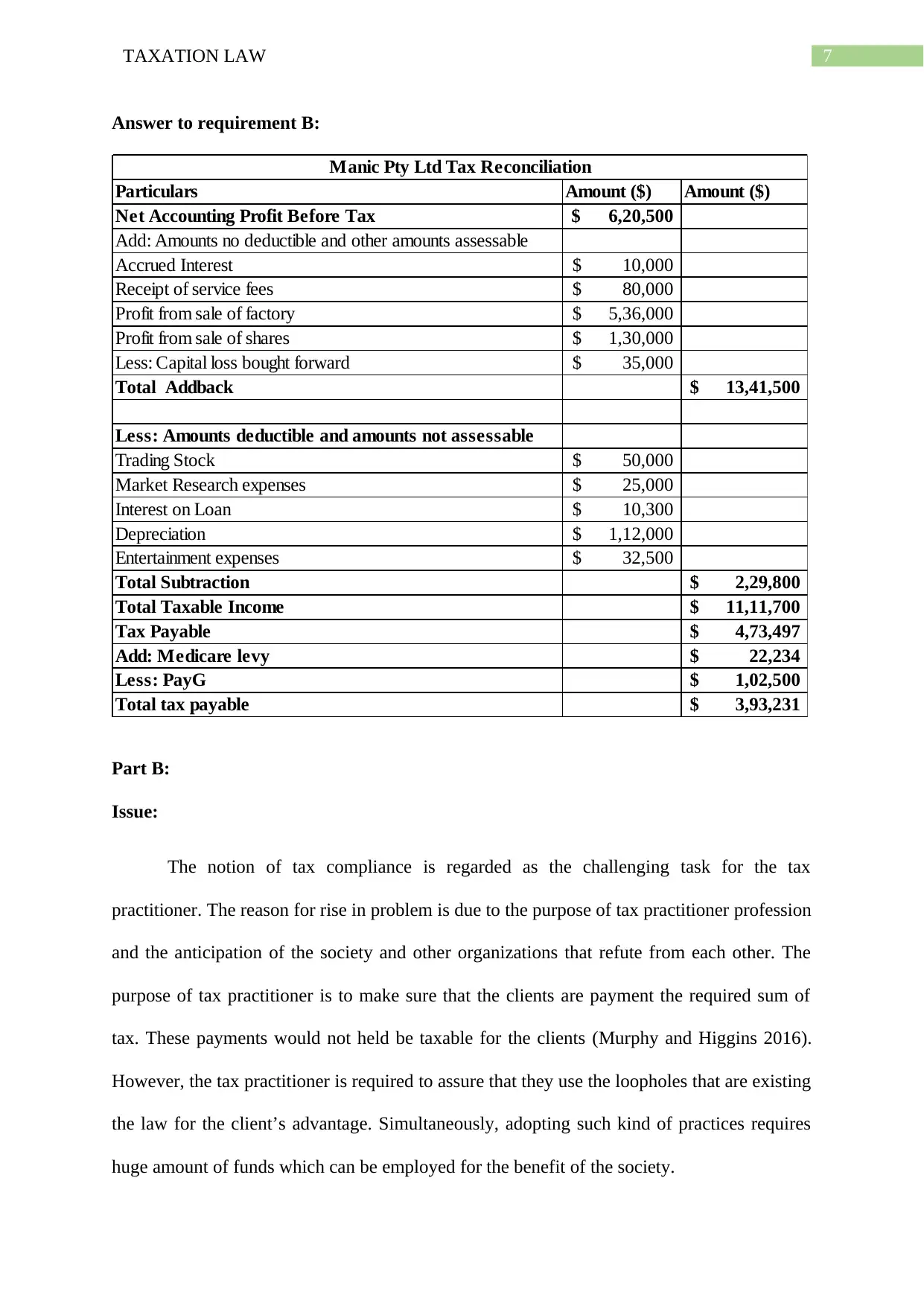

Answer to requirement B:

Particulars Amount ($) Amount ($)

Net Accounting Profit Before Tax 6,20,500$

Add: Amounts no deductible and other amounts assessable

Accrued Interest 10,000$

Receipt of service fees 80,000$

Profit from sale of factory 5,36,000$

Profit from sale of shares 1,30,000$

Less: Capital loss bought forward 35,000$

Total Addback 13,41,500$

Less: Amounts deductible and amounts not assessable

Trading Stock 50,000$

Market Research expenses 25,000$

Interest on Loan 10,300$

Depreciation 1,12,000$

Entertainment expenses 32,500$

Total Subtraction 2,29,800$

Total Taxable Income 11,11,700$

Tax Payable 4,73,497$

Add: Medicare levy 22,234$

Less: PayG 1,02,500$

Total tax payable 3,93,231$

Manic Pty Ltd Tax Reconciliation

Part B:

Issue:

The notion of tax compliance is regarded as the challenging task for the tax

practitioner. The reason for rise in problem is due to the purpose of tax practitioner profession

and the anticipation of the society and other organizations that refute from each other. The

purpose of tax practitioner is to make sure that the clients are payment the required sum of

tax. These payments would not held be taxable for the clients (Murphy and Higgins 2016).

However, the tax practitioner is required to assure that they use the loopholes that are existing

the law for the client’s advantage. Simultaneously, adopting such kind of practices requires

huge amount of funds which can be employed for the benefit of the society.

Answer to requirement B:

Particulars Amount ($) Amount ($)

Net Accounting Profit Before Tax 6,20,500$

Add: Amounts no deductible and other amounts assessable

Accrued Interest 10,000$

Receipt of service fees 80,000$

Profit from sale of factory 5,36,000$

Profit from sale of shares 1,30,000$

Less: Capital loss bought forward 35,000$

Total Addback 13,41,500$

Less: Amounts deductible and amounts not assessable

Trading Stock 50,000$

Market Research expenses 25,000$

Interest on Loan 10,300$

Depreciation 1,12,000$

Entertainment expenses 32,500$

Total Subtraction 2,29,800$

Total Taxable Income 11,11,700$

Tax Payable 4,73,497$

Add: Medicare levy 22,234$

Less: PayG 1,02,500$

Total tax payable 3,93,231$

Manic Pty Ltd Tax Reconciliation

Part B:

Issue:

The notion of tax compliance is regarded as the challenging task for the tax

practitioner. The reason for rise in problem is due to the purpose of tax practitioner profession

and the anticipation of the society and other organizations that refute from each other. The

purpose of tax practitioner is to make sure that the clients are payment the required sum of

tax. These payments would not held be taxable for the clients (Murphy and Higgins 2016).

However, the tax practitioner is required to assure that they use the loopholes that are existing

the law for the client’s advantage. Simultaneously, adopting such kind of practices requires

huge amount of funds which can be employed for the benefit of the society.

8TAXATION LAW

Analysis:

In the modern age, avoiding tax has turn out to be the most argued topics as publics

are reliant on the government expenses for overall growth of the nation. The systematic tax

avoidance act as the major threat for the government when measures are taken by the

government reduce the gap of economic inequalities (Hoffman et al. 2014). Taxes are usually

applied on the profits that are derived by the organizations however in the current age the

profits can be adjusted against several non-cash and non-real expenses.

The accountants use the loopholes and facilitates the client companies to lower the

burden of taxation. The accounts are required to preserve the ethical factors of their

profession and disregard the unethical practices which may hamper the growth of the society

at large (Hill and Mancino 2014). The accounts are required to assure that the tax advantage

that are accrued in the direction of company are authentic and valid.

Critique:

The accusation that business and large corporate firms uses the loopholes that are

present in the law to avoid the tax is regarded as correct thing but the simultaneously it is held

as inconclusive. Alternatively, the companies cannot be held at fault as there are numerous

loopholes in the provisions that is created by state. The objective of the company is increase

the return for its shareholders. On noticing that big business firms are able to lower the

burden of taxation the companies would continue their operations without being hindered

(Pope, Rupert and Anderson 2017). With that being said large corporate firms are required to

return the society and should use the correct resources. Else the society would take away the

powers that is granted to the corporate firms.

Analysis:

In the modern age, avoiding tax has turn out to be the most argued topics as publics

are reliant on the government expenses for overall growth of the nation. The systematic tax

avoidance act as the major threat for the government when measures are taken by the

government reduce the gap of economic inequalities (Hoffman et al. 2014). Taxes are usually

applied on the profits that are derived by the organizations however in the current age the

profits can be adjusted against several non-cash and non-real expenses.

The accountants use the loopholes and facilitates the client companies to lower the

burden of taxation. The accounts are required to preserve the ethical factors of their

profession and disregard the unethical practices which may hamper the growth of the society

at large (Hill and Mancino 2014). The accounts are required to assure that the tax advantage

that are accrued in the direction of company are authentic and valid.

Critique:

The accusation that business and large corporate firms uses the loopholes that are

present in the law to avoid the tax is regarded as correct thing but the simultaneously it is held

as inconclusive. Alternatively, the companies cannot be held at fault as there are numerous

loopholes in the provisions that is created by state. The objective of the company is increase

the return for its shareholders. On noticing that big business firms are able to lower the

burden of taxation the companies would continue their operations without being hindered

(Pope, Rupert and Anderson 2017). With that being said large corporate firms are required to

return the society and should use the correct resources. Else the society would take away the

powers that is granted to the corporate firms.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Conclusion:

On a conclusive note, to address the government issues, the accountants and the

corporations are required to discharge their duties collectively. The government is required to

make sure that there is no form of loophole in the tax provision as any loopholes can be

exploited for personal benefit. The accounts are required to follow the ethical practices at the

time of executing their duties and the organizations are required to refrain from undertaking

any form of unwarranted benefits of the available resources which is granted by the

shareholders with the objective of creating value for them and for the society as well.

Conclusion:

On a conclusive note, to address the government issues, the accountants and the

corporations are required to discharge their duties collectively. The government is required to

make sure that there is no form of loophole in the tax provision as any loopholes can be

exploited for personal benefit. The accounts are required to follow the ethical practices at the

time of executing their duties and the organizations are required to refrain from undertaking

any form of unwarranted benefits of the available resources which is granted by the

shareholders with the objective of creating value for them and for the society as well.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Reference List:

Barkoczy, S., 2016. Foundations of taxation law 2016. OUP Catalogue.

Blakelock, S. and King, P., 2017. Taxation law: The advance of ATO data

matching. Proctor, The, 37(6), p.18.

Braithwaite, V. ed., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., Stark, W. and

Wende, S., 2015. Understanding the economy-wide efficiency and incidence of major

Australian taxes. Canberra: Treasury working paper, 2001.

Davis, A.K., Guenther, D.A., Krull, L.K. and Williams, B.M., 2015. Do socially responsible

firms pay more taxes?. The accounting review, 91(1), pp.47-68.

Fry, M., 2017. Australian taxation of offshore hubs: an examination of the law on the ability

of Australia to tax economic activity in offshore hubs and the position of the Australian

Taxation Office. The APPEA Journal, 57(1), pp.49-63.

Hill, F.R. and Mancino, D.M., 2014. Taxation of exempt organizations.

Hoffman, W.H., Raabe, W.A., Maloney, D.M., Young, J.C. and Smith, J.E., 2014. South-

Western Federal Taxation 2015: Corporations, Partnerships, Estates and Trusts. Nelson

Education.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Murphy, K.E. and Higgins, M., 2016. Concepts in Federal Taxation 2017. Cengage

Learning.

Reference List:

Barkoczy, S., 2016. Foundations of taxation law 2016. OUP Catalogue.

Blakelock, S. and King, P., 2017. Taxation law: The advance of ATO data

matching. Proctor, The, 37(6), p.18.

Braithwaite, V. ed., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., Stark, W. and

Wende, S., 2015. Understanding the economy-wide efficiency and incidence of major

Australian taxes. Canberra: Treasury working paper, 2001.

Davis, A.K., Guenther, D.A., Krull, L.K. and Williams, B.M., 2015. Do socially responsible

firms pay more taxes?. The accounting review, 91(1), pp.47-68.

Fry, M., 2017. Australian taxation of offshore hubs: an examination of the law on the ability

of Australia to tax economic activity in offshore hubs and the position of the Australian

Taxation Office. The APPEA Journal, 57(1), pp.49-63.

Hill, F.R. and Mancino, D.M., 2014. Taxation of exempt organizations.

Hoffman, W.H., Raabe, W.A., Maloney, D.M., Young, J.C. and Smith, J.E., 2014. South-

Western Federal Taxation 2015: Corporations, Partnerships, Estates and Trusts. Nelson

Education.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Murphy, K.E. and Higgins, M., 2016. Concepts in Federal Taxation 2017. Cengage

Learning.

11TAXATION LAW

Pope, T.R., Rupert, T.J. and Anderson, K.E., 2017. Pearson's Federal Taxation 2018

Corporations, Partnerships, Estates & Trusts. Pearson.

Robin and Barkoczy woellner (stephen & murphy, shirley et al.), 2018. Australian taxation

law 2018. OXFORD University Press.

Robin, H., 2017. Australian taxation law 2017. Oxford University Press.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, pp.1069-1075.

Schenk, D.H., 2017. Federal Taxation of S Corporations. Law Journal Press.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

Pope, T.R., Rupert, T.J. and Anderson, K.E., 2017. Pearson's Federal Taxation 2018

Corporations, Partnerships, Estates & Trusts. Pearson.

Robin and Barkoczy woellner (stephen & murphy, shirley et al.), 2018. Australian taxation

law 2018. OXFORD University Press.

Robin, H., 2017. Australian taxation law 2017. Oxford University Press.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, pp.1069-1075.

Schenk, D.H., 2017. Federal Taxation of S Corporations. Law Journal Press.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

![Taxation Law: Spriggs v Federal Commissioner of Taxation [2007]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fdocument%2Fpages%2Fspriggs-taxation-law-case-page-2.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.