Taxation Law Report: Analysis of Tax Issues and Regulations

VerifiedAdded on 2020/04/01

|9

|1881

|472

Report

AI Summary

This report delves into various aspects of Australian taxation law, presenting five distinct case studies. The first case examines the computation of taxable net capital gains or losses, considering asset acquisitions and disposals. The second case focuses on fringe benefits tax, specifically concerning a bank executive's loan with a special interest rate. The third case analyzes the impact of profit and loss allocation in a rental property scenario owned by joint tenants. The fourth case explores tax avoidance through the Duke of Westminster's case, discussing relevant principles and their applicability in Australia. Finally, the fifth case assesses the tax implications of timber sales from a landowner's property. Each case includes an issue, relevant regulations, applicability, and a conclusion, providing a comprehensive overview of the taxation principles involved. The report also includes relevant references.

Assessment task 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

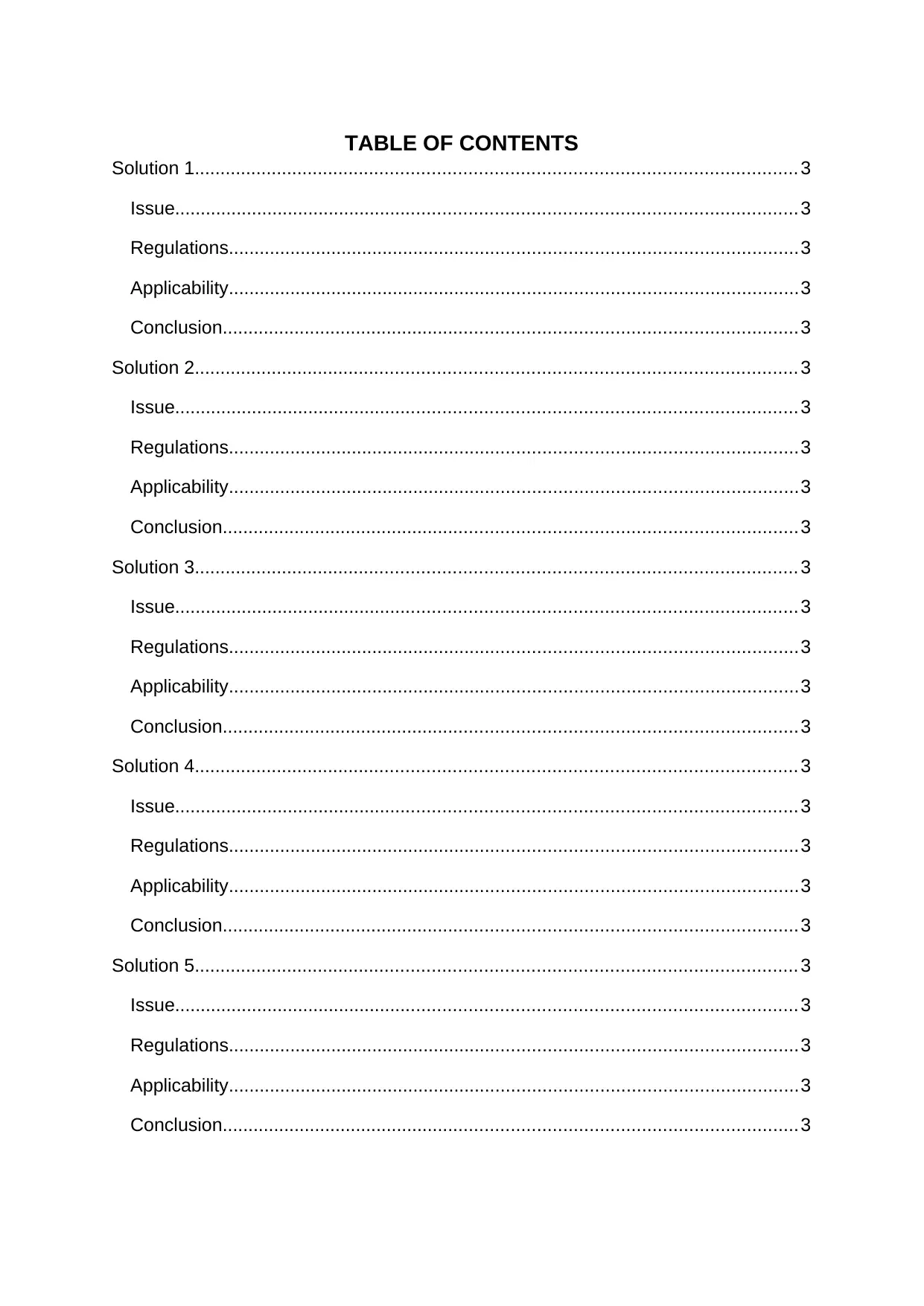

TABLE OF CONTENTS

Solution 1.................................................................................................................... 3

Issue........................................................................................................................ 3

Regulations..............................................................................................................3

Applicability..............................................................................................................3

Conclusion...............................................................................................................3

Solution 2.................................................................................................................... 3

Issue........................................................................................................................ 3

Regulations..............................................................................................................3

Applicability..............................................................................................................3

Conclusion...............................................................................................................3

Solution 3.................................................................................................................... 3

Issue........................................................................................................................ 3

Regulations..............................................................................................................3

Applicability..............................................................................................................3

Conclusion...............................................................................................................3

Solution 4.................................................................................................................... 3

Issue........................................................................................................................ 3

Regulations..............................................................................................................3

Applicability..............................................................................................................3

Conclusion...............................................................................................................3

Solution 5.................................................................................................................... 3

Issue........................................................................................................................ 3

Regulations..............................................................................................................3

Applicability..............................................................................................................3

Conclusion...............................................................................................................3

Solution 1.................................................................................................................... 3

Issue........................................................................................................................ 3

Regulations..............................................................................................................3

Applicability..............................................................................................................3

Conclusion...............................................................................................................3

Solution 2.................................................................................................................... 3

Issue........................................................................................................................ 3

Regulations..............................................................................................................3

Applicability..............................................................................................................3

Conclusion...............................................................................................................3

Solution 3.................................................................................................................... 3

Issue........................................................................................................................ 3

Regulations..............................................................................................................3

Applicability..............................................................................................................3

Conclusion...............................................................................................................3

Solution 4.................................................................................................................... 3

Issue........................................................................................................................ 3

Regulations..............................................................................................................3

Applicability..............................................................................................................3

Conclusion...............................................................................................................3

Solution 5.................................................................................................................... 3

Issue........................................................................................................................ 3

Regulations..............................................................................................................3

Applicability..............................................................................................................3

Conclusion...............................................................................................................3

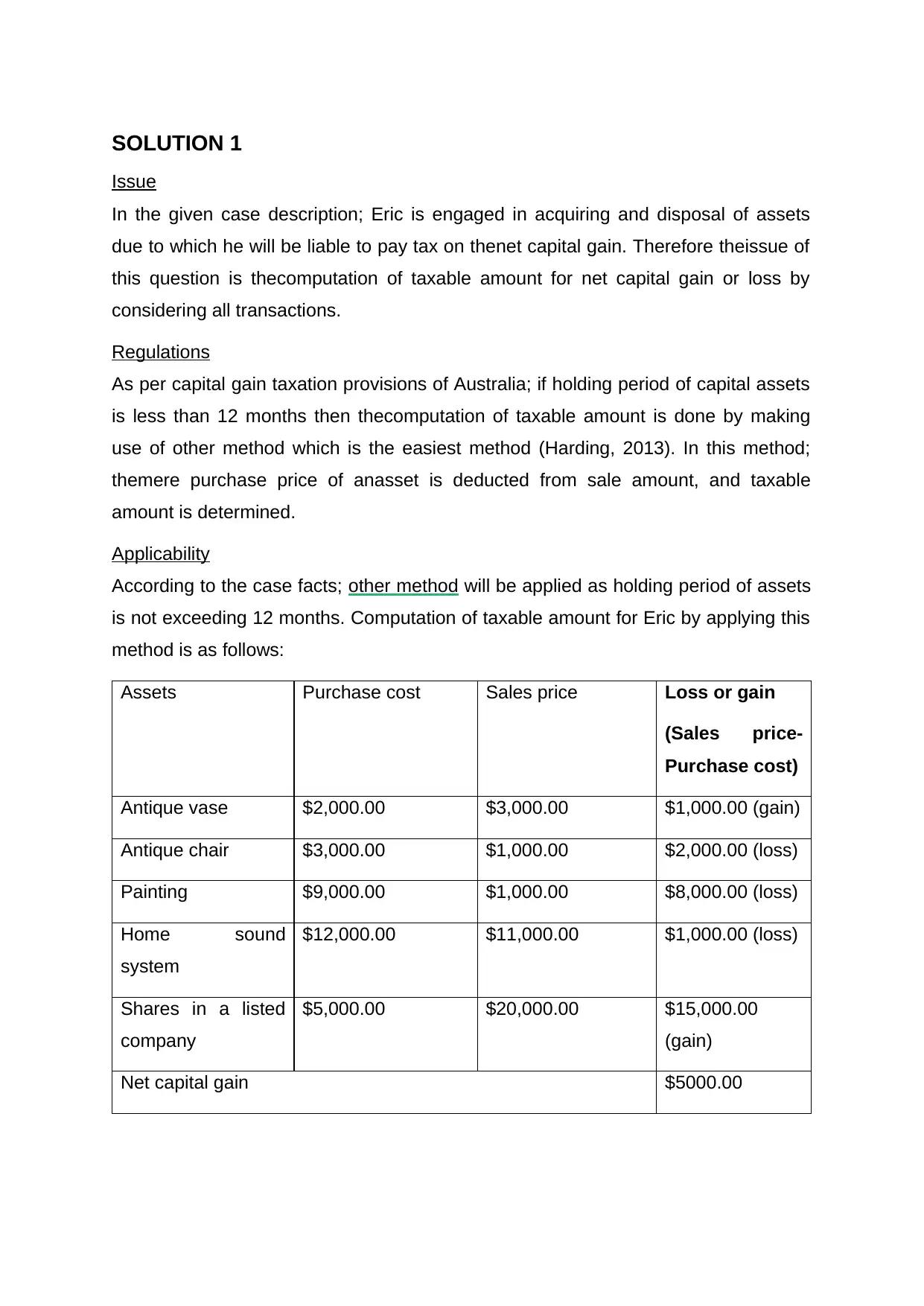

SOLUTION 1

Issue

In the given case description; Eric is engaged in acquiring and disposal of assets

due to which he will be liable to pay tax on thenet capital gain. Therefore theissue of

this question is thecomputation of taxable amount for net capital gain or loss by

considering all transactions.

Regulations

As per capital gain taxation provisions of Australia; if holding period of capital assets

is less than 12 months then thecomputation of taxable amount is done by making

use of other method which is the easiest method (Harding, 2013). In this method;

themere purchase price of anasset is deducted from sale amount, and taxable

amount is determined.

Applicability

According to the case facts; other method will be applied as holding period of assets

is not exceeding 12 months. Computation of taxable amount for Eric by applying this

method is as follows:

Assets Purchase cost Sales price Loss or gain

(Sales price-

Purchase cost)

Antique vase $2,000.00 $3,000.00 $1,000.00 (gain)

Antique chair $3,000.00 $1,000.00 $2,000.00 (loss)

Painting $9,000.00 $1,000.00 $8,000.00 (loss)

Home sound

system

$12,000.00 $11,000.00 $1,000.00 (loss)

Shares in a listed

company

$5,000.00 $20,000.00 $15,000.00

(gain)

Net capital gain $5000.00

Issue

In the given case description; Eric is engaged in acquiring and disposal of assets

due to which he will be liable to pay tax on thenet capital gain. Therefore theissue of

this question is thecomputation of taxable amount for net capital gain or loss by

considering all transactions.

Regulations

As per capital gain taxation provisions of Australia; if holding period of capital assets

is less than 12 months then thecomputation of taxable amount is done by making

use of other method which is the easiest method (Harding, 2013). In this method;

themere purchase price of anasset is deducted from sale amount, and taxable

amount is determined.

Applicability

According to the case facts; other method will be applied as holding period of assets

is not exceeding 12 months. Computation of taxable amount for Eric by applying this

method is as follows:

Assets Purchase cost Sales price Loss or gain

(Sales price-

Purchase cost)

Antique vase $2,000.00 $3,000.00 $1,000.00 (gain)

Antique chair $3,000.00 $1,000.00 $2,000.00 (loss)

Painting $9,000.00 $1,000.00 $8,000.00 (loss)

Home sound

system

$12,000.00 $11,000.00 $1,000.00 (loss)

Shares in a listed

company

$5,000.00 $20,000.00 $15,000.00

(gain)

Net capital gain $5000.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Conclusion

According to cited computation taxable amount for Eric is $5000.00.

SOLUTION 2

Issue

Brian, a bank executive and was provided with the three-year loan of $1m at a

special interest rate, i.e. 1% pa ( monthly instalments payable) as a part of his salary

package. On 1 April 2016, the loan was provided to him. 40% of the funds borrowed

were used for income generating purposes by Bill. Bill also met his interest

payments obligations with these borrowed funds. Thusissue, in this case, is

thecomputation of taxable amount by applying provisions of fringe benefits tax in

Australia by considered all three situations.

Regulations

Fringe benefits are payable on non-monetary benefits provided by theemployer to

anemployee in Australia. In thecontext of theloan; fringe benefits tax is payable on

thedifferent amount of interest charged by theemployer and standard interest

computed as per statutory rates (Woellner and et.al. 2016). For 2016 rate is 5.65%.

Applicability

By applicability of cited provisions; thetaxable amount for Brian is as follows:

Particulars Calculation Amount

The amount of interest payable by

Brain

$ 1,000,000∗1 % $10,000.00

The amount of interest as per

statutory interest rate

$ 1,000,000∗5.65 % $56,500.00

The taxable value of loan fringe

benefit

$ 56,500.00−$ 10,000.00 $46,500.00

According to cited computation taxable amount for Eric is $5000.00.

SOLUTION 2

Issue

Brian, a bank executive and was provided with the three-year loan of $1m at a

special interest rate, i.e. 1% pa ( monthly instalments payable) as a part of his salary

package. On 1 April 2016, the loan was provided to him. 40% of the funds borrowed

were used for income generating purposes by Bill. Bill also met his interest

payments obligations with these borrowed funds. Thusissue, in this case, is

thecomputation of taxable amount by applying provisions of fringe benefits tax in

Australia by considered all three situations.

Regulations

Fringe benefits are payable on non-monetary benefits provided by theemployer to

anemployee in Australia. In thecontext of theloan; fringe benefits tax is payable on

thedifferent amount of interest charged by theemployer and standard interest

computed as per statutory rates (Woellner and et.al. 2016). For 2016 rate is 5.65%.

Applicability

By applicability of cited provisions; thetaxable amount for Brian is as follows:

Particulars Calculation Amount

The amount of interest payable by

Brain

$ 1,000,000∗1 % $10,000.00

The amount of interest as per

statutory interest rate

$ 1,000,000∗5.65 % $56,500.00

The taxable value of loan fringe

benefit

$ 56,500.00−$ 10,000.00 $46,500.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

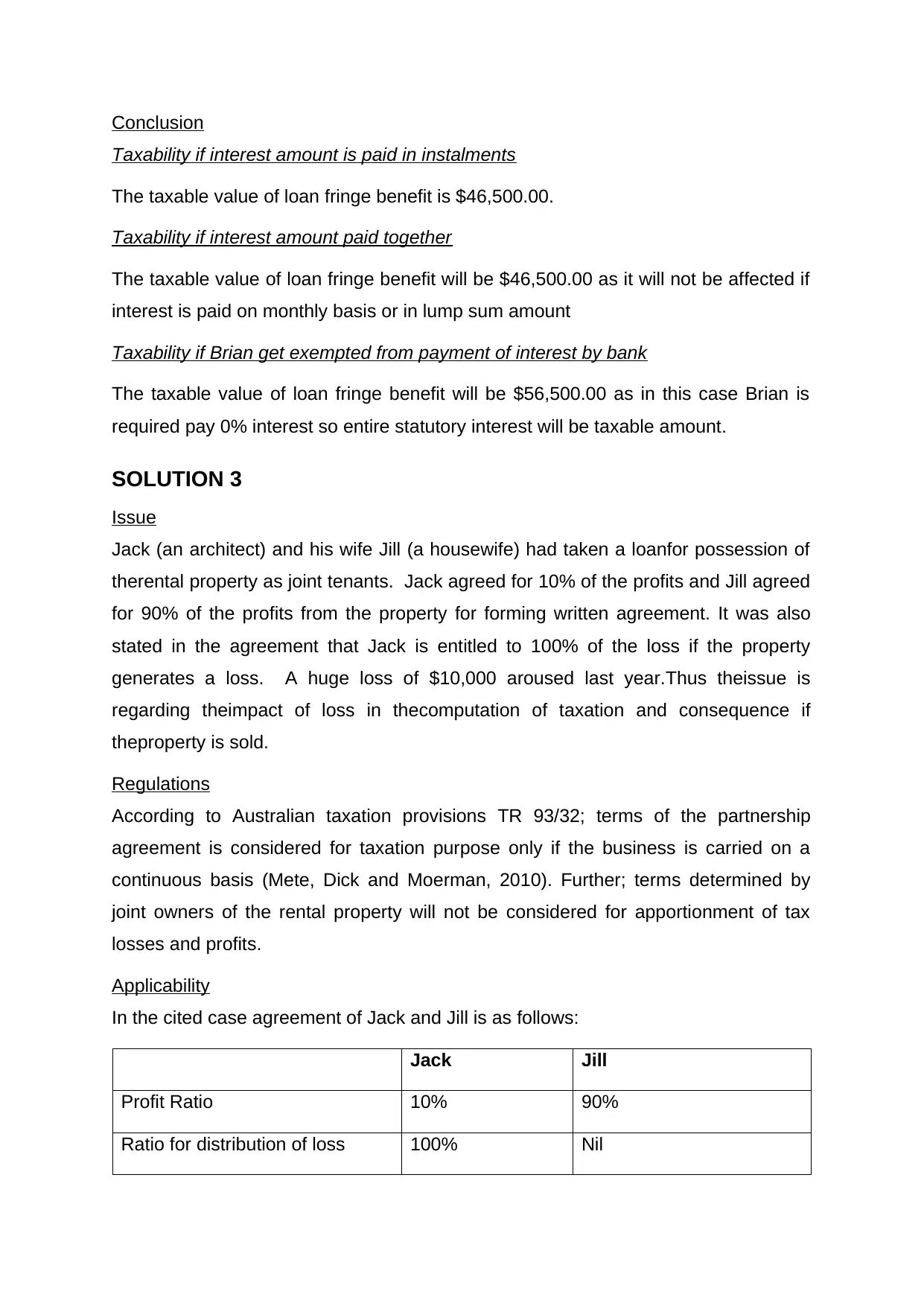

Conclusion

Taxability if interest amount is paid in instalments

The taxable value of loan fringe benefit is $46,500.00.

Taxability if interest amount paid together

The taxable value of loan fringe benefit will be $46,500.00 as it will not be affected if

interest is paid on monthly basis or in lump sum amount

Taxability if Brian get exempted from payment of interest by bank

The taxable value of loan fringe benefit will be $56,500.00 as in this case Brian is

required pay 0% interest so entire statutory interest will be taxable amount.

SOLUTION 3

Issue

Jack (an architect) and his wife Jill (a housewife) had taken a loanfor possession of

therental property as joint tenants. Jack agreed for 10% of the profits and Jill agreed

for 90% of the profits from the property for forming written agreement. It was also

stated in the agreement that Jack is entitled to 100% of the loss if the property

generates a loss. A huge loss of $10,000 aroused last year.Thus theissue is

regarding theimpact of loss in thecomputation of taxation and consequence if

theproperty is sold.

Regulations

According to Australian taxation provisions TR 93/32; terms of the partnership

agreement is considered for taxation purpose only if the business is carried on a

continuous basis (Mete, Dick and Moerman, 2010). Further; terms determined by

joint owners of the rental property will not be considered for apportionment of tax

losses and profits.

Applicability

In the cited case agreement of Jack and Jill is as follows:

Jack Jill

Profit Ratio 10% 90%

Ratio for distribution of loss 100% Nil

Taxability if interest amount is paid in instalments

The taxable value of loan fringe benefit is $46,500.00.

Taxability if interest amount paid together

The taxable value of loan fringe benefit will be $46,500.00 as it will not be affected if

interest is paid on monthly basis or in lump sum amount

Taxability if Brian get exempted from payment of interest by bank

The taxable value of loan fringe benefit will be $56,500.00 as in this case Brian is

required pay 0% interest so entire statutory interest will be taxable amount.

SOLUTION 3

Issue

Jack (an architect) and his wife Jill (a housewife) had taken a loanfor possession of

therental property as joint tenants. Jack agreed for 10% of the profits and Jill agreed

for 90% of the profits from the property for forming written agreement. It was also

stated in the agreement that Jack is entitled to 100% of the loss if the property

generates a loss. A huge loss of $10,000 aroused last year.Thus theissue is

regarding theimpact of loss in thecomputation of taxation and consequence if

theproperty is sold.

Regulations

According to Australian taxation provisions TR 93/32; terms of the partnership

agreement is considered for taxation purpose only if the business is carried on a

continuous basis (Mete, Dick and Moerman, 2010). Further; terms determined by

joint owners of the rental property will not be considered for apportionment of tax

losses and profits.

Applicability

In the cited case agreement of Jack and Jill is as follows:

Jack Jill

Profit Ratio 10% 90%

Ratio for distribution of loss 100% Nil

However, they are not carrying on business due to which terms of their agreement

will not be applicable for computation of taxation.

Conclusion

Allocation of revenue loss

The loss occurred in the previous year will be allocated in the ratio of 1:1 asthey are

not carrying on business due to which terms of their agreement will not be applicable

for computation of taxation.

Allocation of capital gain or loss

Similar provisions will be applied for allocation of capital gain or loss among partners.

QUESTION 4

Case

The case herewith mentioned in the file is of tax avoidance with reference to Duke of

Westminster's and IRC, in which The Duke of Westminster has employed a gardener

who was offered with a salary from Duke's substantial post-tax income. However, the

Duke has reduced tax liability through drew up a covenant instead of paying salary,

with the similar amount. In this regard, Duke was entitled to claim a deduction thus

tax liability and surtax were reduced (Likhovski, 2006). It can be justified that claims

are made for a single year or as an annual payment made.

Principle established in IRC v Duke of Westminster [1936] AC 1

According to the guidelines of taxation, it is illegal to avoid tax but tin this case Inland

Revenue Commissioners (IRC) would not be able to win the case against the Duke.

The court has given words that an individual is allowed to order the affairs, in respect

to the tax attached under appropriate Acts. Nonetheless, in this case the party was

ungrateful and the fellow tax-payers were too clever, so they were not willing to pay

taxes. This case is said to be a case in which people were seeking to avoid tax

legally by making the tax structure more complex. However, the other principle like

“Ramsay principle” that are established by court are said to be under a restrictive

approach which are taken to reduce the cases of tax avoidance (Simpson, 2005).

As per the laws of this principle, if transaction made by the party is pre-arranged

will not be applicable for computation of taxation.

Conclusion

Allocation of revenue loss

The loss occurred in the previous year will be allocated in the ratio of 1:1 asthey are

not carrying on business due to which terms of their agreement will not be applicable

for computation of taxation.

Allocation of capital gain or loss

Similar provisions will be applied for allocation of capital gain or loss among partners.

QUESTION 4

Case

The case herewith mentioned in the file is of tax avoidance with reference to Duke of

Westminster's and IRC, in which The Duke of Westminster has employed a gardener

who was offered with a salary from Duke's substantial post-tax income. However, the

Duke has reduced tax liability through drew up a covenant instead of paying salary,

with the similar amount. In this regard, Duke was entitled to claim a deduction thus

tax liability and surtax were reduced (Likhovski, 2006). It can be justified that claims

are made for a single year or as an annual payment made.

Principle established in IRC v Duke of Westminster [1936] AC 1

According to the guidelines of taxation, it is illegal to avoid tax but tin this case Inland

Revenue Commissioners (IRC) would not be able to win the case against the Duke.

The court has given words that an individual is allowed to order the affairs, in respect

to the tax attached under appropriate Acts. Nonetheless, in this case the party was

ungrateful and the fellow tax-payers were too clever, so they were not willing to pay

taxes. This case is said to be a case in which people were seeking to avoid tax

legally by making the tax structure more complex. However, the other principle like

“Ramsay principle” that are established by court are said to be under a restrictive

approach which are taken to reduce the cases of tax avoidance (Simpson, 2005).

As per the laws of this principle, if transaction made by the party is pre-arranged

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

artificial step and is operated for no commercial purpose than it would not be legally

taken (Simpson, 2005)

Relevance of this principal in Australia

In the present scenario, the issue of tax avoidance has been increased in Australia,

and many of companies are taking advantages of the above mentioned case and its

relevance.

As in the case the liability of Duke is dramatically reduced for not paying salary just

to avoid tax is approved. However, companies are taking advantages of avoiding

and reducing taxable profit. The courts have considered that the fiscal jurisprudence

of Australia have been changed and principle of Duke of Westminster [1936] AC are

not applied, thus tax planers cannot stuck down to this and avoid artificial tax

deductions.

SOLUTION 5

Issue

The case scenario indicates the issue of assessing the receipts from a property and

the tax applied on it. Bill, who is the owner of a land which is covered from pine

trees, has an offer to use the land for grazing sheep. However, he is approached by

a company with a deal to pay him $1,000 for every 100 metres of timber which is

taken from the land. And the next deal is that the company is willing to pay lump sum

of $50,000 for granting the right to remove as much timber as required from his land.

The main issue faced by Bill is whether to pay taxes against the land against the

amount earned in both the cases.

Legal provisions for taxation

Case1: Disposal of standing timber that is not related to regular business

course

As per the taxation rules under TR 95/, taxpayer owns a property for the disposing of

timber, nonetheless, the decision of planting trees is to be taken for the purpose of

sale. The subsection 36(1) reveals the laws against disposal of timber and in other

situation the owner must operates the business of forest operation. Furthermore,

Subsection 36(1) says that trees are planted on leased provides entire ownership of

leased plants (Likhovski, 2006). Subsection 36(1) and 25(1) of TR 95, are applied in

the situation and Bill has to pay tax in bother the cases,

taken (Simpson, 2005)

Relevance of this principal in Australia

In the present scenario, the issue of tax avoidance has been increased in Australia,

and many of companies are taking advantages of the above mentioned case and its

relevance.

As in the case the liability of Duke is dramatically reduced for not paying salary just

to avoid tax is approved. However, companies are taking advantages of avoiding

and reducing taxable profit. The courts have considered that the fiscal jurisprudence

of Australia have been changed and principle of Duke of Westminster [1936] AC are

not applied, thus tax planers cannot stuck down to this and avoid artificial tax

deductions.

SOLUTION 5

Issue

The case scenario indicates the issue of assessing the receipts from a property and

the tax applied on it. Bill, who is the owner of a land which is covered from pine

trees, has an offer to use the land for grazing sheep. However, he is approached by

a company with a deal to pay him $1,000 for every 100 metres of timber which is

taken from the land. And the next deal is that the company is willing to pay lump sum

of $50,000 for granting the right to remove as much timber as required from his land.

The main issue faced by Bill is whether to pay taxes against the land against the

amount earned in both the cases.

Legal provisions for taxation

Case1: Disposal of standing timber that is not related to regular business

course

As per the taxation rules under TR 95/, taxpayer owns a property for the disposing of

timber, nonetheless, the decision of planting trees is to be taken for the purpose of

sale. The subsection 36(1) reveals the laws against disposal of timber and in other

situation the owner must operates the business of forest operation. Furthermore,

Subsection 36(1) says that trees are planted on leased provides entire ownership of

leased plants (Likhovski, 2006). Subsection 36(1) and 25(1) of TR 95, are applied in

the situation and Bill has to pay tax in bother the cases,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Rights disposal to standing timber

Tax payer is operating a business of forest operation should remove the standing

timber, the case revealed against cutting the standing timber. The subsection 25(1),

is applied to the case as the income is accessible from the regular business. The

situation is applicable at the time when disposal will take place (Schofield, 2008).

Application and conclusion

However, subsection 36(1) and 25(1) of TR 95, are applied in the situation

and Bill has to pay tax in bother the cases, whether he received $1000 the income

the section 36(1) is applied and in case lump sum amount subsection 25(1) is

applicable.

Tax payer is operating a business of forest operation should remove the standing

timber, the case revealed against cutting the standing timber. The subsection 25(1),

is applied to the case as the income is accessible from the regular business. The

situation is applicable at the time when disposal will take place (Schofield, 2008).

Application and conclusion

However, subsection 36(1) and 25(1) of TR 95, are applied in the situation

and Bill has to pay tax in bother the cases, whether he received $1000 the income

the section 36(1) is applied and in case lump sum amount subsection 25(1) is

applicable.

REFERENCES

Harding, M., 2013. Taxation of dividend, interest, and capital gain income.

Likhovski, A., 2006. Tax law and public opinion: Explaining IRC v. Duke of

Westminster. Sage

Mete, P., Dick, C. and Moerman, L., 2010. Creating institutional meaning:

Accounting and taxation law perspectives of carbon permits. Critical Perspectives on

Accounting, 21(7), pp.619-630.

Schofield, R., 2008. Taxation under the early Tudors 1485-1547. John Wiley & Sons.

Simpson, E., 2005. The Ramsay Principle: A Curious Incident of Judicial

Reticence?. British Tax Review, 4, p.358.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian

Taxation Law 2016. OUP Catalogue.

Harding, M., 2013. Taxation of dividend, interest, and capital gain income.

Likhovski, A., 2006. Tax law and public opinion: Explaining IRC v. Duke of

Westminster. Sage

Mete, P., Dick, C. and Moerman, L., 2010. Creating institutional meaning:

Accounting and taxation law perspectives of carbon permits. Critical Perspectives on

Accounting, 21(7), pp.619-630.

Schofield, R., 2008. Taxation under the early Tudors 1485-1547. John Wiley & Sons.

Simpson, E., 2005. The Ramsay Principle: A Curious Incident of Judicial

Reticence?. British Tax Review, 4, p.358.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian

Taxation Law 2016. OUP Catalogue.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.