TAX 305 Taxation Law Assignment: Residency, Income and Taxation Issues

VerifiedAdded on 2022/09/17

|16

|3039

|25

Homework Assignment

AI Summary

This taxation law assignment, submitted for TAX 305, addresses the complexities of Australian taxation, focusing on residency and income. The assignment analyzes two case studies, examining whether individuals are considered Australian residents under the Income Tax Assessment Act (ITAA) 1936 and ITAA 1997, applying the resides test, domicile test, and 183-day test. It also explores the sourcing of income and its taxability. The assignment further delves into business versus hobby income, analyzing whether receipts from activities like painting constitute taxable income, considering factors like profit-making intention and commercial approach. Finally, it examines the tax treatment of various income sources, including business income, gifts, and employment income, and the deductibility of expenses, referencing relevant case law and taxation rulings to support the analysis. The assignment concludes with a detailed analysis of each case, providing definitive answers to the presented issues.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................3

Part A:........................................................................................................................................3

Issues:.....................................................................................................................................3

Rule:.......................................................................................................................................3

Application:............................................................................................................................5

Conclusion:............................................................................................................................6

Answer to Part B:.......................................................................................................................7

Issues:.....................................................................................................................................7

Rule:.......................................................................................................................................7

Application:............................................................................................................................8

Conclusion:............................................................................................................................8

Case Study 2: Part A:.................................................................................................................9

Issues:.....................................................................................................................................9

Rule:.......................................................................................................................................9

Application:............................................................................................................................9

Conclusion:..........................................................................................................................10

Case Study Three.....................................................................................................................10

Issues:...................................................................................................................................10

Rule:.....................................................................................................................................10

Application:..........................................................................................................................11

Table of Contents

Answer to question 1:.................................................................................................................3

Part A:........................................................................................................................................3

Issues:.....................................................................................................................................3

Rule:.......................................................................................................................................3

Application:............................................................................................................................5

Conclusion:............................................................................................................................6

Answer to Part B:.......................................................................................................................7

Issues:.....................................................................................................................................7

Rule:.......................................................................................................................................7

Application:............................................................................................................................8

Conclusion:............................................................................................................................8

Case Study 2: Part A:.................................................................................................................9

Issues:.....................................................................................................................................9

Rule:.......................................................................................................................................9

Application:............................................................................................................................9

Conclusion:..........................................................................................................................10

Case Study Three.....................................................................................................................10

Issues:...................................................................................................................................10

Rule:.....................................................................................................................................10

Application:..........................................................................................................................11

2TAXATION LAW

Conclusion:..........................................................................................................................13

References:...............................................................................................................................14

Conclusion:..........................................................................................................................13

References:...............................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Answer to question 1:

Part A:

Issues:

Will Rachel be held as Australian resident within the definition of

“section 6 (1),

ITAA 1936” for the applicable income year.

Rule:

As stated in

“taxation ruling of TR 98/17” the tax commissioner states that the

ordinary meaning of the term

“resides” under the definition of resident is provided within the

“subsection 6 (1), ITAA 1936” (Norbury 2019)

. The ruling is generally implemented on

those people that comes to Australia as the migrant, workers, teachers with pre-arranged

service agreements.

As explained in

“sec 6 (1), ITAA 1997” an Australian resident means a person that

resides in Australia and has permanent place of residence in Australia unless the

commissioner is content that the taxpayer has the perpetual home outside Australia and do

not have any intent of living in Australia (Harding and Scott 2015). The definition of

“sec 6

(1), ITAA 1997” provides four alternative test. These are as follows;

a. The Resides Test

b. The Domicile Test

c. The 183-Day Test

d. The commonwealth superannuation fund test

The Resides Test:

The word

“reside” here means to live on permanent basis or for significant time period

(Jones 2018). This test requires relevant considerations such as;

Answer to question 1:

Part A:

Issues:

Will Rachel be held as Australian resident within the definition of

“section 6 (1),

ITAA 1936” for the applicable income year.

Rule:

As stated in

“taxation ruling of TR 98/17” the tax commissioner states that the

ordinary meaning of the term

“resides” under the definition of resident is provided within the

“subsection 6 (1), ITAA 1936” (Norbury 2019)

. The ruling is generally implemented on

those people that comes to Australia as the migrant, workers, teachers with pre-arranged

service agreements.

As explained in

“sec 6 (1), ITAA 1997” an Australian resident means a person that

resides in Australia and has permanent place of residence in Australia unless the

commissioner is content that the taxpayer has the perpetual home outside Australia and do

not have any intent of living in Australia (Harding and Scott 2015). The definition of

“sec 6

(1), ITAA 1997” provides four alternative test. These are as follows;

a. The Resides Test

b. The Domicile Test

c. The 183-Day Test

d. The commonwealth superannuation fund test

The Resides Test:

The word

“reside” here means to live on permanent basis or for significant time period

(Jones 2018). This test requires relevant considerations such as;

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

a. Intention of existence in Australia

b. Family, employment or business relationship

c. Maintenance of location assets

d. Social and living preparation.

Weightage must be given in every factor. Similarly, in

“Iyengar v FCT (2011)” the

taxpayer was held as Australian resident who took up two year’s employment in overseas but

maintained his family home and relation in Australia.

Domicile Test:

An individual that has their home in Australia will remain an Australian citizen even

though they reside in overseas. A person may not be held Australian citizen if they satisfy the

ATO that they have chosen another country as their own permanent home. Relevant factor

such as durability of relation that a person has with a place in Australia is important. The law

court in

“Applegate v FCT (1979)” held that though Applegate had maintained his domicile

but has established a permanent home outside Australia (Idris 2018). A person intention to

live permanently or temporary is important factor.

The 183-Day test:

This test denotes the existence in Australian either constantly or in breaks for 183 days or

more.

Superannuation Fund Test:

This test is applied on those that has the membership of a specific commonwealth super fund.

Sources of Income:

a. Intention of existence in Australia

b. Family, employment or business relationship

c. Maintenance of location assets

d. Social and living preparation.

Weightage must be given in every factor. Similarly, in

“Iyengar v FCT (2011)” the

taxpayer was held as Australian resident who took up two year’s employment in overseas but

maintained his family home and relation in Australia.

Domicile Test:

An individual that has their home in Australia will remain an Australian citizen even

though they reside in overseas. A person may not be held Australian citizen if they satisfy the

ATO that they have chosen another country as their own permanent home. Relevant factor

such as durability of relation that a person has with a place in Australia is important. The law

court in

“Applegate v FCT (1979)” held that though Applegate had maintained his domicile

but has established a permanent home outside Australia (Idris 2018). A person intention to

live permanently or temporary is important factor.

The 183-Day test:

This test denotes the existence in Australian either constantly or in breaks for 183 days or

more.

Superannuation Fund Test:

This test is applied on those that has the membership of a specific commonwealth super fund.

Sources of Income:

5TAXATION LAW

In order to ascertain the sources of income it is necessary to determine the material

fact. The federal court in

“FCT v French (1957)” held that the liability to impose tax

originates where the services are carried on (Thuronyi and Brooks 2016).

Application:

The evidences obtained puts forward that Racheal came to Australia for twelve

months with a service agreement which required her to stay in Australia for 1st December

2019. Referring to

“sec 6 (1), ITAA 1936” four relevant test is applied in case of Racheal.

Resides Test:

Racheal will be treated as Australian dweller given she is considered to have “reside”

in Australia for significant time period. Denoting the taxation ruling of

“TR 98/17” Racheal

came to Australia with service contract and lives in a house provided by his company. Citing

“Iyengar v FCT (2011)” Racheal will be treated as Australian citizen because she has been

residing here for twelve months (Bankman et al. 2018). The factors that contributes to her

residency is her physical presence, her children accompanying Australia and maintained of

home in Australia.

Domicile Test:

Under the Domicile Test, Racheal has a fixed abode out of Australia. Citing the case

of

“FCT v Applegate (1979)” Racheal has the fixed dwelling out of Australia and she is not

a resident under this test.

The 183-Day Test:

Regardless of whether Racheal is considered Australian occupant under the “Resides

Test”, she will be treated as Australian citizen under the 183-day test because has been

present in Australia for more than 12 months of the relevant income year. Therefore, Racheal

In order to ascertain the sources of income it is necessary to determine the material

fact. The federal court in

“FCT v French (1957)” held that the liability to impose tax

originates where the services are carried on (Thuronyi and Brooks 2016).

Application:

The evidences obtained puts forward that Racheal came to Australia for twelve

months with a service agreement which required her to stay in Australia for 1st December

2019. Referring to

“sec 6 (1), ITAA 1936” four relevant test is applied in case of Racheal.

Resides Test:

Racheal will be treated as Australian dweller given she is considered to have “reside”

in Australia for significant time period. Denoting the taxation ruling of

“TR 98/17” Racheal

came to Australia with service contract and lives in a house provided by his company. Citing

“Iyengar v FCT (2011)” Racheal will be treated as Australian citizen because she has been

residing here for twelve months (Bankman et al. 2018). The factors that contributes to her

residency is her physical presence, her children accompanying Australia and maintained of

home in Australia.

Domicile Test:

Under the Domicile Test, Racheal has a fixed abode out of Australia. Citing the case

of

“FCT v Applegate (1979)” Racheal has the fixed dwelling out of Australia and she is not

a resident under this test.

The 183-Day Test:

Regardless of whether Racheal is considered Australian occupant under the “Resides

Test”, she will be treated as Australian citizen under the 183-day test because has been

present in Australia for more than 12 months of the relevant income year. Therefore, Racheal

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

has met the criteria of the 183-day test and she is an Australian resident under the meaning of

“sec 6 (1), ITAA 1936”.

Commonwealth Superannuation Test:

The commonwealth superannuation test is not relevant in the situation of Racheal

because she does not have any membership with any specific super fund.

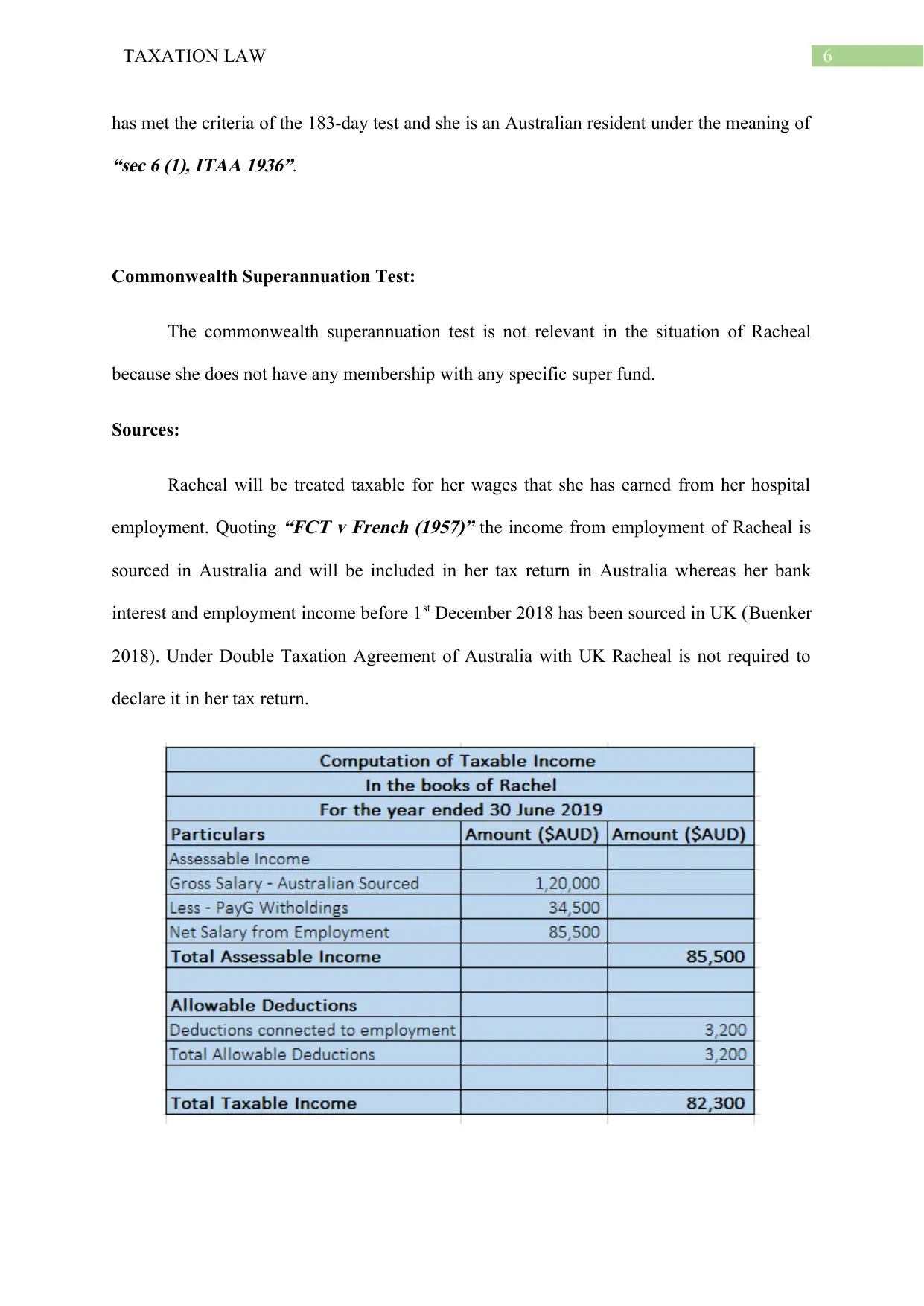

Sources:

Racheal will be treated taxable for her wages that she has earned from her hospital

employment. Quoting

“FCT v French (1957)” the income from employment of Racheal is

sourced in Australia and will be included in her tax return in Australia whereas her bank

interest and employment income before 1st December 2018 has been sourced in UK (Buenker

2018). Under Double Taxation Agreement of Australia with UK Racheal is not required to

declare it in her tax return.

has met the criteria of the 183-day test and she is an Australian resident under the meaning of

“sec 6 (1), ITAA 1936”.

Commonwealth Superannuation Test:

The commonwealth superannuation test is not relevant in the situation of Racheal

because she does not have any membership with any specific super fund.

Sources:

Racheal will be treated taxable for her wages that she has earned from her hospital

employment. Quoting

“FCT v French (1957)” the income from employment of Racheal is

sourced in Australia and will be included in her tax return in Australia whereas her bank

interest and employment income before 1st December 2018 has been sourced in UK (Buenker

2018). Under Double Taxation Agreement of Australia with UK Racheal is not required to

declare it in her tax return.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Conclusion:

Under the meaning of

“sec 6 (1), ITAA 1936” Racheal is an Australian citizen for

taxation purpose because she “resides” here and has also met the 183-day test. Her

employment income from Australian sources will attract tax liability since it is sourced in

Australia.

Answer to Part B:

Issues:

Is John an Australian citizen under the explanation specified in

“subsection 6 (1),

ITAA 1936”.

Rule:

Resides Test:

This test considers the behaviour while present in Australia to be treated consistent

with that of Australian resident. This includes the intention or objective of presence and

location of home or assets in Australia. The law court in

“Dempsey v FC of T (2014)” held

that taxpayer was working in construction industry of Saudi Arabia and was not held

Australian citizen (Schenk 2017). The judged relied heavily on the intention of taxpayer to

live out of Australia.

Domicile Test:

The Domicile Test is defined in

“Domicile Act 1982”. A person’s home represents a

lawful relation with the nation based on which a person is able to summon the country’s laws

as their own. A person’s home represents a place where the permanent home is located

(Mertens and Montiel Olea 2018). The court in

“Harding v FCT (2019)” held the taxpayer

was non-resident of Australia since the taxpayer had the permanent place of abode out of

Australia.

Conclusion:

Under the meaning of

“sec 6 (1), ITAA 1936” Racheal is an Australian citizen for

taxation purpose because she “resides” here and has also met the 183-day test. Her

employment income from Australian sources will attract tax liability since it is sourced in

Australia.

Answer to Part B:

Issues:

Is John an Australian citizen under the explanation specified in

“subsection 6 (1),

ITAA 1936”.

Rule:

Resides Test:

This test considers the behaviour while present in Australia to be treated consistent

with that of Australian resident. This includes the intention or objective of presence and

location of home or assets in Australia. The law court in

“Dempsey v FC of T (2014)” held

that taxpayer was working in construction industry of Saudi Arabia and was not held

Australian citizen (Schenk 2017). The judged relied heavily on the intention of taxpayer to

live out of Australia.

Domicile Test:

The Domicile Test is defined in

“Domicile Act 1982”. A person’s home represents a

lawful relation with the nation based on which a person is able to summon the country’s laws

as their own. A person’s home represents a place where the permanent home is located

(Mertens and Montiel Olea 2018). The court in

“Harding v FCT (2019)” held the taxpayer

was non-resident of Australia since the taxpayer had the permanent place of abode out of

Australia.

8TAXATION LAW

The 183-day Test:

A person is treated as Australian resident given they are physically existent in

Australia for more than six months of a year (Hoynes and Rothstein 2016).

Commonwealth Superannuation test:

This test is applied on members that has membership with the fund.

Application:

In order to ascertain the tax residency status of John the four relevant resident test are used.

Residency Test:

John has not been present in Australia for a considerable time period during the

income year. John has taken all his personal belongings to Brunei. Citing the example of

“Dempsey v FCT (2014)” John do not intend to return Australia (Oishi, Kushlev and

Schimmack 2018). Therefore, John is not an Australian resident under this test.

Domicile Test:

John following his move to Brunei for employment purpose has not illustrated

conclusively that his choice of home is Australia. To support this view, it is noticed that he

renewed his lease apartment in Brunei for another 12 months. Quoting

“Harding v FCT

(2019)” the circumstances gathered suggest that his permanent home is in Brunei.

183-Day Test:

John during 2017/18 and 2018/19 was not present in Australia physically. Therefore, he is not

a citizen of Australia.

Commonwealth Superannuation Test:

This test is irrelevant in the case of John.

The 183-day Test:

A person is treated as Australian resident given they are physically existent in

Australia for more than six months of a year (Hoynes and Rothstein 2016).

Commonwealth Superannuation test:

This test is applied on members that has membership with the fund.

Application:

In order to ascertain the tax residency status of John the four relevant resident test are used.

Residency Test:

John has not been present in Australia for a considerable time period during the

income year. John has taken all his personal belongings to Brunei. Citing the example of

“Dempsey v FCT (2014)” John do not intend to return Australia (Oishi, Kushlev and

Schimmack 2018). Therefore, John is not an Australian resident under this test.

Domicile Test:

John following his move to Brunei for employment purpose has not illustrated

conclusively that his choice of home is Australia. To support this view, it is noticed that he

renewed his lease apartment in Brunei for another 12 months. Quoting

“Harding v FCT

(2019)” the circumstances gathered suggest that his permanent home is in Brunei.

183-Day Test:

John during 2017/18 and 2018/19 was not present in Australia physically. Therefore, he is not

a citizen of Australia.

Commonwealth Superannuation Test:

This test is irrelevant in the case of John.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Conclusion:

John has passed successfully all the four alternative test and he is a foreign resident

under

“sec 995-1 (1), ITAA 1997”.

Case Study 2: Part A:

Issues:

Whether the receipts from paintings will be treated as business or hobby under

“section 995-1, ITAA 1997”?

Rule:

According to

“sec 6-5, ITAA 1997”, business gains are treated as ordinary income

whereas the non-business gains are treated as hobby and it is not treated taxable. It is

necessary to understand when the hobby or recreational activity becomes business (Auerbach

and Hassett 2015). There are some important factors that is considered by the court such as

the existent of profit making intentions. The court in

“Stone v FCT (2005)” found that lack

of profit making intention does not prevent an activity from being considered as business.

The extent of events together with the nature of capital and turnover forms the vital indicators

of business activity. It also includes whether the taxpayer has adopted any commercial

approach or not.

Application:

Nadine in her free time paints landscape for relieving her accounting work stress.

Following one of her friend’s suggestion Nadine decides to display three paintings for sale in

market. She made $4,500 from sales. The receipt of $4,500 by Nadine from selling the

paintings does not constitute any business activity because she did painting to release her

work stress and mainly for recreational purpose. Citing

“Stone v FCT (2005)” Nadine lacked

profit deriving intent because there was no such planning or any significant investment made

Conclusion:

John has passed successfully all the four alternative test and he is a foreign resident

under

“sec 995-1 (1), ITAA 1997”.

Case Study 2: Part A:

Issues:

Whether the receipts from paintings will be treated as business or hobby under

“section 995-1, ITAA 1997”?

Rule:

According to

“sec 6-5, ITAA 1997”, business gains are treated as ordinary income

whereas the non-business gains are treated as hobby and it is not treated taxable. It is

necessary to understand when the hobby or recreational activity becomes business (Auerbach

and Hassett 2015). There are some important factors that is considered by the court such as

the existent of profit making intentions. The court in

“Stone v FCT (2005)” found that lack

of profit making intention does not prevent an activity from being considered as business.

The extent of events together with the nature of capital and turnover forms the vital indicators

of business activity. It also includes whether the taxpayer has adopted any commercial

approach or not.

Application:

Nadine in her free time paints landscape for relieving her accounting work stress.

Following one of her friend’s suggestion Nadine decides to display three paintings for sale in

market. She made $4,500 from sales. The receipt of $4,500 by Nadine from selling the

paintings does not constitute any business activity because she did painting to release her

work stress and mainly for recreational purpose. Citing

“Stone v FCT (2005)” Nadine lacked

profit deriving intent because there was no such planning or any significant investment made

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

(Woellner et al. 2016). Additionally, neither did she adopted any commercial approach to sell

the paintings and only attended market when she had one to sell.

Conclusion:

On a conclusive note, activities of Nadine constitute a hobby for recreational purpose

and the receipts are non-taxable as income.

Case Study Three

Issues:

Whether the receipts earned from the ordinary business course and employment will be

treated taxable as ordinary income under

“section 6-5, ITAA 1997”.

Rule:

As per

“section 6-5, ITAA 1997” usually majority of the business receipts are held as

ordinary income (Barkoczy 2016). Gains are not treated as income because it does not have

income character. In

“Hayes v FCT (1956)” shares received by accountant from company

boss was not held as income.

Where a taxpayer receives payment for rendering personal service then the income is

treated taxable under

“section 6-5, ITAA 1997” as ordinary earnings. The court in

“Dean v

FCT (1997)” employment remuneration was treated as taxable as ordinary income.

Where a taxpayer receives interest it is treated as taxable under the

“section 15-35”.

Similarly, windfall gains are not considered taxable earnings (Woellner et al. 2016). The

decision made in

“Moore v Griffiths (1972)” stated that simple prize winnings are treated as

income.

(Woellner et al. 2016). Additionally, neither did she adopted any commercial approach to sell

the paintings and only attended market when she had one to sell.

Conclusion:

On a conclusive note, activities of Nadine constitute a hobby for recreational purpose

and the receipts are non-taxable as income.

Case Study Three

Issues:

Whether the receipts earned from the ordinary business course and employment will be

treated taxable as ordinary income under

“section 6-5, ITAA 1997”.

Rule:

As per

“section 6-5, ITAA 1997” usually majority of the business receipts are held as

ordinary income (Barkoczy 2016). Gains are not treated as income because it does not have

income character. In

“Hayes v FCT (1956)” shares received by accountant from company

boss was not held as income.

Where a taxpayer receives payment for rendering personal service then the income is

treated taxable under

“section 6-5, ITAA 1997” as ordinary earnings. The court in

“Dean v

FCT (1997)” employment remuneration was treated as taxable as ordinary income.

Where a taxpayer receives interest it is treated as taxable under the

“section 15-35”.

Similarly, windfall gains are not considered taxable earnings (Woellner et al. 2016). The

decision made in

“Moore v Griffiths (1972)” stated that simple prize winnings are treated as

income.

11TAXATION LAW

As per

“section 8-1, ITAA 1997” an individual is only permitted to obtain deduction

from their assessable income for expenses that are incurred at the time of generating

assessable income or occurred at the time of performing business activities. While in negative

limbs of

“sec 8-1(2)”, no deduction is allowed for expenses that are capital or private in

nature.

The ATO states that small business owners having annual revenue of not greater than

$10,000 are permitted to immediately write off the assets which is bought for $20,000 or

lower. While the

“Taxation Ruling of TR 2004/6” explains that for claiming the expenses

associated to meal, allowances there should be written record for the same (Thuronyi and

Brooks 2016). Travel between home and work is regarded as private expenses and not

deductions is allowed. The court in

“Lunney v FCT (1958)” held that no deduction for travel

between home and work is allowed.

Application:

Sam received $450,000 from his accounting business. The receipt will be treated as

income from business and it is taxable as ordinary income under

“section 6-5, ITAA 1997”.

He also received a wedding gift of $10,000. Referring to

“Hayes v FCT (1956)” the gift is

non-taxable income since it was received out of personal relationship. The advertisement

incentives received by Sam from publishing company is a taxable ordinary income under

“section 6-5, ITAA 1997”.

A salary of $34,000 was received by Sam from his part-time employment in

University. The salary is an income from personal exertion and citing

“Dean v FCT (1997)”

it will be taxable as ordinary income under

“section 6-5, ITAA 1997”. Whereas the interest

from bank is an income which is taxable under

“section 15-35” (Hoynes and Rothstein

As per

“section 8-1, ITAA 1997” an individual is only permitted to obtain deduction

from their assessable income for expenses that are incurred at the time of generating

assessable income or occurred at the time of performing business activities. While in negative

limbs of

“sec 8-1(2)”, no deduction is allowed for expenses that are capital or private in

nature.

The ATO states that small business owners having annual revenue of not greater than

$10,000 are permitted to immediately write off the assets which is bought for $20,000 or

lower. While the

“Taxation Ruling of TR 2004/6” explains that for claiming the expenses

associated to meal, allowances there should be written record for the same (Thuronyi and

Brooks 2016). Travel between home and work is regarded as private expenses and not

deductions is allowed. The court in

“Lunney v FCT (1958)” held that no deduction for travel

between home and work is allowed.

Application:

Sam received $450,000 from his accounting business. The receipt will be treated as

income from business and it is taxable as ordinary income under

“section 6-5, ITAA 1997”.

He also received a wedding gift of $10,000. Referring to

“Hayes v FCT (1956)” the gift is

non-taxable income since it was received out of personal relationship. The advertisement

incentives received by Sam from publishing company is a taxable ordinary income under

“section 6-5, ITAA 1997”.

A salary of $34,000 was received by Sam from his part-time employment in

University. The salary is an income from personal exertion and citing

“Dean v FCT (1997)”

it will be taxable as ordinary income under

“section 6-5, ITAA 1997”. Whereas the interest

from bank is an income which is taxable under

“section 15-35” (Hoynes and Rothstein

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.