TAXATION LAW Assignment - Taxation Principles, Semester 2

VerifiedAdded on 2019/11/19

|14

|2681

|160

Homework Assignment

AI Summary

This Taxation Law assignment solution addresses several key areas of Australian taxation. It begins by analyzing capital gains and losses under ITAA 1997, including the treatment of personal use assets and collectibles. The solution then explores Fringe Benefit Tax (FBT), examining how interest offsetting arrangements impact tax obligations. It further delves into the complexities of rental property co-ownership, clarifying the allocation of losses between partners and the implications of partnership agreements. The assignment also addresses the concept of tax avoidance, referencing the Duke of Westminster case and the Ramsay principle, and explaining how individuals can structure their financial agreements to minimize tax liabilities legally. Finally, the solution examines the taxable income of primary producers, specifically focusing on the sale of timber, the definition of primary producer, and the treatment of royalties. The assignment incorporates relevant legislation, rulings, and case law to support its arguments and conclusions, providing a comprehensive overview of the topics covered.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................3

Issues:.........................................................................................................................................3

Legislation:.................................................................................................................................3

Applications:..............................................................................................................................3

Conclusion:................................................................................................................................4

Answer to question 2:.................................................................................................................4

Issue:..........................................................................................................................................4

Legislations:...............................................................................................................................4

Applications:..............................................................................................................................4

Conclusion:................................................................................................................................5

Answer to question 3:.................................................................................................................6

Issue:..........................................................................................................................................6

Legislation:.................................................................................................................................6

Applications:..............................................................................................................................6

Conclusion:................................................................................................................................8

Answer to question 4:.................................................................................................................8

Answer to question 5:.................................................................................................................9

Issues:.........................................................................................................................................9

Legislations:...............................................................................................................................9

Applications:..............................................................................................................................9

Table of Contents

Answer to question 1:.................................................................................................................3

Issues:.........................................................................................................................................3

Legislation:.................................................................................................................................3

Applications:..............................................................................................................................3

Conclusion:................................................................................................................................4

Answer to question 2:.................................................................................................................4

Issue:..........................................................................................................................................4

Legislations:...............................................................................................................................4

Applications:..............................................................................................................................4

Conclusion:................................................................................................................................5

Answer to question 3:.................................................................................................................6

Issue:..........................................................................................................................................6

Legislation:.................................................................................................................................6

Applications:..............................................................................................................................6

Conclusion:................................................................................................................................8

Answer to question 4:.................................................................................................................8

Answer to question 5:.................................................................................................................9

Issues:.........................................................................................................................................9

Legislations:...............................................................................................................................9

Applications:..............................................................................................................................9

2TAXATION LAW

Conclusion:..............................................................................................................................11

Reference list:...........................................................................................................................12

Conclusion:..............................................................................................................................11

Reference list:...........................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

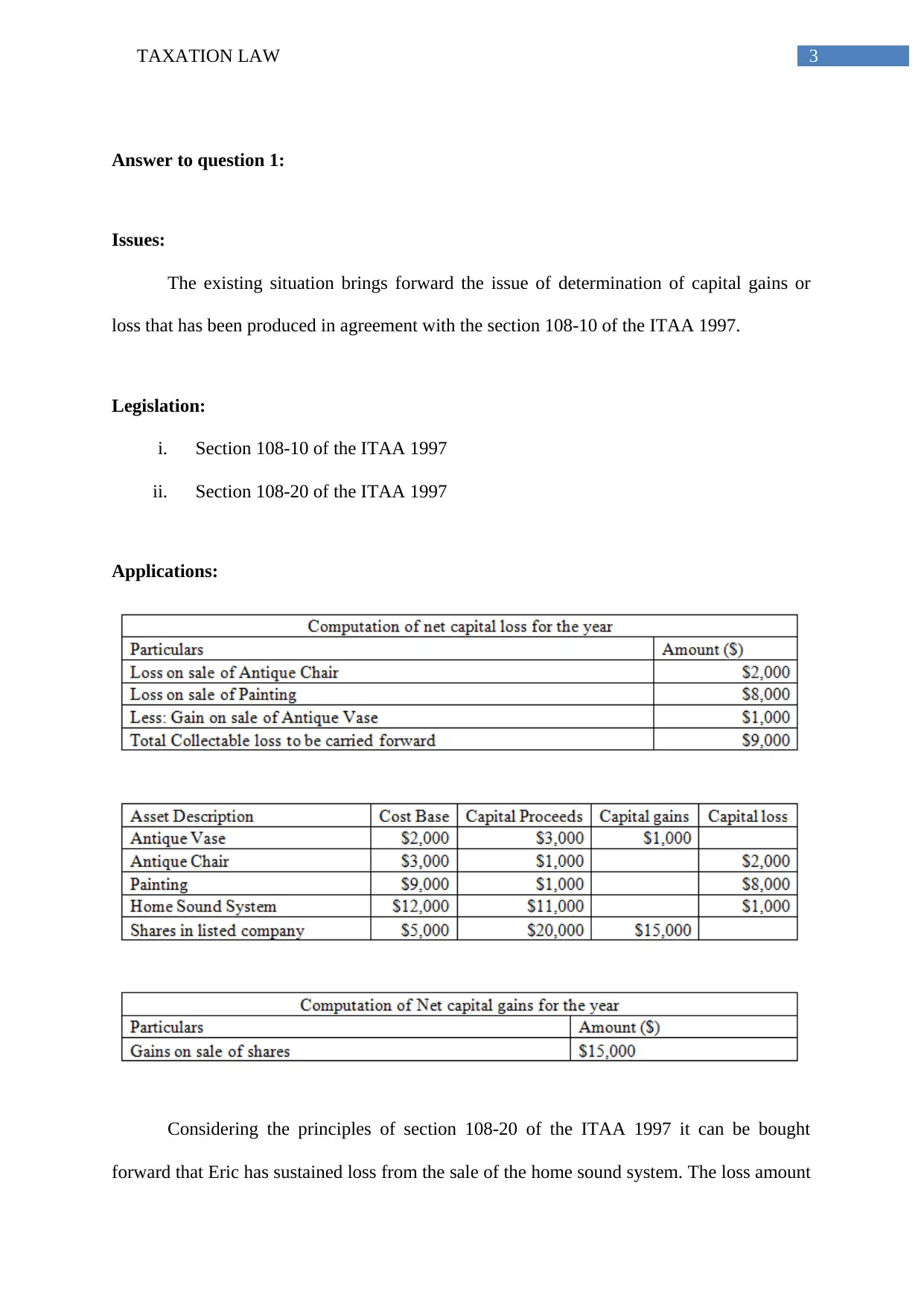

Answer to question 1:

Issues:

The existing situation brings forward the issue of determination of capital gains or

loss that has been produced in agreement with the section 108-10 of the ITAA 1997.

Legislation:

i. Section 108-10 of the ITAA 1997

ii. Section 108-20 of the ITAA 1997

Applications:

Considering the principles of section 108-20 of the ITAA 1997 it can be bought

forward that Eric has sustained loss from the sale of the home sound system. The loss amount

Answer to question 1:

Issues:

The existing situation brings forward the issue of determination of capital gains or

loss that has been produced in agreement with the section 108-10 of the ITAA 1997.

Legislation:

i. Section 108-10 of the ITAA 1997

ii. Section 108-20 of the ITAA 1997

Applications:

Considering the principles of section 108-20 of the ITAA 1997 it can be bought

forward that Eric has sustained loss from the sale of the home sound system. The loss amount

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

stood at $1,000 and this will not be allowed for offset because it represented private use asset

for Eric. In addition to this, section 108-10 of the ITAA 1997 defines that no collectible loss

will be permitted for deductions against the sales of shares (Kenny, Blissenden and Villios

2017). Eric can only offset the collectibles against the gains that has been defined in section

108-10 of the ITAA 1997. It is observed that Eric generated gains only by selling ordinary

assets with no current year capital or any kind of applicable discounts. As a result of this, the

net capital gains for Eric is arrived at $15,000.

Conclusion:

On considering the above situation it can be said that Eric will not be able to set off

loss from selling of personal asset and he has produced capital gains only from the sale of

ordinary assets.

Answer to question 2:

Issue:

The issues introduce the subject of FBT along with the ascertainment of FBT under

the FBT Act 1986.

Legislations:

i. Taxation Ruling TR 93/6

ii. FBT Act 1986

Applications:

Computation of Fringe Benefit Tax

stood at $1,000 and this will not be allowed for offset because it represented private use asset

for Eric. In addition to this, section 108-10 of the ITAA 1997 defines that no collectible loss

will be permitted for deductions against the sales of shares (Kenny, Blissenden and Villios

2017). Eric can only offset the collectibles against the gains that has been defined in section

108-10 of the ITAA 1997. It is observed that Eric generated gains only by selling ordinary

assets with no current year capital or any kind of applicable discounts. As a result of this, the

net capital gains for Eric is arrived at $15,000.

Conclusion:

On considering the above situation it can be said that Eric will not be able to set off

loss from selling of personal asset and he has produced capital gains only from the sale of

ordinary assets.

Answer to question 2:

Issue:

The issues introduce the subject of FBT along with the ascertainment of FBT under

the FBT Act 1986.

Legislations:

i. Taxation Ruling TR 93/6

ii. FBT Act 1986

Applications:

Computation of Fringe Benefit Tax

5TAXATION LAW

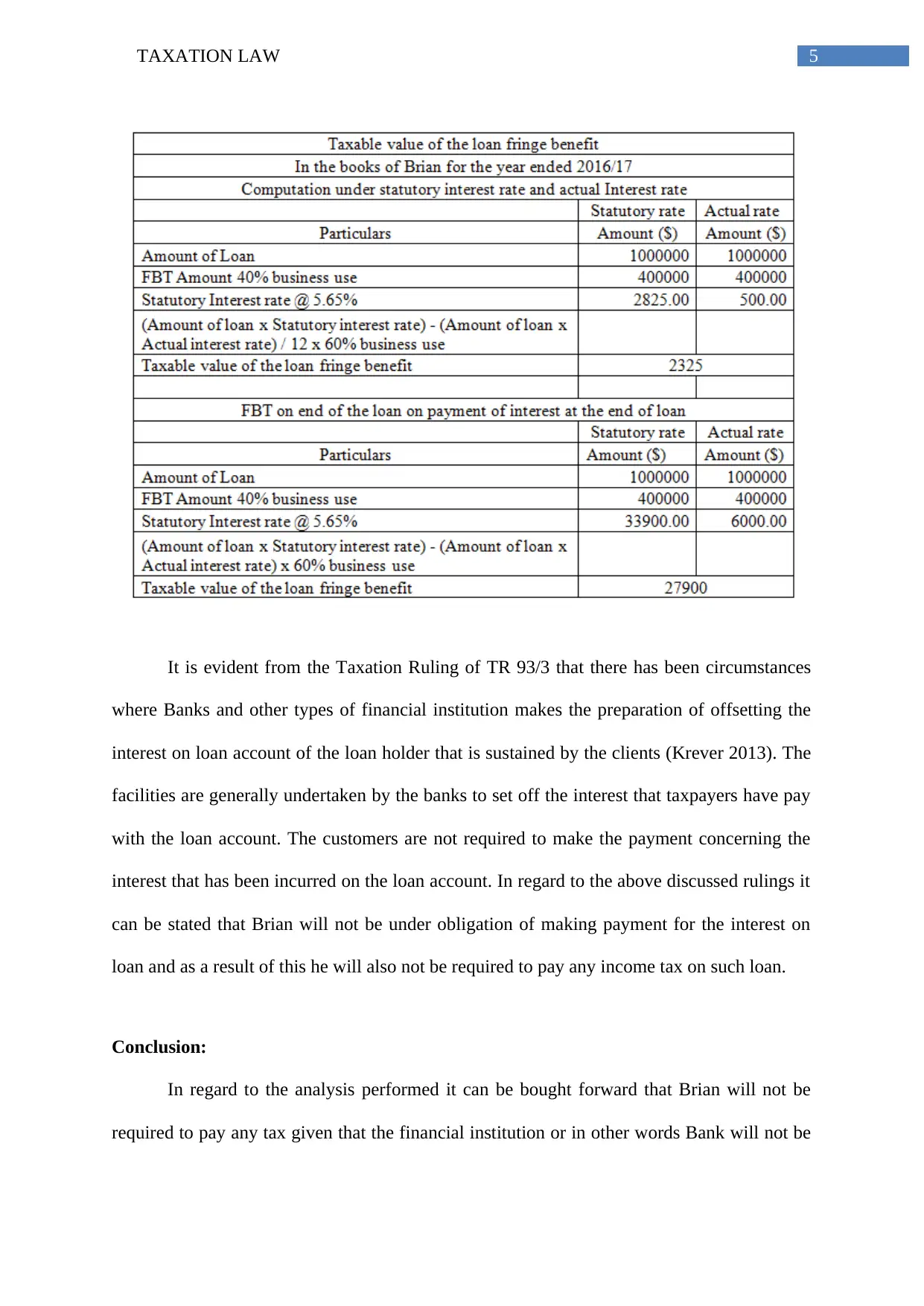

It is evident from the Taxation Ruling of TR 93/3 that there has been circumstances

where Banks and other types of financial institution makes the preparation of offsetting the

interest on loan account of the loan holder that is sustained by the clients (Krever 2013). The

facilities are generally undertaken by the banks to set off the interest that taxpayers have pay

with the loan account. The customers are not required to make the payment concerning the

interest that has been incurred on the loan account. In regard to the above discussed rulings it

can be stated that Brian will not be under obligation of making payment for the interest on

loan and as a result of this he will also not be required to pay any income tax on such loan.

Conclusion:

In regard to the analysis performed it can be bought forward that Brian will not be

required to pay any tax given that the financial institution or in other words Bank will not be

It is evident from the Taxation Ruling of TR 93/3 that there has been circumstances

where Banks and other types of financial institution makes the preparation of offsetting the

interest on loan account of the loan holder that is sustained by the clients (Krever 2013). The

facilities are generally undertaken by the banks to set off the interest that taxpayers have pay

with the loan account. The customers are not required to make the payment concerning the

interest that has been incurred on the loan account. In regard to the above discussed rulings it

can be stated that Brian will not be under obligation of making payment for the interest on

loan and as a result of this he will also not be required to pay any income tax on such loan.

Conclusion:

In regard to the analysis performed it can be bought forward that Brian will not be

required to pay any tax given that the financial institution or in other words Bank will not be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

required to pay the interest that is acquired by him with the help of appropriate interest

offsetting arrangement.

Answer to question 3:

Issue:

The existing situation introduces the issues of the Jack and Jill for determining the

assessable conditions of the loss that has been suffered from the property that is rented by

them.

Legislation:

i. FC of T v McDonald (1987)

ii. Section 51 of the ITAA 1997

iii. Taxation Rulings of TR 93/23

Applications:

In accordance with the Taxation Rulings of TR 93/23 it defines the principles of Co-

ownership of property that is rented under partnership (Moore and Corrigan et al. 2013). The

ruling evidently puts forward the evidence that co-ownership of the rental property will be

regarded for income tax purpose but will not be considered as partnership under the General

Law. From the following situation of Jack and Jill it is noticed that the husband and wife

formed a partnership to undertake the rental property with the agreement of sharing profit and

loss. They agreed to share profit with Jack being entitled to 10% of profit and Jill will be

getting 90% of the profit. The agreement also contained that Jack will have to bear 100% of

loss from that property. In respect of the Taxation Ruling of TR 92/32 an explanation has

required to pay the interest that is acquired by him with the help of appropriate interest

offsetting arrangement.

Answer to question 3:

Issue:

The existing situation introduces the issues of the Jack and Jill for determining the

assessable conditions of the loss that has been suffered from the property that is rented by

them.

Legislation:

i. FC of T v McDonald (1987)

ii. Section 51 of the ITAA 1997

iii. Taxation Rulings of TR 93/23

Applications:

In accordance with the Taxation Rulings of TR 93/23 it defines the principles of Co-

ownership of property that is rented under partnership (Moore and Corrigan et al. 2013). The

ruling evidently puts forward the evidence that co-ownership of the rental property will be

regarded for income tax purpose but will not be considered as partnership under the General

Law. From the following situation of Jack and Jill it is noticed that the husband and wife

formed a partnership to undertake the rental property with the agreement of sharing profit and

loss. They agreed to share profit with Jack being entitled to 10% of profit and Jill will be

getting 90% of the profit. The agreement also contained that Jack will have to bear 100% of

loss from that property. In respect of the Taxation Ruling of TR 92/32 an explanation has

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

been provided that rental property co-owners Jack and Jill will not be viewed as partners in

respect of the general laws (Woellner 2013).

The agreement of partnership whether orally or in writing does not creates any effect

on the allocation of profit or loss generated from such property. It can be stated that both the

joint owners Jack and Jill possess the rental property in the form of “joint owner or tenants in

common”. Considering the decision of the federal court in the case of FC of T v McDonald

(1987) where the taxpayers were the joint owners of the two unit of property. The share profit

contained an agreement where Mr McDonald was entitled to a profit of 25% whereas Mrs

McDonald will be getting 75% of the profit from such rental property (Coleman and Sadiq

2013). There was also no kind of provision relating to the allocation of loss as Mr McDonald

was responsible to should the entire amount of loss. It has been understood that there was no

kind of partnership existed between Mr McDonald and Mrs McDonald under the concept of

general law.

In relation to the evidence that has been found in the case study of Jack and Jill, an

important considerations can be bought forward that loss should be apportioned equally

among them and there should not be provision regarding the deductions that are allowable by

the virtue of agreement (Morgan, Mortimer and Pinto 2013). It can be stated that Jack in the

initial stages provided large part of the earnings to his wife and indemnified Jill, his wife

against the loss from the investment. The supposition of making distribution of loss was

originally made by Jack for the purpose of domestic preparation where is clearly sought to

enhance the income of his wife. Therefore, it is worth mentioning that Section 51 does not

provide permission for making deductions of loss by virtue of the agreement formed.

On the other hand, if both Jack and his wife undertakes the decision of selling

property the cost base and the lowered cost base of the property that is rented out must be

been provided that rental property co-owners Jack and Jill will not be viewed as partners in

respect of the general laws (Woellner 2013).

The agreement of partnership whether orally or in writing does not creates any effect

on the allocation of profit or loss generated from such property. It can be stated that both the

joint owners Jack and Jill possess the rental property in the form of “joint owner or tenants in

common”. Considering the decision of the federal court in the case of FC of T v McDonald

(1987) where the taxpayers were the joint owners of the two unit of property. The share profit

contained an agreement where Mr McDonald was entitled to a profit of 25% whereas Mrs

McDonald will be getting 75% of the profit from such rental property (Coleman and Sadiq

2013). There was also no kind of provision relating to the allocation of loss as Mr McDonald

was responsible to should the entire amount of loss. It has been understood that there was no

kind of partnership existed between Mr McDonald and Mrs McDonald under the concept of

general law.

In relation to the evidence that has been found in the case study of Jack and Jill, an

important considerations can be bought forward that loss should be apportioned equally

among them and there should not be provision regarding the deductions that are allowable by

the virtue of agreement (Morgan, Mortimer and Pinto 2013). It can be stated that Jack in the

initial stages provided large part of the earnings to his wife and indemnified Jill, his wife

against the loss from the investment. The supposition of making distribution of loss was

originally made by Jack for the purpose of domestic preparation where is clearly sought to

enhance the income of his wife. Therefore, it is worth mentioning that Section 51 does not

provide permission for making deductions of loss by virtue of the agreement formed.

On the other hand, if both Jack and his wife undertakes the decision of selling

property the cost base and the lowered cost base of the property that is rented out must be

8TAXATION LAW

considered in the in computing the taxable income. As evident both Jack and Jill are owners

of the property and the capital gains and loss should be recorded in terms of the ownership of

the interest in the property.

Conclusion:

It can be concluded that the Jack and Jill will not be considered as the joint owners

under the general law and the loss that is suffered from the property that is rented out by them

must be allocated equally among them.

Answer to question 4:

IRC v Duke of Westminster (1936) has often being quoted in the event when there

is tax avoidance. The above stated case introduces the principles that each and every person

has been permitted to make order for their tax affairs (Milton 2013). The principles lay down

that tax assignment must be made in such a manner that it is lower than it would have been.

In spite of the fact that ruling is considered as the substance of that appeal for taxpayers that

are seeking to avoid tax by legally establishing a complicated structure that has been

weakened by the successive circumstances where courts have understood the entire impact.

Considering the example of the WT Ramsay v IRC the court in the later stages have taken

restrictive approach (Woellner et al. 2014). It is worth mentioning that the transaction

consists of the pre-arranged false stage that fails to serve any purpose related to business

rather than avoiding tax. The appropriate approach was to impose tax to the consequences of

business entirely.

On implementing the principle in the modern age of Australia if an individual is

successful in ordering the appropriate tax assignment so that it can attain the results of the

principles defined under Commission of Inland Revenue the taxpayers would not be under

considered in the in computing the taxable income. As evident both Jack and Jill are owners

of the property and the capital gains and loss should be recorded in terms of the ownership of

the interest in the property.

Conclusion:

It can be concluded that the Jack and Jill will not be considered as the joint owners

under the general law and the loss that is suffered from the property that is rented out by them

must be allocated equally among them.

Answer to question 4:

IRC v Duke of Westminster (1936) has often being quoted in the event when there

is tax avoidance. The above stated case introduces the principles that each and every person

has been permitted to make order for their tax affairs (Milton 2013). The principles lay down

that tax assignment must be made in such a manner that it is lower than it would have been.

In spite of the fact that ruling is considered as the substance of that appeal for taxpayers that

are seeking to avoid tax by legally establishing a complicated structure that has been

weakened by the successive circumstances where courts have understood the entire impact.

Considering the example of the WT Ramsay v IRC the court in the later stages have taken

restrictive approach (Woellner et al. 2014). It is worth mentioning that the transaction

consists of the pre-arranged false stage that fails to serve any purpose related to business

rather than avoiding tax. The appropriate approach was to impose tax to the consequences of

business entirely.

On implementing the principle in the modern age of Australia if an individual is

successful in ordering the appropriate tax assignment so that it can attain the results of the

principles defined under Commission of Inland Revenue the taxpayers would not be under

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

compulsion of paying more amount of tax (Anderson, Dickfos and Brown 2016). It can stated

that the principles allows the individuals and companies to structure their financial

agreements with the objective of cutting down the tax liability in respect of the legal

configuration of the act.

Answer to question 5:

Issues:

The existing study is related to the issue of the taxable income that is produced by the

taxpayer in relation to the primary producer under section 6 (1) of the ITAA 1997.

Legislations:

a. Section 6 (1) of the ITAA 1936

b. Taxation Rulings of TR 95/6

c. Subsection 36 (1)

d. Section 26 (f)

e. McCauley v FC of T (1944)

Applications:

The current case study introduces the issue that Bill owns a large portion of land on

which there is a several quantity of pine trees. In the early stages Bill was looking forward to

use the land for sheep grazing and desired to clear the land. It was further noticed that a

logging company approached Bill that offered to take timber from his land for every 100

meter by paying him with $1,000. In relation to the Taxation Ruling of TR 95/6 it states that

sale of timber will be accounted as assessable income irrespective of the fact that the taxpayer

was indulged in the activities of forestry (Barkoczy 2016). As it has been defined under the

compulsion of paying more amount of tax (Anderson, Dickfos and Brown 2016). It can stated

that the principles allows the individuals and companies to structure their financial

agreements with the objective of cutting down the tax liability in respect of the legal

configuration of the act.

Answer to question 5:

Issues:

The existing study is related to the issue of the taxable income that is produced by the

taxpayer in relation to the primary producer under section 6 (1) of the ITAA 1997.

Legislations:

a. Section 6 (1) of the ITAA 1936

b. Taxation Rulings of TR 95/6

c. Subsection 36 (1)

d. Section 26 (f)

e. McCauley v FC of T (1944)

Applications:

The current case study introduces the issue that Bill owns a large portion of land on

which there is a several quantity of pine trees. In the early stages Bill was looking forward to

use the land for sheep grazing and desired to clear the land. It was further noticed that a

logging company approached Bill that offered to take timber from his land for every 100

meter by paying him with $1,000. In relation to the Taxation Ruling of TR 95/6 it states that

sale of timber will be accounted as assessable income irrespective of the fact that the taxpayer

was indulged in the activities of forestry (Barkoczy 2016). As it has been defined under the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Subsection 6 (1) of the ITAA 1936, a person being indulged in the activities of forestry as the

primary producer for the purpose of taxation it is concerned with the purpose of carrying of a

business.

In respect of the subsection 6 (1) of the ITAA 1936 Bill will be treated as the primary

producer based on the fact that he was indulged in the activities of the tending trees in his

land that is being owned by him (Cao et al. 2015). In respect of the fact that the activities of

the forest functions consisted of the cutting down the trees in a plantation even thought the

taxpayers was not engaged in the activities of plantation or tending of trees. It can be defined

from the above stated analysis that Bill being the holder of the land did not plant the trees but

it can be asserted that the amount that he received on selling of timber would be included in

the taxable income. Disposal of standing timber where the taxpayer undertakes the decision

of selling the trees that was not planted or felled for sale will be included in their income as

the taxable income. With regard to the principles defined under subsection 36 (1) even

though the sale of timber constitutes income for the purpose of taxation, the trees is

considered as the part of the business assets (Fry 2017).

If Bill is paid with a lump sum of $50,000 by simply enabling the logging company

with the right of taking as much as the amount of timber it wants from his land then his

receipt would be treated as “Royalties” (Russell 2016). In respect of the guidelines that has

been defined under the section 26 (f) of the ITAA 1997 royalties that is received by the

taxpayer from selling of timber from the land that is owned by an individual taxpayer will be

treated as the taxable income for the year in which such income from felling of trees were

derived (James 2016). As it has been stated in the case of McCauley v FC of T (1944)

amount received in the form of payment by the grantor with the right of cutting down the

trees then the amount that is receive from the felled timber would be treated as royalties

under section 26 (f) (Robin 2017). Therefore, the amount derived by Bill on granting rights of

Subsection 6 (1) of the ITAA 1936, a person being indulged in the activities of forestry as the

primary producer for the purpose of taxation it is concerned with the purpose of carrying of a

business.

In respect of the subsection 6 (1) of the ITAA 1936 Bill will be treated as the primary

producer based on the fact that he was indulged in the activities of the tending trees in his

land that is being owned by him (Cao et al. 2015). In respect of the fact that the activities of

the forest functions consisted of the cutting down the trees in a plantation even thought the

taxpayers was not engaged in the activities of plantation or tending of trees. It can be defined

from the above stated analysis that Bill being the holder of the land did not plant the trees but

it can be asserted that the amount that he received on selling of timber would be included in

the taxable income. Disposal of standing timber where the taxpayer undertakes the decision

of selling the trees that was not planted or felled for sale will be included in their income as

the taxable income. With regard to the principles defined under subsection 36 (1) even

though the sale of timber constitutes income for the purpose of taxation, the trees is

considered as the part of the business assets (Fry 2017).

If Bill is paid with a lump sum of $50,000 by simply enabling the logging company

with the right of taking as much as the amount of timber it wants from his land then his

receipt would be treated as “Royalties” (Russell 2016). In respect of the guidelines that has

been defined under the section 26 (f) of the ITAA 1997 royalties that is received by the

taxpayer from selling of timber from the land that is owned by an individual taxpayer will be

treated as the taxable income for the year in which such income from felling of trees were

derived (James 2016). As it has been stated in the case of McCauley v FC of T (1944)

amount received in the form of payment by the grantor with the right of cutting down the

trees then the amount that is receive from the felled timber would be treated as royalties

under section 26 (f) (Robin 2017). Therefore, the amount derived by Bill on granting rights of

11TAXATION LAW

removing trees represents royalties and will be treated as taxable income under section 26 (f)

of the act.

Conclusion:

In respect of the analysis conducted above it can be stated that Bill will be liable for

taxation under subsection 36 (1) for the sale of timber and additionally by granting the right

of removing the desired amount of timber would be treated as royalties under section 26 (1)

of the ITAA 1997.

removing trees represents royalties and will be treated as taxable income under section 26 (f)

of the act.

Conclusion:

In respect of the analysis conducted above it can be stated that Bill will be liable for

taxation under subsection 36 (1) for the sale of timber and additionally by granting the right

of removing the desired amount of timber would be treated as royalties under section 26 (1)

of the ITAA 1997.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

![Taxation Law Analysis Assignment - [University Name]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2F237a5b831ee046ecb975c30288c0819d.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.