Taxation Law Homework: Income, Deductions, and Tax Liability for 2020

VerifiedAdded on 2022/10/15

|7

|1156

|99

Homework Assignment

AI Summary

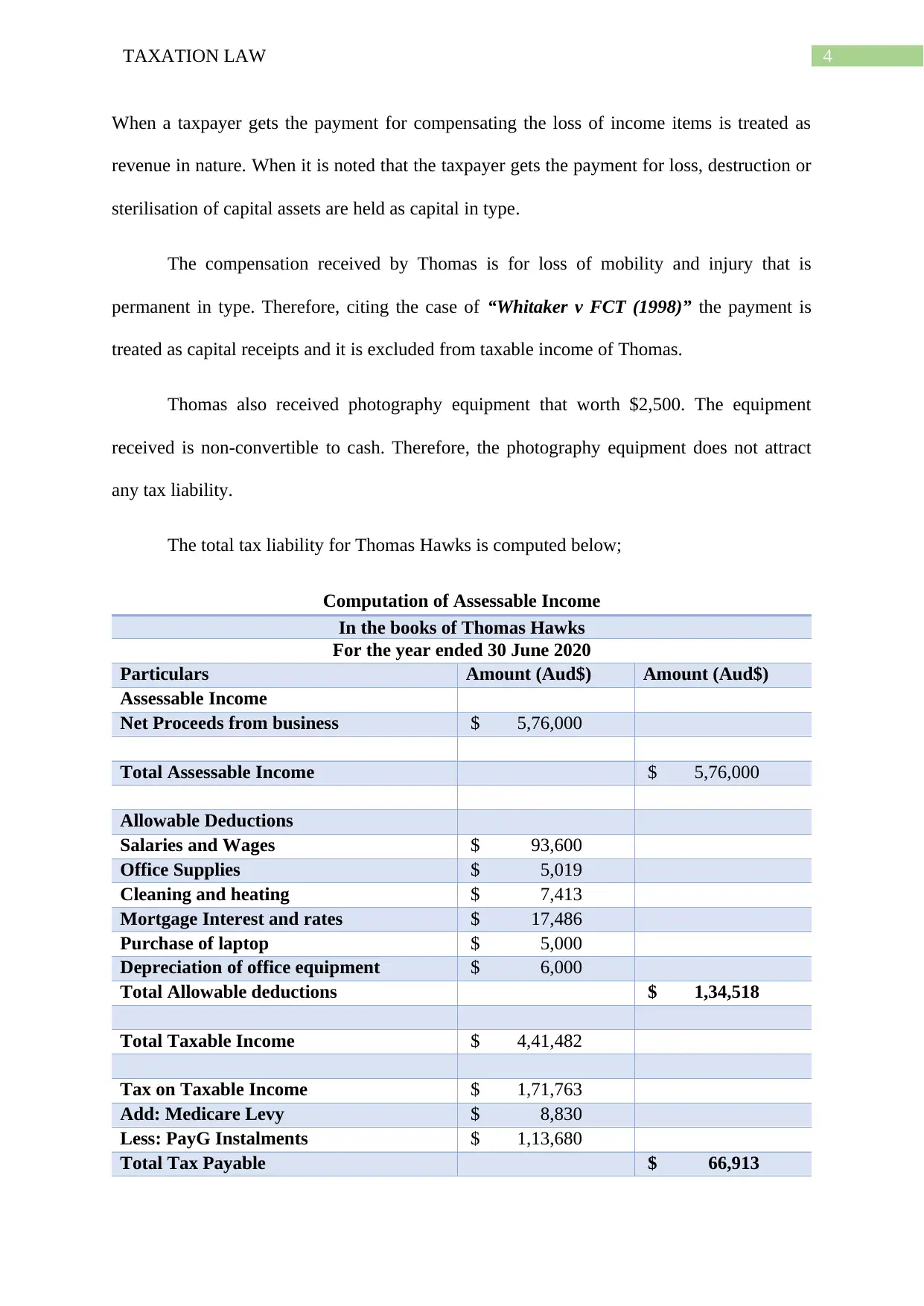

This taxation law assignment solution analyzes the tax implications for Thomas Hawks, a tax accountant, for the year ended June 30, 2020. The solution addresses the classification of income from his personal service business, applying relevant sections of the ITA Act 1936 and ITAA 1997, along with case law such as McNeil v FC (2007). It examines the application of the cash method for income recognition and the deductibility of home office expenses, referencing TR 93/30 and Swinford v FCT (1984). Additionally, the assignment addresses the tax treatment of compensation payments and the receipt of non-cash assets. The solution includes a detailed computation of Thomas Hawks' assessable income, allowable deductions, and total tax liability, providing a comprehensive understanding of the tax principles involved.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.