Taxation Law Assignment: Cryptocurrencies, Tax and Partnership

VerifiedAdded on 2022/08/22

|8

|821

|27

Homework Assignment

AI Summary

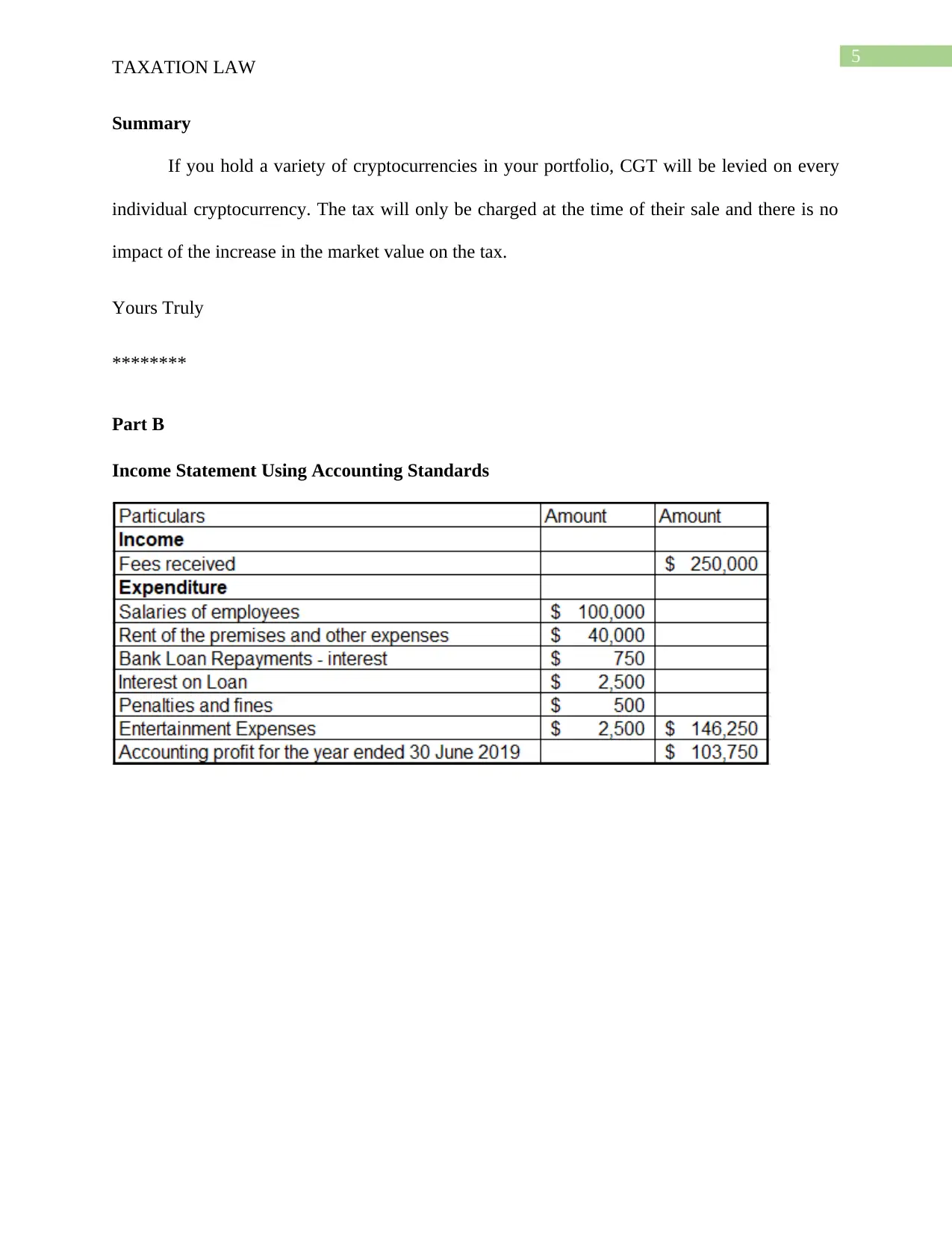

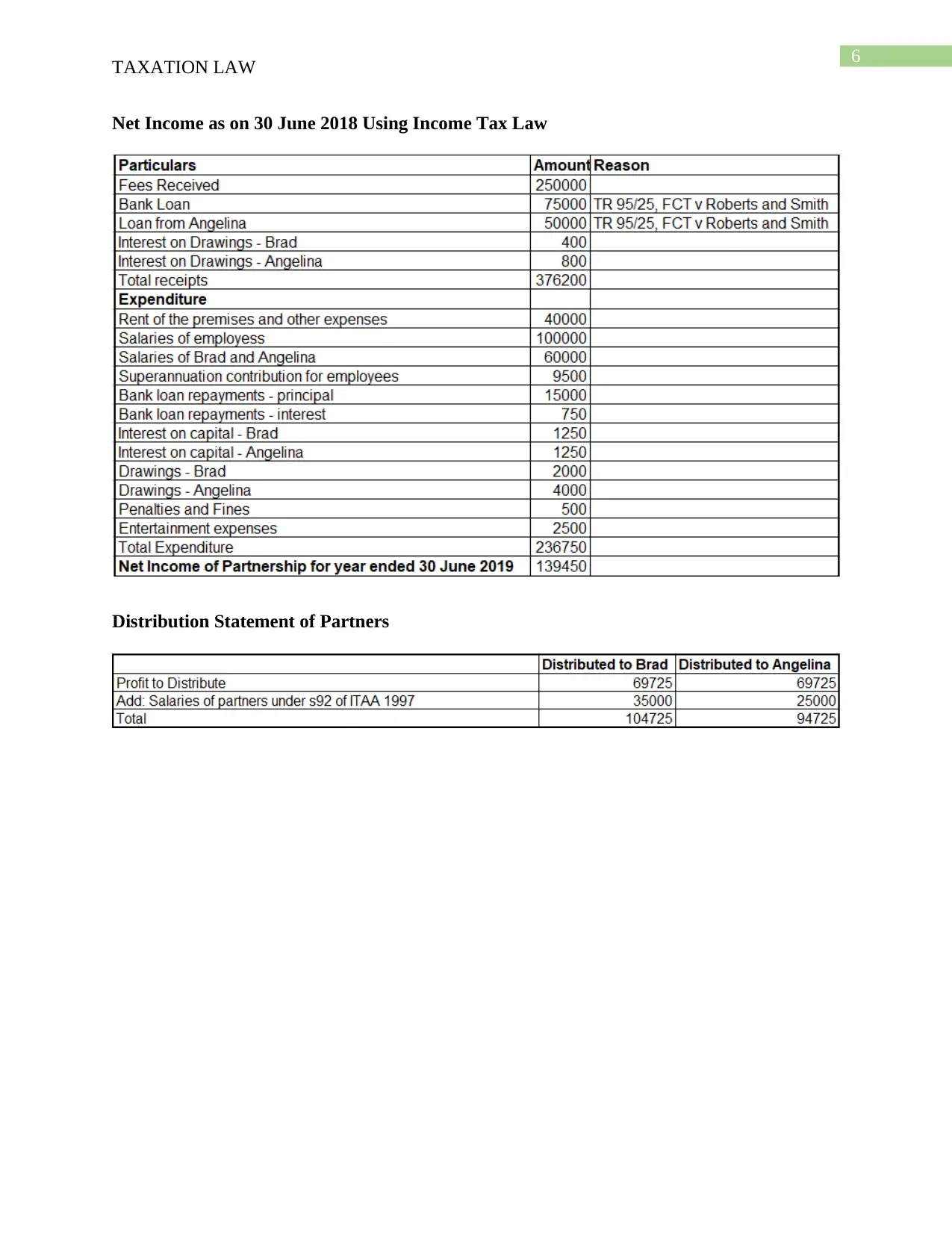

This document presents a comprehensive solution to a Taxation Law assignment, specifically addressing the taxation of cryptocurrencies in Australia. Part A provides a detailed written letter of advice to Mr. Alex Smith, explaining the Australian Taxation Office's (ATO) regulations regarding cryptocurrency taxation, including Capital Gains Tax (CGT), Income Tax, Goods and Services Tax, and Fringe Benefits Tax. The letter clarifies how these taxes apply to transactions such as gifts, trades, and conversions to fiat currency, as well as investments in cryptocurrencies. Part B includes an Income Statement using accounting standards and a Distribution Statement of Partners, demonstrating the financial implications of the tax laws discussed. The assignment utilizes the ATO's publications and relevant resources to offer a clear understanding of the tax treatment of cryptocurrencies. The solution covers various aspects of cryptocurrency taxation, offering practical insights into the subject.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.