Taxation Law Solved Assignment

VerifiedAdded on 2019/11/19

|9

|782

|450

Homework Assignment

AI Summary

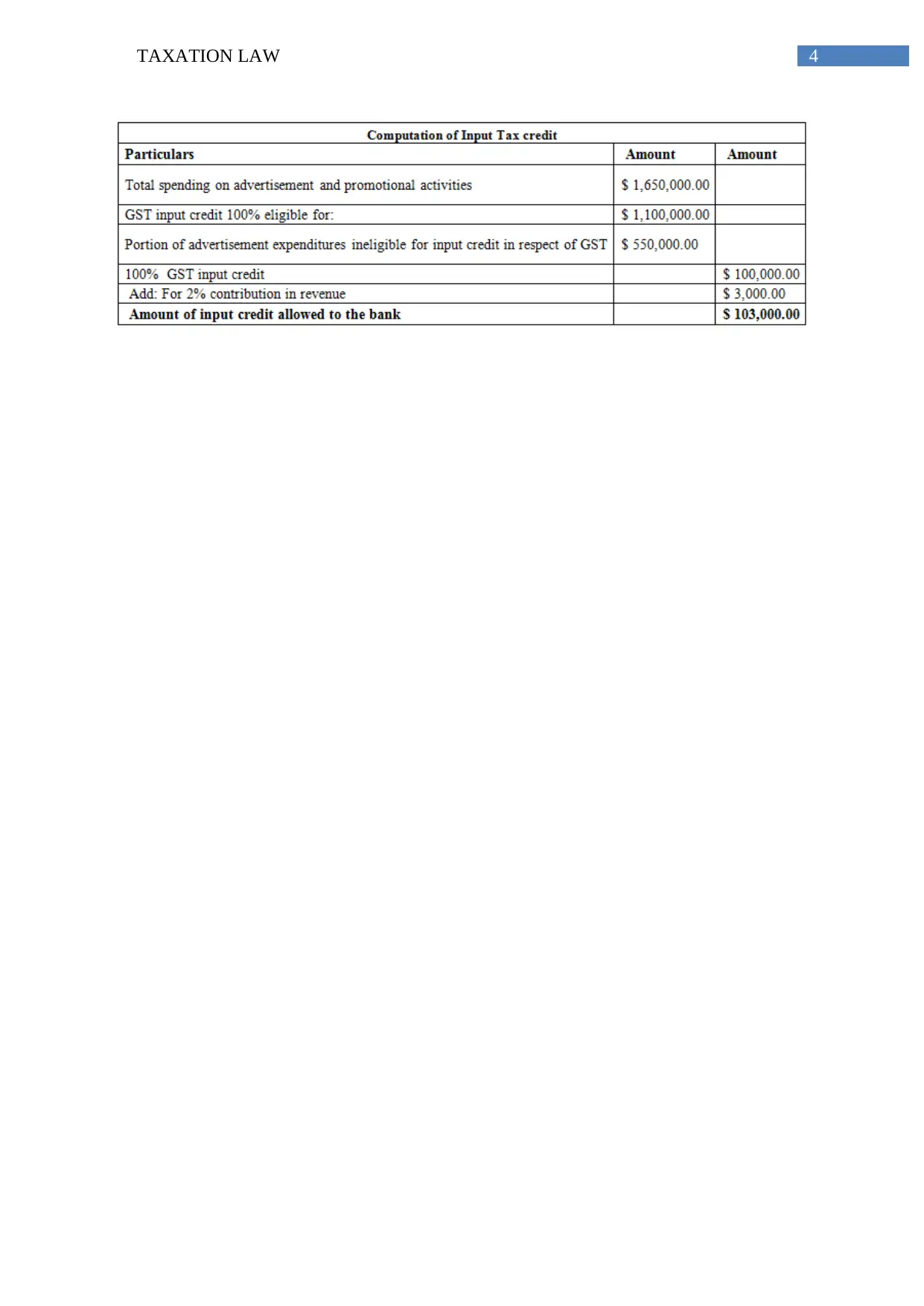

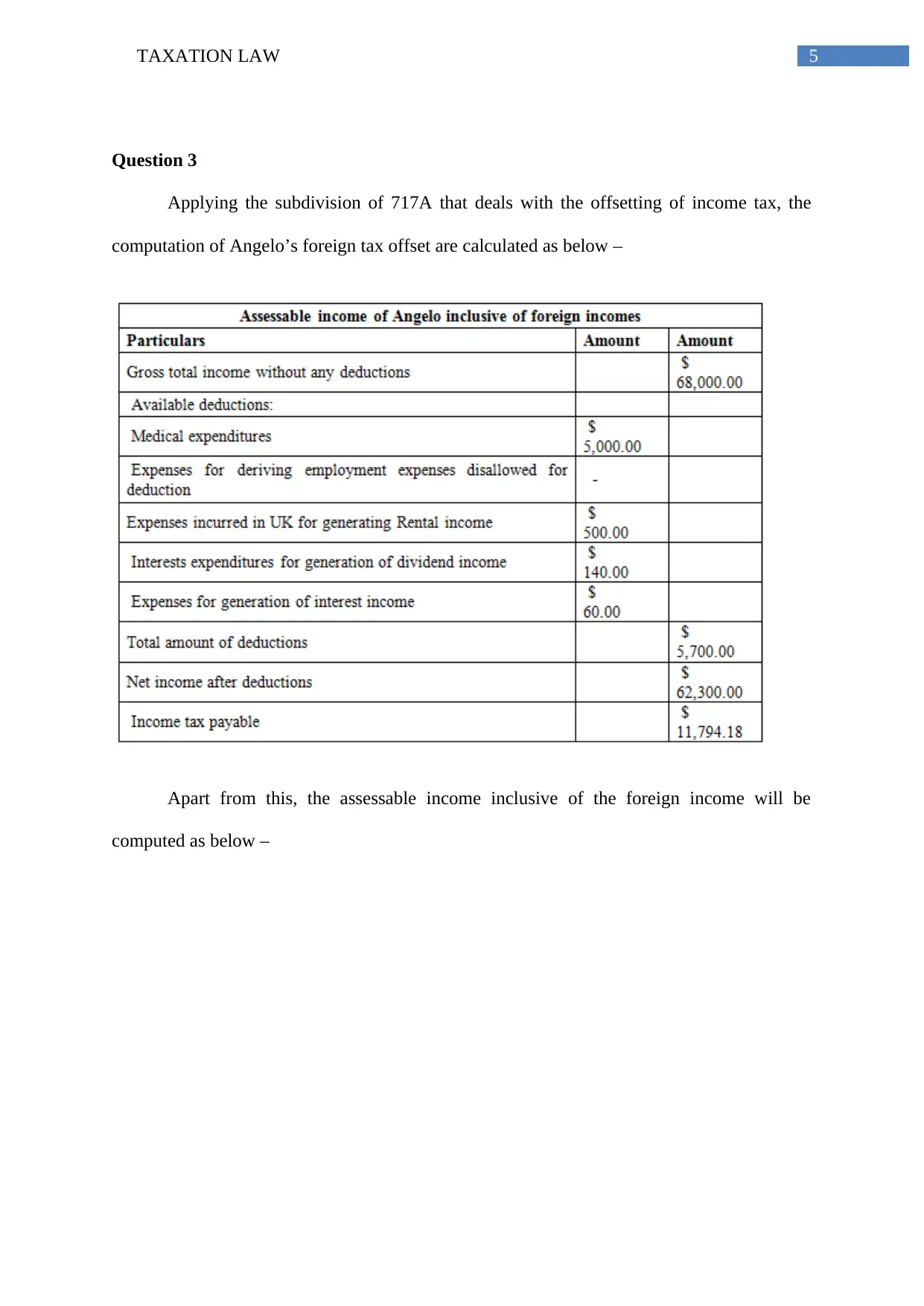

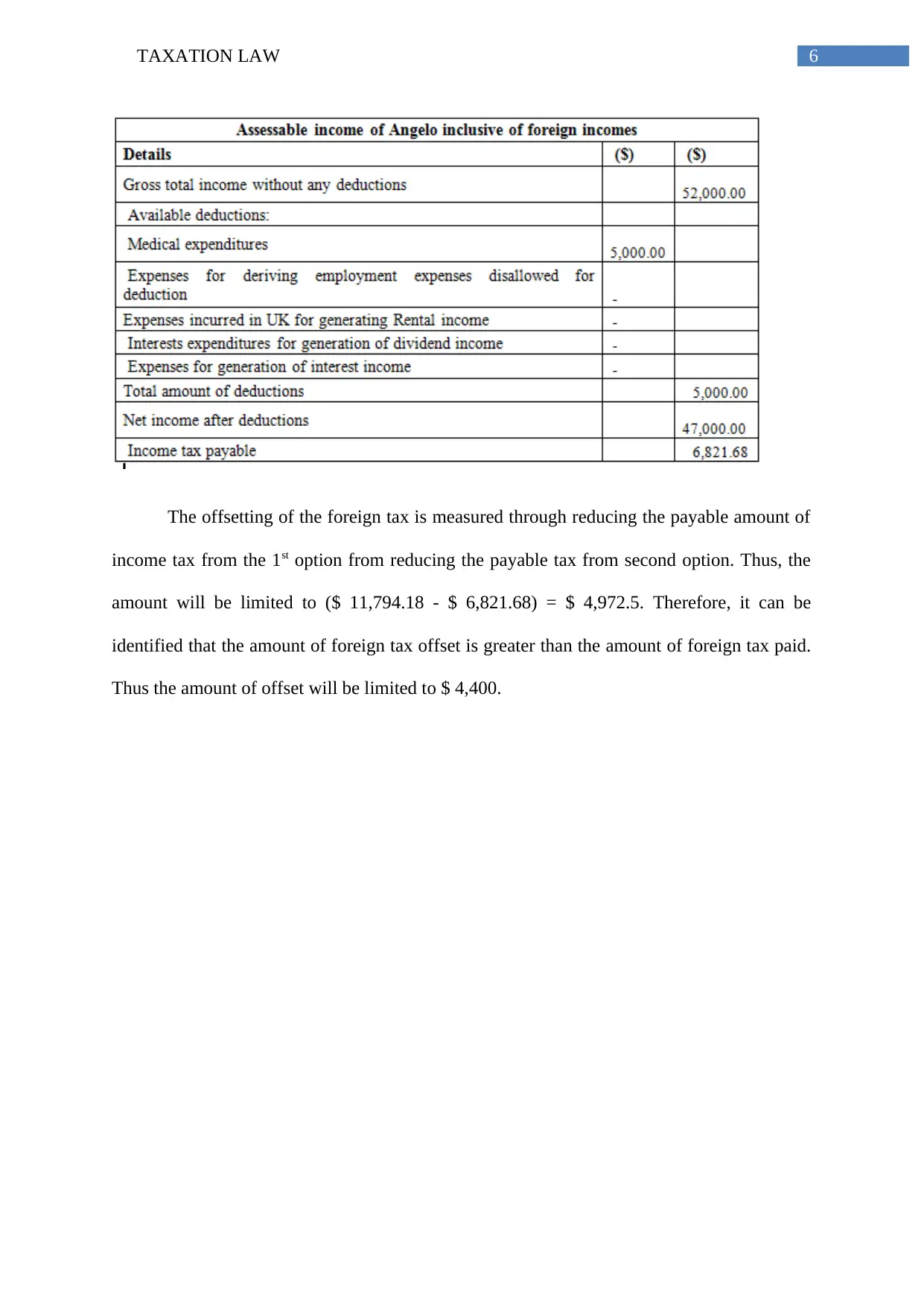

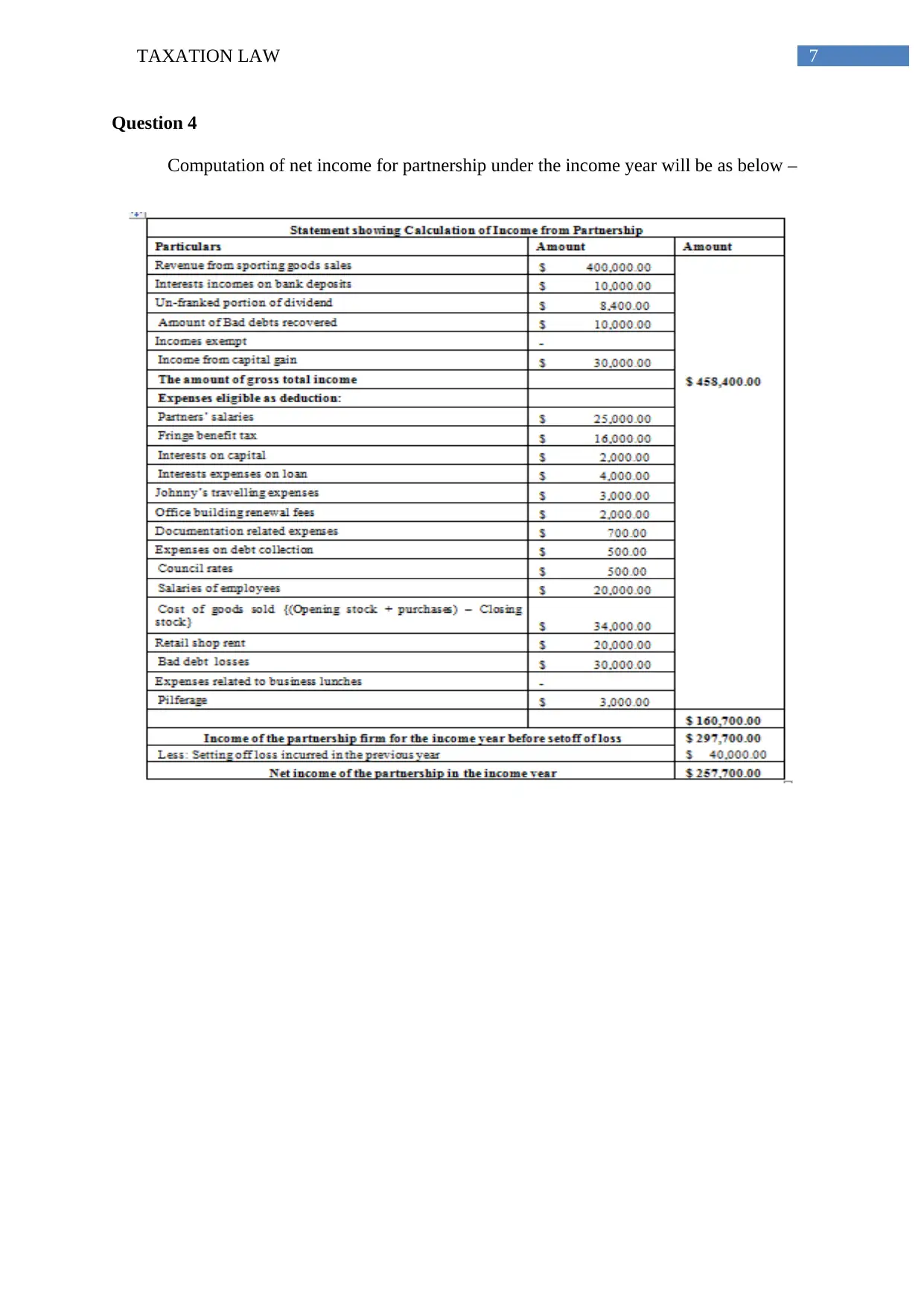

This solved assignment addresses several questions related to taxation law. Question 1 deals with allowable deductions for various expenses, including moving costs, asset revaluation, and legal fees. Question 2 focuses on input tax credit calculations under the GST Act 1999 for a bank's advertising expenses. Question 3 involves calculating Angelo's foreign tax offset using subdivision 717A. Finally, Question 4 demonstrates the computation of net income for a partnership. The assignment provides detailed calculations and explanations, referencing relevant sections of the ITAA 97 and GST Act 1999. It also includes a list of references used in the solutions.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.