Taxation Law: A Report on Tax Treatment of Accounting Items - Analysis

VerifiedAdded on 2023/06/05

|12

|2861

|456

Report

AI Summary

This report provides an analysis of the tax treatment of various accounting items for Technology Pty Ltd, referencing the ITAA 1997 and ITAA 1936. It discusses trading stock valuation, service revenue recognition, depreciation expenses, profits from the sale of machinery and land, and the deductibility of repair and maintenance expenditures. The report also addresses borrowing expenses, employee entertainment costs, provisions for holiday and long service leave, research expenses, and bad debt write-offs, offering interpretative explanations for each item's tax implications and referencing relevant case law and taxation rulings to support the analysis. The aim is to provide the CFO with a clear understanding of how these accounting items should be treated for tax purposes.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Introduction:...............................................................................................................................2

Tax Treatment for accounting items:.........................................................................................2

Calculation of taxable income and tax payable by Technology Pty Ltd:..................................8

Conclusion:................................................................................................................................8

References:...............................................................................................................................10

Table of Contents

Introduction:...............................................................................................................................2

Tax Treatment for accounting items:.........................................................................................2

Calculation of taxable income and tax payable by Technology Pty Ltd:..................................8

Conclusion:................................................................................................................................8

References:...............................................................................................................................10

2TAXATION LAW

Introduction:

In the accrual accounting process an expenditure that originates from the

identification of the liabilities should be measured by referring to the anticipated cash flow on

the liability. Likewise, the income tax expenditure should reflect the amount of income taxes

to be paid in cash whether for the accounting period or for the future period. The current

report will be addressing the CFO of the Technological Computer Pty Ltd regarding the tax

treatment of the accounting items. An interpretative explanation would be provided for the

tax treatment of each accounting transactions by referring to the relevant statutory provisions

of the “ITAA 1997” and “ITAA 1936”.

Tax Treatment for accounting items:

Below listed are the tax treatments for the every items with relevant application of

statutory provisions, cases and rulings;

1). Trading stock on hand: According to the “section 28 of the ITAA 1936” it requires the

taxpayers to value the trading stock on hand at the start and at the end of the income year in

determining the taxable income of the taxpayer in carrying out the business (Woellner et al.

2016). The court of law in “All States Frozen Foods Pty Ltd v FC of T (1990)” upheld its

decision by stating that the goods that are en route from the overseas suppliers were in

definite situations regarded as the trading stock on hand for the taxpayer.

According to the “taxation ruling of IT 2670” goods are treated as the trading stock

on hand within the meaning of “section 28 of the ITAA 1936”, irrespective of the fact that

they are yet to be delivered physically to the business premises of the taxpayer or it is in the

position of disposing of the goods (Robin 2017). Here the trading stock is in transit from

Singapore and the same will be considered as trading stock on hand for Technology

Introduction:

In the accrual accounting process an expenditure that originates from the

identification of the liabilities should be measured by referring to the anticipated cash flow on

the liability. Likewise, the income tax expenditure should reflect the amount of income taxes

to be paid in cash whether for the accounting period or for the future period. The current

report will be addressing the CFO of the Technological Computer Pty Ltd regarding the tax

treatment of the accounting items. An interpretative explanation would be provided for the

tax treatment of each accounting transactions by referring to the relevant statutory provisions

of the “ITAA 1997” and “ITAA 1936”.

Tax Treatment for accounting items:

Below listed are the tax treatments for the every items with relevant application of

statutory provisions, cases and rulings;

1). Trading stock on hand: According to the “section 28 of the ITAA 1936” it requires the

taxpayers to value the trading stock on hand at the start and at the end of the income year in

determining the taxable income of the taxpayer in carrying out the business (Woellner et al.

2016). The court of law in “All States Frozen Foods Pty Ltd v FC of T (1990)” upheld its

decision by stating that the goods that are en route from the overseas suppliers were in

definite situations regarded as the trading stock on hand for the taxpayer.

According to the “taxation ruling of IT 2670” goods are treated as the trading stock

on hand within the meaning of “section 28 of the ITAA 1936”, irrespective of the fact that

they are yet to be delivered physically to the business premises of the taxpayer or it is in the

position of disposing of the goods (Robin 2017). Here the trading stock is in transit from

Singapore and the same will be considered as trading stock on hand for Technology

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Computer Pty Ltd. The amount results in increase in the stock value over the year therefore it

is included in the assessable income.

2). Service revenue $50,000: The “taxation ruling of TR 2014/1” is associated to the

derivation of income from the agreements relating to the right of using the proprietary

software and provisions relating to the services. According to the “taxation ruling of TR

2014/1” where the amount is adequately attributable based on the contract obligations under

the subject of “contingency of repayment” the sum will be considered derived under the

purpose of “section 6-5 of the ITAA 1997” when the obligations is entirely performed or the

contingency of repayment otherwise lapses.

As held in “Arthur Murray (NSW) Pty Ltd v FC of T (1965)” where the basic

obligations is completely performed or the contingency of repayment has lapsed the amount

that is appropriately billed to the obligations turns from “unearned income” to “earned

income” (Blakelock and King 2017). The sum of $50,000 will be included as service revenue

for assessment under the ordinary meaning of “section 6-5 of the ITAA 1997”.

3). Depreciation on Plant: The depreciation expenses is identified in compliance with the

AASB 116 property plant and equipment by allocating the assets depreciable sum in a

systematic manner over the useful life of the asset (Burton 2017). The treatment for tax is

based on the set rates given by the tax office. Similarly the deprecation expenses on plant

amounting to $300,000 will be included added back under the heads of “amounts not

deductible and other assessable amounts” instead of considering the sum of $375,000 in

determining the net accounting profit after tax. This is because the methods adopted for

accounts is different from the methods adopted for tax purpose.

4). Accounting profit on sale of machine: The sale of machine has resulted in gains for

accounting purpose represents the taxable profit of the machine based on the original cost

Computer Pty Ltd. The amount results in increase in the stock value over the year therefore it

is included in the assessable income.

2). Service revenue $50,000: The “taxation ruling of TR 2014/1” is associated to the

derivation of income from the agreements relating to the right of using the proprietary

software and provisions relating to the services. According to the “taxation ruling of TR

2014/1” where the amount is adequately attributable based on the contract obligations under

the subject of “contingency of repayment” the sum will be considered derived under the

purpose of “section 6-5 of the ITAA 1997” when the obligations is entirely performed or the

contingency of repayment otherwise lapses.

As held in “Arthur Murray (NSW) Pty Ltd v FC of T (1965)” where the basic

obligations is completely performed or the contingency of repayment has lapsed the amount

that is appropriately billed to the obligations turns from “unearned income” to “earned

income” (Blakelock and King 2017). The sum of $50,000 will be included as service revenue

for assessment under the ordinary meaning of “section 6-5 of the ITAA 1997”.

3). Depreciation on Plant: The depreciation expenses is identified in compliance with the

AASB 116 property plant and equipment by allocating the assets depreciable sum in a

systematic manner over the useful life of the asset (Burton 2017). The treatment for tax is

based on the set rates given by the tax office. Similarly the deprecation expenses on plant

amounting to $300,000 will be included added back under the heads of “amounts not

deductible and other assessable amounts” instead of considering the sum of $375,000 in

determining the net accounting profit after tax. This is because the methods adopted for

accounts is different from the methods adopted for tax purpose.

4). Accounting profit on sale of machine: The sale of machine has resulted in gains for

accounting purpose represents the taxable profit of the machine based on the original cost

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

(Chardon, Brimble and Freudenberg 2017). The accounting profit made from the sale of the

machinery is included into the taxable profit on the basis of the original cost of the

machinery.

5). Repairs and Maintenance Expenditure: The tax treatment for repairs and maintenance

expenses is given below;

a) Cost of replacing the entire roof: The “taxation ruling of TR 93/23” provides the

explanation relating to the circumstances under which the expenditure that is incurred by the

taxpayer on the repairs are considered for deductions under the “section 25-10 of the ITAA

1997” (Maley 2018). In context of “section 25-10 of the ITAA 1997” the term repair is

related to the work done on the premises, plants or articles. Evidently where the expenses

incurred in replacing or substantial reconstruction of entirety are allowed for deductions.

Under “section 25-10” of the act cost occurred for repairs are not deductible if the

expenses are capital in nature. As held in “Sun Newspaper Ltd v FC of T (1938)” held that

cost incurred in replacing a business structure is working or operating expenditure (Kiprotich

2016). Likewise the cost replacing is the entire will be allowed as deductions. The expense of

$90,600 is deductible under the heads of “deductible amounts”.

b). Cost of demolishing redundant building: The cost that is incurred on demolishing the

redundant building constitute work done in the sense of reconstruction of the entirety. In

“Hallstorms Pty Ltd v FC of T (1946)” the court of law stated that expenses that are

occurred in establishing or replacing the profit-yielding structure is capital expenses under

“section 25-10” of the act (Miller and Oats 2016). In the current context if Technology Pty

Ltd the expense of $5,400 is added back to profit on the basis of “items not allowed as

deductions”.

(Chardon, Brimble and Freudenberg 2017). The accounting profit made from the sale of the

machinery is included into the taxable profit on the basis of the original cost of the

machinery.

5). Repairs and Maintenance Expenditure: The tax treatment for repairs and maintenance

expenses is given below;

a) Cost of replacing the entire roof: The “taxation ruling of TR 93/23” provides the

explanation relating to the circumstances under which the expenditure that is incurred by the

taxpayer on the repairs are considered for deductions under the “section 25-10 of the ITAA

1997” (Maley 2018). In context of “section 25-10 of the ITAA 1997” the term repair is

related to the work done on the premises, plants or articles. Evidently where the expenses

incurred in replacing or substantial reconstruction of entirety are allowed for deductions.

Under “section 25-10” of the act cost occurred for repairs are not deductible if the

expenses are capital in nature. As held in “Sun Newspaper Ltd v FC of T (1938)” held that

cost incurred in replacing a business structure is working or operating expenditure (Kiprotich

2016). Likewise the cost replacing is the entire will be allowed as deductions. The expense of

$90,600 is deductible under the heads of “deductible amounts”.

b). Cost of demolishing redundant building: The cost that is incurred on demolishing the

redundant building constitute work done in the sense of reconstruction of the entirety. In

“Hallstorms Pty Ltd v FC of T (1946)” the court of law stated that expenses that are

occurred in establishing or replacing the profit-yielding structure is capital expenses under

“section 25-10” of the act (Miller and Oats 2016). In the current context if Technology Pty

Ltd the expense of $5,400 is added back to profit on the basis of “items not allowed as

deductions”.

5TAXATION LAW

c). Cost of converting the old storeroom into factory space: A guidelines has been

provided to differentiate between the capital and revenue outgoings by the court in “Sun

Newspaper Ltd v FC of T (1938)” for the purpose of forerunners under “section 8-1” of the

act (James and Nobes 2016). The decision of court have indicated that expenses occurred for

enlarging the profit generating structure is not allowed for deductions. The cost of $14,800

incurred by Technology Pty Ltd for converting the old storeroom into factory space

represents the renewal in the sense of reconstruction of the entirety. The expenses of $14,800

is added back to profit on the basis of “items not allowed as deductions”.

6). Borrowing expense written off: Expenses will be allowed for deductions under “section

8-1 of the ITAA 1997” if the expenses has sufficient association with the operations and

activities that is more directly associated to the generation of taxpayers assessable income. In

“FC of T v Lunney & Anor (1958)” the essentially characteristics of the expenses should be

determined as whether the outgoings has been incurred in producing the assessable income or

necessarily occurred in carrying on of the business (Keen and Mullins 2017). Similarly the

court in “Charles Moore & Co (WA) Pty Ltd v FC of T (1956)” held that the expenditure

should have the necessary association with the activities and the operations which is more

directly related to gain or generation of assessable income.

The expenses must meet the statutory criterion to be considered as outgoing incurred

in gaining assessable income. The borrowing expenses incurred by the Technology Pty Ltd

here is more directly related to gain or generation of assessable income. The expenses meet

the statutory criterion to be considered as outgoing incurred in gaining assessable income.

Therefore, the borrowing expenses of $5,400 is considered for subtraction purpose under the

heads of “deductible and non-assessable”.

c). Cost of converting the old storeroom into factory space: A guidelines has been

provided to differentiate between the capital and revenue outgoings by the court in “Sun

Newspaper Ltd v FC of T (1938)” for the purpose of forerunners under “section 8-1” of the

act (James and Nobes 2016). The decision of court have indicated that expenses occurred for

enlarging the profit generating structure is not allowed for deductions. The cost of $14,800

incurred by Technology Pty Ltd for converting the old storeroom into factory space

represents the renewal in the sense of reconstruction of the entirety. The expenses of $14,800

is added back to profit on the basis of “items not allowed as deductions”.

6). Borrowing expense written off: Expenses will be allowed for deductions under “section

8-1 of the ITAA 1997” if the expenses has sufficient association with the operations and

activities that is more directly associated to the generation of taxpayers assessable income. In

“FC of T v Lunney & Anor (1958)” the essentially characteristics of the expenses should be

determined as whether the outgoings has been incurred in producing the assessable income or

necessarily occurred in carrying on of the business (Keen and Mullins 2017). Similarly the

court in “Charles Moore & Co (WA) Pty Ltd v FC of T (1956)” held that the expenditure

should have the necessary association with the activities and the operations which is more

directly related to gain or generation of assessable income.

The expenses must meet the statutory criterion to be considered as outgoing incurred

in gaining assessable income. The borrowing expenses incurred by the Technology Pty Ltd

here is more directly related to gain or generation of assessable income. The expenses meet

the statutory criterion to be considered as outgoing incurred in gaining assessable income.

Therefore, the borrowing expenses of $5,400 is considered for subtraction purpose under the

heads of “deductible and non-assessable”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

7). Surplus on sale of land: According to the “section 108-5 of the ITAA 1997”, CGT asset

refers to any form of property or the equitable rights that is not treated as the property. A

“CGT event A1” under “section 104-10 (1) of the ITAA 1997” occurs when the entity

disposes a CGT asset (Zeff 2016). When an entity sell the commercial property it is more

likely to make the capital gains or loss. Capital gains made thereof are subjected to capital

gains tax based on the concessions for the small business. Technology Pty Ltd has reported

an accounting profit from the sale of surplus land which resulted in CGT event A1 under

“section 108-10 (1) of the ITAA 1997”. The accounting profit has been included as

assessable amounts in determining the net amount of tax payable.

8). Employee entertainment cost: The employee entertainment costs has been recognized as

the expenses in the accounting profit and the same has been allowed as deductions.

9). Provision for holiday and long service leave: An accrued employee entitlement in the

form of provision of long service leave is treated as the liability for entity under the

accounting standards (Oats, Miller and Mulligan 2017). For the purpose of taxation, an

accrued leave entitlement of the employee is not regarded for deductions during the year in

which it accrues. The expenses will be only allowed for deductions by the company on the

conditions that the liability is discharged.

Consequently, an adjustment is necessary under the “section 705-80” where the

liabilities of the joining entity should include such provision (Weinzierl 2018). In the current

situation of Technology Pty Ltd the directors have created a provision for long service leave

that amounted to $60,000. The provision for long service leave should be treated as the

liability of Technology Pty Ltd in accordance with the accounting principles for the purpose

7). Surplus on sale of land: According to the “section 108-5 of the ITAA 1997”, CGT asset

refers to any form of property or the equitable rights that is not treated as the property. A

“CGT event A1” under “section 104-10 (1) of the ITAA 1997” occurs when the entity

disposes a CGT asset (Zeff 2016). When an entity sell the commercial property it is more

likely to make the capital gains or loss. Capital gains made thereof are subjected to capital

gains tax based on the concessions for the small business. Technology Pty Ltd has reported

an accounting profit from the sale of surplus land which resulted in CGT event A1 under

“section 108-10 (1) of the ITAA 1997”. The accounting profit has been included as

assessable amounts in determining the net amount of tax payable.

8). Employee entertainment cost: The employee entertainment costs has been recognized as

the expenses in the accounting profit and the same has been allowed as deductions.

9). Provision for holiday and long service leave: An accrued employee entitlement in the

form of provision of long service leave is treated as the liability for entity under the

accounting standards (Oats, Miller and Mulligan 2017). For the purpose of taxation, an

accrued leave entitlement of the employee is not regarded for deductions during the year in

which it accrues. The expenses will be only allowed for deductions by the company on the

conditions that the liability is discharged.

Consequently, an adjustment is necessary under the “section 705-80” where the

liabilities of the joining entity should include such provision (Weinzierl 2018). In the current

situation of Technology Pty Ltd the directors have created a provision for long service leave

that amounted to $60,000. The provision for long service leave should be treated as the

liability of Technology Pty Ltd in accordance with the accounting principles for the purpose

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

of tax cost setting. The amount has been added back under the heads of “amounts non-

deductible”.

10). Research expenses on feasibility of opening new factory: According to the general

provisions given under the “section 8-1 of the ITAA 1997” losses or outgoings that are

preliminary to the beginning of the revenue generating activities of the taxpayers are treated

as not incurred in the course of business (Grange, Jover-Ledesma and Maydew 2014). A

guidelines has been provided to differentiate between the capital and revenue outgoings by

the court in “Softwood Pulp and Paper v FC of T (1976)” for the purpose of forerunners

under “section 8-1” of the act (Kenny, Blissenden and Villios 2018). The court stated that

feasibility study and other expenses incurred in determining whether or not the open a new

paper production was not allowed as deductions. The court held that the expenses were

preliminary in the beginning of the revenue producing activity. Similarly, the expenses

incurred by Technology Pty Ltd on feasibility study of opening a new factory in Perth is a

preliminary expenses which is not allowed for deductions. The amount has been added back

under the heads of “amounts not deductible and other assessable amounts”.

11). Bad debt write off$5,500: The “taxation ruling of TR 92/18” is associated with the

discussion relating to the writing of the bad debts. The “taxation ruling of TR 92/18”

provides the clarifications to the situations where the deductions for bad debt is allowed for

taxation purpose. Under “section 63 of the ITAA 1997” the bad should be written off during

the year of income prior to claiming the bad debt deductions (Sadiq et al. 2018). A taxpayer

is allowed to claim deductions for the bad debt in the year of income in which the debt is

written off. The court in “FC of T v Point” held that debt should be existence in order for the

debt to be written off as bad.

of tax cost setting. The amount has been added back under the heads of “amounts non-

deductible”.

10). Research expenses on feasibility of opening new factory: According to the general

provisions given under the “section 8-1 of the ITAA 1997” losses or outgoings that are

preliminary to the beginning of the revenue generating activities of the taxpayers are treated

as not incurred in the course of business (Grange, Jover-Ledesma and Maydew 2014). A

guidelines has been provided to differentiate between the capital and revenue outgoings by

the court in “Softwood Pulp and Paper v FC of T (1976)” for the purpose of forerunners

under “section 8-1” of the act (Kenny, Blissenden and Villios 2018). The court stated that

feasibility study and other expenses incurred in determining whether or not the open a new

paper production was not allowed as deductions. The court held that the expenses were

preliminary in the beginning of the revenue producing activity. Similarly, the expenses

incurred by Technology Pty Ltd on feasibility study of opening a new factory in Perth is a

preliminary expenses which is not allowed for deductions. The amount has been added back

under the heads of “amounts not deductible and other assessable amounts”.

11). Bad debt write off$5,500: The “taxation ruling of TR 92/18” is associated with the

discussion relating to the writing of the bad debts. The “taxation ruling of TR 92/18”

provides the clarifications to the situations where the deductions for bad debt is allowed for

taxation purpose. Under “section 63 of the ITAA 1997” the bad should be written off during

the year of income prior to claiming the bad debt deductions (Sadiq et al. 2018). A taxpayer

is allowed to claim deductions for the bad debt in the year of income in which the debt is

written off. The court in “FC of T v Point” held that debt should be existence in order for the

debt to be written off as bad.

8TAXATION LAW

As evident in the current situation of Technology Pty Ltd the company has reported

the writing off the bad debt that amounted to $5,500. The debt was written off during the year

of income by the company. Therefore, the amount has been included for subtractions under

the heads of “deductible amounts” for determining the net amount of tax payable.

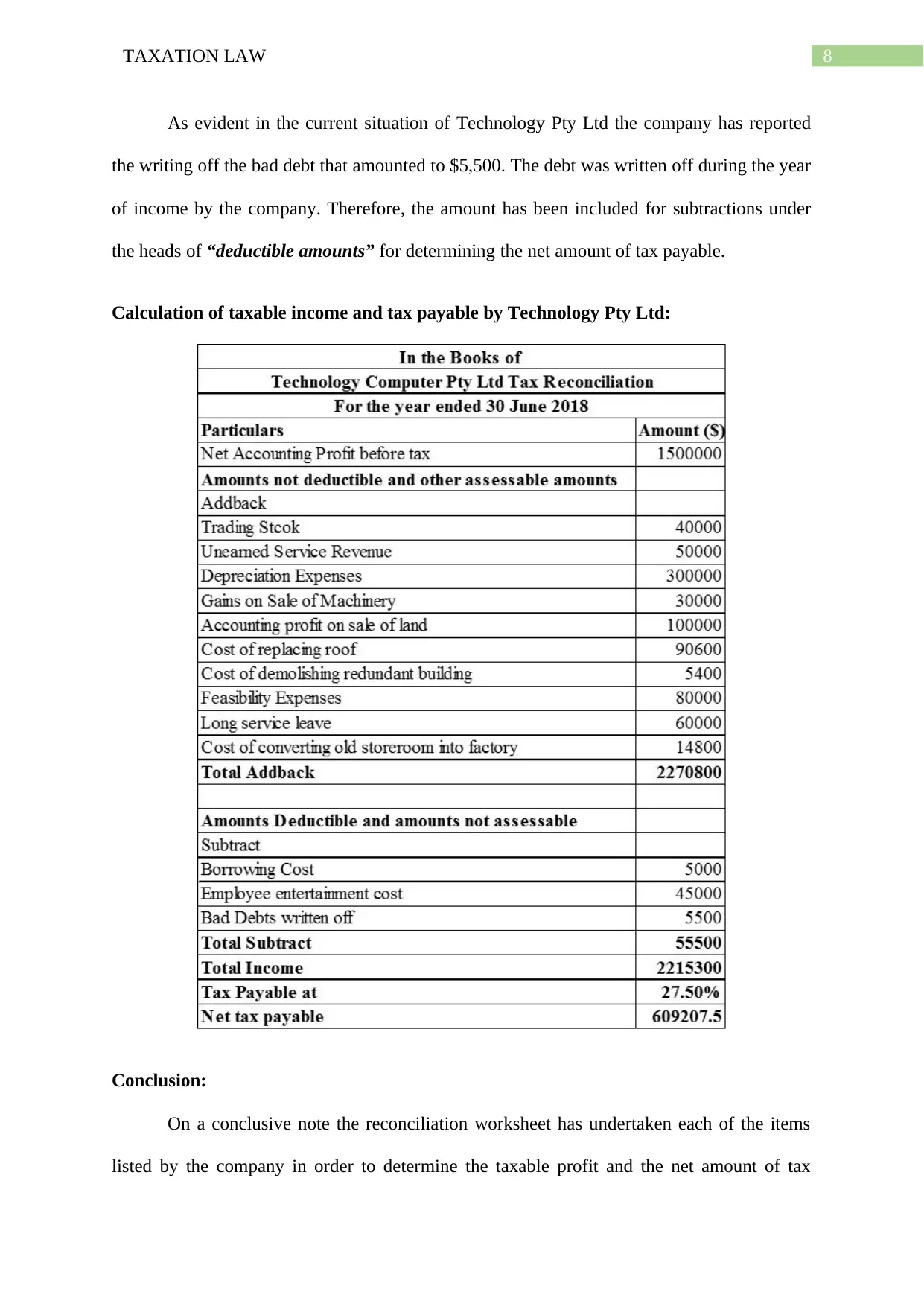

Calculation of taxable income and tax payable by Technology Pty Ltd:

Conclusion:

On a conclusive note the reconciliation worksheet has undertaken each of the items

listed by the company in order to determine the taxable profit and the net amount of tax

As evident in the current situation of Technology Pty Ltd the company has reported

the writing off the bad debt that amounted to $5,500. The debt was written off during the year

of income by the company. Therefore, the amount has been included for subtractions under

the heads of “deductible amounts” for determining the net amount of tax payable.

Calculation of taxable income and tax payable by Technology Pty Ltd:

Conclusion:

On a conclusive note the reconciliation worksheet has undertaken each of the items

listed by the company in order to determine the taxable profit and the net amount of tax

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

payable by the company. The worksheet began with the accounting profit or the profit before

tax and relevant applications of case laws, rulings and legislations was considered to provide

the CEO with the accounting treatment for tax purpose for each of the listed transactions. The

net amount of tax payable by the Technology Pty Ltd represents the amounts that is payable

by the company to the tax office on assessment for the assessment year by applying the

current tax rate and tax laws.

payable by the company. The worksheet began with the accounting profit or the profit before

tax and relevant applications of case laws, rulings and legislations was considered to provide

the CEO with the accounting treatment for tax purpose for each of the listed transactions. The

net amount of tax payable by the Technology Pty Ltd represents the amounts that is payable

by the company to the tax office on assessment for the assessment year by applying the

current tax rate and tax laws.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Blakelock, S. and King, P., 2017. Taxation law: The advance of ATO data

matching. Proctor, The, 37(6), p.18.

Burton, M., 2017. A Review of Judicial References to the Dictum of Jordan CJ, Expressed in

Scott v. Commissioner of Taxation, in Elaborating the Meaning of Income for the Purposes

of the Australian Income Tax. J. Austl. Tax'n, 19, p.50.

Chardon, T., Brimble, M. and Freudenberg, B., 2017. Tax and superannuation literacy:

Australian and New Zealand perspectives [Part 1]. Taxation Today, (102), pp.17-25.

Grange, J., Jover-Ledesma, G. and Maydew, G. 2014.Principles of business taxation.

James, S.R. and Nobes, C., 2016. Economics of Taxation: Principles, Policy and Practice.

Fiscal Publications.

Keen, M. and Mullins, P., 2017. International corporate taxation and the extractive industries:

principles, practice, problems. International Taxation and the Extractive Industries, New

York and London: Routledge.

Kenny, P., Blissenden, M. and Villios, S. 2018. Australian Tax.

Kiprotich, B.A., 2016. Principles of Taxation. governance.

Maley, M.N., 2018. Australian Taxation Office Guidance on the Diverted Profits Tax.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Oats, L., Miller, A. and Mulligan, E., 2017. Principles of International Taxation.

Robin, H., 2017. Australian taxation law 2017. Oxford University Press.

References:

Blakelock, S. and King, P., 2017. Taxation law: The advance of ATO data

matching. Proctor, The, 37(6), p.18.

Burton, M., 2017. A Review of Judicial References to the Dictum of Jordan CJ, Expressed in

Scott v. Commissioner of Taxation, in Elaborating the Meaning of Income for the Purposes

of the Australian Income Tax. J. Austl. Tax'n, 19, p.50.

Chardon, T., Brimble, M. and Freudenberg, B., 2017. Tax and superannuation literacy:

Australian and New Zealand perspectives [Part 1]. Taxation Today, (102), pp.17-25.

Grange, J., Jover-Ledesma, G. and Maydew, G. 2014.Principles of business taxation.

James, S.R. and Nobes, C., 2016. Economics of Taxation: Principles, Policy and Practice.

Fiscal Publications.

Keen, M. and Mullins, P., 2017. International corporate taxation and the extractive industries:

principles, practice, problems. International Taxation and the Extractive Industries, New

York and London: Routledge.

Kenny, P., Blissenden, M. and Villios, S. 2018. Australian Tax.

Kiprotich, B.A., 2016. Principles of Taxation. governance.

Maley, M.N., 2018. Australian Taxation Office Guidance on the Diverted Profits Tax.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Oats, L., Miller, A. and Mulligan, E., 2017. Principles of International Taxation.

Robin, H., 2017. Australian taxation law 2017. Oxford University Press.

11TAXATION LAW

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., Teoh, J. and Ting,

A. 2018. Principles of taxation law.

Weinzierl, M., 2018. Revisiting the Classical View of Benefit‐based Taxation. The Economic

Journal, 128(612), pp.F37-F64.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

Zeff, S.A., 2016. Forging accounting principles in five countries: A history and an analysis

of trends. Routledge.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., Teoh, J. and Ting,

A. 2018. Principles of taxation law.

Weinzierl, M., 2018. Revisiting the Classical View of Benefit‐based Taxation. The Economic

Journal, 128(612), pp.F37-F64.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

Zeff, S.A., 2016. Forging accounting principles in five countries: A history and an analysis

of trends. Routledge.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.