LEGL300 Taxation Law Assignment: Income Tax Consequences Analysis

VerifiedAdded on 2023/06/03

|10

|2427

|446

Homework Assignment

AI Summary

This assignment solution addresses two key questions in taxation law. The first question involves calculating the taxable income of Racing Parts Pty Ltd for the year ended 2018, considering various income and expense items such as exempted income, non-assessable non-exempt income, depreciation, bad debts, provisions for leave, dividends, borrowing expenses, donations, and other deductible expenses. The second question focuses on the determination of income tax consequences arising from transactions incurred by a self-employed architect named John, including the sale of a residential property and an antique desk, home office deductions, fines, capital improvements, depreciation of assets, travel expenses, and car expenses. The solution applies relevant sections of the ITAA 1997 and supporting case law to provide a comprehensive analysis of the tax implications of each scenario, including capital gains tax and allowable deductions.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:............................................................................................................. 2

Answer to question 2:............................................................................................................. 5

References:............................................................................................................................ 9

Table of Contents

Answer to question 1:............................................................................................................. 2

Answer to question 2:............................................................................................................. 5

References:............................................................................................................................ 9

2TAXATION LAW

Answer to question 1:

To determine the taxable income for Racing Parts Pty Ltd certain assumptions are

provided below regarding the exclusion and inclusion of income and expenses for tax

purpose.

a. Referring to

“section 6-20 of the ITAA 1997” the exempted income of $100,000 has

been considered as tax offset against the previous year loss figure of $120,000

incurred under

“Division 36”1. While the sum of $50,000 obtained as Non Assessable

Non Exempted income is included for assessment because previous year tax loss

incurred under Division 36 is deducted against the income.

b. Referring to Division 40 the depreciation sum of $30,000 has been considered for

deduction for taxation purpose.

c. The bad debt of $20,000 has been written off for deduction under

“section 25-35”

while provision for doubtful debt amounting to $40,000 is not allowed for deductions.

d. The amount of $35,000 relating to the provision of long service leave and annual

leave is excluded from the deduction since it is an accounting liabilities and non-

deductible for income tax purpose.

e. The cash dividend received by Racing Parts Pty Ltd has been considered for

assessment while the franking credits attached to the dividends is considered as tax

offset under

“section 67-25” which is equal to the amount of franking credits2.

f. With reference to

“section 8-1 of the ITAA 1997” the borrowing expense of $5000 is

treated as tax deductible expenditure because the expenses were occurred by

Racing Parts Pty Ltd in derivation of assessable income.

g. According to the judgement in

“Arnold v FCT (2017)” value of gifts and contributions

exceeding the amount of $2 given to the gift deductible recipient are treated as

permissible deduction under

“Division 30”. The donation and gift expenses incurred

by Racing Parts Pty Ltd will be treated as tax deductible expenses under

“Division

30”3.

1 Miller, Angharad, and Lynne Oats.

Principles of international taxation. Bloomsbury

Publishing, 2016.

2 James, Simon Robert, and Christopher Nobes.

Economics of Taxation: Principles, Policy

and Practice. Fiscal Publications, 2016.

3 Kabinga, M. "Established principles of taxation."

Tax justice & poverty (2015).

Answer to question 1:

To determine the taxable income for Racing Parts Pty Ltd certain assumptions are

provided below regarding the exclusion and inclusion of income and expenses for tax

purpose.

a. Referring to

“section 6-20 of the ITAA 1997” the exempted income of $100,000 has

been considered as tax offset against the previous year loss figure of $120,000

incurred under

“Division 36”1. While the sum of $50,000 obtained as Non Assessable

Non Exempted income is included for assessment because previous year tax loss

incurred under Division 36 is deducted against the income.

b. Referring to Division 40 the depreciation sum of $30,000 has been considered for

deduction for taxation purpose.

c. The bad debt of $20,000 has been written off for deduction under

“section 25-35”

while provision for doubtful debt amounting to $40,000 is not allowed for deductions.

d. The amount of $35,000 relating to the provision of long service leave and annual

leave is excluded from the deduction since it is an accounting liabilities and non-

deductible for income tax purpose.

e. The cash dividend received by Racing Parts Pty Ltd has been considered for

assessment while the franking credits attached to the dividends is considered as tax

offset under

“section 67-25” which is equal to the amount of franking credits2.

f. With reference to

“section 8-1 of the ITAA 1997” the borrowing expense of $5000 is

treated as tax deductible expenditure because the expenses were occurred by

Racing Parts Pty Ltd in derivation of assessable income.

g. According to the judgement in

“Arnold v FCT (2017)” value of gifts and contributions

exceeding the amount of $2 given to the gift deductible recipient are treated as

permissible deduction under

“Division 30”. The donation and gift expenses incurred

by Racing Parts Pty Ltd will be treated as tax deductible expenses under

“Division

30”3.

1 Miller, Angharad, and Lynne Oats.

Principles of international taxation. Bloomsbury

Publishing, 2016.

2 James, Simon Robert, and Christopher Nobes.

Economics of Taxation: Principles, Policy

and Practice. Fiscal Publications, 2016.

3 Kabinga, M. "Established principles of taxation."

Tax justice & poverty (2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

h. The expenditure occurred for the service of Managing Director husband as the

computer analyst is treated as tax deductible expenditure under the general provision

of

“section 8-1(1) of the ITAA 1997”. The outgoings were occurred in deriving the

assessable income of the Racing Parts Pty Ltd4.

i. Closing has been considered based on LIFO method and the same is included in

cost of goods for tax deductible in order to provide Racing Parts Pty Ltd with higher

tax deductions.

j. With respect to

“Division 36” the tax loss of $120,000 reported by Racing Parts Pty

Ltd during the income year is considered for offset against the NANE and Exempted

Income.

k. Expenses on repair incurred on plant constitutes deductible expenses under

“section

25-10 of the ITAA 1997” because it was occurred in restoring the efficiency of the

plant without changing its nature.

4 Fleurbaey, Marc, and François Maniquet.

Optimal taxation theory and principles of fairness.

No. 2015005. Université catholique de Louvain, Center for Operations Research and

Econometrics (CORE), 2015.

h. The expenditure occurred for the service of Managing Director husband as the

computer analyst is treated as tax deductible expenditure under the general provision

of

“section 8-1(1) of the ITAA 1997”. The outgoings were occurred in deriving the

assessable income of the Racing Parts Pty Ltd4.

i. Closing has been considered based on LIFO method and the same is included in

cost of goods for tax deductible in order to provide Racing Parts Pty Ltd with higher

tax deductions.

j. With respect to

“Division 36” the tax loss of $120,000 reported by Racing Parts Pty

Ltd during the income year is considered for offset against the NANE and Exempted

Income.

k. Expenses on repair incurred on plant constitutes deductible expenses under

“section

25-10 of the ITAA 1997” because it was occurred in restoring the efficiency of the

plant without changing its nature.

4 Fleurbaey, Marc, and François Maniquet.

Optimal taxation theory and principles of fairness.

No. 2015005. Université catholique de Louvain, Center for Operations Research and

Econometrics (CORE), 2015.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

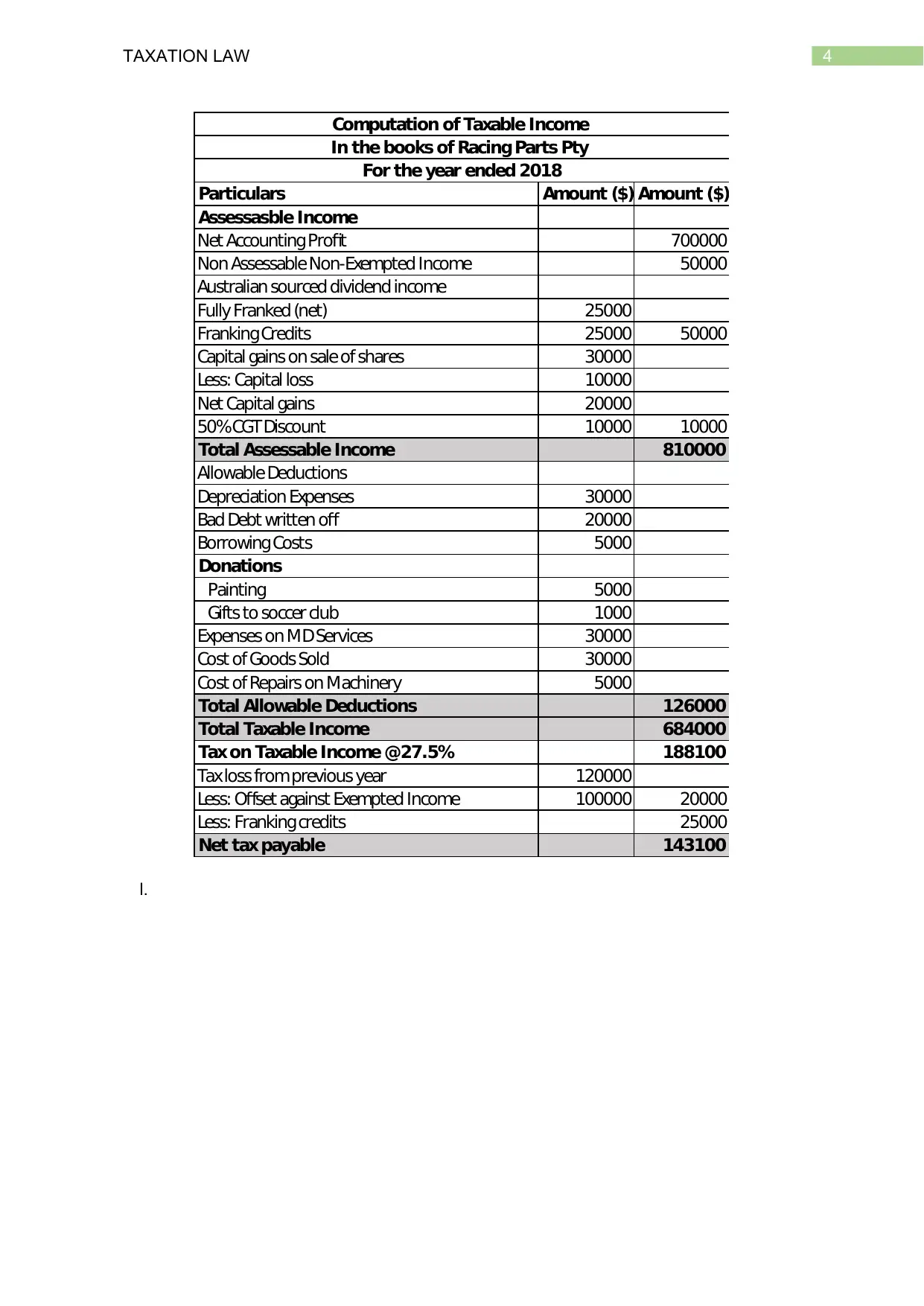

Particulars Amount ($) Amount ($)

Assessasble Income

Net Accounting Profit 700000

Non Assessable Non-Exempted Income 50000

Australian sourced dividend income

Fully Franked (net) 25000

FrankingCredits 25000 50000

Capital gains on sale of shares 30000

Less: Capital loss 10000

Net Capital gains 20000

50%CGT Discount 10000 10000

Total Assessable Income 810000

Allowable Deductions

Depreciation Expenses 30000

Bad Debt written off 20000

Borrowing Costs 5000

Donations

Painting 5000

Gifts to soccer club 1000

Expenses on MDServices 30000

Cost of Goods Sold 30000

Cost of Repairs on Machinery 5000

Total Allowable Deductions 126000

Total Taxable Income 684000

Tax on Taxable Income @27.5% 188100

Taxloss fromprevious year 120000

Less: Offset against Exempted Income 100000 20000

Less: Frankingcredits 25000

Net tax payable 143100

Computation of Taxable Income

In the books of Racing Parts Pty

For the year ended 2018

l.

Particulars Amount ($) Amount ($)

Assessasble Income

Net Accounting Profit 700000

Non Assessable Non-Exempted Income 50000

Australian sourced dividend income

Fully Franked (net) 25000

FrankingCredits 25000 50000

Capital gains on sale of shares 30000

Less: Capital loss 10000

Net Capital gains 20000

50%CGT Discount 10000 10000

Total Assessable Income 810000

Allowable Deductions

Depreciation Expenses 30000

Bad Debt written off 20000

Borrowing Costs 5000

Donations

Painting 5000

Gifts to soccer club 1000

Expenses on MDServices 30000

Cost of Goods Sold 30000

Cost of Repairs on Machinery 5000

Total Allowable Deductions 126000

Total Taxable Income 684000

Tax on Taxable Income @27.5% 188100

Taxloss fromprevious year 120000

Less: Offset against Exempted Income 100000 20000

Less: Frankingcredits 25000

Net tax payable 143100

Computation of Taxable Income

In the books of Racing Parts Pty

For the year ended 2018

l.

5TAXATION LAW

Answer to question 2:

Issue:

The current issue is associated with the determination of the income tax

consequences from the transactions incurred by the taxpayer in the relevant income year.

The issue here would take into the account the capital gains tax consequences that arises

from the sale of residential property and antique desk.

Rule:

According to the explanation given under the

“Taxation Ruling of TR 93/30” where

the home office is simply is used by the taxpayer for deriving assessable income but does

not comprises the character of business place only the appropriate part of the running

outgoings will be allowed for deductions5. To support the argument the decision made by

court in

“Swinford v FC of T (1984)” held that the self-employed script writer was allowed

deduction under the positive limbs of

“section 8-1 of the ITAA 1997” relating to the portion of

rent that was paid for house where a separate room was dedicated by the taxpayer for the

purpose of study.

According to the

“section 26-5 of the ITAA 1997” a taxpayer is not allowed to claim

deduction for the expenses that are incurred in the form of fines or penalties for breaching

the Australian law6.

According to

“Taxation Ruling of TR 97/23” outgoings occurred in replacing the

exhaust fans and locks of a permanent fixtures installed in property that are employed for

deriving assessable income are held as repairs of deductible nature under

“section 25-10”7.

An exception to this rule is that repairs or replacement of damaged unit by a new unit would

not be treated as repairs instead it constitute an improvement of capital nature. The

explanation made in

“Western Suburbs Cinemas v FC of T (1952)” stated that the replacing

the old ceiling with an improved and new ceiling was treated as the improvement carrying

capital nature and was held as non-allowable expenditure under

“section 25-10”8.

5 Sikka, Prem. "Accounting and taxation: Conjoined twins or separate siblings?."

Accounting

forum. Vol. 41. No. 4. Elsevier, 2017.

6 Bankman, Joseph, et al.

Federal Income Taxation. Wolters Kluwer Law & Business, 2017.

7 Schenk, Deborah H.

Federal Taxation of S Corporations. Law Journal Press, 2017

Answer to question 2:

Issue:

The current issue is associated with the determination of the income tax

consequences from the transactions incurred by the taxpayer in the relevant income year.

The issue here would take into the account the capital gains tax consequences that arises

from the sale of residential property and antique desk.

Rule:

According to the explanation given under the

“Taxation Ruling of TR 93/30” where

the home office is simply is used by the taxpayer for deriving assessable income but does

not comprises the character of business place only the appropriate part of the running

outgoings will be allowed for deductions5. To support the argument the decision made by

court in

“Swinford v FC of T (1984)” held that the self-employed script writer was allowed

deduction under the positive limbs of

“section 8-1 of the ITAA 1997” relating to the portion of

rent that was paid for house where a separate room was dedicated by the taxpayer for the

purpose of study.

According to the

“section 26-5 of the ITAA 1997” a taxpayer is not allowed to claim

deduction for the expenses that are incurred in the form of fines or penalties for breaching

the Australian law6.

According to

“Taxation Ruling of TR 97/23” outgoings occurred in replacing the

exhaust fans and locks of a permanent fixtures installed in property that are employed for

deriving assessable income are held as repairs of deductible nature under

“section 25-10”7.

An exception to this rule is that repairs or replacement of damaged unit by a new unit would

not be treated as repairs instead it constitute an improvement of capital nature. The

explanation made in

“Western Suburbs Cinemas v FC of T (1952)” stated that the replacing

the old ceiling with an improved and new ceiling was treated as the improvement carrying

capital nature and was held as non-allowable expenditure under

“section 25-10”8.

5 Sikka, Prem. "Accounting and taxation: Conjoined twins or separate siblings?."

Accounting

forum. Vol. 41. No. 4. Elsevier, 2017.

6 Bankman, Joseph, et al.

Federal Income Taxation. Wolters Kluwer Law & Business, 2017.

7 Schenk, Deborah H.

Federal Taxation of S Corporations. Law Journal Press, 2017

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

As defined under

“section 40-25 (1) of the ITAA 1997” a taxpayer is allowed to

deduction relating to the depreciating asset that is equivalent to the sum of decline in value

during the income year.

Correspondingly, travel from and to the place of work is not allowed for deductions

since it is treated as the private expenditure of domestic nature. However, travel in the

course of employment will be held as permissible deductions. Evidently the decision made in

the case of

“Weiner v FCT (1978)” held that the teacher was permitted deductions for the

travelling expenditure because the travel from one place of employment to another place

was travel during the course of work9.

As per the ATO when a taxpayer uses their own car for carrying out business

activities then the expenses incurred for the business purpose would be treated as the

allowable deduction. The expenses are viewed as car expenditure. By using the log book

method, the business proportion of the car expenses used by the taxpayer during business

will be allowed for deductions.

The main residence of an individual taxpayer is generally held exempted from the

provision of capital gains tax10. Nevertheless, the taxpayer can obtain the partial main

residence exemption if any part of the property is used by the taxpayer for deriving

assessable income. As per the ATO a taxpayer under the interest deductibility test can claim

an allowable deduction relating to the amount of money borrowed for purchasing the

residential property and interest occurred from such borrowed funds.

“Section 108-10 (1)” explains that the taxpayer must separate any amount of capital loss and

under

“section 108-10 (4) of the ITAA 1997” the net amount of capital loss can be carried

forward in the relevant income year.

Application:

8 Murphy, Kevin E., and Mark Higgins.

Concepts in Federal Taxation 2017. Cengage

Learning, 2016.

9 Schmalbeck, Richard, Lawrence Zelenak, and Sarah B. Lawsky.

Federal Income Taxation.

Wolters Kluwer Law & Business, 2015.

10 Simmons, Daniel L., et al.

Federal Income Taxation. Foundation Press, 2017.

As defined under

“section 40-25 (1) of the ITAA 1997” a taxpayer is allowed to

deduction relating to the depreciating asset that is equivalent to the sum of decline in value

during the income year.

Correspondingly, travel from and to the place of work is not allowed for deductions

since it is treated as the private expenditure of domestic nature. However, travel in the

course of employment will be held as permissible deductions. Evidently the decision made in

the case of

“Weiner v FCT (1978)” held that the teacher was permitted deductions for the

travelling expenditure because the travel from one place of employment to another place

was travel during the course of work9.

As per the ATO when a taxpayer uses their own car for carrying out business

activities then the expenses incurred for the business purpose would be treated as the

allowable deduction. The expenses are viewed as car expenditure. By using the log book

method, the business proportion of the car expenses used by the taxpayer during business

will be allowed for deductions.

The main residence of an individual taxpayer is generally held exempted from the

provision of capital gains tax10. Nevertheless, the taxpayer can obtain the partial main

residence exemption if any part of the property is used by the taxpayer for deriving

assessable income. As per the ATO a taxpayer under the interest deductibility test can claim

an allowable deduction relating to the amount of money borrowed for purchasing the

residential property and interest occurred from such borrowed funds.

“Section 108-10 (1)” explains that the taxpayer must separate any amount of capital loss and

under

“section 108-10 (4) of the ITAA 1997” the net amount of capital loss can be carried

forward in the relevant income year.

Application:

8 Murphy, Kevin E., and Mark Higgins.

Concepts in Federal Taxation 2017. Cengage

Learning, 2016.

9 Schmalbeck, Richard, Lawrence Zelenak, and Sarah B. Lawsky.

Federal Income Taxation.

Wolters Kluwer Law & Business, 2015.

10 Simmons, Daniel L., et al.

Federal Income Taxation. Foundation Press, 2017.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

The case study provides that John is a self-employed architect and purchased a

residential property in the outskirts of Melbourne. John used a portion of house for his

architect business where his clients could visit him. An expenses in the form of interest on

loan was occurred by John during the income year. Referring to the

“Swinford v FC of T

(1984)” a deduction is allowed to John for loan interest of house. John can claim deduction

under

“section 8-1 of the ITAA 1997” up to the part of house that is exclusively used from

where he carried is business activities11. Later John reports a payment of fine for installing

door without obtaining permission. The fines imposed will be non-deductible under section

26-5 since it is a breach of Australian law.

John reports expenses on his house where the old carpet in his room was replaced

by the new carpet of improved quality and incurred a cost of $6000. Referring to

“Western

Suburbs Cinemas v FC of T (1952)” replacing the old carpet with new on is a capital

improvement and not allowed for deduction under

“section 25-10 of the ITAA 1997”.

An antique desk was bought by John for the purpose of work. Citing

“section 40-25

(1) of the ITAA 1997” a deduction is allowable to John for an equivalent amount that is

related to the decline in the value of antique desk. John later reports traveling to visit clients

regarding the building designs and simultaneously travelled to the building sites. Referring to“Weiner v FCT (1978)” the travel by John is the travel during the course of work and any

expenses arising thereof is deductible12. John later reports car expenses that was used for

business purpose. With the help of log book only the business proportion will be permitted

for deduction while the private part of car expenses is non-deductible.

The house bought by John during July 2018 was eventually sold. Since John used

the house for generating income he can claim partial main residence exemption. The interest

expenses on borrowed funds meets the interest deductibility test and hence will be allowed

for deduction. Furthermore, the sale of antique desk resulted loss and hence under

“section

108-10 (4) of the ITAA 1997” the net amount of capital loss can be carried forward by John

in the relevant income year.

Conclusion:

11 Seto, Theodore.

Federal Income Taxation: Cases, Problems, and Materials. West

Academic Publishing, 2015.

12 Finkelstein, Maurice. "Cases on Federal Taxation (Book Review)." (2014): 22.

The case study provides that John is a self-employed architect and purchased a

residential property in the outskirts of Melbourne. John used a portion of house for his

architect business where his clients could visit him. An expenses in the form of interest on

loan was occurred by John during the income year. Referring to the

“Swinford v FC of T

(1984)” a deduction is allowed to John for loan interest of house. John can claim deduction

under

“section 8-1 of the ITAA 1997” up to the part of house that is exclusively used from

where he carried is business activities11. Later John reports a payment of fine for installing

door without obtaining permission. The fines imposed will be non-deductible under section

26-5 since it is a breach of Australian law.

John reports expenses on his house where the old carpet in his room was replaced

by the new carpet of improved quality and incurred a cost of $6000. Referring to

“Western

Suburbs Cinemas v FC of T (1952)” replacing the old carpet with new on is a capital

improvement and not allowed for deduction under

“section 25-10 of the ITAA 1997”.

An antique desk was bought by John for the purpose of work. Citing

“section 40-25

(1) of the ITAA 1997” a deduction is allowable to John for an equivalent amount that is

related to the decline in the value of antique desk. John later reports traveling to visit clients

regarding the building designs and simultaneously travelled to the building sites. Referring to“Weiner v FCT (1978)” the travel by John is the travel during the course of work and any

expenses arising thereof is deductible12. John later reports car expenses that was used for

business purpose. With the help of log book only the business proportion will be permitted

for deduction while the private part of car expenses is non-deductible.

The house bought by John during July 2018 was eventually sold. Since John used

the house for generating income he can claim partial main residence exemption. The interest

expenses on borrowed funds meets the interest deductibility test and hence will be allowed

for deduction. Furthermore, the sale of antique desk resulted loss and hence under

“section

108-10 (4) of the ITAA 1997” the net amount of capital loss can be carried forward by John

in the relevant income year.

Conclusion:

11 Seto, Theodore.

Federal Income Taxation: Cases, Problems, and Materials. West

Academic Publishing, 2015.

12 Finkelstein, Maurice. "Cases on Federal Taxation (Book Review)." (2014): 22.

8TAXATION LAW

On a conclusive note, a deduction will be allowed to John incurred for home office

purpose but john cannot claim any deduction for capital expenses. Similarly a partial main

residence exemption can be claimed by John as the property was partially used for

generating income.

On a conclusive note, a deduction will be allowed to John incurred for home office

purpose but john cannot claim any deduction for capital expenses. Similarly a partial main

residence exemption can be claimed by John as the property was partially used for

generating income.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

References:

Bankman, Joseph, et al.

Federal Income Taxation. Wolters Kluwer Law & Business, 2017.

Finkelstein, Maurice. "Cases on Federal Taxation (Book Review)." (2014): 22.

Fleurbaey, Marc, and François Maniquet.

Optimal taxation theory and principles of fairness.

No. 2015005. Université catholique de Louvain, Center for Operations Research and

Econometrics (CORE), 2015.

James, Simon Robert, and Christopher Nobes.

Economics of Taxation: Principles, Policy

and Practice. Fiscal Publications, 2016.

Kabinga, M. "Established principles of taxation."

Tax justice & poverty (2015).

Miller, Angharad, and Lynne Oats.

Principles of international taxation. Bloomsbury

Publishing, 2016.

Murphy, Kevin E., and Mark Higgins.

Concepts in Federal Taxation 2017. Cengage

Learning, 2016.

Schenk, Deborah H.

Federal Taxation of S Corporations. Law Journal Press, 2017.

Schmalbeck, Richard, Lawrence Zelenak, and Sarah B. Lawsky.

Federal Income Taxation.

Wolters Kluwer Law & Business, 2015.

Seto, Theodore.

Federal Income Taxation: Cases, Problems, and Materials. West Academic

Publishing, 2015.

Sikka, Prem. "Accounting and taxation: Conjoined twins or separate siblings?."

Accounting

forum. Vol. 41. No. 4. Elsevier, 2017.

Simmons, Daniel L., et al.

Federal Income Taxation. Foundation Press, 2017.

References:

Bankman, Joseph, et al.

Federal Income Taxation. Wolters Kluwer Law & Business, 2017.

Finkelstein, Maurice. "Cases on Federal Taxation (Book Review)." (2014): 22.

Fleurbaey, Marc, and François Maniquet.

Optimal taxation theory and principles of fairness.

No. 2015005. Université catholique de Louvain, Center for Operations Research and

Econometrics (CORE), 2015.

James, Simon Robert, and Christopher Nobes.

Economics of Taxation: Principles, Policy

and Practice. Fiscal Publications, 2016.

Kabinga, M. "Established principles of taxation."

Tax justice & poverty (2015).

Miller, Angharad, and Lynne Oats.

Principles of international taxation. Bloomsbury

Publishing, 2016.

Murphy, Kevin E., and Mark Higgins.

Concepts in Federal Taxation 2017. Cengage

Learning, 2016.

Schenk, Deborah H.

Federal Taxation of S Corporations. Law Journal Press, 2017.

Schmalbeck, Richard, Lawrence Zelenak, and Sarah B. Lawsky.

Federal Income Taxation.

Wolters Kluwer Law & Business, 2015.

Seto, Theodore.

Federal Income Taxation: Cases, Problems, and Materials. West Academic

Publishing, 2015.

Sikka, Prem. "Accounting and taxation: Conjoined twins or separate siblings?."

Accounting

forum. Vol. 41. No. 4. Elsevier, 2017.

Simmons, Daniel L., et al.

Federal Income Taxation. Foundation Press, 2017.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.