Detailed Report: Australian Taxation Laws, Deductions, and Credits

VerifiedAdded on 2020/06/06

|11

|2211

|41

Report

AI Summary

This report provides a detailed analysis of Australian taxation laws, focusing on various aspects such as income tax calculation under ITAA 1997, general deductions, and GST credits. The report examines specific scenarios, including the deductibility of expenses related to business relocation and legal costs. It also delves into the calculation of GST credits for businesses launching new products and services. Furthermore, the report includes a comprehensive calculation of a taxpayer's gross income, expenses, and foreign tax offset, providing a step-by-step breakdown of the process. The report concludes with an overview of the key takeaways from each section and the implications of the tax laws.

Taxation Laws

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Question 1........................................................................................................................................1

Introduction............................................................................................................................1

Critical Analysis.....................................................................................................................1

Supporting Evidences.............................................................................................................2

Conclusion..............................................................................................................................3

Question 2........................................................................................................................................3

Critical Analysis.....................................................................................................................3

Supporting Evidences.............................................................................................................4

Conclusion..............................................................................................................................4

Question 3........................................................................................................................................4

Q.4..........................................................................................................................................7

Conclusion.......................................................................................................................................7

References........................................................................................................................................8

Books and Journals.................................................................................................................8

Question 1........................................................................................................................................1

Introduction............................................................................................................................1

Critical Analysis.....................................................................................................................1

Supporting Evidences.............................................................................................................2

Conclusion..............................................................................................................................3

Question 2........................................................................................................................................3

Critical Analysis.....................................................................................................................3

Supporting Evidences.............................................................................................................4

Conclusion..............................................................................................................................4

Question 3........................................................................................................................................4

Q.4..........................................................................................................................................7

Conclusion.......................................................................................................................................7

References........................................................................................................................................8

Books and Journals.................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Question 1.

Introduction

ITAA 1997 expanded as Income Tax Act 1997 made by the Parliament of Australia.

Through it income tax can be calculated and was taken from Income Tax Assessment Act 1936

and in this new amendments was done in year 1997. Section 8-1 of this act details about the

deductions for expenses included in getting assessable income. Section 25-5 shows tax

deductibility of overheads on managing tax affairs. It is not related to above provision as this

expenditure does not have to do with producing income 1. Stock or the shares information is

described from the Section 70-40 which highlights the buying and selling of the shares. There are

also other provisions like Section 104-5, 104-145 and 116-30. There can be deductions from the

the assessable income which has been gained for the aim of gaining net income. In the same

provision there should be a business activity. No losses can be deducted if it is of the capital

nature or domestic nature. On the other hand if the losses are incurred during gaining some sort

of income. All the losses which can be deducted in the whole section will be refereed to as

general deduction.

Critical Analysis

In the situation given where cost of moving to a new site is a expense which is done for

the business purpose so that they can get better business environment thus increasing their profit

margins. According to this they have to look at the deductions as mentioned in the Section 8-1 of

ITAA 1997. Cost of moving fixed assets from one site to another can be called as expenses & no

deduction are available under Section 8-1 of ITAA 1997. In this case expenses can increase the

cost of the item for purposes of depreciation 2.

On the other hand in the case of cost of revaluing assets to effect insurance cover the

expenses are related to fixed assets. In determining deductibility it is relevant whether the

expenses enhance or enlarge income earning capacity or are faced just to protect it. If the end and

1 Woellner, R and et. al., 2011. Australian Taxation Law Select: legislation and

commentary. CCH Australia.

2 Olatunji, O. A., 2011. A preliminary review on the legal implications of BIM and model

ownership. Journal of Information Technology in Construction (Itcon). 16(40). pp.687-696.

1

Introduction

ITAA 1997 expanded as Income Tax Act 1997 made by the Parliament of Australia.

Through it income tax can be calculated and was taken from Income Tax Assessment Act 1936

and in this new amendments was done in year 1997. Section 8-1 of this act details about the

deductions for expenses included in getting assessable income. Section 25-5 shows tax

deductibility of overheads on managing tax affairs. It is not related to above provision as this

expenditure does not have to do with producing income 1. Stock or the shares information is

described from the Section 70-40 which highlights the buying and selling of the shares. There are

also other provisions like Section 104-5, 104-145 and 116-30. There can be deductions from the

the assessable income which has been gained for the aim of gaining net income. In the same

provision there should be a business activity. No losses can be deducted if it is of the capital

nature or domestic nature. On the other hand if the losses are incurred during gaining some sort

of income. All the losses which can be deducted in the whole section will be refereed to as

general deduction.

Critical Analysis

In the situation given where cost of moving to a new site is a expense which is done for

the business purpose so that they can get better business environment thus increasing their profit

margins. According to this they have to look at the deductions as mentioned in the Section 8-1 of

ITAA 1997. Cost of moving fixed assets from one site to another can be called as expenses & no

deduction are available under Section 8-1 of ITAA 1997. In this case expenses can increase the

cost of the item for purposes of depreciation 2.

On the other hand in the case of cost of revaluing assets to effect insurance cover the

expenses are related to fixed assets. In determining deductibility it is relevant whether the

expenses enhance or enlarge income earning capacity or are faced just to protect it. If the end and

1 Woellner, R and et. al., 2011. Australian Taxation Law Select: legislation and

commentary. CCH Australia.

2 Olatunji, O. A., 2011. A preliminary review on the legal implications of BIM and model

ownership. Journal of Information Technology in Construction (Itcon). 16(40). pp.687-696.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

if the benefit is likely to be temporary and normally the expenses is likely to be come again then

it should be deductible under Section 8-1.

In the legal expenses comes over by the firm opposing a petition for winding up is a issue

which shows whether the expenditure is related to the infrastructure and income earning capacity

of the business or just its operations. It looks that if the result of a case would be outcome in the

extinction of profit making ability as in the case then the expense will be regarded as capital in

nature. But if the case has more to do with the procedure of operating the business, then it will be

considered as revenue in nature 3.

In the legal expenses which come over for the services of a solicitor in respect of a

number of matters, including conveyancing, discharge of a mortgage and general legal advice

considering to client's business operations. This cannot be cleared out till more information can

be provided. It is necessary to know the nature or type of the expenses, apportionment and any

other.

Supporting Evidences

A general deduction can be called as the loss or certain which has to be deduced under

the general principles of deductibility. It is the part of the Section 8-1 of ITAA 1997 and they

need the loss or current to have the suitable coordination with assessable income or carrying on

of an enterprise given that they not have a capital, private or domestic nature. In the case of

moving machinery loss occurred in the case of capital, private and domestic nature will not be

included 4. A tax payer is eligible for the general abstraction which is part of the section 8-1 with

including current loss or outgoing convince any single or double positive limbs in the subsection

8-1(1).

If the money received is in the form of insurance so whatever the money is received than

the party have to pay the tax because that amount will come in assessable income. This is shown

in Subdivision 20-A.

3 O'Connell, A., Martin, F and Chia, J., 2013. Law, policy and politics in Australia's recent

not-for-profit sector reforms. Austl. Tax F. 28. p.289.

4 Brandon, G., 2016. Mid market focus: Tax treatment of consumables and stores. Taxation

in Australia. 50(7). p.374.

2

it should be deductible under Section 8-1.

In the legal expenses comes over by the firm opposing a petition for winding up is a issue

which shows whether the expenditure is related to the infrastructure and income earning capacity

of the business or just its operations. It looks that if the result of a case would be outcome in the

extinction of profit making ability as in the case then the expense will be regarded as capital in

nature. But if the case has more to do with the procedure of operating the business, then it will be

considered as revenue in nature 3.

In the legal expenses which come over for the services of a solicitor in respect of a

number of matters, including conveyancing, discharge of a mortgage and general legal advice

considering to client's business operations. This cannot be cleared out till more information can

be provided. It is necessary to know the nature or type of the expenses, apportionment and any

other.

Supporting Evidences

A general deduction can be called as the loss or certain which has to be deduced under

the general principles of deductibility. It is the part of the Section 8-1 of ITAA 1997 and they

need the loss or current to have the suitable coordination with assessable income or carrying on

of an enterprise given that they not have a capital, private or domestic nature. In the case of

moving machinery loss occurred in the case of capital, private and domestic nature will not be

included 4. A tax payer is eligible for the general abstraction which is part of the section 8-1 with

including current loss or outgoing convince any single or double positive limbs in the subsection

8-1(1).

If the money received is in the form of insurance so whatever the money is received than

the party have to pay the tax because that amount will come in assessable income. This is shown

in Subdivision 20-A.

3 O'Connell, A., Martin, F and Chia, J., 2013. Law, policy and politics in Australia's recent

not-for-profit sector reforms. Austl. Tax F. 28. p.289.

4 Brandon, G., 2016. Mid market focus: Tax treatment of consumables and stores. Taxation

in Australia. 50(7). p.374.

2

Legal expenses are non commercial business operations which may give its contribute to

a tax loss as it is not a assessable income. This is briefed by Division 35 of Income Tax

Assessment Act 1997.

Conclusion

Tax is to be paid or not it depend upon the activities which is carried out by the firm. If

the activity is a commercial activities and is done with purpose of profit making then they have

to pay the tax. In the case of legal activity they does not have to pay the taxes 5.

Question 2.

Introduction

Anyone can request a credit for GST added in amount of any particular goods and

services that he purchase for their enterprise 6. It is referred as GST credit or an input tax credit

fro the taxes which has added in the amount of the enterprise inputs. GST is applied to the sale of

particular property like vacant lying land new residential places and the commercial areas. For

this the person need to have registration. In the scenario Big Bank Ltd is going to launch home

and contents insurance policies and they estimated that this will constitute 2% of the total

enterprise. They had been successful in estimating about this and the rest 98% of the business is

made up of their traditional loans and deposit businesses 7. In previous month, the advertising

advisor issued their tax invoice for $1,650000. This will deal with that how the bank with claim

GST credits.

Critical Analysis

The bank can claim it in their activity statement and to claim GST credits they they are

able to apply four conditions:-

5 Buchanan, R and Consett, E., 2016. Section 974-80 ITAA97: The current state of

play. Tax Specialist. 19(5). p.217.

6 Gitman, L J., Juchau, R and Flanagan, J., 2015. Principles of managerial finance.

Pearson Higher Education AU.

7 Schenk, A., Thuronyi, V and Cui, W., 2015. Value added tax. Cambridge University

Press.

3

a tax loss as it is not a assessable income. This is briefed by Division 35 of Income Tax

Assessment Act 1997.

Conclusion

Tax is to be paid or not it depend upon the activities which is carried out by the firm. If

the activity is a commercial activities and is done with purpose of profit making then they have

to pay the tax. In the case of legal activity they does not have to pay the taxes 5.

Question 2.

Introduction

Anyone can request a credit for GST added in amount of any particular goods and

services that he purchase for their enterprise 6. It is referred as GST credit or an input tax credit

fro the taxes which has added in the amount of the enterprise inputs. GST is applied to the sale of

particular property like vacant lying land new residential places and the commercial areas. For

this the person need to have registration. In the scenario Big Bank Ltd is going to launch home

and contents insurance policies and they estimated that this will constitute 2% of the total

enterprise. They had been successful in estimating about this and the rest 98% of the business is

made up of their traditional loans and deposit businesses 7. In previous month, the advertising

advisor issued their tax invoice for $1,650000. This will deal with that how the bank with claim

GST credits.

Critical Analysis

The bank can claim it in their activity statement and to claim GST credits they they are

able to apply four conditions:-

5 Buchanan, R and Consett, E., 2016. Section 974-80 ITAA97: The current state of

play. Tax Specialist. 19(5). p.217.

6 Gitman, L J., Juchau, R and Flanagan, J., 2015. Principles of managerial finance.

Pearson Higher Education AU.

7 Schenk, A., Thuronyi, V and Cui, W., 2015. Value added tax. Cambridge University

Press.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

If they have intention to buy solely in transmit their business and purchase does not have

to do with input taxed supplies.

To include the purchase price with GST

They give payment for the product which they have purchased

Have tax invoice from suppliers

Big Bank cannot claim input tax credits for the amount $1,100,000 as this was an older expense

and was used for basic advertising campaigns which included television, radio and the print

promotions. The reason of this is that they have not done promotion for the new product and this

was not part of this campaigns 8. For the new product they have launched new promotional and

advertising campaigns and spent around $1,650,000. So for this they can claim input tax credits

as it is the recent business operations which are done to promote their new service among people.

Supporting Evidences

It can be claimed for creditable acquisitions and a acquisition will not be creditable to the

extent that is related to making supplies that would be input taxed. There might be a negotiations

between a firm that has manufacturing operations and a prospective purchaser of the activity.

Both the parties have to face sustainable cost which can happen diligence, take advice of the

lawyers who will help them in knowing certain necessary requirements 9.

Conclusion

So the bank have to pay the GST for the normal advertising not for the new product

promotional campaigns.

Question 3

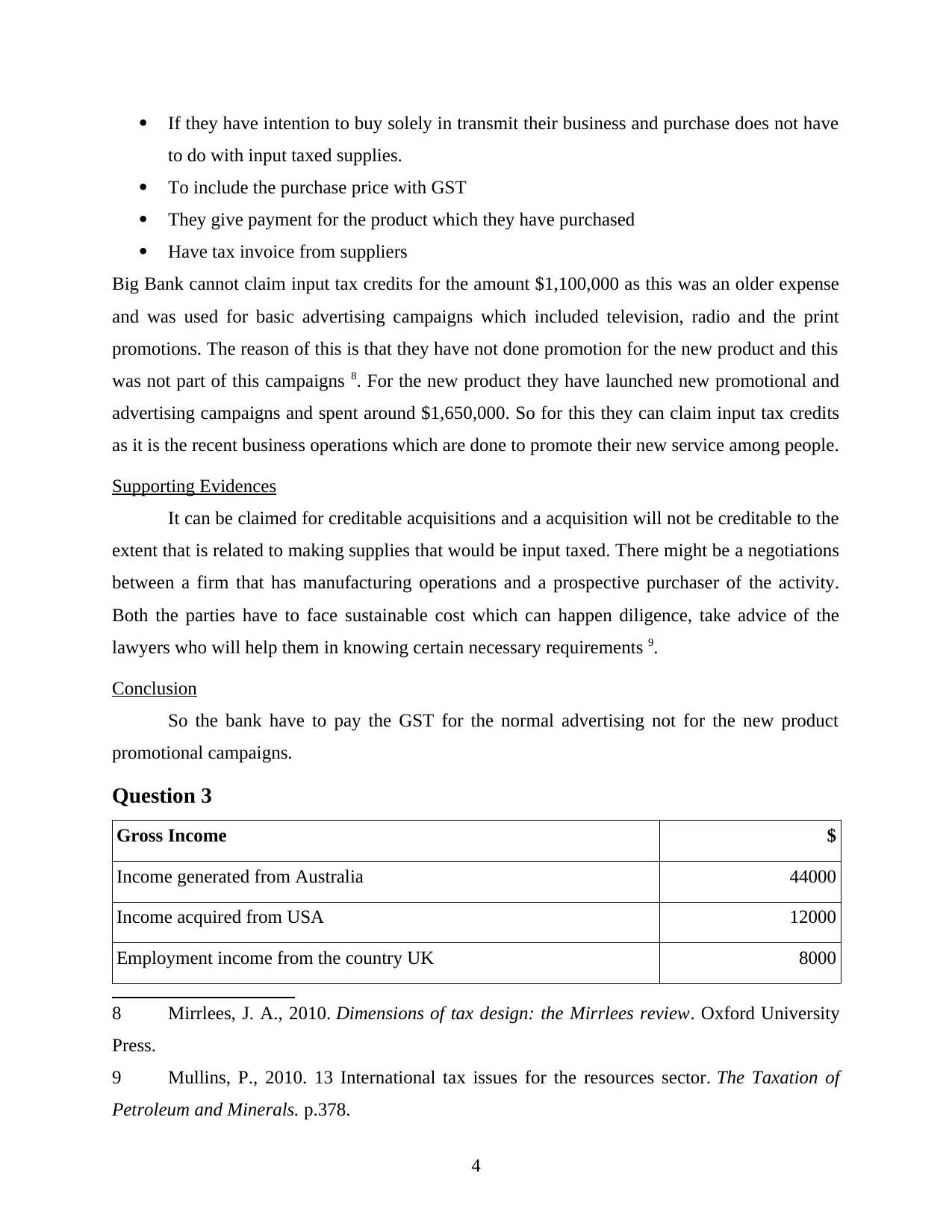

Gross Income $

Income generated from Australia 44000

Income acquired from USA 12000

Employment income from the country UK 8000

8 Mirrlees, J. A., 2010. Dimensions of tax design: the Mirrlees review. Oxford University

Press.

9 Mullins, P., 2010. 13 International tax issues for the resources sector. The Taxation of

Petroleum and Minerals. p.378.

4

to do with input taxed supplies.

To include the purchase price with GST

They give payment for the product which they have purchased

Have tax invoice from suppliers

Big Bank cannot claim input tax credits for the amount $1,100,000 as this was an older expense

and was used for basic advertising campaigns which included television, radio and the print

promotions. The reason of this is that they have not done promotion for the new product and this

was not part of this campaigns 8. For the new product they have launched new promotional and

advertising campaigns and spent around $1,650,000. So for this they can claim input tax credits

as it is the recent business operations which are done to promote their new service among people.

Supporting Evidences

It can be claimed for creditable acquisitions and a acquisition will not be creditable to the

extent that is related to making supplies that would be input taxed. There might be a negotiations

between a firm that has manufacturing operations and a prospective purchaser of the activity.

Both the parties have to face sustainable cost which can happen diligence, take advice of the

lawyers who will help them in knowing certain necessary requirements 9.

Conclusion

So the bank have to pay the GST for the normal advertising not for the new product

promotional campaigns.

Question 3

Gross Income $

Income generated from Australia 44000

Income acquired from USA 12000

Employment income from the country UK 8000

8 Mirrlees, J. A., 2010. Dimensions of tax design: the Mirrlees review. Oxford University

Press.

9 Mullins, P., 2010. 13 International tax issues for the resources sector. The Taxation of

Petroleum and Minerals. p.378.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Property rental income which is in UK 2000

UK's dividend income 1200

Income of the interest from UK 800

Overall Gross Income 68000

Expenses $

Expenses incurred from medical 5000

Cost came in taking out employment income from Australia 4000

Expenses which incurred while taking employment income generated

from USA

900

Cost of the expenses which came while deriving rental income from

UK

500

Deductible gift recipient 400

Interest (debt deductions) came in taking out dividend income 140

Expenses (debt deductions) in knowing interest income 60

Overall expenses 11000

Overseas tax paid $

USA employment income 3600

Dividend income which came form UK 120

UK's income of interest 80

Income of rent of UK 600

Overall foreign tax paid 4400

Angelo can calculate his foreign tax offset through following:

Taxable Income= Total Gross Income – Total Expenses

5

UK's dividend income 1200

Income of the interest from UK 800

Overall Gross Income 68000

Expenses $

Expenses incurred from medical 5000

Cost came in taking out employment income from Australia 4000

Expenses which incurred while taking employment income generated

from USA

900

Cost of the expenses which came while deriving rental income from

UK

500

Deductible gift recipient 400

Interest (debt deductions) came in taking out dividend income 140

Expenses (debt deductions) in knowing interest income 60

Overall expenses 11000

Overseas tax paid $

USA employment income 3600

Dividend income which came form UK 120

UK's income of interest 80

Income of rent of UK 600

Overall foreign tax paid 4400

Angelo can calculate his foreign tax offset through following:

Taxable Income= Total Gross Income – Total Expenses

5

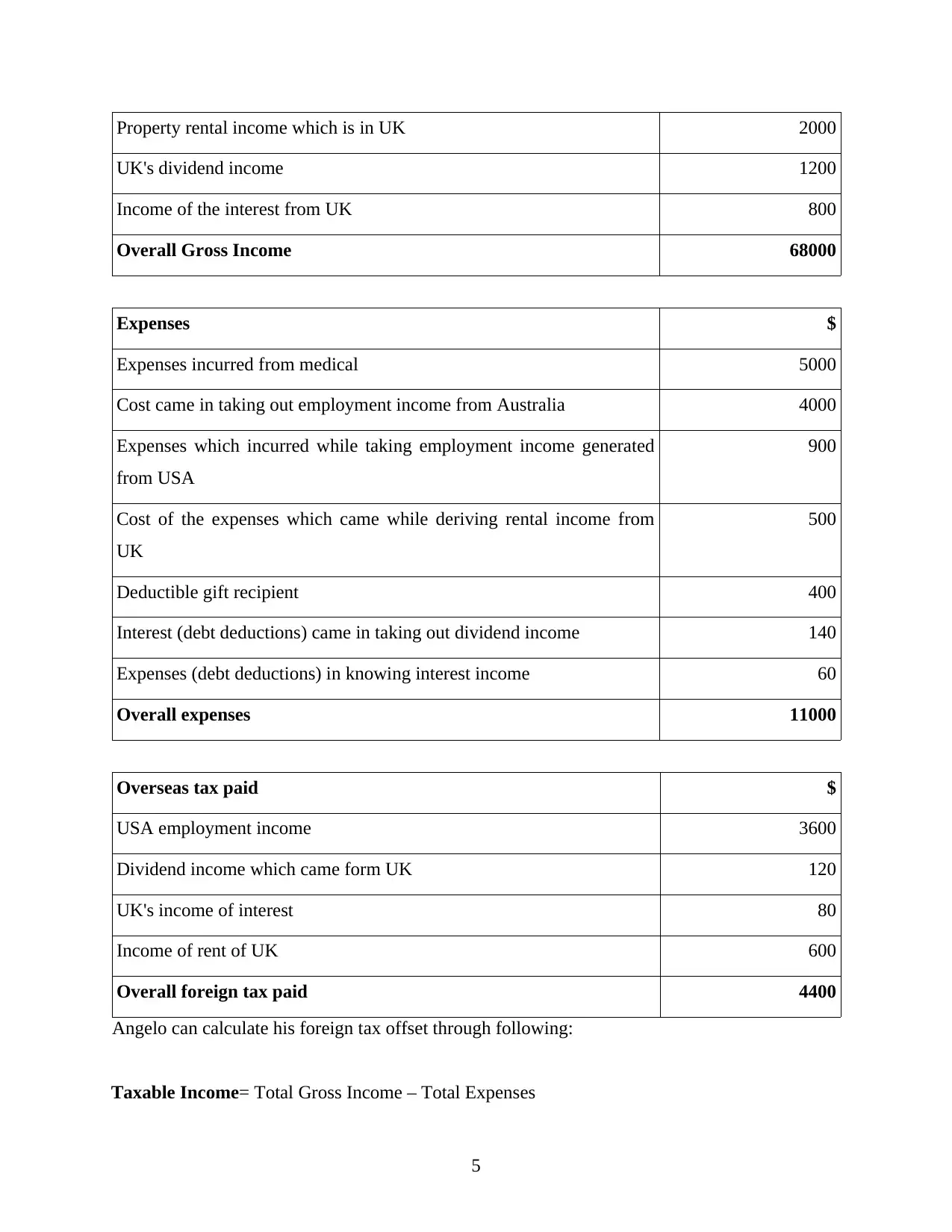

68000-11000= 57000

Tax which needs to paid on taxable income defined

Tax on $57000= $10072

In assessable income overseas amount income will not be calculated. So those expenses

will not be considered and they are the expenses that are include in his assessable income in

which the foreign income has been paid 10.

Kinds of Expenses Incurred i.e., which happened in taking employment income from US

is 900 and expenses happened in taking rental income from UK is 500. The overall expenses will

be the sum of these i.e., is 1400. Debt dedications and interest income of $200 are not included

as he is not permanent resident of those overseas countries 11. In the same there will be disregard

of deduction of $400 for the gift recipient.

Calculation:

Taxable income excluding the foreign tax paid i.e., $68000 – $4400= $63600

Less allowable deduction excluding expenses i.e., $11000-4400= $6600

So the taxable income= $63600-6600

$57000

Tax on $57000 is $10,072

11000-10072= $928

$928 will be the overseas income tax offset of Angelo but he has paid foreign tax of $4400 and

his foreign tax is limited to $928. So, the difference of both cannot be refunded.

10 Genschel, P and Schwarz, P., 2011. Tax competition: a literature review. Socio-Economic

Review. 9(2). pp.339-370.

11 Garnaut, R., 2010. Principles and practice of resource rent taxation. Australian Economic

Review. 43(4). pp.347-356.

6

Tax which needs to paid on taxable income defined

Tax on $57000= $10072

In assessable income overseas amount income will not be calculated. So those expenses

will not be considered and they are the expenses that are include in his assessable income in

which the foreign income has been paid 10.

Kinds of Expenses Incurred i.e., which happened in taking employment income from US

is 900 and expenses happened in taking rental income from UK is 500. The overall expenses will

be the sum of these i.e., is 1400. Debt dedications and interest income of $200 are not included

as he is not permanent resident of those overseas countries 11. In the same there will be disregard

of deduction of $400 for the gift recipient.

Calculation:

Taxable income excluding the foreign tax paid i.e., $68000 – $4400= $63600

Less allowable deduction excluding expenses i.e., $11000-4400= $6600

So the taxable income= $63600-6600

$57000

Tax on $57000 is $10,072

11000-10072= $928

$928 will be the overseas income tax offset of Angelo but he has paid foreign tax of $4400 and

his foreign tax is limited to $928. So, the difference of both cannot be refunded.

10 Genschel, P and Schwarz, P., 2011. Tax competition: a literature review. Socio-Economic

Review. 9(2). pp.339-370.

11 Garnaut, R., 2010. Principles and practice of resource rent taxation. Australian Economic

Review. 43(4). pp.347-356.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

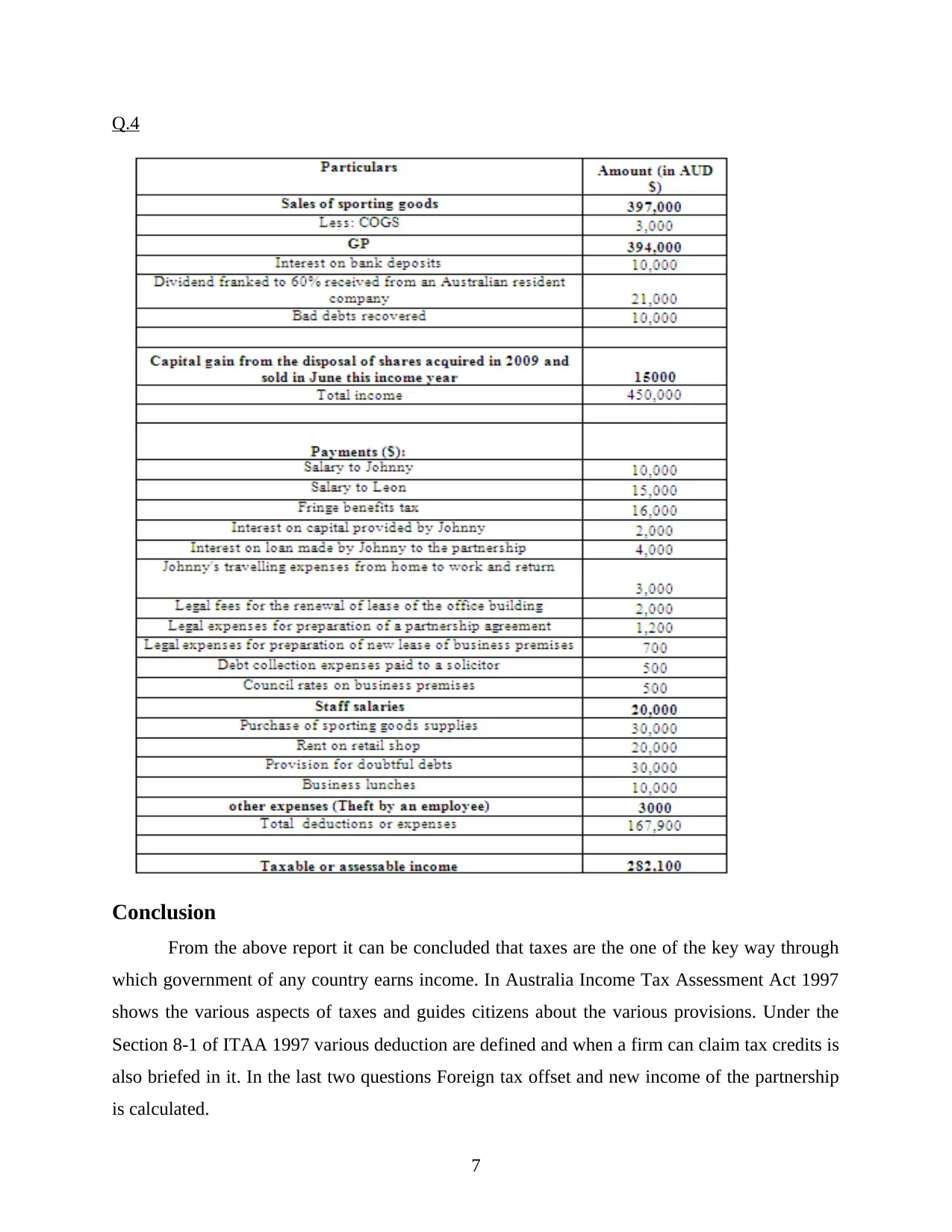

Q.4

Conclusion

From the above report it can be concluded that taxes are the one of the key way through

which government of any country earns income. In Australia Income Tax Assessment Act 1997

shows the various aspects of taxes and guides citizens about the various provisions. Under the

Section 8-1 of ITAA 1997 various deduction are defined and when a firm can claim tax credits is

also briefed in it. In the last two questions Foreign tax offset and new income of the partnership

is calculated.

7

Conclusion

From the above report it can be concluded that taxes are the one of the key way through

which government of any country earns income. In Australia Income Tax Assessment Act 1997

shows the various aspects of taxes and guides citizens about the various provisions. Under the

Section 8-1 of ITAA 1997 various deduction are defined and when a firm can claim tax credits is

also briefed in it. In the last two questions Foreign tax offset and new income of the partnership

is calculated.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.