Taxation Laws Assignment: Compensation, CGT, and Legal Fees Analysis

VerifiedAdded on 2023/01/03

|14

|3707

|39

Homework Assignment

AI Summary

This assignment addresses two key questions related to Australian taxation laws. The first question examines the tax implications of compensation received for patent infringement, loss of income, interest on compensation, and reimbursement of legal fees. The analysis considers whether receipts are of a capital or revenue nature, referencing relevant case law and sections of the ITAA 1997 to determine assessable income. The second question explores the application of Capital Gains Tax (CGT) on the subdivision of land, distinguishing between pre-CGT and post-CGT assets and considering different methods for assessing capital gains. The assignment emphasizes the importance of determining the date of asset purchase and the nature of the CGT event, providing a comprehensive overview of relevant tax regulations.

Running head: TAXATION LAWS

Taxation Laws

Name of the Student:

Name of the University:

Author’s Note

Taxation Laws

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAWS

Table of Contents

Answer to question 1.................................................................................................................2

Issues.....................................................................................................................................2

Rule........................................................................................................................................3

Application............................................................................................................................5

Conclusion.............................................................................................................................6

Answer to Question 2................................................................................................................7

Issues.....................................................................................................................................7

Laws......................................................................................................................................7

Application..........................................................................................................................10

Conclusion...........................................................................................................................12

Reference.................................................................................................................................13

Table of Contents

Answer to question 1.................................................................................................................2

Issues.....................................................................................................................................2

Rule........................................................................................................................................3

Application............................................................................................................................5

Conclusion.............................................................................................................................6

Answer to Question 2................................................................................................................7

Issues.....................................................................................................................................7

Laws......................................................................................................................................7

Application..........................................................................................................................10

Conclusion...........................................................................................................................12

Reference.................................................................................................................................13

2TAXATION LAWS

Answer to question 1

Issues

a) Is there any tax liability on the taxpayer for the $ 300,000 which is received by the

taxpayer as compensation damages for breaching patents rights?

b) Will the taxpayers be held liable for the compensation which is received for loss of

income as considered in the case study?

c) Will the taxpayer be held liable for tax on interest that is received on compensation?

d) Is reimbursement of legal fees considered as ordinary income?

Rule

There are cases where the cash which is received for the damage which is done to an

asset of a business which affects its operation or usage or any form of revenue generating

activity, then in such cases the cash received would be treated as capital receipts. The

compensation which is paid for damage caused to a capital asset would be considered to be a

capital receipt was stated in the verdict given in “Glenboig Union Fireclay Co Ltd v IRC

(1921)”.

In case any damage is caused to an asset of a business, then the business receives a

lumpsum payment which is compensation for the damage and the same can be treated as either

revenue or capital receipts which would entirely depend on the nature of receipt. The Federal

Commissioner in the case of “FCT v Federal Wharf Co Ltd” provided the verdict that the

compensation which is received by a taxpayer for loss of income would be considered to be a

revenue natured receipt and therefore the same would be subjected to taxes (Askari, Cummings

& Glover, 2013). The term compensatory payment was effectively described by law as payment

Answer to question 1

Issues

a) Is there any tax liability on the taxpayer for the $ 300,000 which is received by the

taxpayer as compensation damages for breaching patents rights?

b) Will the taxpayers be held liable for the compensation which is received for loss of

income as considered in the case study?

c) Will the taxpayer be held liable for tax on interest that is received on compensation?

d) Is reimbursement of legal fees considered as ordinary income?

Rule

There are cases where the cash which is received for the damage which is done to an

asset of a business which affects its operation or usage or any form of revenue generating

activity, then in such cases the cash received would be treated as capital receipts. The

compensation which is paid for damage caused to a capital asset would be considered to be a

capital receipt was stated in the verdict given in “Glenboig Union Fireclay Co Ltd v IRC

(1921)”.

In case any damage is caused to an asset of a business, then the business receives a

lumpsum payment which is compensation for the damage and the same can be treated as either

revenue or capital receipts which would entirely depend on the nature of receipt. The Federal

Commissioner in the case of “FCT v Federal Wharf Co Ltd” provided the verdict that the

compensation which is received by a taxpayer for loss of income would be considered to be a

revenue natured receipt and therefore the same would be subjected to taxes (Askari, Cummings

& Glover, 2013). The term compensatory payment was effectively described by law as payment

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAWS

received by an entity as the right of seeking compensation or as a result of cause of action which

is related to the right of underlying asset. The amount which is received as compensatory damage

would be included in assessable income at the time of its receipts within the “Division 6 of the

ITAA 1997” or may be treated as statutory income for tax purpose.

The provisions of “section 25 (1), ITAA 1997” makes it clear that the payment which is

received by the taxpayer in respect of loss of profits which is related to a period of time would be

considered as assessable income. As per cases rulings of “Mc Laurin v FC of T (1961)” the

compensation which is paid to the taxpayer would be held taxable within the legislation of

“subsection 25 (1), ITAA 1936” if the same is satisfying the condition that the income is

recognised.

In some cases, a taxpayer can also receive compensation for damage which may

temporary or permanent damage which is caused of a capital asset. Alternative situation where

such cases would arise are termination of contract, business dealings gone wrong. The

compensation which is received by the taxpayer in such scenarios would be considered as a part

of assessable income of the business.

The federal commissioner provided a verdict on “Californian Oil Products Ltd v FCT

(1934)” that the compensation which the taxpayer receives for the opportunity to make profits or

lost earnings would be treated as ordinary income within the ruling of “section 6-5, ITAA 1997”

The amount which is generated is treated as income because it is generated and closely related to

its business activities.

An alternative verdict was also provided by “CT (Vic) v Phillips (1936)” that when any

compensation for damage that are closely related with the business loss or commercial structure

received by an entity as the right of seeking compensation or as a result of cause of action which

is related to the right of underlying asset. The amount which is received as compensatory damage

would be included in assessable income at the time of its receipts within the “Division 6 of the

ITAA 1997” or may be treated as statutory income for tax purpose.

The provisions of “section 25 (1), ITAA 1997” makes it clear that the payment which is

received by the taxpayer in respect of loss of profits which is related to a period of time would be

considered as assessable income. As per cases rulings of “Mc Laurin v FC of T (1961)” the

compensation which is paid to the taxpayer would be held taxable within the legislation of

“subsection 25 (1), ITAA 1936” if the same is satisfying the condition that the income is

recognised.

In some cases, a taxpayer can also receive compensation for damage which may

temporary or permanent damage which is caused of a capital asset. Alternative situation where

such cases would arise are termination of contract, business dealings gone wrong. The

compensation which is received by the taxpayer in such scenarios would be considered as a part

of assessable income of the business.

The federal commissioner provided a verdict on “Californian Oil Products Ltd v FCT

(1934)” that the compensation which the taxpayer receives for the opportunity to make profits or

lost earnings would be treated as ordinary income within the ruling of “section 6-5, ITAA 1997”

The amount which is generated is treated as income because it is generated and closely related to

its business activities.

An alternative verdict was also provided by “CT (Vic) v Phillips (1936)” that when any

compensation for damage that are closely related with the business loss or commercial structure

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAWS

that forms a major portion of the activities which are undertaken by the business then the

compensation amount would be regarded as loss which is attributable to capital loss. In the case

of “FCT v Spedley Securities Ltd (1988)” it was also noticed that compensation which is

received for the damaged caused to goodwill would be considered capital receipt.

The interest received along the compensation would also be considered to be assessable

for the purpose of taxation as per the provisions stated in “section 6-5, ITAA 1997”. In addition

to this, the court also provided the verdict in “DFCT v Whitaker (1998)” that post judgement

interest is similar to income generated under ordinary concept. When a taxpayer receives interest

on the ordinary income than the same should also be considered for the purpose of taxation.

The taxpayers are also eligible for claiming deductions for the purpose of tax assessment

on legal charges as per the provisions which is stated under “section 8-1 of the ITAA 1997” and

it is also to be noted that amount which is paid as an award for legal expenses would also be

included in assessment of tax as per “subdivision 20-A”. Legal outgoings that is paid to a

business or a person is mainly for indemnifying the receiver for any legal expenses. As the legal

fees are not treated as ordinary income but the same is treated as assessment recoupment under

“subsection 20-20 (2)”.

Application

The case of Our Earth Pty Ltd shows that the business designs and manufactures coffee

cups which is then sold in the market. The management of Our Earth Pty Ltd hears the new that

Coffee Beans Pty Ltd has copied their cup designs and selling the same in overseas market and

that too at a significant discount for attracting more customers. On the basis of the news the

management of Our Earth Pty Ltd filed a complaint suit which the management won and was

that forms a major portion of the activities which are undertaken by the business then the

compensation amount would be regarded as loss which is attributable to capital loss. In the case

of “FCT v Spedley Securities Ltd (1988)” it was also noticed that compensation which is

received for the damaged caused to goodwill would be considered capital receipt.

The interest received along the compensation would also be considered to be assessable

for the purpose of taxation as per the provisions stated in “section 6-5, ITAA 1997”. In addition

to this, the court also provided the verdict in “DFCT v Whitaker (1998)” that post judgement

interest is similar to income generated under ordinary concept. When a taxpayer receives interest

on the ordinary income than the same should also be considered for the purpose of taxation.

The taxpayers are also eligible for claiming deductions for the purpose of tax assessment

on legal charges as per the provisions which is stated under “section 8-1 of the ITAA 1997” and

it is also to be noted that amount which is paid as an award for legal expenses would also be

included in assessment of tax as per “subdivision 20-A”. Legal outgoings that is paid to a

business or a person is mainly for indemnifying the receiver for any legal expenses. As the legal

fees are not treated as ordinary income but the same is treated as assessment recoupment under

“subsection 20-20 (2)”.

Application

The case of Our Earth Pty Ltd shows that the business designs and manufactures coffee

cups which is then sold in the market. The management of Our Earth Pty Ltd hears the new that

Coffee Beans Pty Ltd has copied their cup designs and selling the same in overseas market and

that too at a significant discount for attracting more customers. On the basis of the news the

management of Our Earth Pty Ltd filed a complaint suit which the management won and was

5TAXATION LAWS

awarded $ 300,000 as damage compensation for infringement of patent rights. The nature of

receipts is to be considered in such a case in order to determine whether the same would be

included in assessable income of the business (White, Blackwood & Cooper, 2019). The case of

CT (Vic) v Phillips (1936)” shows that the compensation which is generated is provided for a

damage which is caused to the asset of the business. As the amount $ 300,000 is paid to the

company for damaged caused to patent rights therefore the nature of the receipts would be

considered to be capital in nature and therefore the same would not be attracting taxes.

In addition to this, Our Earth Pty Ltd was also awarded with the amount of $200,000 as

loss compensation for the past 12 months. By referring the case laws of “Californian Oil

Products Ltd FCT (1934)” it can be said that compensation which is received for loss of revenue

for the company would be considered as taxable income. The amount which is received by Our

Earth Pty Ltd is of revenue nature as the same is closely related to the main functions of the

business. Therefore, the amount of $ 200,000 would be considered for the purpose to be included

in the tax assessment with in the ordinary concepts of the “section 6-5, of the ITAA 1997”.

The management of Our Earth Pty Ltd also received interest which was awarded along

with the compensation The decision of the Federal commissioner in “Whitaker v FCT (1998)”

the interest received would be regarded as post judgement. The interest income will be included

within the ordinary meaning of “section 6-5, ITAA 1997” for assessment purpose. In addition to

this, Our Earth Pty Ltd also received legal fees imbursement which should be considered as a

part of the ordinary income. Therefore, the amount will be included for assessment purpose of

“subdivision 20-A”.

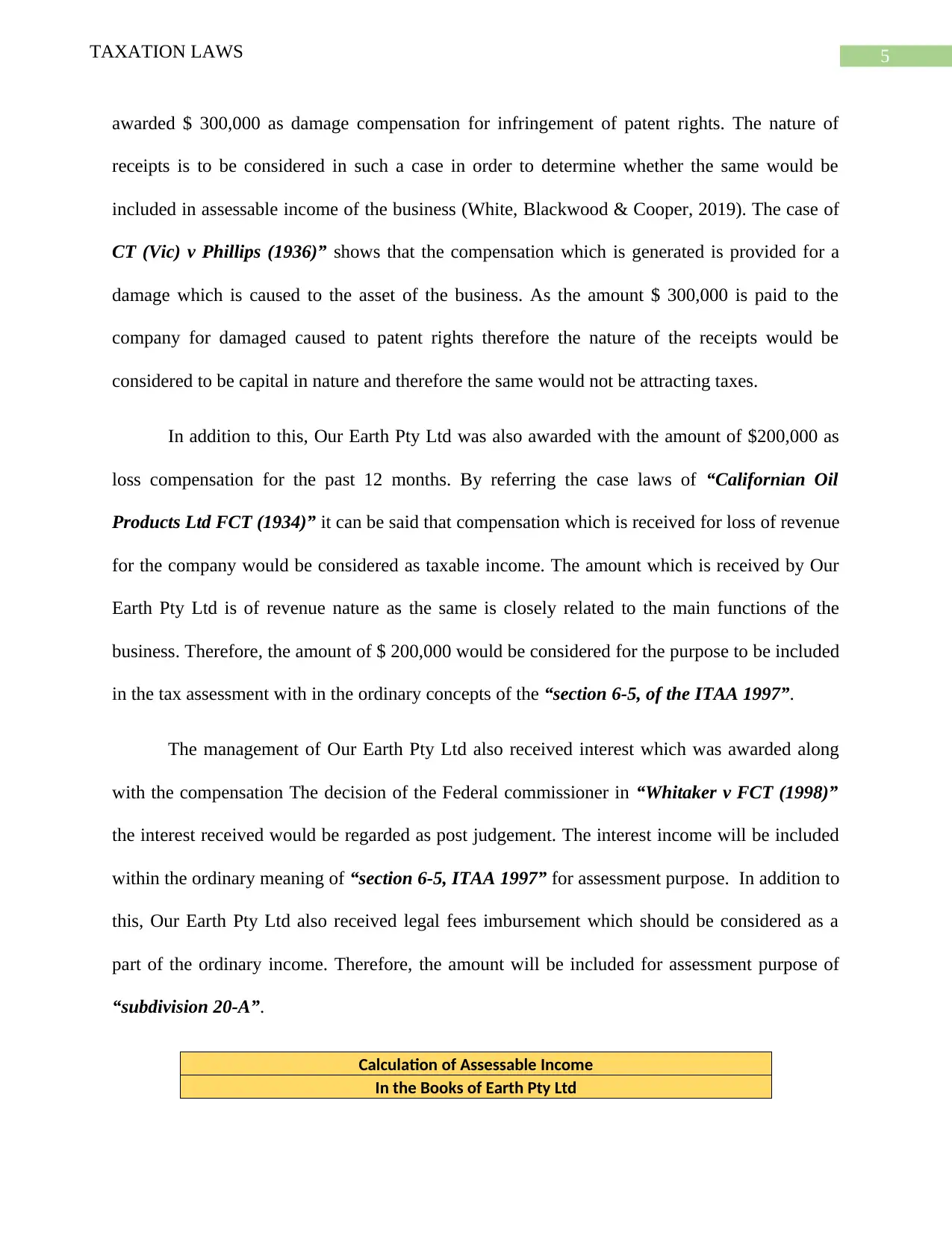

Calculation of Assessable Income

In the Books of Earth Pty Ltd

awarded $ 300,000 as damage compensation for infringement of patent rights. The nature of

receipts is to be considered in such a case in order to determine whether the same would be

included in assessable income of the business (White, Blackwood & Cooper, 2019). The case of

CT (Vic) v Phillips (1936)” shows that the compensation which is generated is provided for a

damage which is caused to the asset of the business. As the amount $ 300,000 is paid to the

company for damaged caused to patent rights therefore the nature of the receipts would be

considered to be capital in nature and therefore the same would not be attracting taxes.

In addition to this, Our Earth Pty Ltd was also awarded with the amount of $200,000 as

loss compensation for the past 12 months. By referring the case laws of “Californian Oil

Products Ltd FCT (1934)” it can be said that compensation which is received for loss of revenue

for the company would be considered as taxable income. The amount which is received by Our

Earth Pty Ltd is of revenue nature as the same is closely related to the main functions of the

business. Therefore, the amount of $ 200,000 would be considered for the purpose to be included

in the tax assessment with in the ordinary concepts of the “section 6-5, of the ITAA 1997”.

The management of Our Earth Pty Ltd also received interest which was awarded along

with the compensation The decision of the Federal commissioner in “Whitaker v FCT (1998)”

the interest received would be regarded as post judgement. The interest income will be included

within the ordinary meaning of “section 6-5, ITAA 1997” for assessment purpose. In addition to

this, Our Earth Pty Ltd also received legal fees imbursement which should be considered as a

part of the ordinary income. Therefore, the amount will be included for assessment purpose of

“subdivision 20-A”.

Calculation of Assessable Income

In the Books of Earth Pty Ltd

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAWS

For the year ended 30th June 2019

Particulars Amount ($) Amount ($)

Receipts of expected loss 200000

Receipts of Interest 15000

Reimbursement of Legal fees 40000

Total Assessable Income 255000

Conclusion

The analysis of the business of Our Earth Pty Ltd shows that amount of $ 300,000 which

was initially received by Our Earth Pty Ltd is shown to be a receipt of capital nature while the

amount which is received by Our Earth Pty Ltd for loss of revenue for the past 12 months is $

200,000. The nature of such payment is revenue is nature and therefore the sane would be

considered for the purpose of taxation. In addition to this, the interest which is paid along side

compensation would also be included in assessable income within the ordinary meaning of

section 6-5, ITAA 1997. The legal fee reimbursement would be considered under “subdivision

20-A”.

For the year ended 30th June 2019

Particulars Amount ($) Amount ($)

Receipts of expected loss 200000

Receipts of Interest 15000

Reimbursement of Legal fees 40000

Total Assessable Income 255000

Conclusion

The analysis of the business of Our Earth Pty Ltd shows that amount of $ 300,000 which

was initially received by Our Earth Pty Ltd is shown to be a receipt of capital nature while the

amount which is received by Our Earth Pty Ltd for loss of revenue for the past 12 months is $

200,000. The nature of such payment is revenue is nature and therefore the sane would be

considered for the purpose of taxation. In addition to this, the interest which is paid along side

compensation would also be included in assessable income within the ordinary meaning of

section 6-5, ITAA 1997. The legal fee reimbursement would be considered under “subdivision

20-A”.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAWS

Answer to Question 2

Issues

The case study effectively shows the provisions where Capital gains Taxes are attracted

when considering sub-division of ploys of lands which can be considered for taxation either

under “section 25 (1)” or “section 26 (a)”.

Laws

The most important ruling which is associated with Capital gain tax is that the same are

applicable on the basis of date of purchase of the asset. Capital gains are generally applied on

assets which are purchased on or after 20th September 1985. It is to be noted that the concepts of

Pre-CGT and Post CGT are used with this respect. An asset which is obtained before the the

prescribed date then the nature of the asset is pre-CGT and if the asset is purchased after the

prescribed date then the asset is considered as post CGT (Woellner et al., 2014). Then the

taxpayer needs to ascertain whether capital gain is actually arising from the sale of the asset or

not.

It is to be noted that the rules which are established regarding capital gains works

prospectively and capital gains arises when a capital gain events takes place and the date of

purchase of the asset should be after 20th September 1985. As per, “subsection 104-10 (5) of the

ITAA 1997” makes it clear that capital gain which are of pre-CGT nature are exempted from tax

regime (Sadiq, 2019).

Answer to Question 2

Issues

The case study effectively shows the provisions where Capital gains Taxes are attracted

when considering sub-division of ploys of lands which can be considered for taxation either

under “section 25 (1)” or “section 26 (a)”.

Laws

The most important ruling which is associated with Capital gain tax is that the same are

applicable on the basis of date of purchase of the asset. Capital gains are generally applied on

assets which are purchased on or after 20th September 1985. It is to be noted that the concepts of

Pre-CGT and Post CGT are used with this respect. An asset which is obtained before the the

prescribed date then the nature of the asset is pre-CGT and if the asset is purchased after the

prescribed date then the asset is considered as post CGT (Woellner et al., 2014). Then the

taxpayer needs to ascertain whether capital gain is actually arising from the sale of the asset or

not.

It is to be noted that the rules which are established regarding capital gains works

prospectively and capital gains arises when a capital gain events takes place and the date of

purchase of the asset should be after 20th September 1985. As per, “subsection 104-10 (5) of the

ITAA 1997” makes it clear that capital gain which are of pre-CGT nature are exempted from tax

regime (Sadiq, 2019).

8TAXATION LAWS

As per the rules regarding land ownership, the land owner has the right to subdivide land

in smaller plots which can then be used for selling them off for making more revenue. This

situation is a common situation of farmers who want to shift from agriculture development to

land and property development. These plots of lands are often situated at the outskirts urban

centres and believes that the property development for residential purpose. This is considered as

an an appropriate substitute for activities of farming. In such a situation, the taxpayer has the

option to choose either can sell of the land o develop property in the same which is done to

enhance the profits which is generated by the business. There are three methods for assessing the

Capital gain taxes which are listed below in details:

The sake of land can be done by simple realization of the capital assets

The assessment of income might also be including the carrying costs of the event which

is related to property development

The development may go further than simple land realisation however it might fall short

of the requirements associated to carrying on the business. In such a scheme the objective

of the taxpayer would be to maximise the profits of the business.

The assets can be effectively considered for tax if it is clear about when the asset was

originally purchased which means whether the asset is a pre-CGT asset or a post CGT asset.

According to the “section 108-5 (1), ITAA 1997” CGT asset is regarded as any form of property

or legal or equitable rights which is not the property. It is to be noted that Land is regarded as a

CGT asset and sale of land is taken as event A1. As per “section 104-10, ITAA 1997” a CGT

event A1 takes place when the taxpayers sell off the land.

As per the legislation of “section 15-15, ITAA 1997” profits or revenue which is generated

by a business by adopting proper profit schemes or for plans which is developed for assets which

As per the rules regarding land ownership, the land owner has the right to subdivide land

in smaller plots which can then be used for selling them off for making more revenue. This

situation is a common situation of farmers who want to shift from agriculture development to

land and property development. These plots of lands are often situated at the outskirts urban

centres and believes that the property development for residential purpose. This is considered as

an an appropriate substitute for activities of farming. In such a situation, the taxpayer has the

option to choose either can sell of the land o develop property in the same which is done to

enhance the profits which is generated by the business. There are three methods for assessing the

Capital gain taxes which are listed below in details:

The sake of land can be done by simple realization of the capital assets

The assessment of income might also be including the carrying costs of the event which

is related to property development

The development may go further than simple land realisation however it might fall short

of the requirements associated to carrying on the business. In such a scheme the objective

of the taxpayer would be to maximise the profits of the business.

The assets can be effectively considered for tax if it is clear about when the asset was

originally purchased which means whether the asset is a pre-CGT asset or a post CGT asset.

According to the “section 108-5 (1), ITAA 1997” CGT asset is regarded as any form of property

or legal or equitable rights which is not the property. It is to be noted that Land is regarded as a

CGT asset and sale of land is taken as event A1. As per “section 104-10, ITAA 1997” a CGT

event A1 takes place when the taxpayers sell off the land.

As per the legislation of “section 15-15, ITAA 1997” profits or revenue which is generated

by a business by adopting proper profit schemes or for plans which is developed for assets which

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAWS

is purchased before date would be considered as Pre-CGT assets and the same would be held

taxable as per the rulings. It is also to be noted that any improvement which is made to a capital

asset would also be considered for the purpose of estimating CGT. In case the improvement

which is made by the taxpayer is significant than the costs of the improvements made would be

added to the cost base of the asset for computing the CGT applicable to the taxpayer (Stiglitz,

2014).

The ve5rdict which was provided in the case of “Scottish Australian Mining Co Ltd v FC

of T (1950)” showed that the taxpayer generated significant amount of profits during the period

by selling off sub-divided lands (Bankman et al., 2018). Therefore, the verdict which was

provided was simple and it stated that the income which is derived by the taxpayer would be held

assessable and liable for tax (Yuan, 2016). As per the judgement of commissioner of taxation,

the profits generated by the taxpayer would be treated as gains from business land development

activities which is covered under “section 25 (1), ITAA 1936” or profits which were made from

revenue making activities under the provision of “section 26 (a)”.

The income or profits which is made by a taxpayer when he disposes off his land which

can be in ordinary course of business or not would be considered as part of assessable income

and therefore would be subjected to tax provided that the main objective of the taxpayer was to

generate profits from the sale of land in the first place.

Application

Sam who is the taxpayer in the case is shown to have purchased 80 acres of land the first

time for engaging in the business of agriculture and then in order to expand the operations of the

business purchased a plot of land of 20 acres (Gale & Brown, 2013). The land will be used for

is purchased before date would be considered as Pre-CGT assets and the same would be held

taxable as per the rulings. It is also to be noted that any improvement which is made to a capital

asset would also be considered for the purpose of estimating CGT. In case the improvement

which is made by the taxpayer is significant than the costs of the improvements made would be

added to the cost base of the asset for computing the CGT applicable to the taxpayer (Stiglitz,

2014).

The ve5rdict which was provided in the case of “Scottish Australian Mining Co Ltd v FC

of T (1950)” showed that the taxpayer generated significant amount of profits during the period

by selling off sub-divided lands (Bankman et al., 2018). Therefore, the verdict which was

provided was simple and it stated that the income which is derived by the taxpayer would be held

assessable and liable for tax (Yuan, 2016). As per the judgement of commissioner of taxation,

the profits generated by the taxpayer would be treated as gains from business land development

activities which is covered under “section 25 (1), ITAA 1936” or profits which were made from

revenue making activities under the provision of “section 26 (a)”.

The income or profits which is made by a taxpayer when he disposes off his land which

can be in ordinary course of business or not would be considered as part of assessable income

and therefore would be subjected to tax provided that the main objective of the taxpayer was to

generate profits from the sale of land in the first place.

Application

Sam who is the taxpayer in the case is shown to have purchased 80 acres of land the first

time for engaging in the business of agriculture and then in order to expand the operations of the

business purchased a plot of land of 20 acres (Gale & Brown, 2013). The land will be used for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAWS

the purpose of conducting agricultural practices in the area. The case further shows that Sam

become disinterested in agriculture after a certain interval of time due to poor conditions and

thereby approached a property agent. Sam therefore decided to sell off the land on the advice of

the agent. The advice which was given by the property agent was to sub-divide the land which

would help Sam to get the best deals and also increase his profits.

In order to assess the applicability of CGT, the date of purchase for the asset is to be

considered which would decide whether the asset is pre-CGT or Post CGT. The 80 acres of land

which Sam bought was before 1984. Therefore, 80 acres of land which Sam has, would be

treated as Pre-CGT if the same is disposed and CGT provisions becomes applicable on the same.

The capital gains which is made from sale of 80 acres of land would be exempted (Yinger,

Bloom & Boersch-Supan, 2016).

The 20 acres farm land was bought by Sam for expanding operation on February 1995.

This is clear that the sale of this land would be treated as Post CGT because it meets the date

criteria (Zucman, 2014). The process of sub-division started in 2017 and the land was finally

sold out in 2018. Therefore, capital gains made from the sale of 20 acres of land will be

subjected to capital gains tax as the post-CGT asset.

The case shows that the plots of sub-divided land was sold off by Sam for the purpose of

enhancing the profits of the taxpayer from land development and sales of the same. By referring

to the “Taxation Determination TD 97/3” the income generated from disposal of land should be

considered as income by Sam and hence should be taxable under “subsection 25 (1), ITAA

1936”. It is to be noted that the purpose of Sam was not to derive profits but the same become

necessary at a later stage (Evans, Minas & Lim, 2015).

the purpose of conducting agricultural practices in the area. The case further shows that Sam

become disinterested in agriculture after a certain interval of time due to poor conditions and

thereby approached a property agent. Sam therefore decided to sell off the land on the advice of

the agent. The advice which was given by the property agent was to sub-divide the land which

would help Sam to get the best deals and also increase his profits.

In order to assess the applicability of CGT, the date of purchase for the asset is to be

considered which would decide whether the asset is pre-CGT or Post CGT. The 80 acres of land

which Sam bought was before 1984. Therefore, 80 acres of land which Sam has, would be

treated as Pre-CGT if the same is disposed and CGT provisions becomes applicable on the same.

The capital gains which is made from sale of 80 acres of land would be exempted (Yinger,

Bloom & Boersch-Supan, 2016).

The 20 acres farm land was bought by Sam for expanding operation on February 1995.

This is clear that the sale of this land would be treated as Post CGT because it meets the date

criteria (Zucman, 2014). The process of sub-division started in 2017 and the land was finally

sold out in 2018. Therefore, capital gains made from the sale of 20 acres of land will be

subjected to capital gains tax as the post-CGT asset.

The case shows that the plots of sub-divided land was sold off by Sam for the purpose of

enhancing the profits of the taxpayer from land development and sales of the same. By referring

to the “Taxation Determination TD 97/3” the income generated from disposal of land should be

considered as income by Sam and hence should be taxable under “subsection 25 (1), ITAA

1936”. It is to be noted that the purpose of Sam was not to derive profits but the same become

necessary at a later stage (Evans, Minas & Lim, 2015).

11TAXATION LAWS

As per the decision of federal court in “Scottish Australian Mining Co Ltd v FC of T

(1950)” considerable income was generated by Sam from sale of subdivided plots of land. This

is reason that the Sam would be considered as assessable under the purview of CGT either as

gains made from performing activities of business of land development under the “section 25

(1), ITAA 1936” or profits which were made from revenue generating activities under legislative

provision of “section 26 (a)”.

An alternative case law which can be suggested is of “Federal Commissioner of Taxation v

Whitfords Beach Pty Ltd (1982)” where decision was given that the taxpayer was held

assessable for taxation for sale of plots of land (Askari, Cummings & Glover, 2013). The profits

which is made by the taxpayer would for activities or performing business of land development

under the “section 25 (1), ITAA 1936” or profits which were made from revenue generating

activities under legislative provision of “section 26 (a)”.

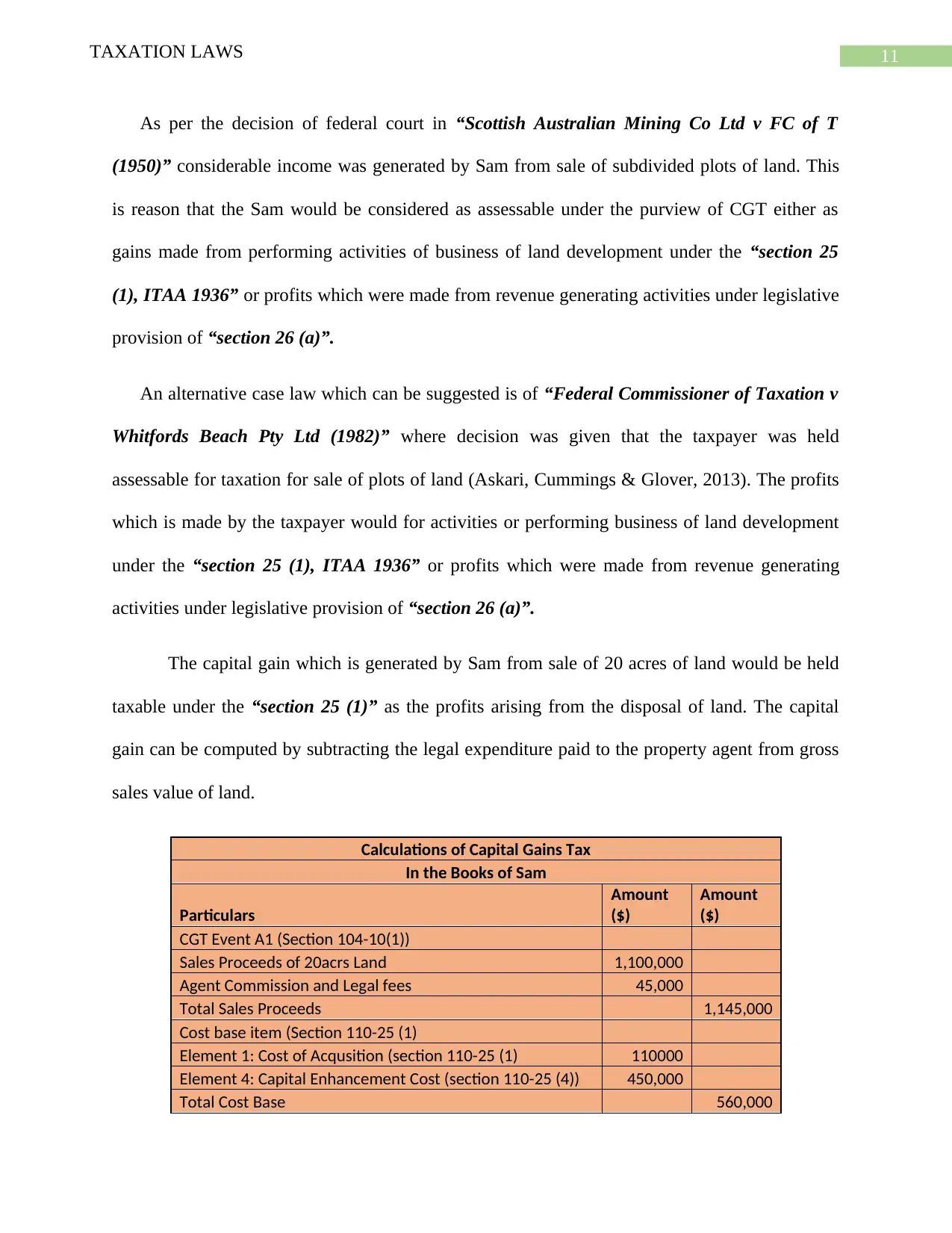

The capital gain which is generated by Sam from sale of 20 acres of land would be held

taxable under the “section 25 (1)” as the profits arising from the disposal of land. The capital

gain can be computed by subtracting the legal expenditure paid to the property agent from gross

sales value of land.

Calculations of Capital Gains Tax

In the Books of Sam

Particulars

Amount

($)

Amount

($)

CGT Event A1 (Section 104-10(1))

Sales Proceeds of 20acrs Land 1,100,000

Agent Commission and Legal fees 45,000

Total Sales Proceeds 1,145,000

Cost base item (Section 110-25 (1)

Element 1: Cost of Acqusition (section 110-25 (1) 110000

Element 4: Capital Enhancement Cost (section 110-25 (4)) 450,000

Total Cost Base 560,000

As per the decision of federal court in “Scottish Australian Mining Co Ltd v FC of T

(1950)” considerable income was generated by Sam from sale of subdivided plots of land. This

is reason that the Sam would be considered as assessable under the purview of CGT either as

gains made from performing activities of business of land development under the “section 25

(1), ITAA 1936” or profits which were made from revenue generating activities under legislative

provision of “section 26 (a)”.

An alternative case law which can be suggested is of “Federal Commissioner of Taxation v

Whitfords Beach Pty Ltd (1982)” where decision was given that the taxpayer was held

assessable for taxation for sale of plots of land (Askari, Cummings & Glover, 2013). The profits

which is made by the taxpayer would for activities or performing business of land development

under the “section 25 (1), ITAA 1936” or profits which were made from revenue generating

activities under legislative provision of “section 26 (a)”.

The capital gain which is generated by Sam from sale of 20 acres of land would be held

taxable under the “section 25 (1)” as the profits arising from the disposal of land. The capital

gain can be computed by subtracting the legal expenditure paid to the property agent from gross

sales value of land.

Calculations of Capital Gains Tax

In the Books of Sam

Particulars

Amount

($)

Amount

($)

CGT Event A1 (Section 104-10(1))

Sales Proceeds of 20acrs Land 1,100,000

Agent Commission and Legal fees 45,000

Total Sales Proceeds 1,145,000

Cost base item (Section 110-25 (1)

Element 1: Cost of Acqusition (section 110-25 (1) 110000

Element 4: Capital Enhancement Cost (section 110-25 (4)) 450,000

Total Cost Base 560,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.