Taxation Assignment: Capital Gains, Loans, and Legal Plans

VerifiedAdded on 2020/04/01

|10

|3452

|34

Homework Assignment

AI Summary

This assignment solution delves into various aspects of taxation, providing a comprehensive analysis of capital gains and losses, loan taxation, and legal tax planning. The solution begins with a detailed calculation of net capital gains or losses for the year, considering different asset types and their acquisition costs. It then analyzes a loan scenario involving Brian, calculating the tax implications of offering loans to employees with below-market interest rates. The assignment also examines a partnership loan between Jack and Jill, determining how losses are allocated and the tax implications for each partner. Finally, it explores legal tax planning strategies, referencing the IRC v Duke of Westminster case, and outlining principles for minimizing tax liabilities. The document provides a clear and concise overview of complex taxation concepts.

1

Taxation

<Student ID>

<Student Name>

<University Name>

Taxation

<Student ID>

<Student Name>

<University Name>

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Contents

1. Overall calculation of the net capital loss or gain for this year...................................................3

2. Loan to Brain...............................................................................................................................5

3. About Jack and Jill Loan.............................................................................................................6

4. Legal Plan....................................................................................................................................7

5. Land Problem of Bill...................................................................................................................8

References........................................................................................................................................9

Contents

1. Overall calculation of the net capital loss or gain for this year...................................................3

2. Loan to Brain...............................................................................................................................5

3. About Jack and Jill Loan.............................................................................................................6

4. Legal Plan....................................................................................................................................7

5. Land Problem of Bill...................................................................................................................8

References........................................................................................................................................9

3

The term taxation means the compulsory money that is collected by the levying authorities,

mainly by the government. The term is applicable to the involuntary levies, from the income to

the other gains in the capital to the estate taxes. The taxation is quite different from the other

forms of the payment such as the market exchange and other services. The government collects

the taxation through explicit and implicit manner or threat of force. The taxation is different from

the protection racket and the extortion because the institute on which is imposed is a government,

not private (Auerbach & Hassett, 2015). The tax system varies from place to place, countries to

countries. In the recent situations, the taxation occurs both in the physical asset like the property,

events and the sale transactions. The formulation of the tax is one the vital thing and issues in the

political circles.

The taxation is the principle where the government is raising the revenue. Without the taxation,

the government wasn't able to circulate the laws properly and face problems in the export and

import of the products. So the taxation is important to deliver the products or the public goods

and services to the various communities (Basu, et al., 2014). There are various ways government

can raise the revenue like; they can charge the fees for the rendering services and also for

granting the license impose fines amount for the breaches of the laws and generate new laws and

rules for various assets and investments (Besley & Persson, 2013).

Taxes are the special systems that are imposed on the communities. The taxation laws are

described as the body of the laws that helps to govern the liabilities of a person and the

organization to pay the tax. It covers the entire rule and establishes the tax base and incidence of

the tax. Australia has the vast body of the taxation law (Bick & Fuchs-Schündeln, 2017). The

primary source of the country is to find the thousands of pages of the tax legislation that are

enacted by the commonwealth, the territory parliaments, and the state.

1. Overall calculation of the net capital loss or gain for this year

The Australia's taxation laws are operated by the commonwealth constitution and the

international treaties that include the Double tax agreements (DTAs) entered into the foreign

countries. The taxation is extremely important and useful for various study and challenges of the

society because of the voluminous nature as well as due to the technical complexities. From the

The term taxation means the compulsory money that is collected by the levying authorities,

mainly by the government. The term is applicable to the involuntary levies, from the income to

the other gains in the capital to the estate taxes. The taxation is quite different from the other

forms of the payment such as the market exchange and other services. The government collects

the taxation through explicit and implicit manner or threat of force. The taxation is different from

the protection racket and the extortion because the institute on which is imposed is a government,

not private (Auerbach & Hassett, 2015). The tax system varies from place to place, countries to

countries. In the recent situations, the taxation occurs both in the physical asset like the property,

events and the sale transactions. The formulation of the tax is one the vital thing and issues in the

political circles.

The taxation is the principle where the government is raising the revenue. Without the taxation,

the government wasn't able to circulate the laws properly and face problems in the export and

import of the products. So the taxation is important to deliver the products or the public goods

and services to the various communities (Basu, et al., 2014). There are various ways government

can raise the revenue like; they can charge the fees for the rendering services and also for

granting the license impose fines amount for the breaches of the laws and generate new laws and

rules for various assets and investments (Besley & Persson, 2013).

Taxes are the special systems that are imposed on the communities. The taxation laws are

described as the body of the laws that helps to govern the liabilities of a person and the

organization to pay the tax. It covers the entire rule and establishes the tax base and incidence of

the tax. Australia has the vast body of the taxation law (Bick & Fuchs-Schündeln, 2017). The

primary source of the country is to find the thousands of pages of the tax legislation that are

enacted by the commonwealth, the territory parliaments, and the state.

1. Overall calculation of the net capital loss or gain for this year

The Australia's taxation laws are operated by the commonwealth constitution and the

international treaties that include the Double tax agreements (DTAs) entered into the foreign

countries. The taxation is extremely important and useful for various study and challenges of the

society because of the voluminous nature as well as due to the technical complexities. From the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

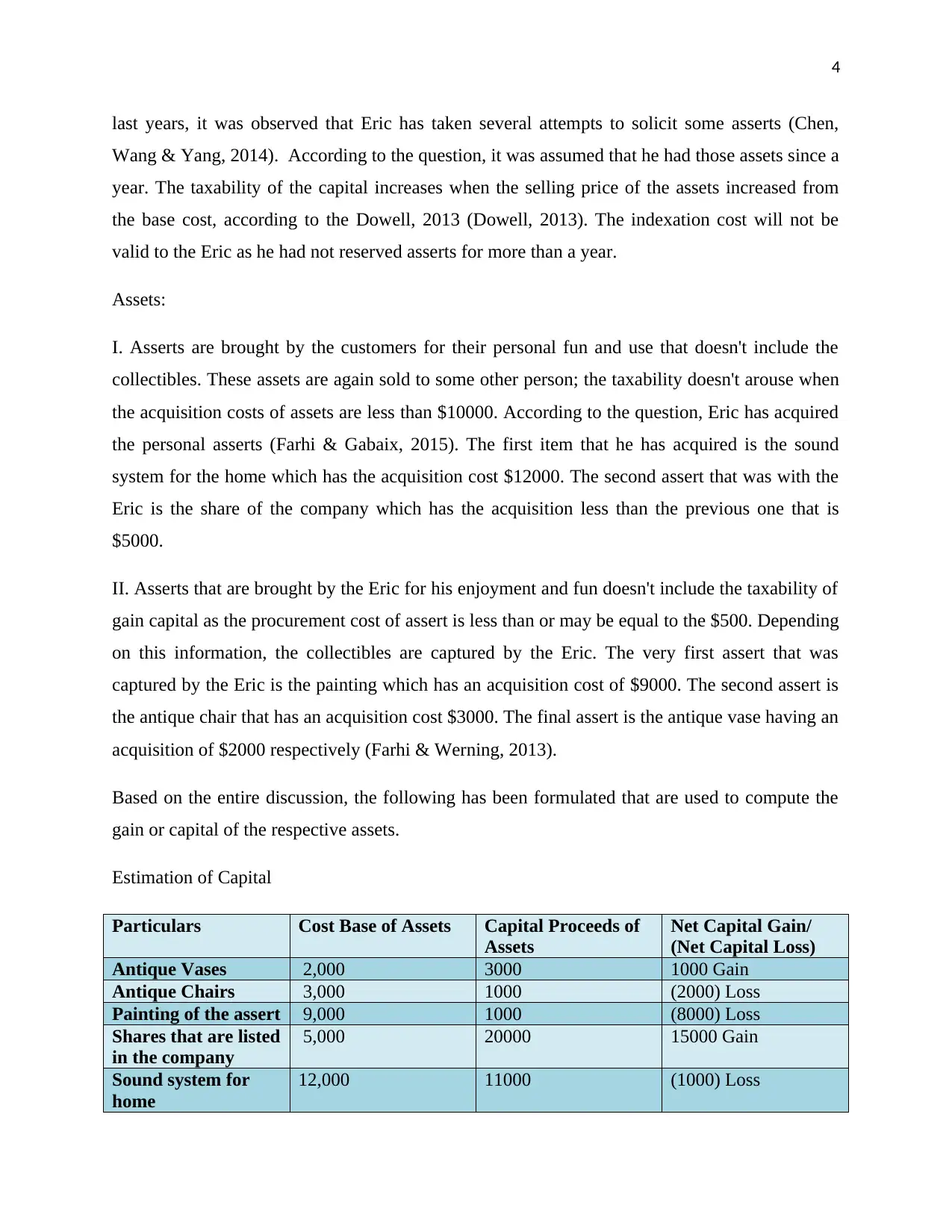

last years, it was observed that Eric has taken several attempts to solicit some asserts (Chen,

Wang & Yang, 2014). According to the question, it was assumed that he had those assets since a

year. The taxability of the capital increases when the selling price of the assets increased from

the base cost, according to the Dowell, 2013 (Dowell, 2013). The indexation cost will not be

valid to the Eric as he had not reserved asserts for more than a year.

Assets:

I. Asserts are brought by the customers for their personal fun and use that doesn't include the

collectibles. These assets are again sold to some other person; the taxability doesn't arouse when

the acquisition costs of assets are less than $10000. According to the question, Eric has acquired

the personal asserts (Farhi & Gabaix, 2015). The first item that he has acquired is the sound

system for the home which has the acquisition cost $12000. The second assert that was with the

Eric is the share of the company which has the acquisition less than the previous one that is

$5000.

II. Asserts that are brought by the Eric for his enjoyment and fun doesn't include the taxability of

gain capital as the procurement cost of assert is less than or may be equal to the $500. Depending

on this information, the collectibles are captured by the Eric. The very first assert that was

captured by the Eric is the painting which has an acquisition cost of $9000. The second assert is

the antique chair that has an acquisition cost $3000. The final assert is the antique vase having an

acquisition of $2000 respectively (Farhi & Werning, 2013).

Based on the entire discussion, the following has been formulated that are used to compute the

gain or capital of the respective assets.

Estimation of Capital

Particulars Cost Base of Assets Capital Proceeds of

Assets

Net Capital Gain/

(Net Capital Loss)

Antique Vases 2,000 3000 1000 Gain

Antique Chairs 3,000 1000 (2000) Loss

Painting of the assert 9,000 1000 (8000) Loss

Shares that are listed

in the company

5,000 20000 15000 Gain

Sound system for

home

12,000 11000 (1000) Loss

last years, it was observed that Eric has taken several attempts to solicit some asserts (Chen,

Wang & Yang, 2014). According to the question, it was assumed that he had those assets since a

year. The taxability of the capital increases when the selling price of the assets increased from

the base cost, according to the Dowell, 2013 (Dowell, 2013). The indexation cost will not be

valid to the Eric as he had not reserved asserts for more than a year.

Assets:

I. Asserts are brought by the customers for their personal fun and use that doesn't include the

collectibles. These assets are again sold to some other person; the taxability doesn't arouse when

the acquisition costs of assets are less than $10000. According to the question, Eric has acquired

the personal asserts (Farhi & Gabaix, 2015). The first item that he has acquired is the sound

system for the home which has the acquisition cost $12000. The second assert that was with the

Eric is the share of the company which has the acquisition less than the previous one that is

$5000.

II. Asserts that are brought by the Eric for his enjoyment and fun doesn't include the taxability of

gain capital as the procurement cost of assert is less than or may be equal to the $500. Depending

on this information, the collectibles are captured by the Eric. The very first assert that was

captured by the Eric is the painting which has an acquisition cost of $9000. The second assert is

the antique chair that has an acquisition cost $3000. The final assert is the antique vase having an

acquisition of $2000 respectively (Farhi & Werning, 2013).

Based on the entire discussion, the following has been formulated that are used to compute the

gain or capital of the respective assets.

Estimation of Capital

Particulars Cost Base of Assets Capital Proceeds of

Assets

Net Capital Gain/

(Net Capital Loss)

Antique Vases 2,000 3000 1000 Gain

Antique Chairs 3,000 1000 (2000) Loss

Painting of the assert 9,000 1000 (8000) Loss

Shares that are listed

in the company

5,000 20000 15000 Gain

Sound system for

home

12,000 11000 (1000) Loss

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

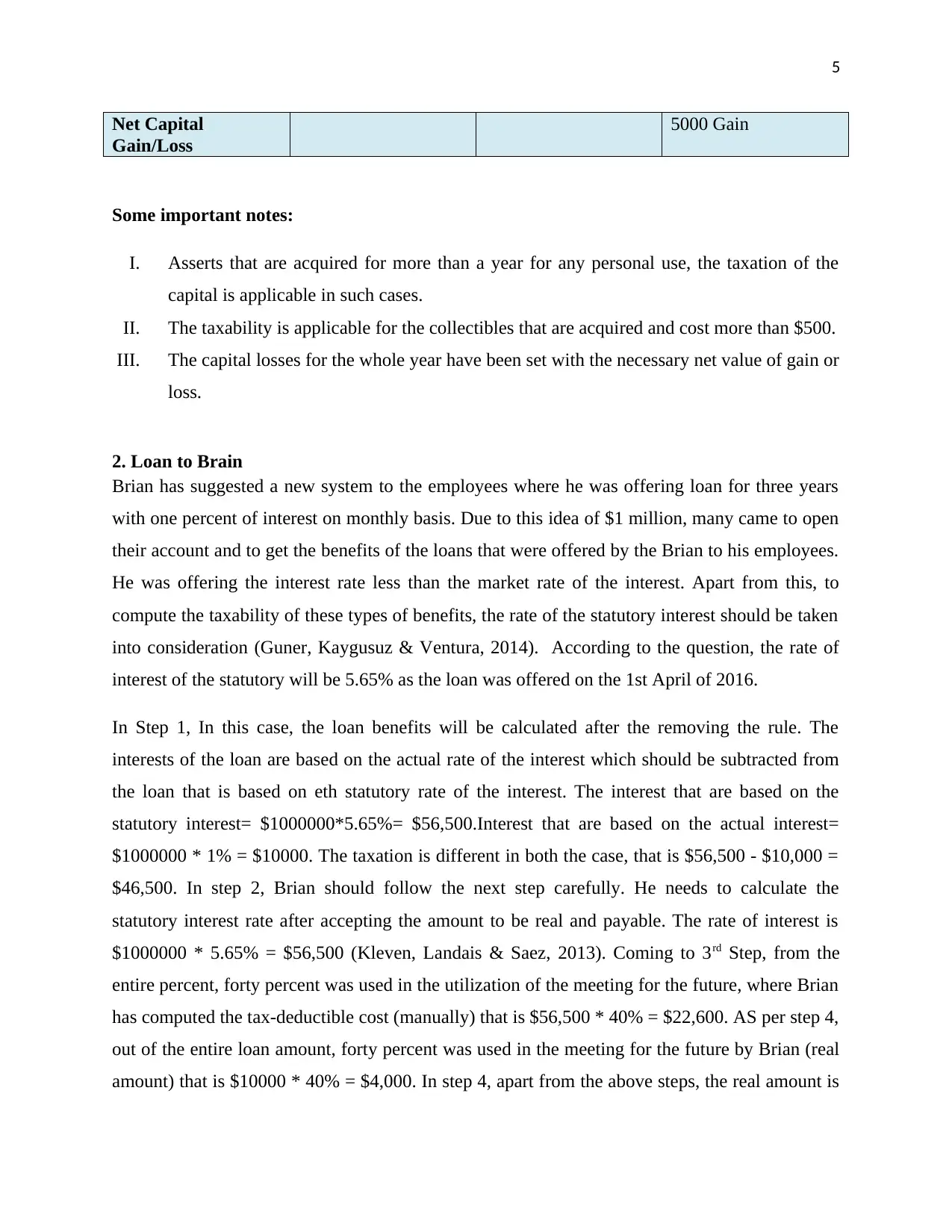

Net Capital

Gain/Loss

5000 Gain

Some important notes:

I. Asserts that are acquired for more than a year for any personal use, the taxation of the

capital is applicable in such cases.

II. The taxability is applicable for the collectibles that are acquired and cost more than $500.

III. The capital losses for the whole year have been set with the necessary net value of gain or

loss.

2. Loan to Brain

Brian has suggested a new system to the employees where he was offering loan for three years

with one percent of interest on monthly basis. Due to this idea of $1 million, many came to open

their account and to get the benefits of the loans that were offered by the Brian to his employees.

He was offering the interest rate less than the market rate of the interest. Apart from this, to

compute the taxability of these types of benefits, the rate of the statutory interest should be taken

into consideration (Guner, Kaygusuz & Ventura, 2014). According to the question, the rate of

interest of the statutory will be 5.65% as the loan was offered on the 1st April of 2016.

In Step 1, In this case, the loan benefits will be calculated after the removing the rule. The

interests of the loan are based on the actual rate of the interest which should be subtracted from

the loan that is based on eth statutory rate of the interest. The interest that are based on the

statutory interest= $1000000*5.65%= $56,500.Interest that are based on the actual interest=

$1000000 * 1% = $10000. The taxation is different in both the case, that is $56,500 - $10,000 =

$46,500. In step 2, Brian should follow the next step carefully. He needs to calculate the

statutory interest rate after accepting the amount to be real and payable. The rate of interest is

$1000000 * 5.65% = $56,500 (Kleven, Landais & Saez, 2013). Coming to 3rd Step, from the

entire percent, forty percent was used in the utilization of the meeting for the future, where Brian

has computed the tax-deductible cost (manually) that is $56,500 * 40% = $22,600. AS per step 4,

out of the entire loan amount, forty percent was used in the meeting for the future by Brian (real

amount) that is $10000 * 40% = $4,000. In step 4, apart from the above steps, the real amount is

Net Capital

Gain/Loss

5000 Gain

Some important notes:

I. Asserts that are acquired for more than a year for any personal use, the taxation of the

capital is applicable in such cases.

II. The taxability is applicable for the collectibles that are acquired and cost more than $500.

III. The capital losses for the whole year have been set with the necessary net value of gain or

loss.

2. Loan to Brain

Brian has suggested a new system to the employees where he was offering loan for three years

with one percent of interest on monthly basis. Due to this idea of $1 million, many came to open

their account and to get the benefits of the loans that were offered by the Brian to his employees.

He was offering the interest rate less than the market rate of the interest. Apart from this, to

compute the taxability of these types of benefits, the rate of the statutory interest should be taken

into consideration (Guner, Kaygusuz & Ventura, 2014). According to the question, the rate of

interest of the statutory will be 5.65% as the loan was offered on the 1st April of 2016.

In Step 1, In this case, the loan benefits will be calculated after the removing the rule. The

interests of the loan are based on the actual rate of the interest which should be subtracted from

the loan that is based on eth statutory rate of the interest. The interest that are based on the

statutory interest= $1000000*5.65%= $56,500.Interest that are based on the actual interest=

$1000000 * 1% = $10000. The taxation is different in both the case, that is $56,500 - $10,000 =

$46,500. In step 2, Brian should follow the next step carefully. He needs to calculate the

statutory interest rate after accepting the amount to be real and payable. The rate of interest is

$1000000 * 5.65% = $56,500 (Kleven, Landais & Saez, 2013). Coming to 3rd Step, from the

entire percent, forty percent was used in the utilization of the meeting for the future, where Brian

has computed the tax-deductible cost (manually) that is $56,500 * 40% = $22,600. AS per step 4,

out of the entire loan amount, forty percent was used in the meeting for the future by Brian (real

amount) that is $10000 * 40% = $4,000. In step 4, apart from the above steps, the real amount is

6

now calculated in this step from the manual figure in order to arrive at the conclusion. Therefore,

$22,600 - $4,000 = $18,600. In Final step, the final amount should be calculated by deducting

the amount from the step 1 after determining the amount till step 5.Therefore, $46,500 - $18,600

= $27,900 (McDaniel, Repetti & Ring, 2014).

However, if there is any system of repayment of these loans before the termination period, then

instead of the usual repayment system, the deemed period of the loan will be assumed from

where the interest has been started or become payable, respectively (Mellon, 2016). Apart from

all these, the obligation is on the part of the repay mode of the interests, then in such cases, the

computation should be done in a similar manner like the actual interest rate which is considered

as zero (Miller & Oats, 2016).

3. About Jack and Jill Loan

Jack and Jill both have agreed to borrow the money for their rent house where the jack was

capable of receiving the 10% of the profit, whereas the Jill was supposed to get 90% of the profit

from their entire property. As per the written agreement in between the jack and Jill, in case of

any loss in the property, jack has to bear the full loss that is 100%. In the last year, they have

sustained a loss of $1000 which was completely paid by the jack without any obligation of the

loss on the Jill (Piketty & Saez, 2013). The loss created a set off on the other forms of the

incomes of the Jack which will determine the net profit or loss for the entire year. Apart from

this option, he has one more option that is to carry forward the entire loss for the following year.

Whenever Jack is facing is any type of loss, and then he has right to borne the total amount and

can carry forward the same amount in the upcoming years in order to maintain the net income or

loss of amount (Tanzi, 2014). In the second case, if there is any gain then the amount will be

divided between the jack and Jill in the ratio 10:90. In these cases, jack has the full right to set

off the entire loss of $1000 which has come after selling the property. Therefore, from the entire

discussion, it was cleared that jack was able to bear the losses that have occurred in the previous

year and he is gaining the amount in the present year after selling the property (Rothschild &

Scheuer, 2016). It was concluded that, if Jack didn't have any gain in the recent year then he has

to carry the entire loss without any involvement of the Jill. So, this process has helped the Jill to

now calculated in this step from the manual figure in order to arrive at the conclusion. Therefore,

$22,600 - $4,000 = $18,600. In Final step, the final amount should be calculated by deducting

the amount from the step 1 after determining the amount till step 5.Therefore, $46,500 - $18,600

= $27,900 (McDaniel, Repetti & Ring, 2014).

However, if there is any system of repayment of these loans before the termination period, then

instead of the usual repayment system, the deemed period of the loan will be assumed from

where the interest has been started or become payable, respectively (Mellon, 2016). Apart from

all these, the obligation is on the part of the repay mode of the interests, then in such cases, the

computation should be done in a similar manner like the actual interest rate which is considered

as zero (Miller & Oats, 2016).

3. About Jack and Jill Loan

Jack and Jill both have agreed to borrow the money for their rent house where the jack was

capable of receiving the 10% of the profit, whereas the Jill was supposed to get 90% of the profit

from their entire property. As per the written agreement in between the jack and Jill, in case of

any loss in the property, jack has to bear the full loss that is 100%. In the last year, they have

sustained a loss of $1000 which was completely paid by the jack without any obligation of the

loss on the Jill (Piketty & Saez, 2013). The loss created a set off on the other forms of the

incomes of the Jack which will determine the net profit or loss for the entire year. Apart from

this option, he has one more option that is to carry forward the entire loss for the following year.

Whenever Jack is facing is any type of loss, and then he has right to borne the total amount and

can carry forward the same amount in the upcoming years in order to maintain the net income or

loss of amount (Tanzi, 2014). In the second case, if there is any gain then the amount will be

divided between the jack and Jill in the ratio 10:90. In these cases, jack has the full right to set

off the entire loss of $1000 which has come after selling the property. Therefore, from the entire

discussion, it was cleared that jack was able to bear the losses that have occurred in the previous

year and he is gaining the amount in the present year after selling the property (Rothschild &

Scheuer, 2016). It was concluded that, if Jack didn't have any gain in the recent year then he has

to carry the entire loss without any involvement of the Jill. So, this process has helped the Jill to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

stay away from the taxation affects where the jack was only supposed to bear the loss of the

books (Tanzi, 2014).

4. Legal Plan

According to the law, every individual has the power to the legal plans and strategies that help

them to decrease the total income at the last of the every year, according to the case study of the

IRC v Duke of Westminster [1936] AC 1 (Miller & Oats, 2016). After going through the case, it

was cleared that every individual has the right to utilize the right and benefits that are attached to

the total income. In familiar terms, the rights are only valid when they are used in a fair manner

and correct methods are applied to it which is supposed to reduce the cost of the income and the

tax values at the end of the year.

The following principles are classified from the above case study:

Principles 1:

The complete authority has been given to the individual to use the strategic methods and plans to

reduce the total income by managing their own accounts (Chen, Wang & Yang, 2014).

Principles 2:

No extra taxes will be implemented if the process will be followed in a relevant manner without

any illegal means and methods.

Principles 3:

When the individual follows the fairway to reduce their amount and tax rate, then they will not

be forced to pay the extra tax rate in the near future.

The point number is valid until any new law is implemented in the country. The ideology is

different from each other and varies from the previous one. The main aim of these rules has huge

significance in the current situation in various manners (Kleven, Landais & Saez, 2013).

The rules are quite true and relevant for the surrounding as they are capable of preventing the

organization from extra accounts an advantage. Apart from this, the rule also offers the legal

power to the business authorities in a simple manner. For an example, when a business is facing

stay away from the taxation affects where the jack was only supposed to bear the loss of the

books (Tanzi, 2014).

4. Legal Plan

According to the law, every individual has the power to the legal plans and strategies that help

them to decrease the total income at the last of the every year, according to the case study of the

IRC v Duke of Westminster [1936] AC 1 (Miller & Oats, 2016). After going through the case, it

was cleared that every individual has the right to utilize the right and benefits that are attached to

the total income. In familiar terms, the rights are only valid when they are used in a fair manner

and correct methods are applied to it which is supposed to reduce the cost of the income and the

tax values at the end of the year.

The following principles are classified from the above case study:

Principles 1:

The complete authority has been given to the individual to use the strategic methods and plans to

reduce the total income by managing their own accounts (Chen, Wang & Yang, 2014).

Principles 2:

No extra taxes will be implemented if the process will be followed in a relevant manner without

any illegal means and methods.

Principles 3:

When the individual follows the fairway to reduce their amount and tax rate, then they will not

be forced to pay the extra tax rate in the near future.

The point number is valid until any new law is implemented in the country. The ideology is

different from each other and varies from the previous one. The main aim of these rules has huge

significance in the current situation in various manners (Kleven, Landais & Saez, 2013).

The rules are quite true and relevant for the surrounding as they are capable of preventing the

organization from extra accounts an advantage. Apart from this, the rule also offers the legal

power to the business authorities in a simple manner. For an example, when a business is facing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

huge losses in a particular year that address its obligations, then in such cases, they have the

chance to change the balance sheets and the amount and can prepare the new one with the fixed

assets and their values (Bick & Fuchs-Schündeln, 2017). In some cases, the business didn't

provide the relevant documents but still, they can proceed further. But certain restrictions are

applicable to them. They should not follow any illegal path to achieve so. Combining the entire

discussion, it is cleared that the organization has to operate in a fair manner to achieve the target

and should follow the laws and its procedure.

5. Land Problem of Bill

In this scenario, Bill has a piece of land which he has thought of using it for the grazing purpose

of the sheep. In order to fulfill his desire, the entire land needs to be cleared as trees were present

over there. Therefore, he has hired a logging company to clear the land. The company has

charged him $1000 per every 100 meters of the timber. But here the main question arises, that is

whether the tax is applicable on the logging company for the entire amount (Farhi & Gabaix,

2015). According to the given situation, there are no facts on the receipts that are received from

the firm which is considered as the revenue object or may not be considered as an object. The

highest degree of uncertainty proves that the rules which are related to the capital gains are not

applicable to Bill's recent situation (Farhi & Gabaix, 2015).

When the Bill is investing a total amount of the $50000 to the logging company for the removal

of the trees to get the timbers, then the same amount completely comes to Bill's hand as a capital

receipt. This happens due to reason where the total amount is considered as the lump sum and

there is no other recurring receipt for it. Again, the transaction that has occurred provides the

right to the particular authority to remove the trees from the respective lands. So, after the entire

scenario, the case was considered as the lump sum receipt as well as the total capital receipt.

Hence, the taxation of the capital is in the hands of the Bill (Bick & Fuchs-Schündeln, 2017).

So in the above two scenarios, the value of the invested money has a huge significance on the

laws of the taxation. The two cases are completely different. In the very first case, the receipt is

in the hands of the Bill and is recurring whereas in the second case, the receipt is in the hands of

the bill but that is not recurring that provides the right to receive the payments from the logging

of the trees in the further situations. He will get the same receipt in a bigger one and that will be

huge losses in a particular year that address its obligations, then in such cases, they have the

chance to change the balance sheets and the amount and can prepare the new one with the fixed

assets and their values (Bick & Fuchs-Schündeln, 2017). In some cases, the business didn't

provide the relevant documents but still, they can proceed further. But certain restrictions are

applicable to them. They should not follow any illegal path to achieve so. Combining the entire

discussion, it is cleared that the organization has to operate in a fair manner to achieve the target

and should follow the laws and its procedure.

5. Land Problem of Bill

In this scenario, Bill has a piece of land which he has thought of using it for the grazing purpose

of the sheep. In order to fulfill his desire, the entire land needs to be cleared as trees were present

over there. Therefore, he has hired a logging company to clear the land. The company has

charged him $1000 per every 100 meters of the timber. But here the main question arises, that is

whether the tax is applicable on the logging company for the entire amount (Farhi & Gabaix,

2015). According to the given situation, there are no facts on the receipts that are received from

the firm which is considered as the revenue object or may not be considered as an object. The

highest degree of uncertainty proves that the rules which are related to the capital gains are not

applicable to Bill's recent situation (Farhi & Gabaix, 2015).

When the Bill is investing a total amount of the $50000 to the logging company for the removal

of the trees to get the timbers, then the same amount completely comes to Bill's hand as a capital

receipt. This happens due to reason where the total amount is considered as the lump sum and

there is no other recurring receipt for it. Again, the transaction that has occurred provides the

right to the particular authority to remove the trees from the respective lands. So, after the entire

scenario, the case was considered as the lump sum receipt as well as the total capital receipt.

Hence, the taxation of the capital is in the hands of the Bill (Bick & Fuchs-Schündeln, 2017).

So in the above two scenarios, the value of the invested money has a huge significance on the

laws of the taxation. The two cases are completely different. In the very first case, the receipt is

in the hands of the Bill and is recurring whereas in the second case, the receipt is in the hands of

the bill but that is not recurring that provides the right to receive the payments from the logging

of the trees in the further situations. He will get the same receipt in a bigger one and that will be

9

considered as the one-time receipt (Besley & Persson, 2013). These are considered as the one-

time receipt because, when they are removed from the land, it will take more time to again grow

the trees on the same piece of the land. So, in the next situation, Bill is getting enough amount of

money from the opposite side. This act is considered a lump sum by selling assets. When one

party sells the product to the other party, then the same receipt is considered as well as the

taxation. When it was observed that the first case didn't attract any tax gain, then it should treat

as a normal tax and no capital gain.

References

Auerbach, A.J. and Hassett, K., 2015. Capital taxation in the twenty-first century. The American

Economic Review, 105(5), pp.38-42.

Basu, S., Vellakkal, S., Agrawal, S., Stuckler, D., Popkin, B. and Ebrahim, S., 2014. Averting

obesity and type 2 diabetes in India through sugar-sweetened beverage taxation: an economic-

epidemiologic modeling study. PLoS medicine, 11(1), p.e1001582.

Besley, T.J. and Persson, T., 2013. Taxation and development.

Bick, A. and Fuchs-Schündeln, N., 2017. Quantifying the Disincentive Effects of Joint Taxation

on Married Women's Labor Supply. American Economic Review, 107(5), pp.100-104.

Chen, Q., Wang, Y. and Yang, C.L., 2014. Taxation under Autocracy: Theory and Evidence

from Late Imperial China (No. 2014-03). School of Economics, Shandong University.

Dowell, S., 2013. History of Taxation and Taxes in England (Vol. 1). Routledge.

Farhi, E. and Gabaix, X., 2015. Optimal taxation with behavioral agents (No. w21524). National

Bureau of Economic Research.

Farhi, E. and Werning, I., 2013. Insurance and taxation over the life cycle. Review of Economic

Studies, 80(2), pp.596-635.

Guner, N., Kaygusuz, R. and Ventura, G., 2014. Income taxation of US households: Facts and

parametric estimates. Review of Economic Dynamics, 17(4), pp.559-581.

considered as the one-time receipt (Besley & Persson, 2013). These are considered as the one-

time receipt because, when they are removed from the land, it will take more time to again grow

the trees on the same piece of the land. So, in the next situation, Bill is getting enough amount of

money from the opposite side. This act is considered a lump sum by selling assets. When one

party sells the product to the other party, then the same receipt is considered as well as the

taxation. When it was observed that the first case didn't attract any tax gain, then it should treat

as a normal tax and no capital gain.

References

Auerbach, A.J. and Hassett, K., 2015. Capital taxation in the twenty-first century. The American

Economic Review, 105(5), pp.38-42.

Basu, S., Vellakkal, S., Agrawal, S., Stuckler, D., Popkin, B. and Ebrahim, S., 2014. Averting

obesity and type 2 diabetes in India through sugar-sweetened beverage taxation: an economic-

epidemiologic modeling study. PLoS medicine, 11(1), p.e1001582.

Besley, T.J. and Persson, T., 2013. Taxation and development.

Bick, A. and Fuchs-Schündeln, N., 2017. Quantifying the Disincentive Effects of Joint Taxation

on Married Women's Labor Supply. American Economic Review, 107(5), pp.100-104.

Chen, Q., Wang, Y. and Yang, C.L., 2014. Taxation under Autocracy: Theory and Evidence

from Late Imperial China (No. 2014-03). School of Economics, Shandong University.

Dowell, S., 2013. History of Taxation and Taxes in England (Vol. 1). Routledge.

Farhi, E. and Gabaix, X., 2015. Optimal taxation with behavioral agents (No. w21524). National

Bureau of Economic Research.

Farhi, E. and Werning, I., 2013. Insurance and taxation over the life cycle. Review of Economic

Studies, 80(2), pp.596-635.

Guner, N., Kaygusuz, R. and Ventura, G., 2014. Income taxation of US households: Facts and

parametric estimates. Review of Economic Dynamics, 17(4), pp.559-581.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

Kleven, H.J., Landais, C. and Saez, E., 2013. Taxation and international migration of superstars:

Evidence from the European football market. The American Economic Review, 103(5), pp.1892-

1924.

McDaniel, P.R., Repetti, J.R. and Ring, D.M., 2014. Introduction to United States international

taxation. Wolters Kluwer Law & Business.

Mellon, A.W., 2016. Taxation: the people’s business. Pickle Partners Publishing.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Piketty, T. and Saez, E., 2013. A theory of optimal inheritance taxation. Econometrica, 81(5),

pp.1851-1886.

Rothschild, C. and Scheuer, F., 2016. Optimal taxation with rent-seeking. The Review of

Economic Studies, 83(3), pp.1225-1262.

Tanzi, V., 2014. Inflation, indexation and interest income taxation. PSL Quarterly

Review, 29(116).

Kleven, H.J., Landais, C. and Saez, E., 2013. Taxation and international migration of superstars:

Evidence from the European football market. The American Economic Review, 103(5), pp.1892-

1924.

McDaniel, P.R., Repetti, J.R. and Ring, D.M., 2014. Introduction to United States international

taxation. Wolters Kluwer Law & Business.

Mellon, A.W., 2016. Taxation: the people’s business. Pickle Partners Publishing.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Piketty, T. and Saez, E., 2013. A theory of optimal inheritance taxation. Econometrica, 81(5),

pp.1851-1886.

Rothschild, C. and Scheuer, F., 2016. Optimal taxation with rent-seeking. The Review of

Economic Studies, 83(3), pp.1225-1262.

Tanzi, V., 2014. Inflation, indexation and interest income taxation. PSL Quarterly

Review, 29(116).

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.