Taxation Report: Analysis of Capital Gains, Personal Exertion, Loans

VerifiedAdded on 2021/01/02

|9

|2439

|208

Report

AI Summary

This report examines various aspects of taxation in Australia, focusing on capital gains tax (CGT) consequences, income generated from personal exertion, and the impact of loan arrangements between family members. The report begins by defining CGT events and their treatment, including exemptions for personal properties and collectables. It then analyzes specific scenarios involving the sale of collectables, detailing the tax treatment based on acquisition and disposal dates. The second part delves into income from personal exertion, using a two-step approach to identify relevant transactions and assess whether the rewards received are directly linked to personal efforts. The report analyzes scenarios where an individual, Barbara, receives income from writing and selling a book, as well as from selling manuscripts and collecting interview manuscripts. The third part assesses the impact of a loan arrangement between a father and son on Patrick's income, considering the tax implications of the additional payments received by Patrick. The report concludes by summarizing the key findings and emphasizing the importance of understanding tax implications for businesses and individuals.

TAXATION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

QUESTION 1...................................................................................................................................3

Capital Gain Tax Consequences.................................................................................................3

QUESTION 2...................................................................................................................................5

Identifying transactions generating Income from Personal Exertion..........................................5

Treatment of Rewards Received if Book was written otherwise................................................6

QUESTION 3...................................................................................................................................7

Impact of Arrangement on Income of Patrick.............................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................3

QUESTION 1...................................................................................................................................3

Capital Gain Tax Consequences.................................................................................................3

QUESTION 2...................................................................................................................................5

Identifying transactions generating Income from Personal Exertion..........................................5

Treatment of Rewards Received if Book was written otherwise................................................6

QUESTION 3...................................................................................................................................7

Impact of Arrangement on Income of Patrick.............................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................9

INTRODUCTION

Taxation is a method of revenue collection which is implemented by National, State or

Territorial governments all around the world (Evans, Minas and Lim, 2015). In Australia, this

activity is carried out by ATO, the Australian Taxation Office. This report aims to look at

different case scenarios in the light of various statutory tax as well as case laws. The report is

divided into three parts viz. Question One, Two and Three, that mainly discuss about Capital

Gain Tax Consequences and their treatment for taxation purposes, income generated from

personal exertion as well as impact of loan arrangements made between the family members on

the assessable income of lender.

QUESTION 1

Capital Gain Tax Consequences

A Capital Gain Tax (CGT) Event is one which results in either Capital Gain or Loss on

part of the individual (Types of CGT Event, 2019). It may relate either Purchase of an asset or its

disposal. There are many that have been identified under this category like loss or destruction of

a class or a single unit of an asset. It is important to note that there are some exemptions to this

rule. These exclude personal properties of the buyer or seller such as main residence,

collectables, car or motorcycle or those which have been acquired on or before September 20,

1985.

A collectable is defined as an asset which is mainly used for personal purposes. These

include paintings, sculptures, jewellery, drawings and pictures among others. In case of any

interest, debt, option and/or right arises either on acquisition or disposition of such an asset, it

can be termed as a collectable too. Any Capital Gain or Loss generated through Disposal of

Asset, specifically Collectables [CGT Event A1], is disregarded. This statement holds true under

the following conditions:

Acquisition Cost of such a CGT Asset is less than $500;

Interest Acquired in the collectable is less than $500 on or before December 16, 1995;

Interest Acquired in the collectable when its market value did not exceed $500.

Whereas any Capital Loss generated is treated as a reduction from the total capital gains

amount which is acquired from the sale of other collectables. Also, if an asset is disposed of

Taxation is a method of revenue collection which is implemented by National, State or

Territorial governments all around the world (Evans, Minas and Lim, 2015). In Australia, this

activity is carried out by ATO, the Australian Taxation Office. This report aims to look at

different case scenarios in the light of various statutory tax as well as case laws. The report is

divided into three parts viz. Question One, Two and Three, that mainly discuss about Capital

Gain Tax Consequences and their treatment for taxation purposes, income generated from

personal exertion as well as impact of loan arrangements made between the family members on

the assessable income of lender.

QUESTION 1

Capital Gain Tax Consequences

A Capital Gain Tax (CGT) Event is one which results in either Capital Gain or Loss on

part of the individual (Types of CGT Event, 2019). It may relate either Purchase of an asset or its

disposal. There are many that have been identified under this category like loss or destruction of

a class or a single unit of an asset. It is important to note that there are some exemptions to this

rule. These exclude personal properties of the buyer or seller such as main residence,

collectables, car or motorcycle or those which have been acquired on or before September 20,

1985.

A collectable is defined as an asset which is mainly used for personal purposes. These

include paintings, sculptures, jewellery, drawings and pictures among others. In case of any

interest, debt, option and/or right arises either on acquisition or disposition of such an asset, it

can be termed as a collectable too. Any Capital Gain or Loss generated through Disposal of

Asset, specifically Collectables [CGT Event A1], is disregarded. This statement holds true under

the following conditions:

Acquisition Cost of such a CGT Asset is less than $500;

Interest Acquired in the collectable is less than $500 on or before December 16, 1995;

Interest Acquired in the collectable when its market value did not exceed $500.

Whereas any Capital Loss generated is treated as a reduction from the total capital gains

amount which is acquired from the sale of other collectables. Also, if an asset is disposed of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

separately which would otherwise be sold as a set, it is exempted in case such a set of an asset

was acquired at a price of $500 or less on or after December 16, 1995.

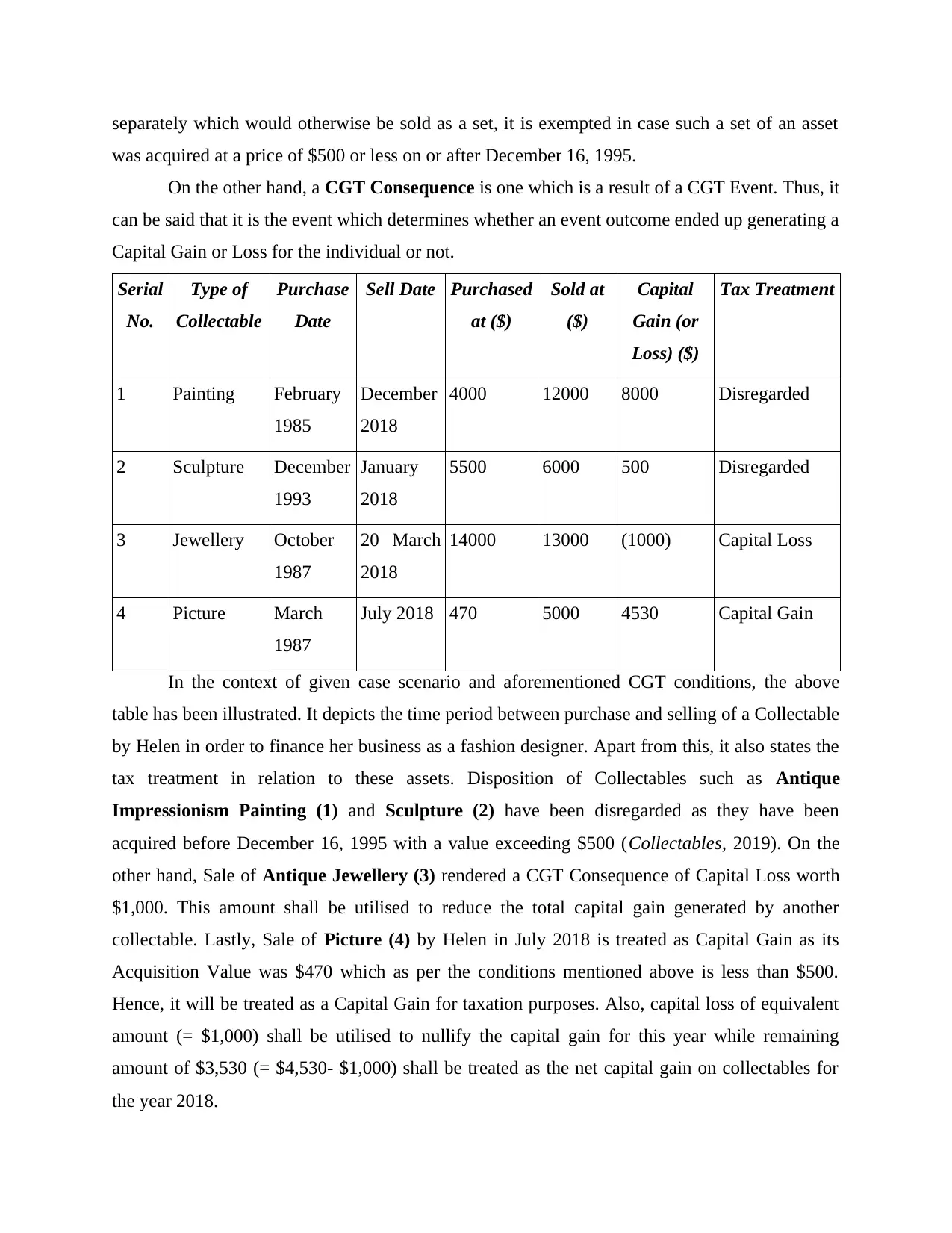

On the other hand, a CGT Consequence is one which is a result of a CGT Event. Thus, it

can be said that it is the event which determines whether an event outcome ended up generating a

Capital Gain or Loss for the individual or not.

Serial

No.

Type of

Collectable

Purchase

Date

Sell Date Purchased

at ($)

Sold at

($)

Capital

Gain (or

Loss) ($)

Tax Treatment

1 Painting February

1985

December

2018

4000 12000 8000 Disregarded

2 Sculpture December

1993

January

2018

5500 6000 500 Disregarded

3 Jewellery October

1987

20 March

2018

14000 13000 (1000) Capital Loss

4 Picture March

1987

July 2018 470 5000 4530 Capital Gain

In the context of given case scenario and aforementioned CGT conditions, the above

table has been illustrated. It depicts the time period between purchase and selling of a Collectable

by Helen in order to finance her business as a fashion designer. Apart from this, it also states the

tax treatment in relation to these assets. Disposition of Collectables such as Antique

Impressionism Painting (1) and Sculpture (2) have been disregarded as they have been

acquired before December 16, 1995 with a value exceeding $500 (Collectables, 2019). On the

other hand, Sale of Antique Jewellery (3) rendered a CGT Consequence of Capital Loss worth

$1,000. This amount shall be utilised to reduce the total capital gain generated by another

collectable. Lastly, Sale of Picture (4) by Helen in July 2018 is treated as Capital Gain as its

Acquisition Value was $470 which as per the conditions mentioned above is less than $500.

Hence, it will be treated as a Capital Gain for taxation purposes. Also, capital loss of equivalent

amount (= $1,000) shall be utilised to nullify the capital gain for this year while remaining

amount of $3,530 (= $4,530- $1,000) shall be treated as the net capital gain on collectables for

the year 2018.

was acquired at a price of $500 or less on or after December 16, 1995.

On the other hand, a CGT Consequence is one which is a result of a CGT Event. Thus, it

can be said that it is the event which determines whether an event outcome ended up generating a

Capital Gain or Loss for the individual or not.

Serial

No.

Type of

Collectable

Purchase

Date

Sell Date Purchased

at ($)

Sold at

($)

Capital

Gain (or

Loss) ($)

Tax Treatment

1 Painting February

1985

December

2018

4000 12000 8000 Disregarded

2 Sculpture December

1993

January

2018

5500 6000 500 Disregarded

3 Jewellery October

1987

20 March

2018

14000 13000 (1000) Capital Loss

4 Picture March

1987

July 2018 470 5000 4530 Capital Gain

In the context of given case scenario and aforementioned CGT conditions, the above

table has been illustrated. It depicts the time period between purchase and selling of a Collectable

by Helen in order to finance her business as a fashion designer. Apart from this, it also states the

tax treatment in relation to these assets. Disposition of Collectables such as Antique

Impressionism Painting (1) and Sculpture (2) have been disregarded as they have been

acquired before December 16, 1995 with a value exceeding $500 (Collectables, 2019). On the

other hand, Sale of Antique Jewellery (3) rendered a CGT Consequence of Capital Loss worth

$1,000. This amount shall be utilised to reduce the total capital gain generated by another

collectable. Lastly, Sale of Picture (4) by Helen in July 2018 is treated as Capital Gain as its

Acquisition Value was $470 which as per the conditions mentioned above is less than $500.

Hence, it will be treated as a Capital Gain for taxation purposes. Also, capital loss of equivalent

amount (= $1,000) shall be utilised to nullify the capital gain for this year while remaining

amount of $3,530 (= $4,530- $1,000) shall be treated as the net capital gain on collectables for

the year 2018.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

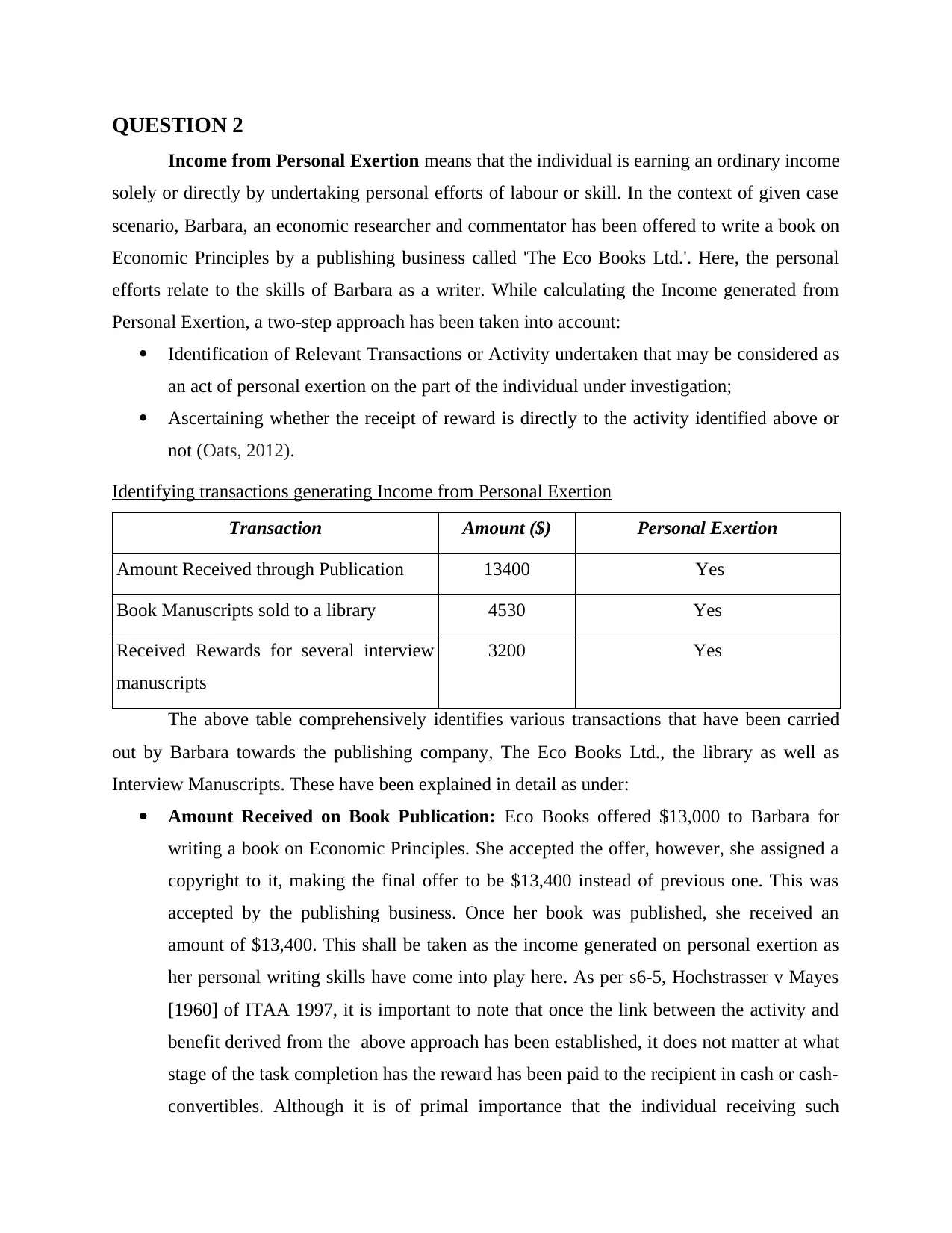

QUESTION 2

Income from Personal Exertion means that the individual is earning an ordinary income

solely or directly by undertaking personal efforts of labour or skill. In the context of given case

scenario, Barbara, an economic researcher and commentator has been offered to write a book on

Economic Principles by a publishing business called 'The Eco Books Ltd.'. Here, the personal

efforts relate to the skills of Barbara as a writer. While calculating the Income generated from

Personal Exertion, a two-step approach has been taken into account:

Identification of Relevant Transactions or Activity undertaken that may be considered as

an act of personal exertion on the part of the individual under investigation;

Ascertaining whether the receipt of reward is directly to the activity identified above or

not (Oats, 2012).

Identifying transactions generating Income from Personal Exertion

Transaction Amount ($) Personal Exertion

Amount Received through Publication 13400 Yes

Book Manuscripts sold to a library 4530 Yes

Received Rewards for several interview

manuscripts

3200 Yes

The above table comprehensively identifies various transactions that have been carried

out by Barbara towards the publishing company, The Eco Books Ltd., the library as well as

Interview Manuscripts. These have been explained in detail as under:

Amount Received on Book Publication: Eco Books offered $13,000 to Barbara for

writing a book on Economic Principles. She accepted the offer, however, she assigned a

copyright to it, making the final offer to be $13,400 instead of previous one. This was

accepted by the publishing business. Once her book was published, she received an

amount of $13,400. This shall be taken as the income generated on personal exertion as

her personal writing skills have come into play here. As per s6-5, Hochstrasser v Mayes

[1960] of ITAA 1997, it is important to note that once the link between the activity and

benefit derived from the above approach has been established, it does not matter at what

stage of the task completion has the reward has been paid to the recipient in cash or cash-

convertibles. Although it is of primal importance that the individual receiving such

Income from Personal Exertion means that the individual is earning an ordinary income

solely or directly by undertaking personal efforts of labour or skill. In the context of given case

scenario, Barbara, an economic researcher and commentator has been offered to write a book on

Economic Principles by a publishing business called 'The Eco Books Ltd.'. Here, the personal

efforts relate to the skills of Barbara as a writer. While calculating the Income generated from

Personal Exertion, a two-step approach has been taken into account:

Identification of Relevant Transactions or Activity undertaken that may be considered as

an act of personal exertion on the part of the individual under investigation;

Ascertaining whether the receipt of reward is directly to the activity identified above or

not (Oats, 2012).

Identifying transactions generating Income from Personal Exertion

Transaction Amount ($) Personal Exertion

Amount Received through Publication 13400 Yes

Book Manuscripts sold to a library 4530 Yes

Received Rewards for several interview

manuscripts

3200 Yes

The above table comprehensively identifies various transactions that have been carried

out by Barbara towards the publishing company, The Eco Books Ltd., the library as well as

Interview Manuscripts. These have been explained in detail as under:

Amount Received on Book Publication: Eco Books offered $13,000 to Barbara for

writing a book on Economic Principles. She accepted the offer, however, she assigned a

copyright to it, making the final offer to be $13,400 instead of previous one. This was

accepted by the publishing business. Once her book was published, she received an

amount of $13,400. This shall be taken as the income generated on personal exertion as

her personal writing skills have come into play here. As per s6-5, Hochstrasser v Mayes

[1960] of ITAA 1997, it is important to note that once the link between the activity and

benefit derived from the above approach has been established, it does not matter at what

stage of the task completion has the reward has been paid to the recipient in cash or cash-

convertibles. Although it is of primal importance that the individual receiving such

payment has incurred a real gain through it. In the following steps, transactions have been

identified in order to ascertain Barbara's Income generated from personal exertion

(Personal Exertion, 2019).

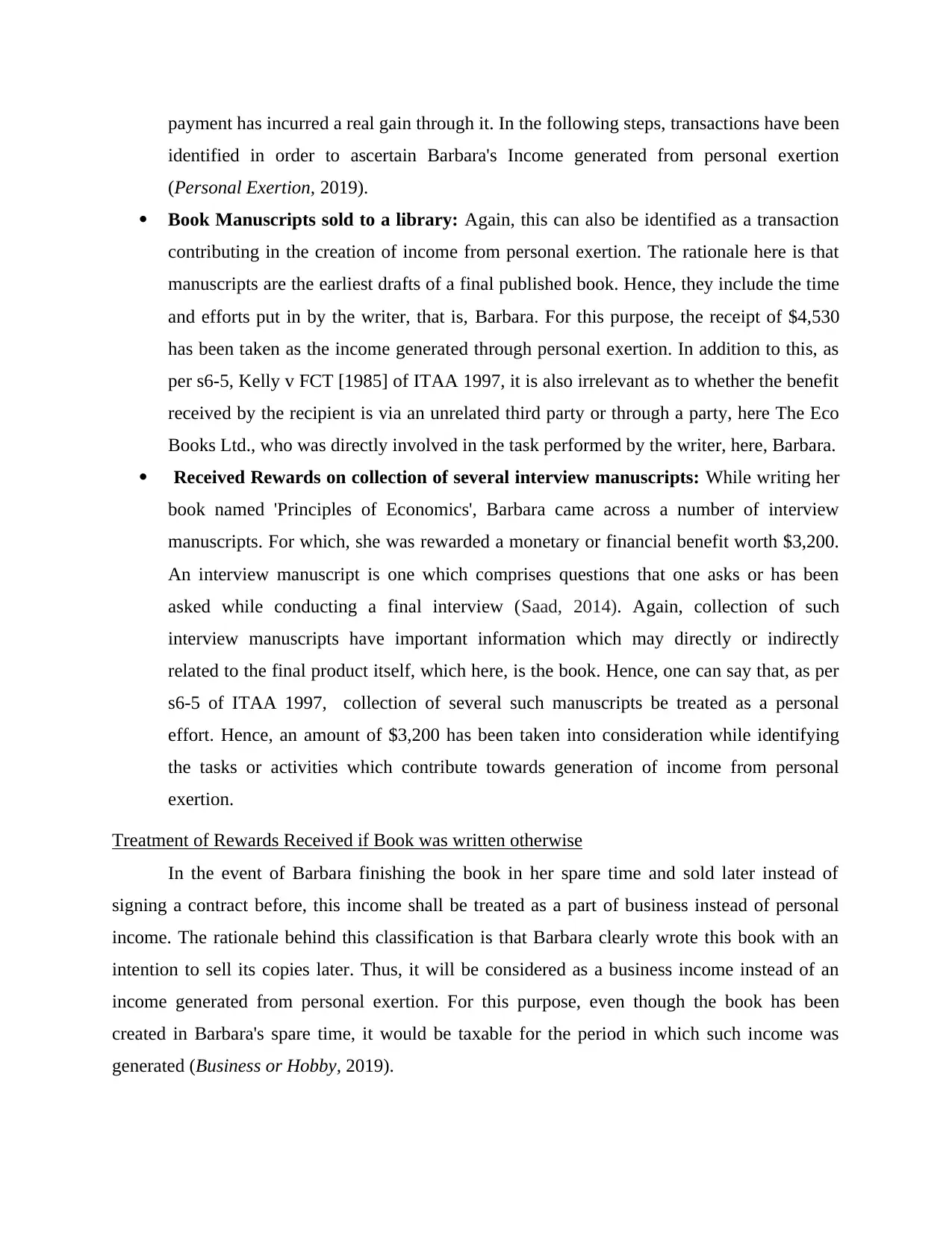

Book Manuscripts sold to a library: Again, this can also be identified as a transaction

contributing in the creation of income from personal exertion. The rationale here is that

manuscripts are the earliest drafts of a final published book. Hence, they include the time

and efforts put in by the writer, that is, Barbara. For this purpose, the receipt of $4,530

has been taken as the income generated through personal exertion. In addition to this, as

per s6-5, Kelly v FCT [1985] of ITAA 1997, it is also irrelevant as to whether the benefit

received by the recipient is via an unrelated third party or through a party, here The Eco

Books Ltd., who was directly involved in the task performed by the writer, here, Barbara.

Received Rewards on collection of several interview manuscripts: While writing her

book named 'Principles of Economics', Barbara came across a number of interview

manuscripts. For which, she was rewarded a monetary or financial benefit worth $3,200.

An interview manuscript is one which comprises questions that one asks or has been

asked while conducting a final interview (Saad, 2014). Again, collection of such

interview manuscripts have important information which may directly or indirectly

related to the final product itself, which here, is the book. Hence, one can say that, as per

s6-5 of ITAA 1997, collection of several such manuscripts be treated as a personal

effort. Hence, an amount of $3,200 has been taken into consideration while identifying

the tasks or activities which contribute towards generation of income from personal

exertion.

Treatment of Rewards Received if Book was written otherwise

In the event of Barbara finishing the book in her spare time and sold later instead of

signing a contract before, this income shall be treated as a part of business instead of personal

income. The rationale behind this classification is that Barbara clearly wrote this book with an

intention to sell its copies later. Thus, it will be considered as a business income instead of an

income generated from personal exertion. For this purpose, even though the book has been

created in Barbara's spare time, it would be taxable for the period in which such income was

generated (Business or Hobby, 2019).

identified in order to ascertain Barbara's Income generated from personal exertion

(Personal Exertion, 2019).

Book Manuscripts sold to a library: Again, this can also be identified as a transaction

contributing in the creation of income from personal exertion. The rationale here is that

manuscripts are the earliest drafts of a final published book. Hence, they include the time

and efforts put in by the writer, that is, Barbara. For this purpose, the receipt of $4,530

has been taken as the income generated through personal exertion. In addition to this, as

per s6-5, Kelly v FCT [1985] of ITAA 1997, it is also irrelevant as to whether the benefit

received by the recipient is via an unrelated third party or through a party, here The Eco

Books Ltd., who was directly involved in the task performed by the writer, here, Barbara.

Received Rewards on collection of several interview manuscripts: While writing her

book named 'Principles of Economics', Barbara came across a number of interview

manuscripts. For which, she was rewarded a monetary or financial benefit worth $3,200.

An interview manuscript is one which comprises questions that one asks or has been

asked while conducting a final interview (Saad, 2014). Again, collection of such

interview manuscripts have important information which may directly or indirectly

related to the final product itself, which here, is the book. Hence, one can say that, as per

s6-5 of ITAA 1997, collection of several such manuscripts be treated as a personal

effort. Hence, an amount of $3,200 has been taken into consideration while identifying

the tasks or activities which contribute towards generation of income from personal

exertion.

Treatment of Rewards Received if Book was written otherwise

In the event of Barbara finishing the book in her spare time and sold later instead of

signing a contract before, this income shall be treated as a part of business instead of personal

income. The rationale behind this classification is that Barbara clearly wrote this book with an

intention to sell its copies later. Thus, it will be considered as a business income instead of an

income generated from personal exertion. For this purpose, even though the book has been

created in Barbara's spare time, it would be taxable for the period in which such income was

generated (Business or Hobby, 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

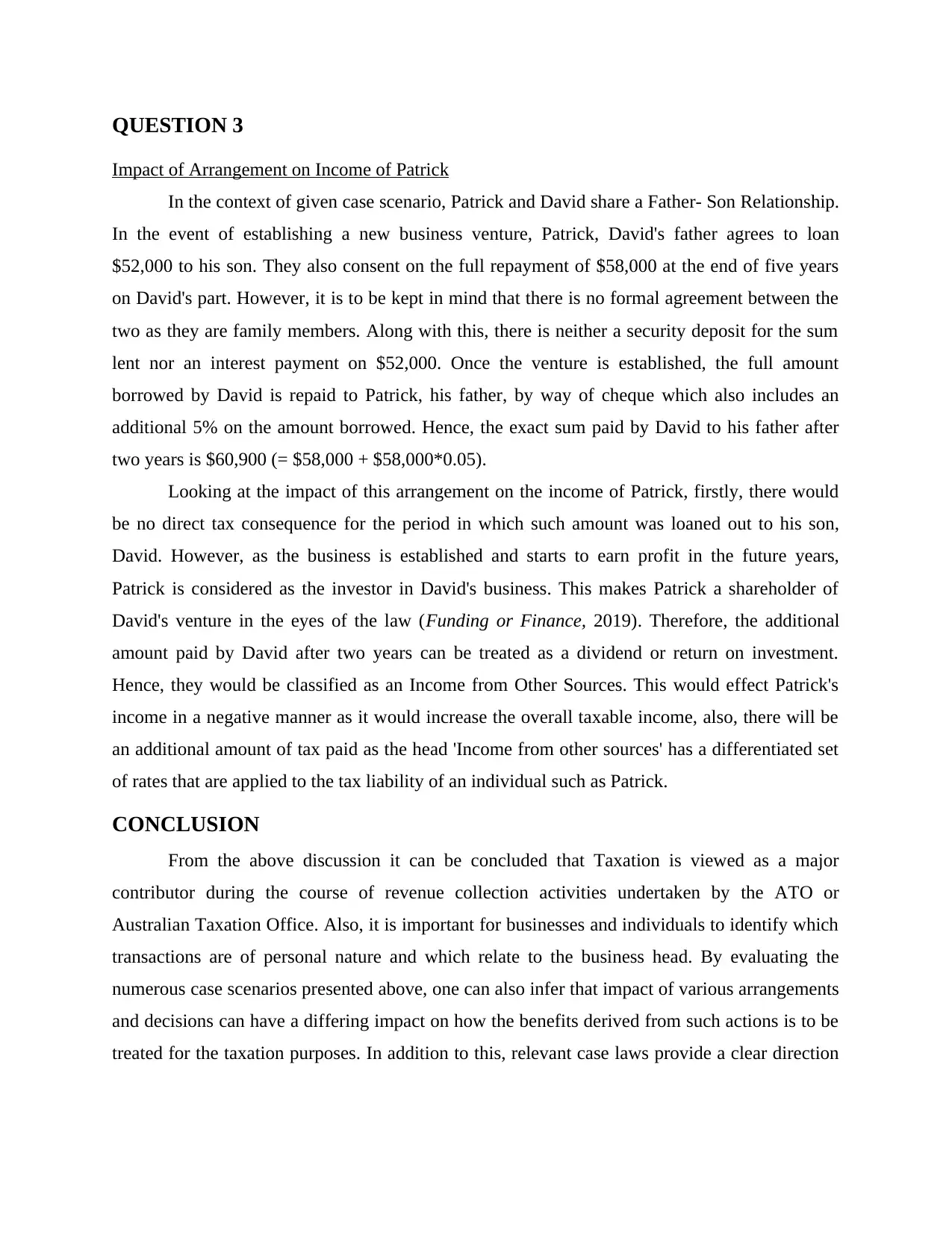

QUESTION 3

Impact of Arrangement on Income of Patrick

In the context of given case scenario, Patrick and David share a Father- Son Relationship.

In the event of establishing a new business venture, Patrick, David's father agrees to loan

$52,000 to his son. They also consent on the full repayment of $58,000 at the end of five years

on David's part. However, it is to be kept in mind that there is no formal agreement between the

two as they are family members. Along with this, there is neither a security deposit for the sum

lent nor an interest payment on $52,000. Once the venture is established, the full amount

borrowed by David is repaid to Patrick, his father, by way of cheque which also includes an

additional 5% on the amount borrowed. Hence, the exact sum paid by David to his father after

two years is $60,900 (= $58,000 + $58,000*0.05).

Looking at the impact of this arrangement on the income of Patrick, firstly, there would

be no direct tax consequence for the period in which such amount was loaned out to his son,

David. However, as the business is established and starts to earn profit in the future years,

Patrick is considered as the investor in David's business. This makes Patrick a shareholder of

David's venture in the eyes of the law (Funding or Finance, 2019). Therefore, the additional

amount paid by David after two years can be treated as a dividend or return on investment.

Hence, they would be classified as an Income from Other Sources. This would effect Patrick's

income in a negative manner as it would increase the overall taxable income, also, there will be

an additional amount of tax paid as the head 'Income from other sources' has a differentiated set

of rates that are applied to the tax liability of an individual such as Patrick.

CONCLUSION

From the above discussion it can be concluded that Taxation is viewed as a major

contributor during the course of revenue collection activities undertaken by the ATO or

Australian Taxation Office. Also, it is important for businesses and individuals to identify which

transactions are of personal nature and which relate to the business head. By evaluating the

numerous case scenarios presented above, one can also infer that impact of various arrangements

and decisions can have a differing impact on how the benefits derived from such actions is to be

treated for the taxation purposes. In addition to this, relevant case laws provide a clear direction

Impact of Arrangement on Income of Patrick

In the context of given case scenario, Patrick and David share a Father- Son Relationship.

In the event of establishing a new business venture, Patrick, David's father agrees to loan

$52,000 to his son. They also consent on the full repayment of $58,000 at the end of five years

on David's part. However, it is to be kept in mind that there is no formal agreement between the

two as they are family members. Along with this, there is neither a security deposit for the sum

lent nor an interest payment on $52,000. Once the venture is established, the full amount

borrowed by David is repaid to Patrick, his father, by way of cheque which also includes an

additional 5% on the amount borrowed. Hence, the exact sum paid by David to his father after

two years is $60,900 (= $58,000 + $58,000*0.05).

Looking at the impact of this arrangement on the income of Patrick, firstly, there would

be no direct tax consequence for the period in which such amount was loaned out to his son,

David. However, as the business is established and starts to earn profit in the future years,

Patrick is considered as the investor in David's business. This makes Patrick a shareholder of

David's venture in the eyes of the law (Funding or Finance, 2019). Therefore, the additional

amount paid by David after two years can be treated as a dividend or return on investment.

Hence, they would be classified as an Income from Other Sources. This would effect Patrick's

income in a negative manner as it would increase the overall taxable income, also, there will be

an additional amount of tax paid as the head 'Income from other sources' has a differentiated set

of rates that are applied to the tax liability of an individual such as Patrick.

CONCLUSION

From the above discussion it can be concluded that Taxation is viewed as a major

contributor during the course of revenue collection activities undertaken by the ATO or

Australian Taxation Office. Also, it is important for businesses and individuals to identify which

transactions are of personal nature and which relate to the business head. By evaluating the

numerous case scenarios presented above, one can also infer that impact of various arrangements

and decisions can have a differing impact on how the benefits derived from such actions is to be

treated for the taxation purposes. In addition to this, relevant case laws provide a clear direction

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

to individuals as well as tax authorities in determining the nature of income generated for a

particular assessment year.

particular assessment year.

REFERENCES

Books and Journal

Evans, C., Minas, J. and Lim, Y., 2015. Taxing personal capital gains in Australia: an alternative

way forward. Austl. Tax F.. 30. p.735.

Oats, L. ed., 2012. Taxation: a fieldwork research handbook. Routledge.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’ view. Procedia-

Social and Behavioral Sciences. 109. pp.1069-1075.

Online:

Types of CGT Event. 2019. [Online]. Available Through:

<https://www.ato.gov.au/general/capital-gains-tax/selling-an-asset-and-other-cgt-

events/types-of-cgt-events/#DisposalA>

Collectables. 2019. [Online]. Available Through:

<https://www.ato.gov.au/general/capital-gains-tax/cgt-assets-and-exemptions/>

Personal Exertion. 2019. [Online]. Available Through:

<https://s3.studentvip.com.au/notes/10824-sample.pdf>

Business or Hobby. 2019. [Online]. Available Through:

<https://www.business.gov.au/planning/new-businesses/a-business-or-a-hobby/>

Funding or Finance. 2019. [Online]. Available Through:

<https://www.ato.gov.au/Business/Privately-owned-and-wealthy-groups/Tax-

governance/Funding-and-finance/>

Books and Journal

Evans, C., Minas, J. and Lim, Y., 2015. Taxing personal capital gains in Australia: an alternative

way forward. Austl. Tax F.. 30. p.735.

Oats, L. ed., 2012. Taxation: a fieldwork research handbook. Routledge.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’ view. Procedia-

Social and Behavioral Sciences. 109. pp.1069-1075.

Online:

Types of CGT Event. 2019. [Online]. Available Through:

<https://www.ato.gov.au/general/capital-gains-tax/selling-an-asset-and-other-cgt-

events/types-of-cgt-events/#DisposalA>

Collectables. 2019. [Online]. Available Through:

<https://www.ato.gov.au/general/capital-gains-tax/cgt-assets-and-exemptions/>

Personal Exertion. 2019. [Online]. Available Through:

<https://s3.studentvip.com.au/notes/10824-sample.pdf>

Business or Hobby. 2019. [Online]. Available Through:

<https://www.business.gov.au/planning/new-businesses/a-business-or-a-hobby/>

Funding or Finance. 2019. [Online]. Available Through:

<https://www.ato.gov.au/Business/Privately-owned-and-wealthy-groups/Tax-

governance/Funding-and-finance/>

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.