Taxation Report: Mayfield Firm and Rapid Heat Pty Ltd Tax Analysis

VerifiedAdded on 2020/10/05

|11

|3388

|466

Report

AI Summary

This report, prepared for Desklib, delves into Australian taxation laws and practices, focusing on capital gains tax and tax liabilities for Mayfield firm and Rapid Heat Pty Ltd. It examines various scenarios, including the sale of land, an antique bed, a painting, shares, and a violin, to determine the tax implications. The report calculates capital gains and net tax payable amounts, offering insights into relevant tax regulations and policies. The report also addresses fringe benefit tax and provides suggestions for calculating tax liabilities in different situations, providing a comprehensive overview of taxation principles and practical applications, demonstrating the analysis of assessable income and tax implications for various transactions.

TAXATION THEORY, PRACTICE

& LAW

& LAW

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

a) Block of land...........................................................................................................................1

b) Antique bed.............................................................................................................................2

c) Painting...................................................................................................................................3

d) Shares......................................................................................................................................4

e) Violin......................................................................................................................................5

QUESTION 2...................................................................................................................................6

a) Suggestion regarding consequences while calculating FBT...................................................6

b) Changes in answer if purchase $50000 of the shares............................................................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

a) Block of land...........................................................................................................................1

b) Antique bed.............................................................................................................................2

c) Painting...................................................................................................................................3

d) Shares......................................................................................................................................4

e) Violin......................................................................................................................................5

QUESTION 2...................................................................................................................................6

a) Suggestion regarding consequences while calculating FBT...................................................6

b) Changes in answer if purchase $50000 of the shares............................................................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Tax is considered as a financial liability to be paid by individual to government, which is

utilised further to fulfil the public expenditure and projects. Taxation office of the governed

authority that provides rules and legislations related to tax collection, determining the tax

liability and finance charge for a particular time period (Burton, 2012). this report is divided in

major two parts in first part taxable criteria and calculations subject to capital gain or losses are

made for Mayfield firm as a tax consultant.

Second part contains the analysis of assessable tax for Rapid heat Pty Ltd an electric

heater manufacturer firm. A study on Fringe benefit tax is critically evaluated to attain tax credit.

Suggestions are provided in respect of consequences while calculating the tax liabilities for

different case scenarios and transactions. There are some transactions are given to determine the

tax accessibility and determine the total tax liability are considered in this report.

QUESTION 1

There are type of taxation rules are formed in Australia to ascertain the tax liability. As

an tax consultant of the region, advises and recommendations are asked and relate with the laws

form with the organisation. Diverse taxation rules and policies related to income tax and other

laws are considered viable for addressing public expenditure requirements (Tricker and Tricker,

2015). Solutions and remedies provided for treatment of different monetary and non monetary

transactions with in and outside the organisation.

a) Block of land

Case study: As an tax consultant in Mafirld, New south Wales, it is required to analyse

the transaction of block of land. On 3 June of the current tax year a contract of sale of block of

land was considered that contains cost of $320000 for block f land. The cost of acquisition in

January was $100000 and cost was incurred as $20000 in local council, water and sewerage rates

as deposit. A capital gain would be occurred in this case and a taxable amount will be paid by

client for current assessment year.

Rules and legislations related to tax: In the above case, it is determined that the capital

gain will be payable to the government of the Australia by the assesses. Block of land will be

countable as an immovable property owned by the organisation or individual as an investment or

for residential purpose (Capital gain tax. 2018). In the above case the block of land acquired

1

Tax is considered as a financial liability to be paid by individual to government, which is

utilised further to fulfil the public expenditure and projects. Taxation office of the governed

authority that provides rules and legislations related to tax collection, determining the tax

liability and finance charge for a particular time period (Burton, 2012). this report is divided in

major two parts in first part taxable criteria and calculations subject to capital gain or losses are

made for Mayfield firm as a tax consultant.

Second part contains the analysis of assessable tax for Rapid heat Pty Ltd an electric

heater manufacturer firm. A study on Fringe benefit tax is critically evaluated to attain tax credit.

Suggestions are provided in respect of consequences while calculating the tax liabilities for

different case scenarios and transactions. There are some transactions are given to determine the

tax accessibility and determine the total tax liability are considered in this report.

QUESTION 1

There are type of taxation rules are formed in Australia to ascertain the tax liability. As

an tax consultant of the region, advises and recommendations are asked and relate with the laws

form with the organisation. Diverse taxation rules and policies related to income tax and other

laws are considered viable for addressing public expenditure requirements (Tricker and Tricker,

2015). Solutions and remedies provided for treatment of different monetary and non monetary

transactions with in and outside the organisation.

a) Block of land

Case study: As an tax consultant in Mafirld, New south Wales, it is required to analyse

the transaction of block of land. On 3 June of the current tax year a contract of sale of block of

land was considered that contains cost of $320000 for block f land. The cost of acquisition in

January was $100000 and cost was incurred as $20000 in local council, water and sewerage rates

as deposit. A capital gain would be occurred in this case and a taxable amount will be paid by

client for current assessment year.

Rules and legislations related to tax: In the above case, it is determined that the capital

gain will be payable to the government of the Australia by the assesses. Block of land will be

countable as an immovable property owned by the organisation or individual as an investment or

for residential purpose (Capital gain tax. 2018). In the above case the block of land acquired

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

after September 20, 1985. As per Australian Taxation office, vacant land will be counted as a

capital asset and similar capital gain taxes rules are analysed with the properties (Hopkins, 2011).

The cost incurred for maintenance, repair and extension will be allowed as income tax

deductions. Tax liability for the client is determined below;

Date Particulars Amount

Jan 2001 Purchase of block of vacant land 100000

Expenses of water, sewage and land taxes on land 20000

Total cost of land 120000

3 June 2017 Contract price of sale of block of vacant land 320000

3 June 2017 Deposit of contract price 20000

3 Jan 2018 Balance payment 300000

Capital gain 200000

Taxable capital gain 20000

Tax rate

19cents per dollars

exceeding 18201

Net tax payable amount 342

The above calculation produce the value of capital assets which is higher then the actual

cost. The above case helps to find out the value of correct capital gain and the total acquisition

cost of land. The gross capital gain is counted as $200000 after deducting the cost of acquisition

at the beginning of the year. $20000 will be considered at the time of aggrievement and

remaining amount will be received in next assessment year. According to current tax rate the if

capital amount is lower than $18201 than no any tax will be payable. Thus, the taxable ampunt

of in the case study is determined as $342.

b) Antique bed

Case scenario: A case of ascertaining the cost of antique bed is given in which assesses

claims for getting compensation form insurance company reading the antique bed bought in 1986

worth costing $5000 containing the expenses. The bed was stolen form the house and in this

duration the cost of the bed was valued at $25000. On November 13, 2017 client claimed for the

value of bed and insurance company rejected the application by mentioning that bed was not the

2

capital asset and similar capital gain taxes rules are analysed with the properties (Hopkins, 2011).

The cost incurred for maintenance, repair and extension will be allowed as income tax

deductions. Tax liability for the client is determined below;

Date Particulars Amount

Jan 2001 Purchase of block of vacant land 100000

Expenses of water, sewage and land taxes on land 20000

Total cost of land 120000

3 June 2017 Contract price of sale of block of vacant land 320000

3 June 2017 Deposit of contract price 20000

3 Jan 2018 Balance payment 300000

Capital gain 200000

Taxable capital gain 20000

Tax rate

19cents per dollars

exceeding 18201

Net tax payable amount 342

The above calculation produce the value of capital assets which is higher then the actual

cost. The above case helps to find out the value of correct capital gain and the total acquisition

cost of land. The gross capital gain is counted as $200000 after deducting the cost of acquisition

at the beginning of the year. $20000 will be considered at the time of aggrievement and

remaining amount will be received in next assessment year. According to current tax rate the if

capital amount is lower than $18201 than no any tax will be payable. Thus, the taxable ampunt

of in the case study is determined as $342.

b) Antique bed

Case scenario: A case of ascertaining the cost of antique bed is given in which assesses

claims for getting compensation form insurance company reading the antique bed bought in 1986

worth costing $5000 containing the expenses. The bed was stolen form the house and in this

duration the cost of the bed was valued at $25000. On November 13, 2017 client claimed for the

value of bed and insurance company rejected the application by mentioning that bed was not the

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

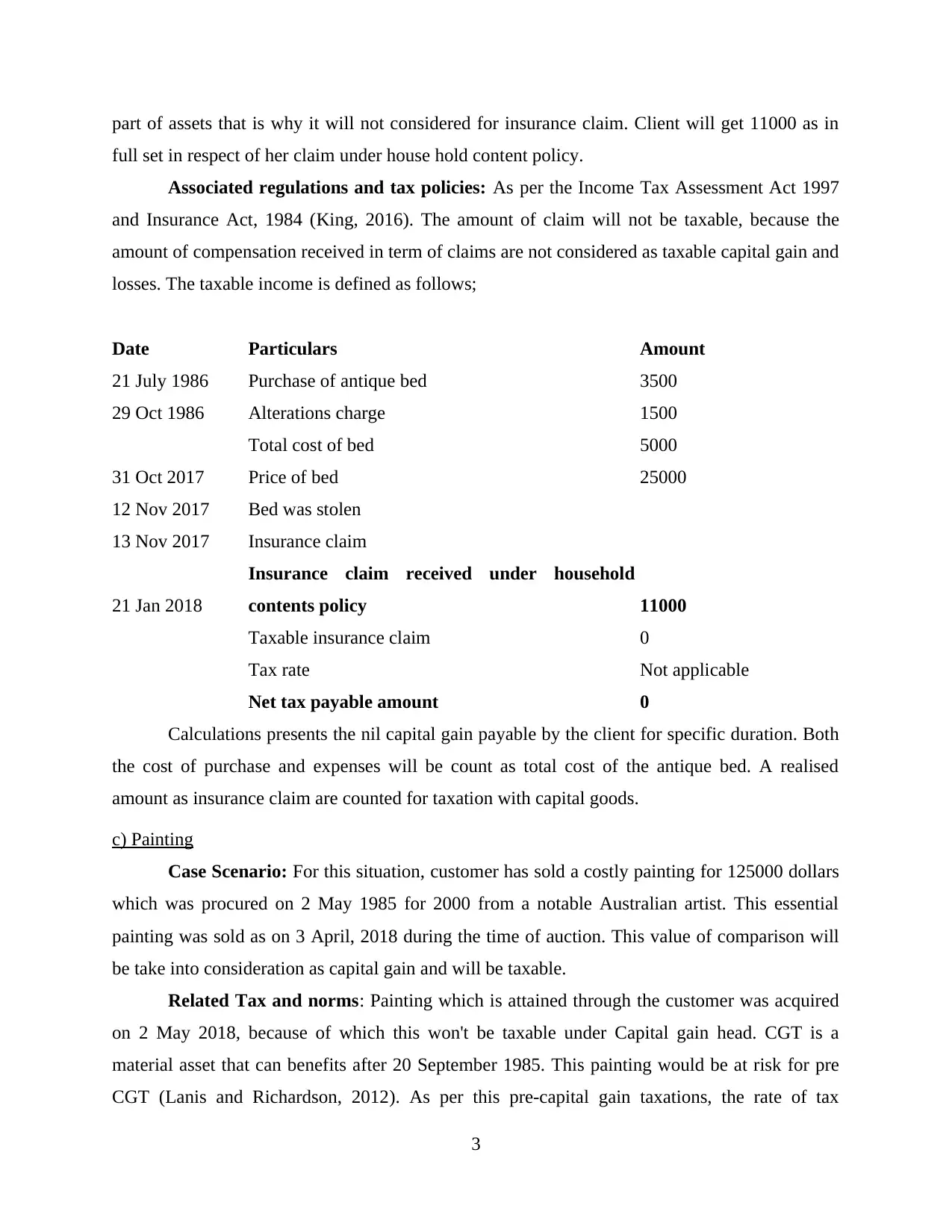

part of assets that is why it will not considered for insurance claim. Client will get 11000 as in

full set in respect of her claim under house hold content policy.

Associated regulations and tax policies: As per the Income Tax Assessment Act 1997

and Insurance Act, 1984 (King, 2016). The amount of claim will not be taxable, because the

amount of compensation received in term of claims are not considered as taxable capital gain and

losses. The taxable income is defined as follows;

Date Particulars Amount

21 July 1986 Purchase of antique bed 3500

29 Oct 1986 Alterations charge 1500

Total cost of bed 5000

31 Oct 2017 Price of bed 25000

12 Nov 2017 Bed was stolen

13 Nov 2017 Insurance claim

21 Jan 2018

Insurance claim received under household

contents policy 11000

Taxable insurance claim 0

Tax rate Not applicable

Net tax payable amount 0

Calculations presents the nil capital gain payable by the client for specific duration. Both

the cost of purchase and expenses will be count as total cost of the antique bed. A realised

amount as insurance claim are counted for taxation with capital goods.

c) Painting

Case Scenario: For this situation, customer has sold a costly painting for 125000 dollars

which was procured on 2 May 1985 for 2000 from a notable Australian artist. This essential

painting was sold as on 3 April, 2018 during the time of auction. This value of comparison will

be take into consideration as capital gain and will be taxable.

Related Tax and norms: Painting which is attained through the customer was acquired

on 2 May 2018, because of which this won't be taxable under Capital gain head. CGT is a

material asset that can benefits after 20 September 1985. This painting would be at risk for pre

CGT (Lanis and Richardson, 2012). As per this pre-capital gain taxations, the rate of tax

3

full set in respect of her claim under house hold content policy.

Associated regulations and tax policies: As per the Income Tax Assessment Act 1997

and Insurance Act, 1984 (King, 2016). The amount of claim will not be taxable, because the

amount of compensation received in term of claims are not considered as taxable capital gain and

losses. The taxable income is defined as follows;

Date Particulars Amount

21 July 1986 Purchase of antique bed 3500

29 Oct 1986 Alterations charge 1500

Total cost of bed 5000

31 Oct 2017 Price of bed 25000

12 Nov 2017 Bed was stolen

13 Nov 2017 Insurance claim

21 Jan 2018

Insurance claim received under household

contents policy 11000

Taxable insurance claim 0

Tax rate Not applicable

Net tax payable amount 0

Calculations presents the nil capital gain payable by the client for specific duration. Both

the cost of purchase and expenses will be count as total cost of the antique bed. A realised

amount as insurance claim are counted for taxation with capital goods.

c) Painting

Case Scenario: For this situation, customer has sold a costly painting for 125000 dollars

which was procured on 2 May 1985 for 2000 from a notable Australian artist. This essential

painting was sold as on 3 April, 2018 during the time of auction. This value of comparison will

be take into consideration as capital gain and will be taxable.

Related Tax and norms: Painting which is attained through the customer was acquired

on 2 May 2018, because of which this won't be taxable under Capital gain head. CGT is a

material asset that can benefits after 20 September 1985. This painting would be at risk for pre

CGT (Lanis and Richardson, 2012). As per this pre-capital gain taxations, the rate of tax

3

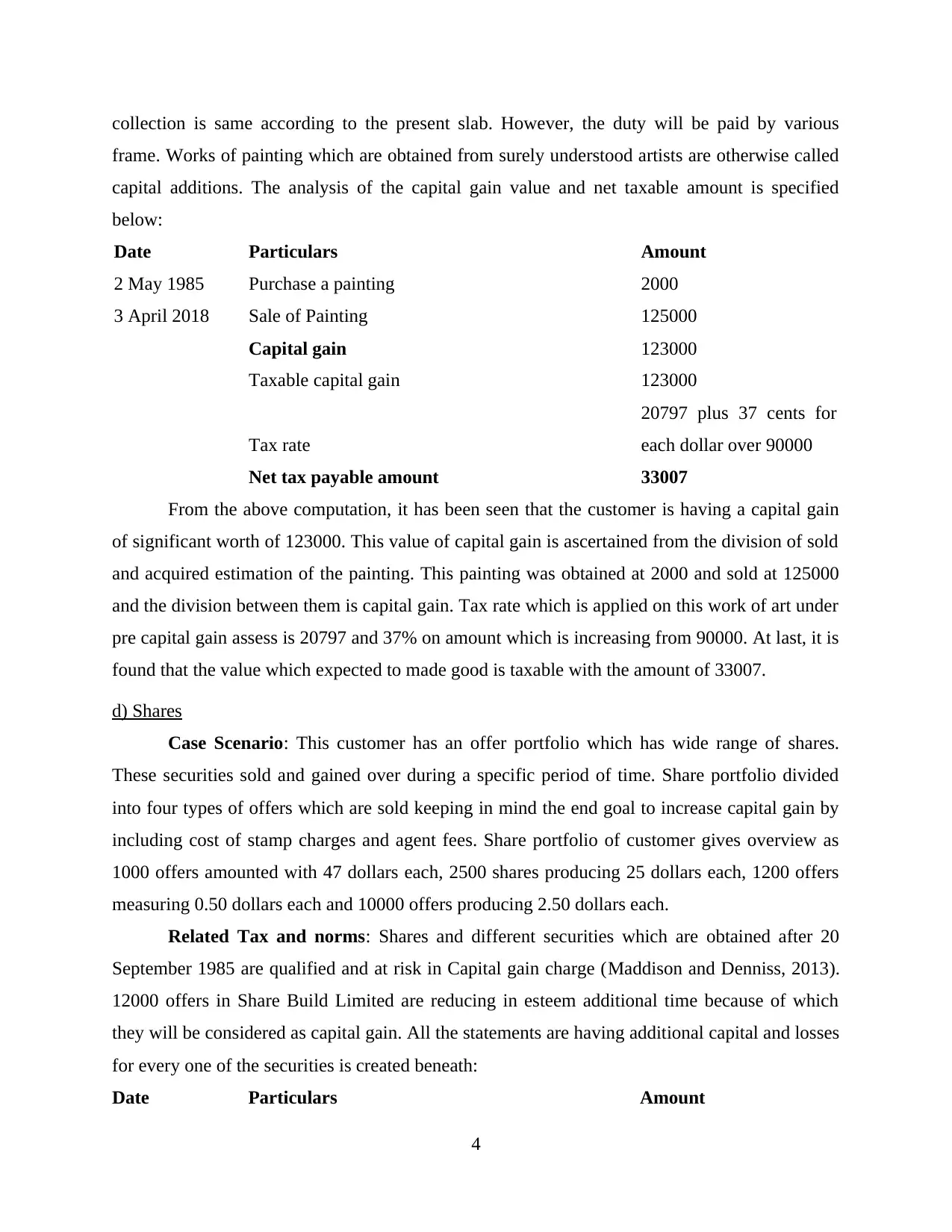

collection is same according to the present slab. However, the duty will be paid by various

frame. Works of painting which are obtained from surely understood artists are otherwise called

capital additions. The analysis of the capital gain value and net taxable amount is specified

below:

Date Particulars Amount

2 May 1985 Purchase a painting 2000

3 April 2018 Sale of Painting 125000

Capital gain 123000

Taxable capital gain 123000

Tax rate

20797 plus 37 cents for

each dollar over 90000

Net tax payable amount 33007

From the above computation, it has been seen that the customer is having a capital gain

of significant worth of 123000. This value of capital gain is ascertained from the division of sold

and acquired estimation of the painting. This painting was obtained at 2000 and sold at 125000

and the division between them is capital gain. Tax rate which is applied on this work of art under

pre capital gain assess is 20797 and 37% on amount which is increasing from 90000. At last, it is

found that the value which expected to made good is taxable with the amount of 33007.

d) Shares

Case Scenario: This customer has an offer portfolio which has wide range of shares.

These securities sold and gained over during a specific period of time. Share portfolio divided

into four types of offers which are sold keeping in mind the end goal to increase capital gain by

including cost of stamp charges and agent fees. Share portfolio of customer gives overview as

1000 offers amounted with 47 dollars each, 2500 shares producing 25 dollars each, 1200 offers

measuring 0.50 dollars each and 10000 offers producing 2.50 dollars each.

Related Tax and norms: Shares and different securities which are obtained after 20

September 1985 are qualified and at risk in Capital gain charge (Maddison and Denniss, 2013).

12000 offers in Share Build Limited are reducing in esteem additional time because of which

they will be considered as capital gain. All the statements are having additional capital and losses

for every one of the securities is created beneath:

Date Particulars Amount

4

frame. Works of painting which are obtained from surely understood artists are otherwise called

capital additions. The analysis of the capital gain value and net taxable amount is specified

below:

Date Particulars Amount

2 May 1985 Purchase a painting 2000

3 April 2018 Sale of Painting 125000

Capital gain 123000

Taxable capital gain 123000

Tax rate

20797 plus 37 cents for

each dollar over 90000

Net tax payable amount 33007

From the above computation, it has been seen that the customer is having a capital gain

of significant worth of 123000. This value of capital gain is ascertained from the division of sold

and acquired estimation of the painting. This painting was obtained at 2000 and sold at 125000

and the division between them is capital gain. Tax rate which is applied on this work of art under

pre capital gain assess is 20797 and 37% on amount which is increasing from 90000. At last, it is

found that the value which expected to made good is taxable with the amount of 33007.

d) Shares

Case Scenario: This customer has an offer portfolio which has wide range of shares.

These securities sold and gained over during a specific period of time. Share portfolio divided

into four types of offers which are sold keeping in mind the end goal to increase capital gain by

including cost of stamp charges and agent fees. Share portfolio of customer gives overview as

1000 offers amounted with 47 dollars each, 2500 shares producing 25 dollars each, 1200 offers

measuring 0.50 dollars each and 10000 offers producing 2.50 dollars each.

Related Tax and norms: Shares and different securities which are obtained after 20

September 1985 are qualified and at risk in Capital gain charge (Maddison and Denniss, 2013).

12000 offers in Share Build Limited are reducing in esteem additional time because of which

they will be considered as capital gain. All the statements are having additional capital and losses

for every one of the securities is created beneath:

Date Particulars Amount

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

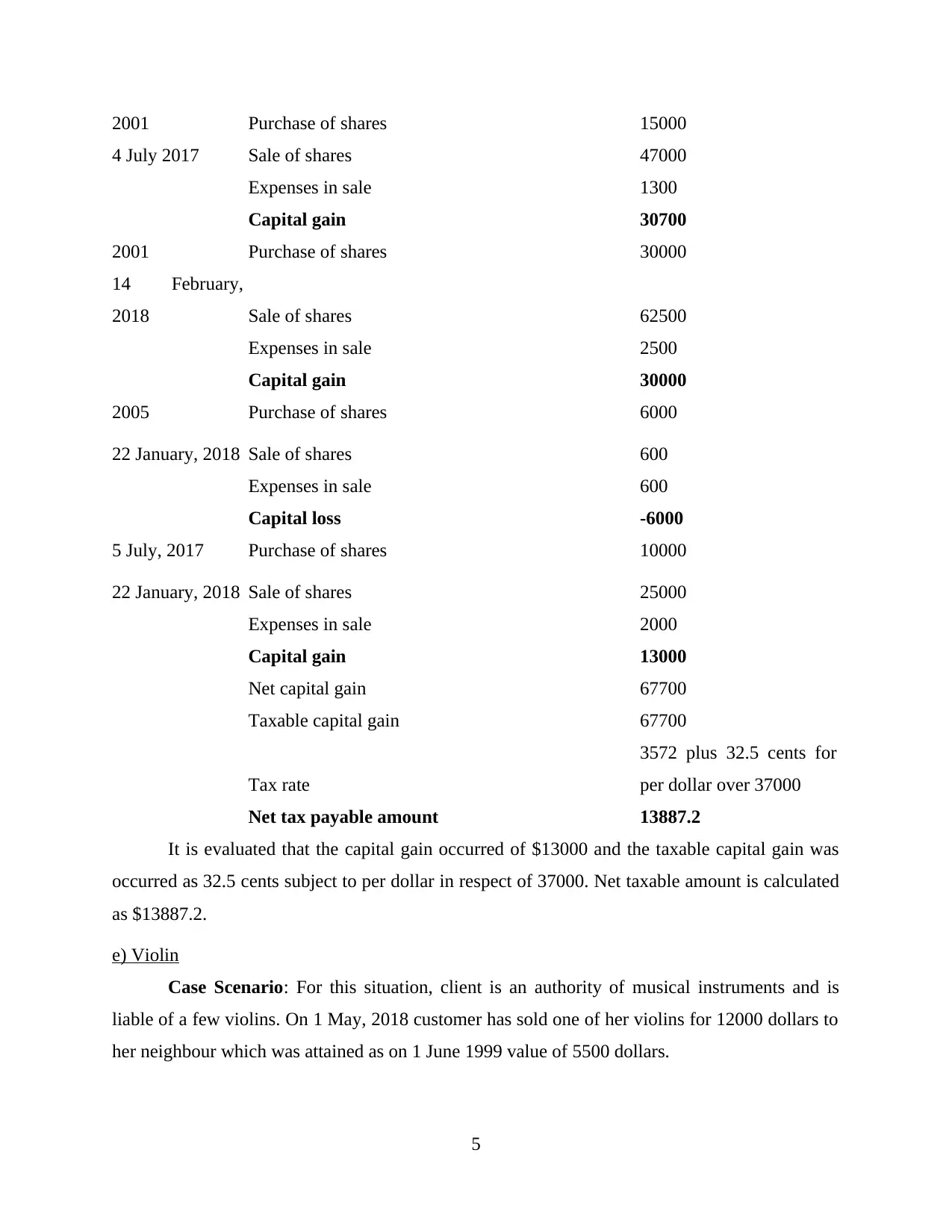

2001 Purchase of shares 15000

4 July 2017 Sale of shares 47000

Expenses in sale 1300

Capital gain 30700

2001 Purchase of shares 30000

14 February,

2018 Sale of shares 62500

Expenses in sale 2500

Capital gain 30000

2005 Purchase of shares 6000

22 January, 2018 Sale of shares 600

Expenses in sale 600

Capital loss -6000

5 July, 2017 Purchase of shares 10000

22 January, 2018 Sale of shares 25000

Expenses in sale 2000

Capital gain 13000

Net capital gain 67700

Taxable capital gain 67700

Tax rate

3572 plus 32.5 cents for

per dollar over 37000

Net tax payable amount 13887.2

It is evaluated that the capital gain occurred of $13000 and the taxable capital gain was

occurred as 32.5 cents subject to per dollar in respect of 37000. Net taxable amount is calculated

as $13887.2.

e) Violin

Case Scenario: For this situation, client is an authority of musical instruments and is

liable of a few violins. On 1 May, 2018 customer has sold one of her violins for 12000 dollars to

her neighbour which was attained as on 1 June 1999 value of 5500 dollars.

5

4 July 2017 Sale of shares 47000

Expenses in sale 1300

Capital gain 30700

2001 Purchase of shares 30000

14 February,

2018 Sale of shares 62500

Expenses in sale 2500

Capital gain 30000

2005 Purchase of shares 6000

22 January, 2018 Sale of shares 600

Expenses in sale 600

Capital loss -6000

5 July, 2017 Purchase of shares 10000

22 January, 2018 Sale of shares 25000

Expenses in sale 2000

Capital gain 13000

Net capital gain 67700

Taxable capital gain 67700

Tax rate

3572 plus 32.5 cents for

per dollar over 37000

Net tax payable amount 13887.2

It is evaluated that the capital gain occurred of $13000 and the taxable capital gain was

occurred as 32.5 cents subject to per dollar in respect of 37000. Net taxable amount is calculated

as $13887.2.

e) Violin

Case Scenario: For this situation, client is an authority of musical instruments and is

liable of a few violins. On 1 May, 2018 customer has sold one of her violins for 12000 dollars to

her neighbour which was attained as on 1 June 1999 value of 5500 dollars.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

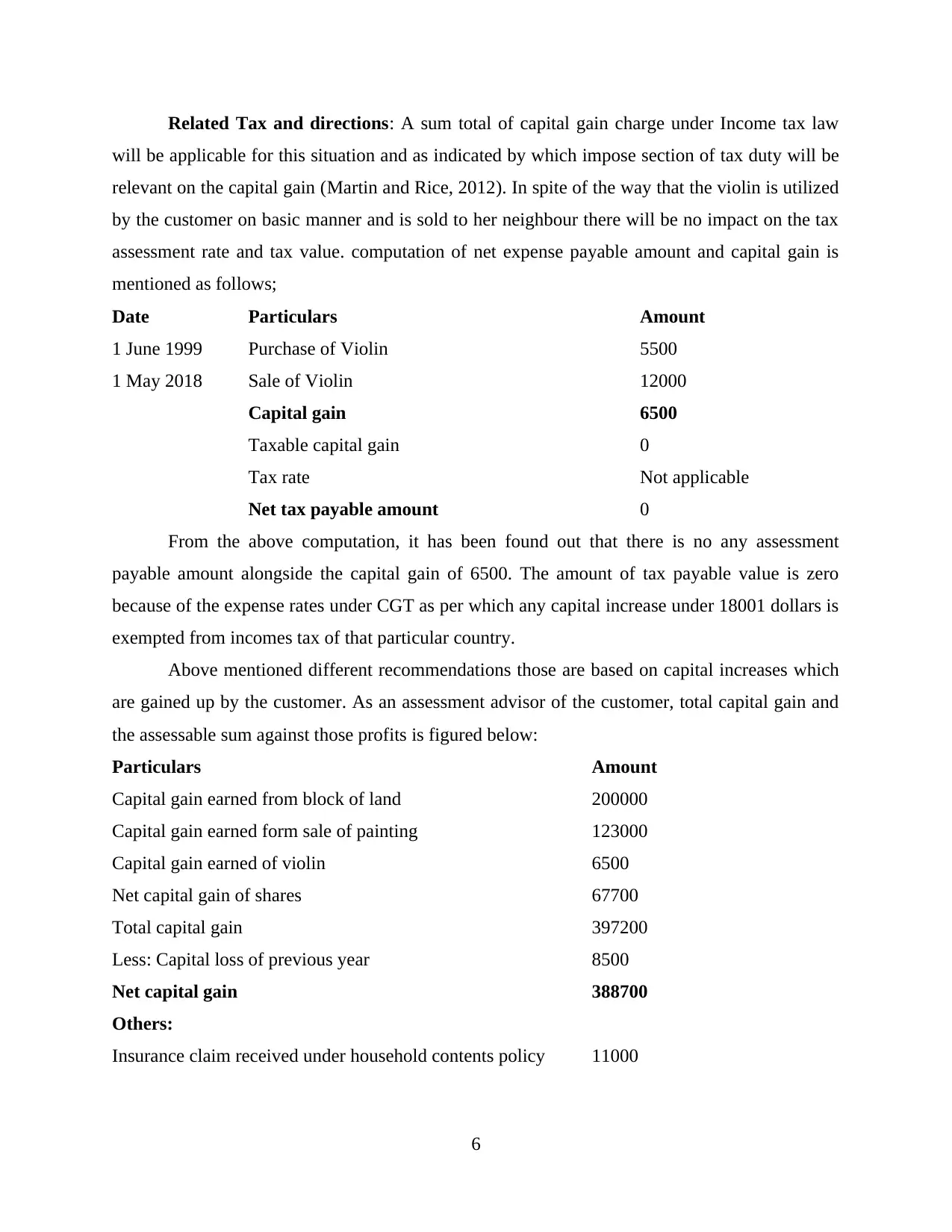

Related Tax and directions: A sum total of capital gain charge under Income tax law

will be applicable for this situation and as indicated by which impose section of tax duty will be

relevant on the capital gain (Martin and Rice, 2012). In spite of the way that the violin is utilized

by the customer on basic manner and is sold to her neighbour there will be no impact on the tax

assessment rate and tax value. computation of net expense payable amount and capital gain is

mentioned as follows;

Date Particulars Amount

1 June 1999 Purchase of Violin 5500

1 May 2018 Sale of Violin 12000

Capital gain 6500

Taxable capital gain 0

Tax rate Not applicable

Net tax payable amount 0

From the above computation, it has been found out that there is no any assessment

payable amount alongside the capital gain of 6500. The amount of tax payable value is zero

because of the expense rates under CGT as per which any capital increase under 18001 dollars is

exempted from incomes tax of that particular country.

Above mentioned different recommendations those are based on capital increases which

are gained up by the customer. As an assessment advisor of the customer, total capital gain and

the assessable sum against those profits is figured below:

Particulars Amount

Capital gain earned from block of land 200000

Capital gain earned form sale of painting 123000

Capital gain earned of violin 6500

Net capital gain of shares 67700

Total capital gain 397200

Less: Capital loss of previous year 8500

Net capital gain 388700

Others:

Insurance claim received under household contents policy 11000

6

will be applicable for this situation and as indicated by which impose section of tax duty will be

relevant on the capital gain (Martin and Rice, 2012). In spite of the way that the violin is utilized

by the customer on basic manner and is sold to her neighbour there will be no impact on the tax

assessment rate and tax value. computation of net expense payable amount and capital gain is

mentioned as follows;

Date Particulars Amount

1 June 1999 Purchase of Violin 5500

1 May 2018 Sale of Violin 12000

Capital gain 6500

Taxable capital gain 0

Tax rate Not applicable

Net tax payable amount 0

From the above computation, it has been found out that there is no any assessment

payable amount alongside the capital gain of 6500. The amount of tax payable value is zero

because of the expense rates under CGT as per which any capital increase under 18001 dollars is

exempted from incomes tax of that particular country.

Above mentioned different recommendations those are based on capital increases which

are gained up by the customer. As an assessment advisor of the customer, total capital gain and

the assessable sum against those profits is figured below:

Particulars Amount

Capital gain earned from block of land 200000

Capital gain earned form sale of painting 123000

Capital gain earned of violin 6500

Net capital gain of shares 67700

Total capital gain 397200

Less: Capital loss of previous year 8500

Net capital gain 388700

Others:

Insurance claim received under household contents policy 11000

6

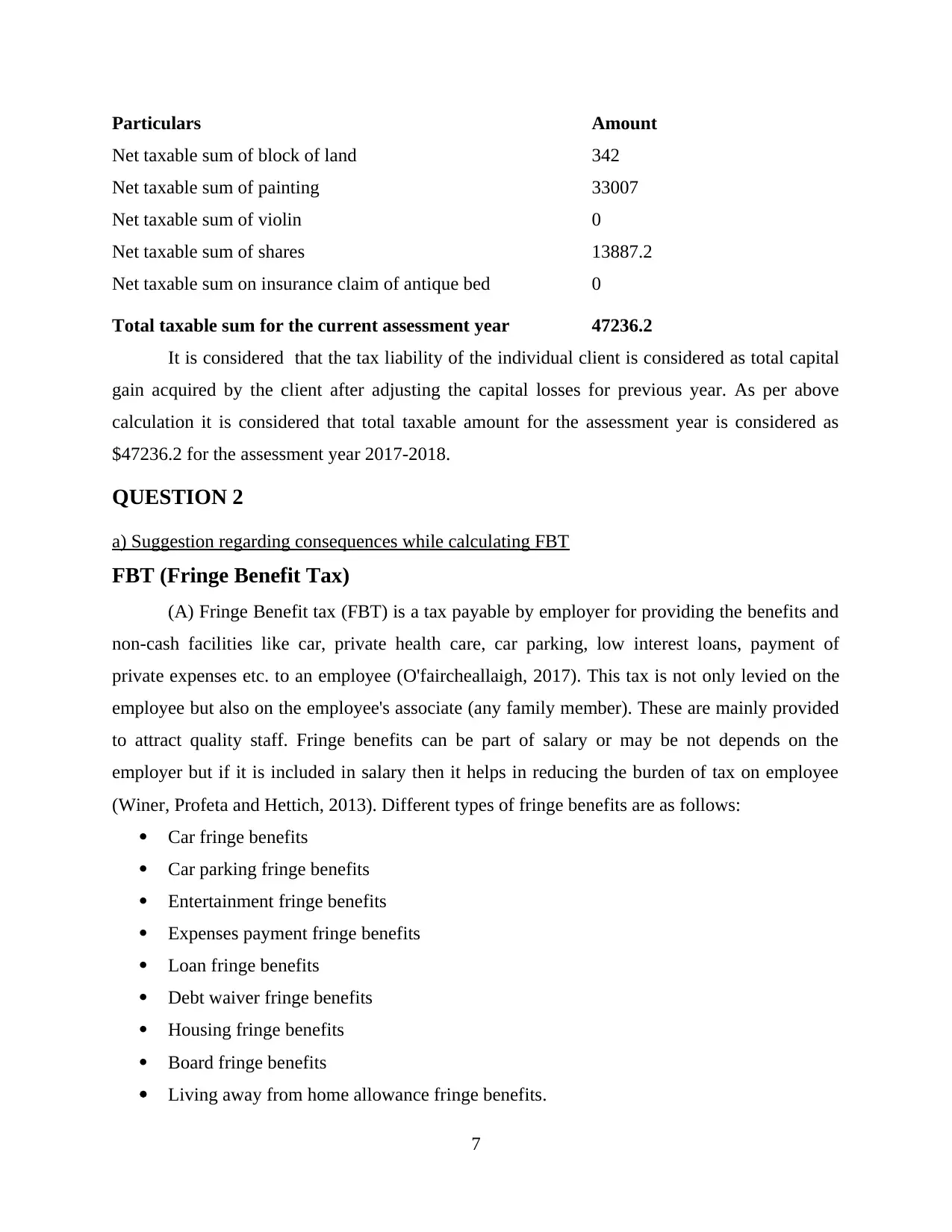

Particulars Amount

Net taxable sum of block of land 342

Net taxable sum of painting 33007

Net taxable sum of violin 0

Net taxable sum of shares 13887.2

Net taxable sum on insurance claim of antique bed 0

Total taxable sum for the current assessment year 47236.2

It is considered that the tax liability of the individual client is considered as total capital

gain acquired by the client after adjusting the capital losses for previous year. As per above

calculation it is considered that total taxable amount for the assessment year is considered as

$47236.2 for the assessment year 2017-2018.

QUESTION 2

a) Suggestion regarding consequences while calculating FBT

FBT (Fringe Benefit Tax)

(A) Fringe Benefit tax (FBT) is a tax payable by employer for providing the benefits and

non-cash facilities like car, private health care, car parking, low interest loans, payment of

private expenses etc. to an employee (O'faircheallaigh, 2017). This tax is not only levied on the

employee but also on the employee's associate (any family member). These are mainly provided

to attract quality staff. Fringe benefits can be part of salary or may be not depends on the

employer but if it is included in salary then it helps in reducing the burden of tax on employee

(Winer, Profeta and Hettich, 2013). Different types of fringe benefits are as follows:

Car fringe benefits

Car parking fringe benefits

Entertainment fringe benefits

Expenses payment fringe benefits

Loan fringe benefits

Debt waiver fringe benefits

Housing fringe benefits

Board fringe benefits

Living away from home allowance fringe benefits.

7

Net taxable sum of block of land 342

Net taxable sum of painting 33007

Net taxable sum of violin 0

Net taxable sum of shares 13887.2

Net taxable sum on insurance claim of antique bed 0

Total taxable sum for the current assessment year 47236.2

It is considered that the tax liability of the individual client is considered as total capital

gain acquired by the client after adjusting the capital losses for previous year. As per above

calculation it is considered that total taxable amount for the assessment year is considered as

$47236.2 for the assessment year 2017-2018.

QUESTION 2

a) Suggestion regarding consequences while calculating FBT

FBT (Fringe Benefit Tax)

(A) Fringe Benefit tax (FBT) is a tax payable by employer for providing the benefits and

non-cash facilities like car, private health care, car parking, low interest loans, payment of

private expenses etc. to an employee (O'faircheallaigh, 2017). This tax is not only levied on the

employee but also on the employee's associate (any family member). These are mainly provided

to attract quality staff. Fringe benefits can be part of salary or may be not depends on the

employer but if it is included in salary then it helps in reducing the burden of tax on employee

(Winer, Profeta and Hettich, 2013). Different types of fringe benefits are as follows:

Car fringe benefits

Car parking fringe benefits

Entertainment fringe benefits

Expenses payment fringe benefits

Loan fringe benefits

Debt waiver fringe benefits

Housing fringe benefits

Board fringe benefits

Living away from home allowance fringe benefits.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

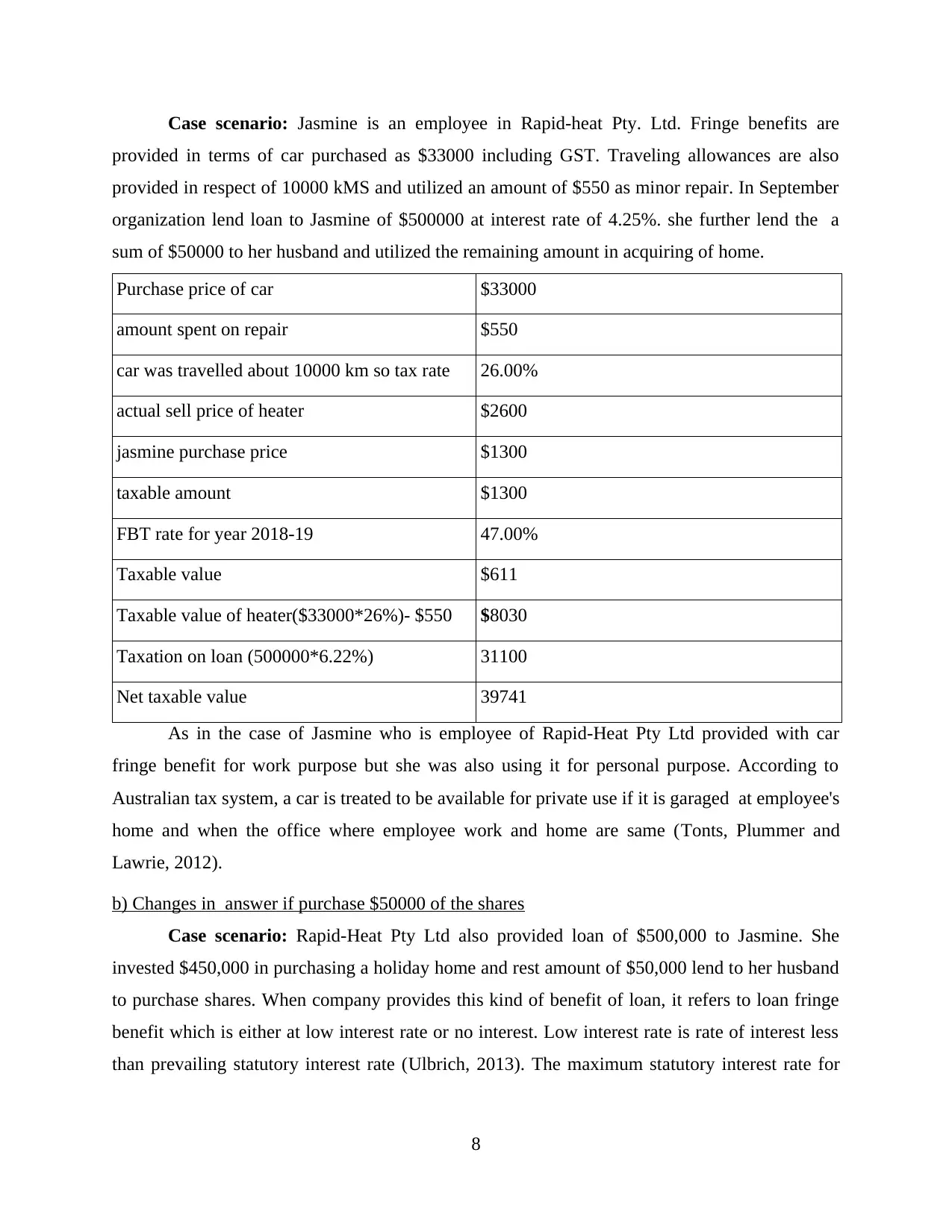

Case scenario: Jasmine is an employee in Rapid-heat Pty. Ltd. Fringe benefits are

provided in terms of car purchased as $33000 including GST. Traveling allowances are also

provided in respect of 10000 kMS and utilized an amount of $550 as minor repair. In September

organization lend loan to Jasmine of $500000 at interest rate of 4.25%. she further lend the a

sum of $50000 to her husband and utilized the remaining amount in acquiring of home.

Purchase price of car $33000

amount spent on repair $550

car was travelled about 10000 km so tax rate 26.00%

actual sell price of heater $2600

jasmine purchase price $1300

taxable amount $1300

FBT rate for year 2018-19 47.00%

Taxable value $611

Taxable value of heater($33000*26%)- $550 $8030

Taxation on loan (500000*6.22%) 31100

Net taxable value 39741

As in the case of Jasmine who is employee of Rapid-Heat Pty Ltd provided with car

fringe benefit for work purpose but she was also using it for personal purpose. According to

Australian tax system, a car is treated to be available for private use if it is garaged at employee's

home and when the office where employee work and home are same (Tonts, Plummer and

Lawrie, 2012).

b) Changes in answer if purchase $50000 of the shares

Case scenario: Rapid-Heat Pty Ltd also provided loan of $500,000 to Jasmine. She

invested $450,000 in purchasing a holiday home and rest amount of $50,000 lend to her husband

to purchase shares. When company provides this kind of benefit of loan, it refers to loan fringe

benefit which is either at low interest rate or no interest. Low interest rate is rate of interest less

than prevailing statutory interest rate (Ulbrich, 2013). The maximum statutory interest rate for

8

provided in terms of car purchased as $33000 including GST. Traveling allowances are also

provided in respect of 10000 kMS and utilized an amount of $550 as minor repair. In September

organization lend loan to Jasmine of $500000 at interest rate of 4.25%. she further lend the a

sum of $50000 to her husband and utilized the remaining amount in acquiring of home.

Purchase price of car $33000

amount spent on repair $550

car was travelled about 10000 km so tax rate 26.00%

actual sell price of heater $2600

jasmine purchase price $1300

taxable amount $1300

FBT rate for year 2018-19 47.00%

Taxable value $611

Taxable value of heater($33000*26%)- $550 $8030

Taxation on loan (500000*6.22%) 31100

Net taxable value 39741

As in the case of Jasmine who is employee of Rapid-Heat Pty Ltd provided with car

fringe benefit for work purpose but she was also using it for personal purpose. According to

Australian tax system, a car is treated to be available for private use if it is garaged at employee's

home and when the office where employee work and home are same (Tonts, Plummer and

Lawrie, 2012).

b) Changes in answer if purchase $50000 of the shares

Case scenario: Rapid-Heat Pty Ltd also provided loan of $500,000 to Jasmine. She

invested $450,000 in purchasing a holiday home and rest amount of $50,000 lend to her husband

to purchase shares. When company provides this kind of benefit of loan, it refers to loan fringe

benefit which is either at low interest rate or no interest. Low interest rate is rate of interest less

than prevailing statutory interest rate (Ulbrich, 2013). The maximum statutory interest rate for

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

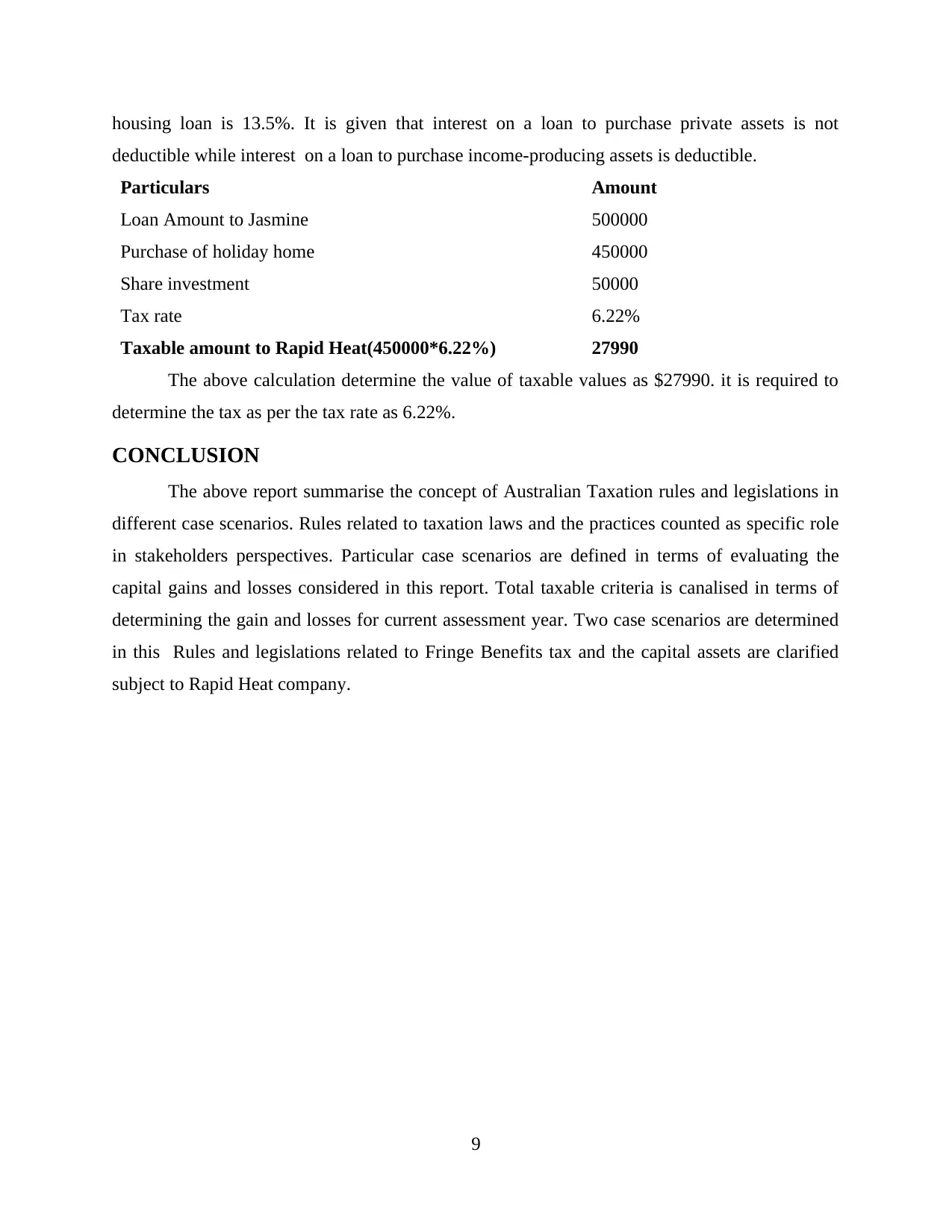

housing loan is 13.5%. It is given that interest on a loan to purchase private assets is not

deductible while interest on a loan to purchase income-producing assets is deductible.

Particulars Amount

Loan Amount to Jasmine 500000

Purchase of holiday home 450000

Share investment 50000

Tax rate 6.22%

Taxable amount to Rapid Heat(450000*6.22%) 27990

The above calculation determine the value of taxable values as $27990. it is required to

determine the tax as per the tax rate as 6.22%.

CONCLUSION

The above report summarise the concept of Australian Taxation rules and legislations in

different case scenarios. Rules related to taxation laws and the practices counted as specific role

in stakeholders perspectives. Particular case scenarios are defined in terms of evaluating the

capital gains and losses considered in this report. Total taxable criteria is canalised in terms of

determining the gain and losses for current assessment year. Two case scenarios are determined

in this Rules and legislations related to Fringe Benefits tax and the capital assets are clarified

subject to Rapid Heat company.

9

deductible while interest on a loan to purchase income-producing assets is deductible.

Particulars Amount

Loan Amount to Jasmine 500000

Purchase of holiday home 450000

Share investment 50000

Tax rate 6.22%

Taxable amount to Rapid Heat(450000*6.22%) 27990

The above calculation determine the value of taxable values as $27990. it is required to

determine the tax as per the tax rate as 6.22%.

CONCLUSION

The above report summarise the concept of Australian Taxation rules and legislations in

different case scenarios. Rules related to taxation laws and the practices counted as specific role

in stakeholders perspectives. Particular case scenarios are defined in terms of evaluating the

capital gains and losses considered in this report. Total taxable criteria is canalised in terms of

determining the gain and losses for current assessment year. Two case scenarios are determined

in this Rules and legislations related to Fringe Benefits tax and the capital assets are clarified

subject to Rapid Heat company.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.