Detailed Analysis of McDonald v FC of T Case - BBAL501 Taxation Law

VerifiedAdded on 2023/06/10

|9

|679

|262

Report

AI Summary

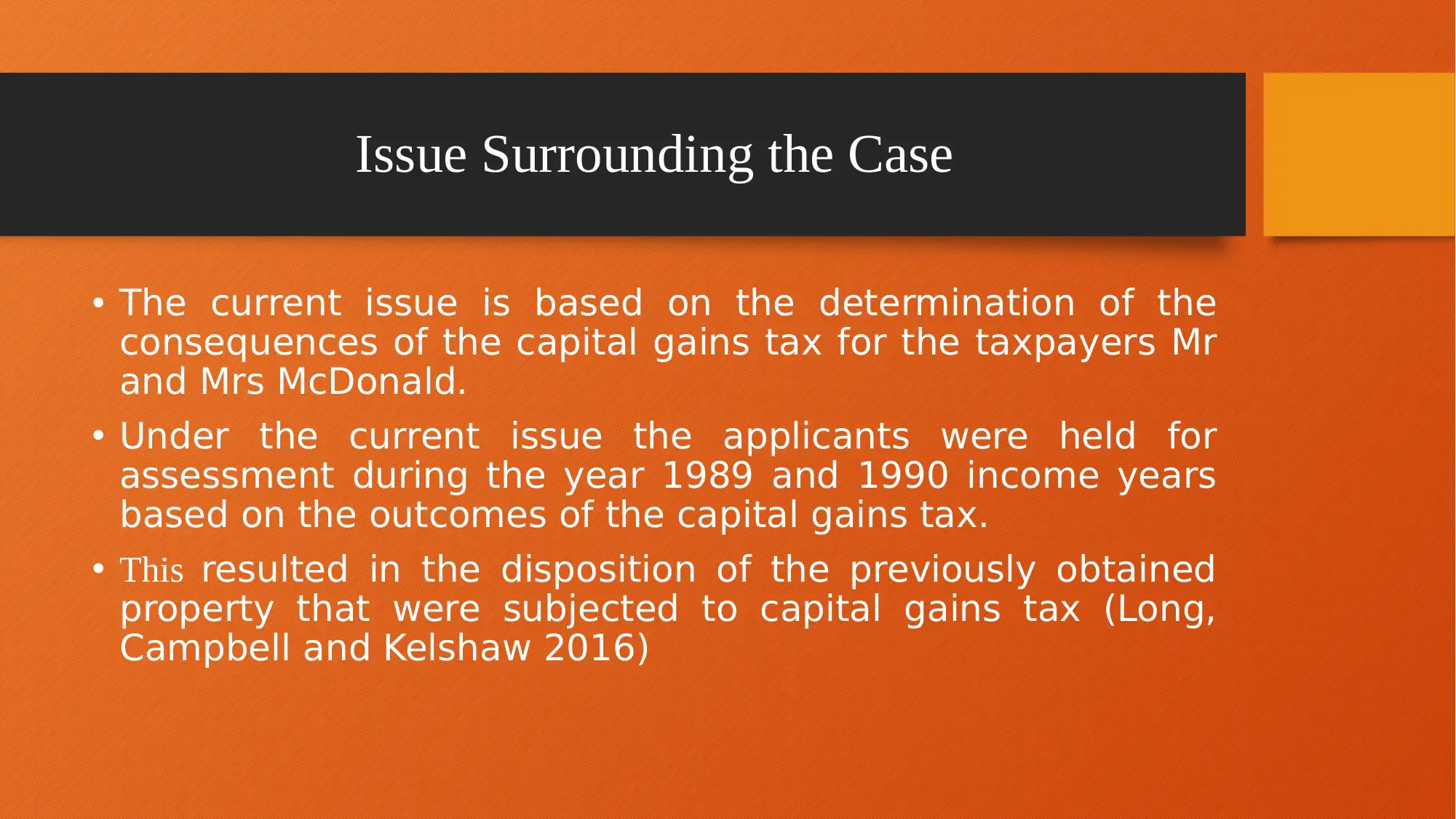

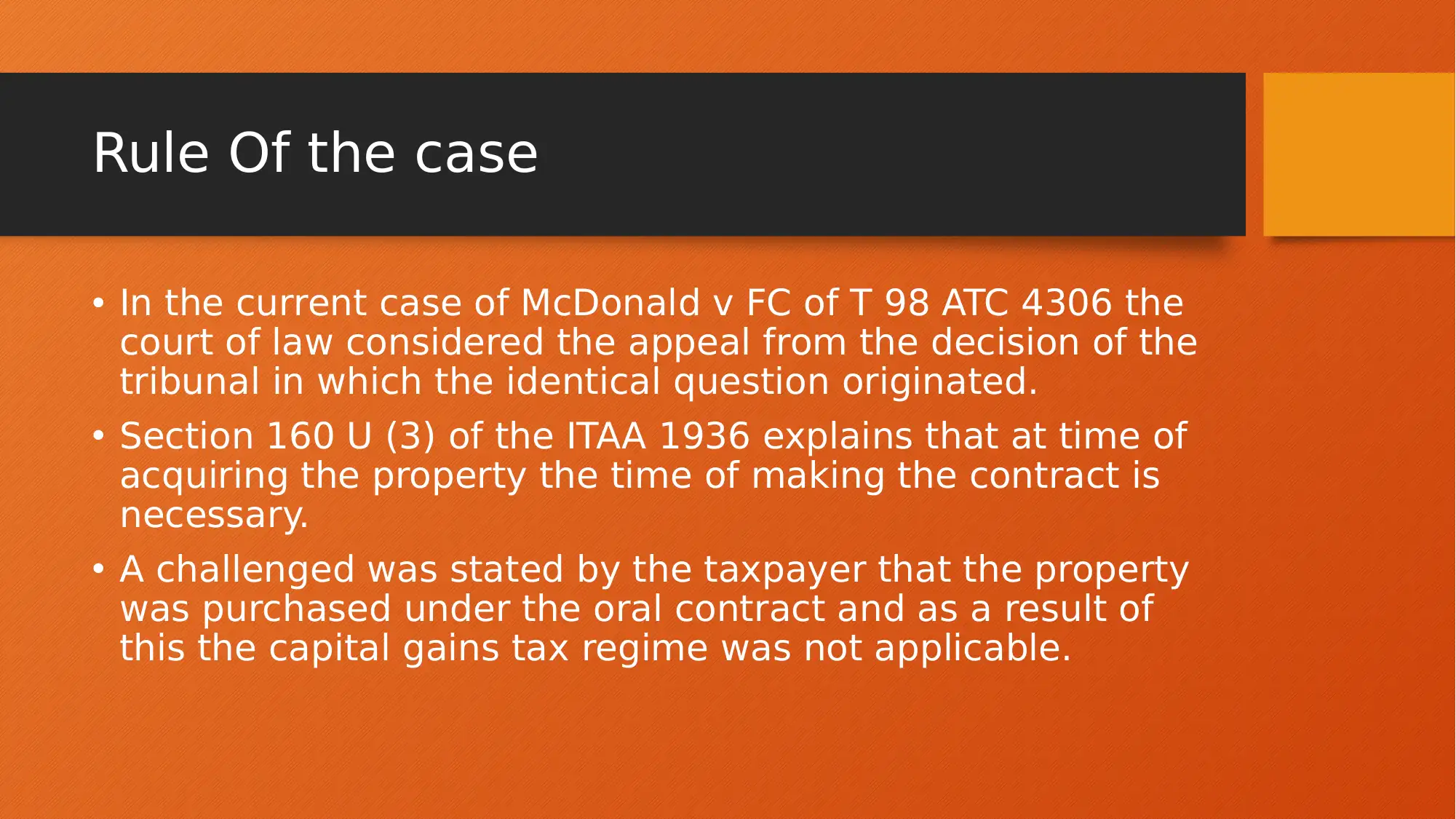

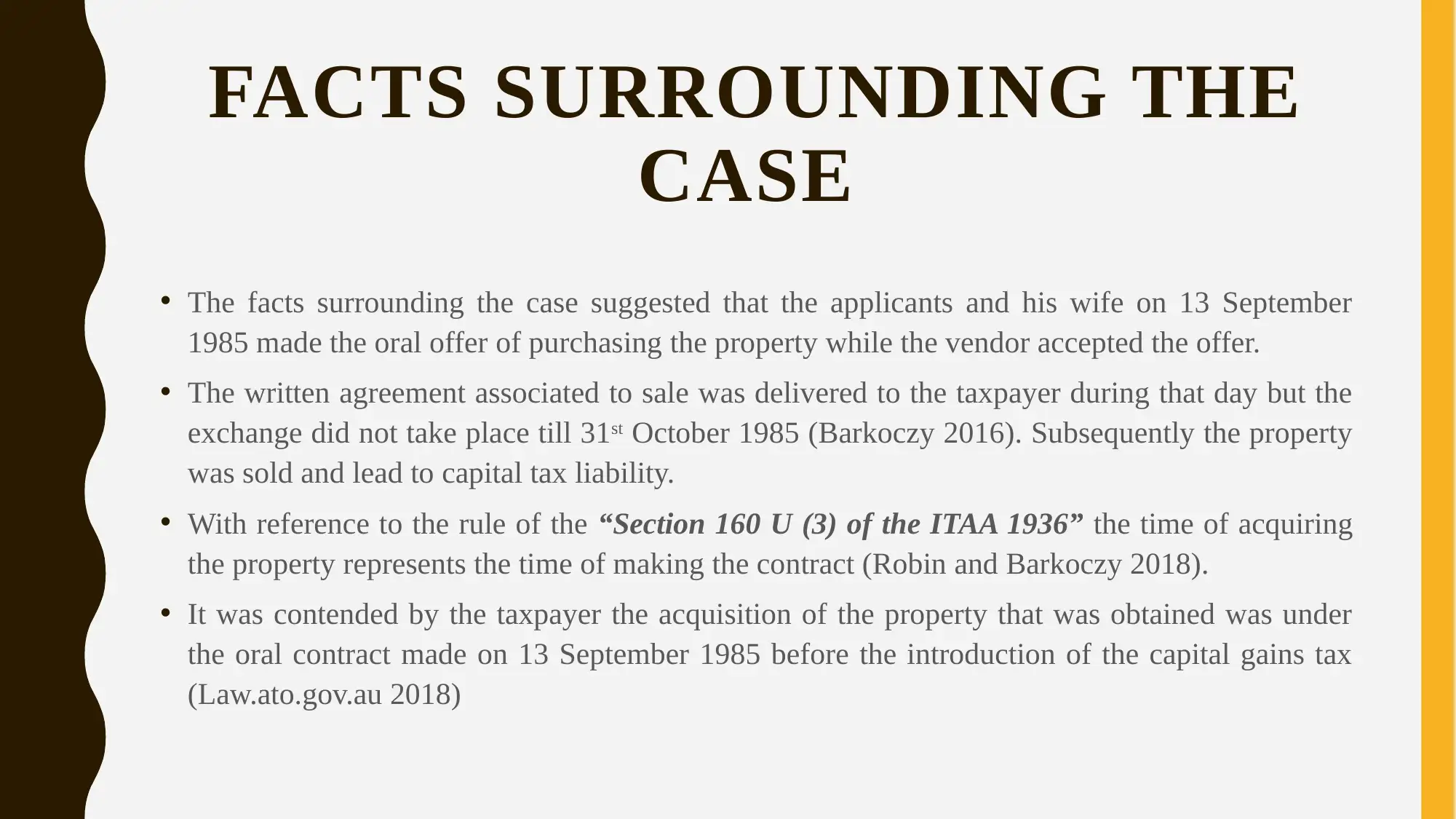

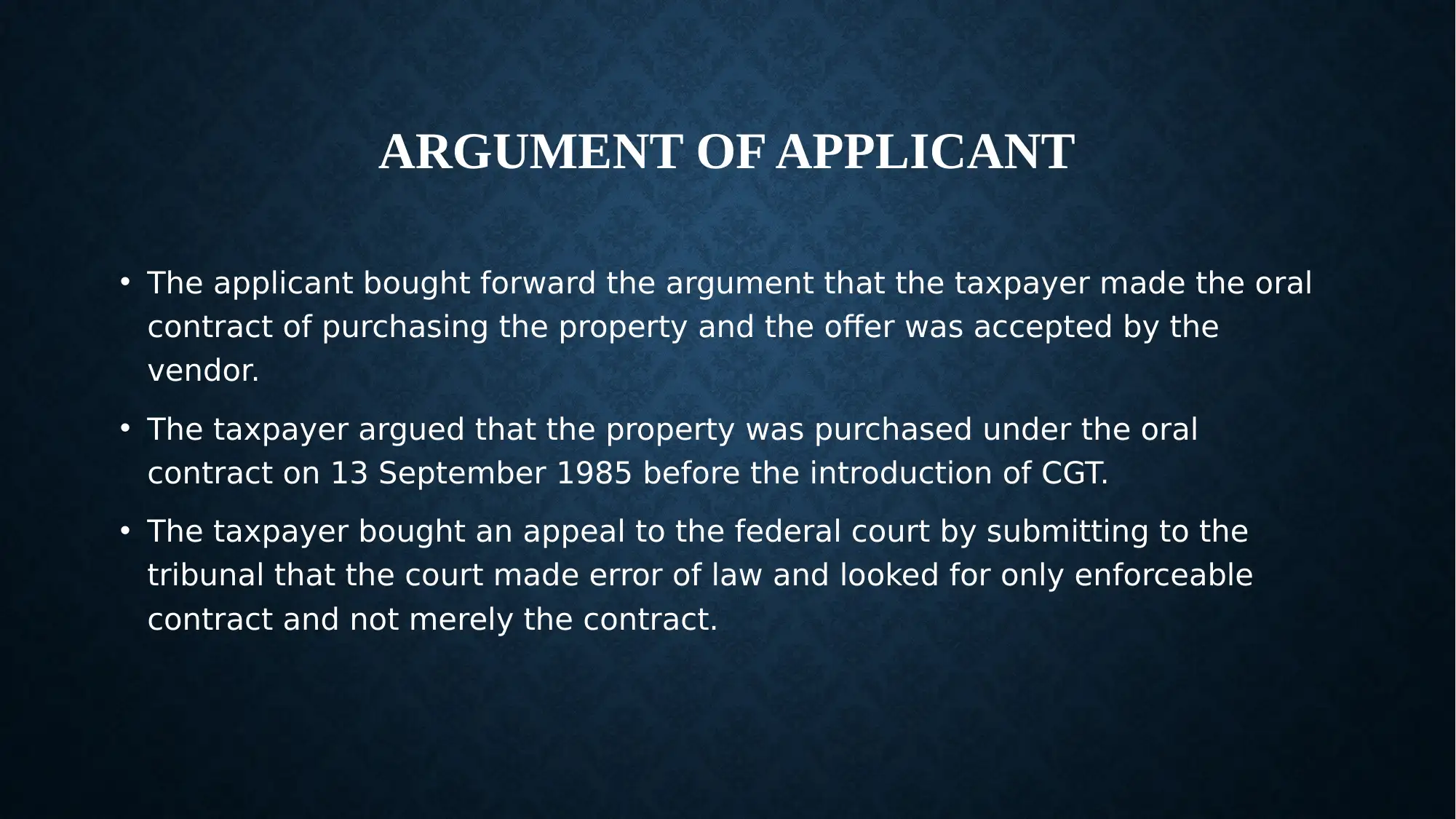

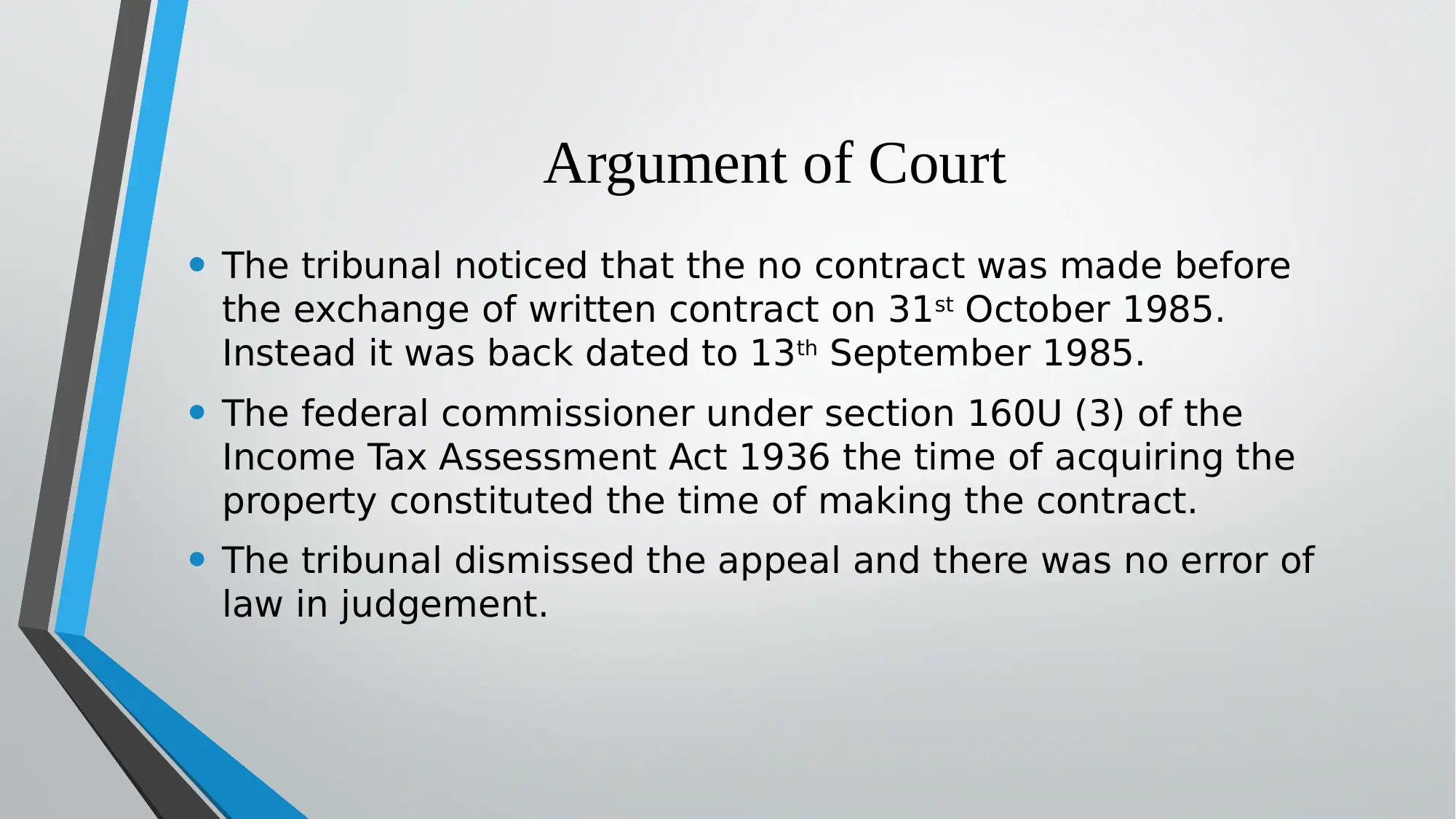

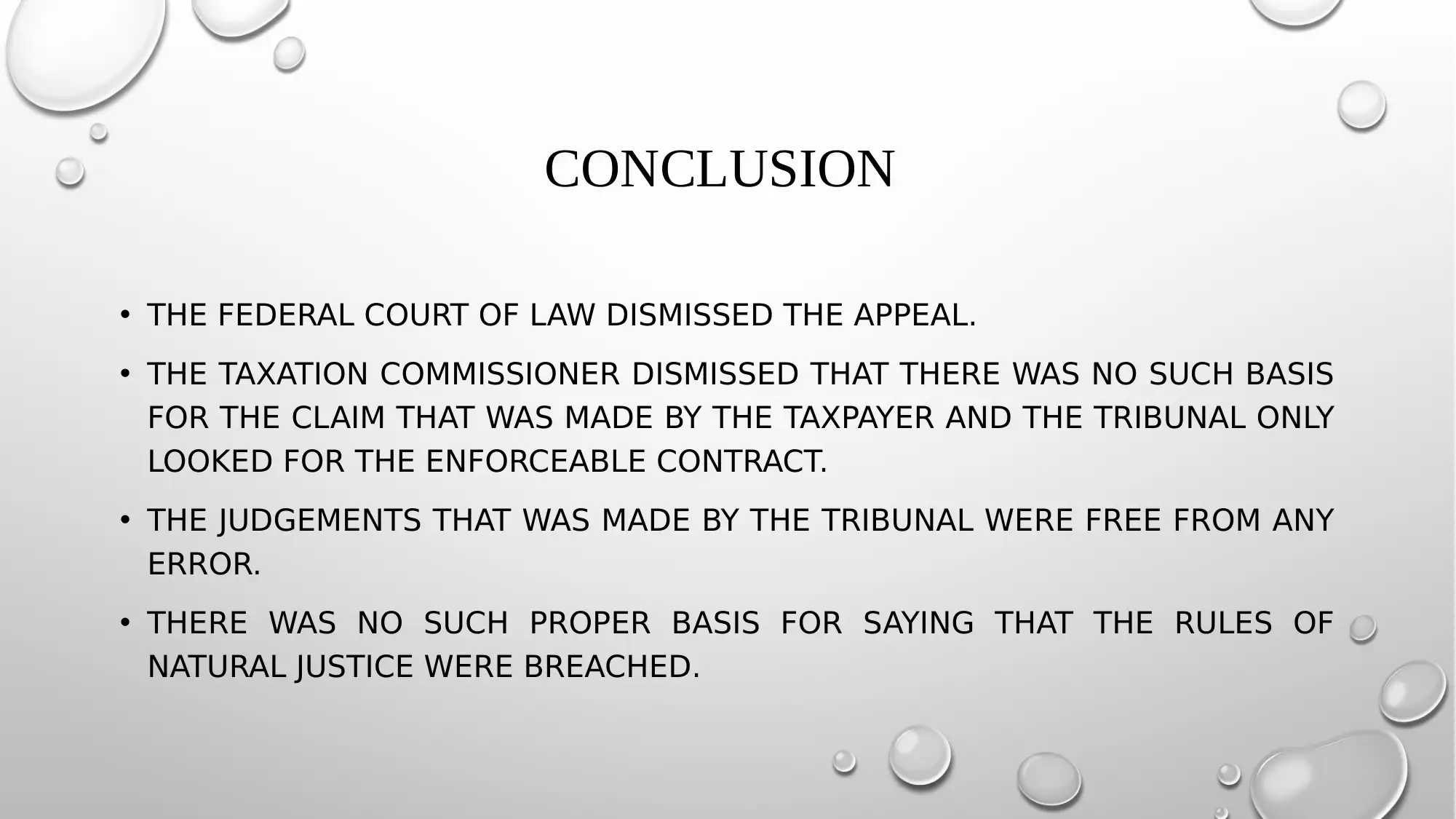

This report provides a comprehensive analysis of the McDonald v FC of T case, focusing on the central issue of capital gains tax. The case revolves around the taxpayers, Mr. and Mrs. McDonald, and their liability for capital gains tax following the disposition of a property. The core legal question concerns the interpretation of Section 160U (3) of the ITAA 1936, specifically addressing when an asset is considered acquired. The taxpayer argued an oral contract predated the tax introduction, while the court considered the written contract's exchange date. The report examines the arguments presented by both the applicant and the court, including the tribunal's dismissal of the appeal and the Federal Court's affirmation. The conclusion underscores the dismissal of the appeal, the court's adherence to the enforceable contract, and the absence of any legal errors in the tribunal's judgement. The report also references key legal sources and precedents relevant to the case.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.