BFA714 Taxation Law Assignment: Omega Pty Ltd Case Study

VerifiedAdded on 2022/09/28

|7

|847

|28

Homework Assignment

AI Summary

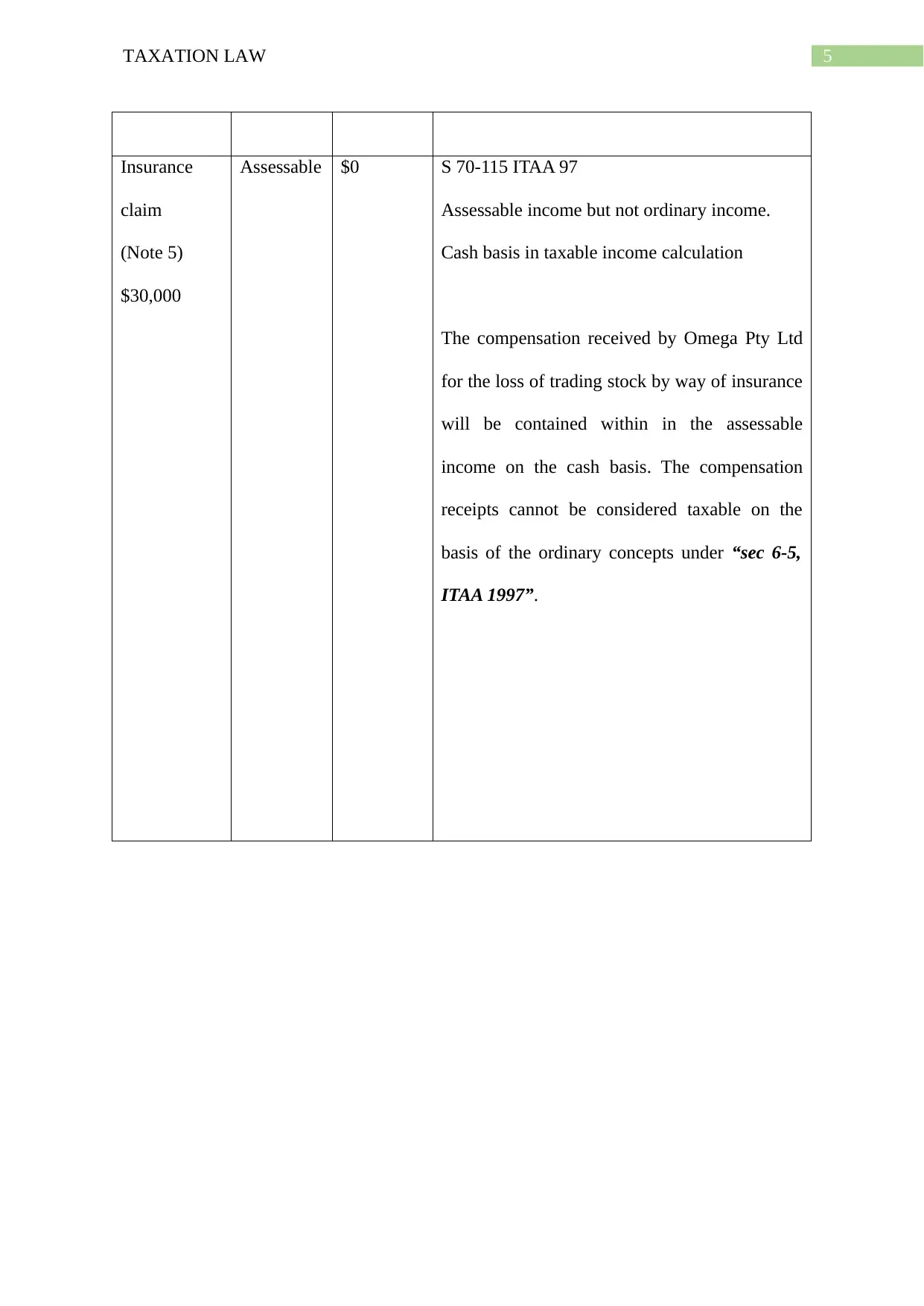

This assignment analyzes the taxation law implications for Omega Pty Ltd, focusing on the financial year ending June 30, 2019. It addresses whether Omega qualifies as a small business entity based on its 2017/18 turnover of $9 million, which is below the $10 million threshold. The assignment then examines various income items, including sales revenue, interest, rent, royalties, and an insurance claim, determining whether each is assessable and calculating the assessable amount. It references relevant sections of the Income Tax Assessment Act 1997 (ITAA 97) and other rulings to justify the tax treatment of each income component. The analysis considers cash basis accounting where applicable and explains the rationale behind the assessability or non-assessability of each item, along with the applicable laws and regulations. The assignment provides a comprehensive overview of how different types of income are treated for taxation purposes, specifically within the context of an Australian small business entity.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.