HI6028 Taxation Law T3 2018: Partnership Income and Fringe Benefit

VerifiedAdded on 2023/04/23

|12

|2646

|477

Report

AI Summary

This report provides a comprehensive analysis of taxation law, focusing on the determination of partnership income and the implications of fringe benefits. It examines the case of Daniel and Olivia Smith's partnership, calculating their net income for the year ended June 30, 2017, based on business sales, debtor payments, and eligible deductions such as electricity bills, council rates, and repair expenses. The report also addresses fringe benefits, specifically the payment of an employee's child's school fees and the provision of housing, discussing the relevant sections of the FBTAA 1986 and ITAA 1997 to determine taxable values and employer liabilities. Desklib offers numerous resources for students, including past papers and solved assignments.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1..................................................................................................................2

Issues:.....................................................................................................................................2

Rule:.......................................................................................................................................2

Application:............................................................................................................................3

Conclusion:............................................................................................................................7

Answer to questions 2:...............................................................................................................7

Issues:.....................................................................................................................................7

Rule:.......................................................................................................................................7

Application:............................................................................................................................8

Conclusion:............................................................................................................................9

References:...............................................................................................................................10

Table of Contents

Answer to question 1..................................................................................................................2

Issues:.....................................................................................................................................2

Rule:.......................................................................................................................................2

Application:............................................................................................................................3

Conclusion:............................................................................................................................7

Answer to questions 2:...............................................................................................................7

Issues:.....................................................................................................................................7

Rule:.......................................................................................................................................7

Application:............................................................................................................................8

Conclusion:............................................................................................................................9

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1

Issues:

The expenses and receipts are two main key elements which are considered in case

study to discuss about the net partnership income under “section 995-1 of the ITAA 1997”.

Rule:

According to “division 5 of the ITAA 1936” income from a partnership business is

nothing but the amount gained from the assessable income deducting the permissible

expenses. As per the “Section 92 of the ITAA 1997” the partners who are liable in paying tax

get the loss as well as profit distributed among themselves in terms of distribution (Willis et

al. 2014). According to the “section 995-1 (1)” continuation of a business with a common

objective of earning profit throughout the income years is called partnership.

Ordinary income is not mentioned under the taxation acts. As per “section 6-5, ITAA

1997” ordinary income is involved within the assessable income of the taxpayer. “Scott v

FCT 14 ATD 286” mentions income is declared as word of art and all the gains throughout

the income year is involved in it (Willis 2014). According to the ordinary income concepts,

the receipts are considered as income until the statute is indicating that the income is not

under the parlance.

As held in “section 8-1, ITAA 1997” there are two positive limbs for saving the

taxpayers from the losses incurred while continuing the business or for any other expense

those are involved into the business while involving their taxable incomes (Lind 2015).

Subsequently, the negative limb of “section 8-1, ITAA 1997” is, this section restricts the tax

payer in deducing any losses incurred during the involvement of taxable incomes into the

business. Along with this, “section 8-1, ITAA 1997” also does not allows any domestic,

capital and private losses while calculating the deductions of income tax (Laing 2015).

Answer to question 1

Issues:

The expenses and receipts are two main key elements which are considered in case

study to discuss about the net partnership income under “section 995-1 of the ITAA 1997”.

Rule:

According to “division 5 of the ITAA 1936” income from a partnership business is

nothing but the amount gained from the assessable income deducting the permissible

expenses. As per the “Section 92 of the ITAA 1997” the partners who are liable in paying tax

get the loss as well as profit distributed among themselves in terms of distribution (Willis et

al. 2014). According to the “section 995-1 (1)” continuation of a business with a common

objective of earning profit throughout the income years is called partnership.

Ordinary income is not mentioned under the taxation acts. As per “section 6-5, ITAA

1997” ordinary income is involved within the assessable income of the taxpayer. “Scott v

FCT 14 ATD 286” mentions income is declared as word of art and all the gains throughout

the income year is involved in it (Willis 2014). According to the ordinary income concepts,

the receipts are considered as income until the statute is indicating that the income is not

under the parlance.

As held in “section 8-1, ITAA 1997” there are two positive limbs for saving the

taxpayers from the losses incurred while continuing the business or for any other expense

those are involved into the business while involving their taxable incomes (Lind 2015).

Subsequently, the negative limb of “section 8-1, ITAA 1997” is, this section restricts the tax

payer in deducing any losses incurred during the involvement of taxable incomes into the

business. Along with this, “section 8-1, ITAA 1997” also does not allows any domestic,

capital and private losses while calculating the deductions of income tax (Laing 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Agreeing to the concepts of “section 25-10 of the ITAA 1997”, repairs are considered

as some work to be done on some specific sets of machineries or plant and premises. A repair

can be defined as the replacement of parts of any specific entity that is not in situation to

provide profit in the business (Kwall 2019). According to the section 25-10 there are certain

maintenances such painting of any plant for maintaining the condition of the plant in order to

make it productive.

Likewise, under “section 25-10” there are certain replacements such as locks, exhaust

fans are considered as some permanent fixes those are making the area more productive or

keeping the area productive as it was, are considered as some deductible repairs

(Schwidetzky 2017). However, if the repair is not increasing the efficiency of the unit then it

will not be considered as a permissible repair into that particular part. This shows lack of

improvement through that particular repair.

According to the Australian taxation office, any business is allowed to get instant

payment through a write- off if the cost discussed is lesser than $20,000.

Application:

The case study of Olivia and Daniel is highlighting that they are continuing their

business with a common objective of gaining profit throughout the income year under

“section 995-1 (1) of the ITAA 1997”. The determination of net profit or loss is discussed

according to the section 90. In contrast with this discussion, the partnership of Daniel and

Olivia gained receipts from the business cash sales and debtors payments on 30th June 2017.

According to the judgement made in “Scott v FCT 14 ATD 286” the received amount from

these above mentioned aspects are treated as the business receipts under a partnership.

According to “section 6-5, ITAA 1997” this business receipts are determining the net income

for Daniel and Olivia.

Agreeing to the concepts of “section 25-10 of the ITAA 1997”, repairs are considered

as some work to be done on some specific sets of machineries or plant and premises. A repair

can be defined as the replacement of parts of any specific entity that is not in situation to

provide profit in the business (Kwall 2019). According to the section 25-10 there are certain

maintenances such painting of any plant for maintaining the condition of the plant in order to

make it productive.

Likewise, under “section 25-10” there are certain replacements such as locks, exhaust

fans are considered as some permanent fixes those are making the area more productive or

keeping the area productive as it was, are considered as some deductible repairs

(Schwidetzky 2017). However, if the repair is not increasing the efficiency of the unit then it

will not be considered as a permissible repair into that particular part. This shows lack of

improvement through that particular repair.

According to the Australian taxation office, any business is allowed to get instant

payment through a write- off if the cost discussed is lesser than $20,000.

Application:

The case study of Olivia and Daniel is highlighting that they are continuing their

business with a common objective of gaining profit throughout the income year under

“section 995-1 (1) of the ITAA 1997”. The determination of net profit or loss is discussed

according to the section 90. In contrast with this discussion, the partnership of Daniel and

Olivia gained receipts from the business cash sales and debtors payments on 30th June 2017.

According to the judgement made in “Scott v FCT 14 ATD 286” the received amount from

these above mentioned aspects are treated as the business receipts under a partnership.

According to “section 6-5, ITAA 1997” this business receipts are determining the net income

for Daniel and Olivia.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Daniel and Olivia are also liable for drawing cash amount $5,600 for private purpose

and purchase of items from bottle shop. According to some of their drawings are involving

their net income into the income tax deductions. According to “section 8-1 (2), ITAA 1997”,

as they have drawn money for private reasons, they have indulge their net come for income

deduction.

Apart from these discussions, Olivia and Daniel also included repairs for shop

painting and motor replacement of a refrigerator. Underneath “section 25-10” Olivia and

Daniel has involved their income into taxable deductions as they have applied a permanent

fix to the refrigerator and also for the painting of business premises.

The business has also stated an acquisition of air- conditioner for $1200.

Henceforward, this is lower than $20,000, so they will be eligible for permissible taxable

deductions.

Daniel and Olivia are also liable for drawing cash amount $5,600 for private purpose

and purchase of items from bottle shop. According to some of their drawings are involving

their net income into the income tax deductions. According to “section 8-1 (2), ITAA 1997”,

as they have drawn money for private reasons, they have indulge their net come for income

deduction.

Apart from these discussions, Olivia and Daniel also included repairs for shop

painting and motor replacement of a refrigerator. Underneath “section 25-10” Olivia and

Daniel has involved their income into taxable deductions as they have applied a permanent

fix to the refrigerator and also for the painting of business premises.

The business has also stated an acquisition of air- conditioner for $1200.

Henceforward, this is lower than $20,000, so they will be eligible for permissible taxable

deductions.

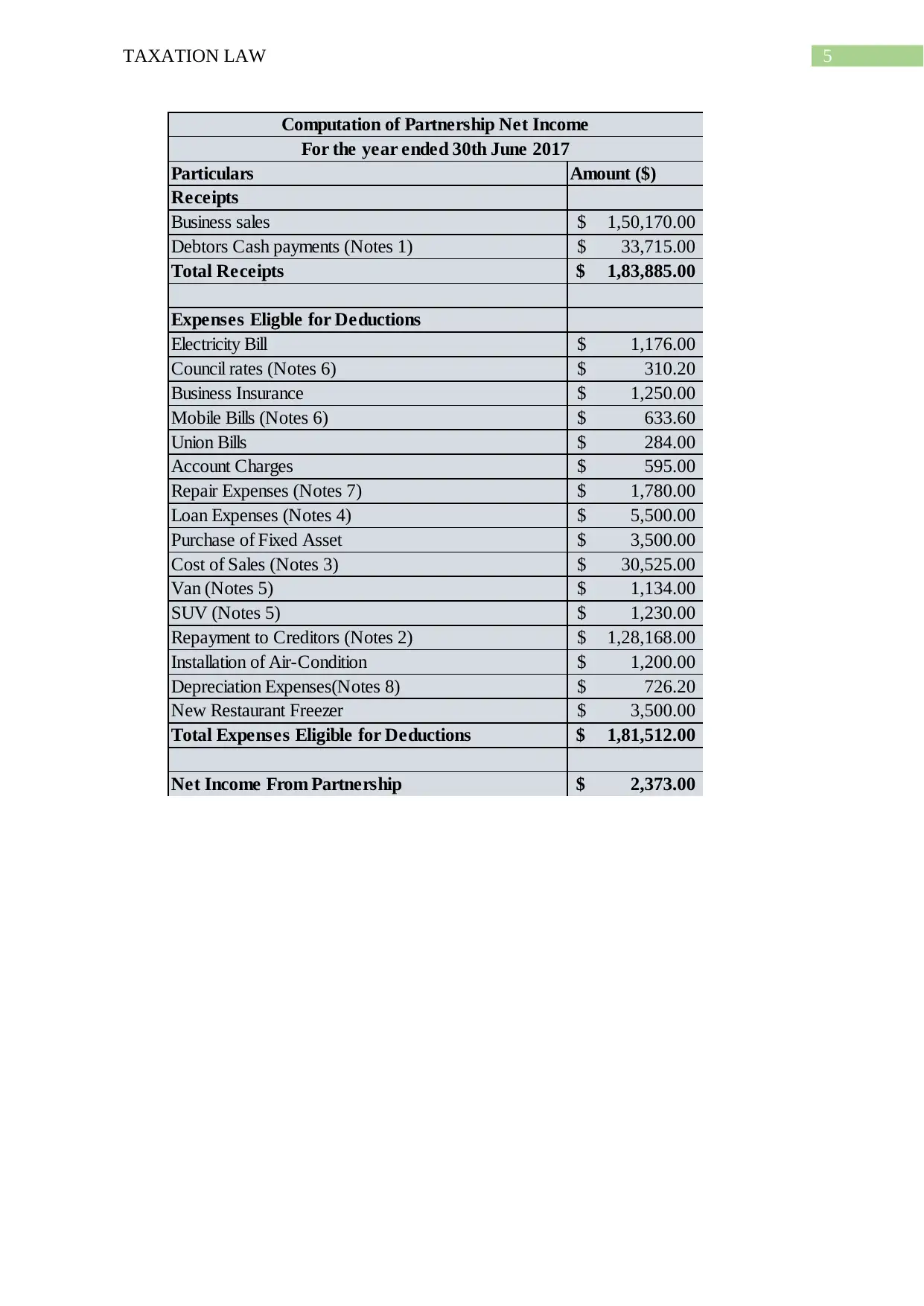

5TAXATION LAW

Particulars Amount ($)

Receipts

Business sales 1,50,170.00$

Debtors Cash payments (Notes 1) 33,715.00$

Total Receipts 1,83,885.00$

Expenses Eligble for Deductions

Electricity Bill 1,176.00$

Council rates (Notes 6) 310.20$

Business Insurance 1,250.00$

Mobile Bills (Notes 6) 633.60$

Union Bills 284.00$

Account Charges 595.00$

Repair Expenses (Notes 7) 1,780.00$

Loan Expenses (Notes 4) 5,500.00$

Purchase of Fixed Asset 3,500.00$

Cost of Sales (Notes 3) 30,525.00$

Van (Notes 5) 1,134.00$

SUV (Notes 5) 1,230.00$

Repayment to Creditors (Notes 2) 1,28,168.00$

Installation of Air-Condition 1,200.00$

Depreciation Expenses(Notes 8) 726.20$

New Restaurant Freezer 3,500.00$

Total Expenses Eligible for Deductions 1,81,512.00$

Net Income From Partnership 2,373.00$

Computation of Partnership Net Income

For the year ended 30th June 2017

Particulars Amount ($)

Receipts

Business sales 1,50,170.00$

Debtors Cash payments (Notes 1) 33,715.00$

Total Receipts 1,83,885.00$

Expenses Eligble for Deductions

Electricity Bill 1,176.00$

Council rates (Notes 6) 310.20$

Business Insurance 1,250.00$

Mobile Bills (Notes 6) 633.60$

Union Bills 284.00$

Account Charges 595.00$

Repair Expenses (Notes 7) 1,780.00$

Loan Expenses (Notes 4) 5,500.00$

Purchase of Fixed Asset 3,500.00$

Cost of Sales (Notes 3) 30,525.00$

Van (Notes 5) 1,134.00$

SUV (Notes 5) 1,230.00$

Repayment to Creditors (Notes 2) 1,28,168.00$

Installation of Air-Condition 1,200.00$

Depreciation Expenses(Notes 8) 726.20$

New Restaurant Freezer 3,500.00$

Total Expenses Eligible for Deductions 1,81,512.00$

Net Income From Partnership 2,373.00$

Computation of Partnership Net Income

For the year ended 30th June 2017

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Working Papers:

Notes 1

Debtors at 1st July 2016 3,925.00$

Debtors Cash Payments 32,800.00$

Debtors at 30th June 2017 3,010.00$

Debtors Net 33,715.00$

Notes 2

Creditors at 1st July 2016 6,500.00$

Add: Repayment to Creditors 1,28,678.00$

Less: Creditors at 30 June 2017 7,010.00$

Creditors Net 1,28,168.00$

Notes 3

Cost of Sales

Stock on 1st July 2016 9,120.00$

Add: Purchase 31,155.00$

Less: Stock on 30th June 2017 9,750.00$

Notes 4 30,525.00$

Loan Repayment

Business Loan 8,500.00$

Less: Reduction of loan 3,000.00$

Net Loan Re-Payment 5,500.00$

Notes 5

Cost of Maintainance

Van 1,260.00$

Less: Business use 90% 1,134.00$

SUV 2,050.00$

Less: Business use 60% 1,230.00$

Total cost of Maintainance 2,364.00$

Notes 6

Mobile Bills 704.00$

Less: 90% Business Use 633.60$

Electricity Expenses 1,470.00$

Less: 80% Business Use 1,176.00$

Council Rates 517.00$

Less: 60% Business Use 310.20$

Notes 7

Repairs Expenses 1,780.00$

Add: Shop painting 150.00$

Add: Motor replacement expenses 140.00$

Total Repairs 2,070.00$

Working Papers:

Notes 1

Debtors at 1st July 2016 3,925.00$

Debtors Cash Payments 32,800.00$

Debtors at 30th June 2017 3,010.00$

Debtors Net 33,715.00$

Notes 2

Creditors at 1st July 2016 6,500.00$

Add: Repayment to Creditors 1,28,678.00$

Less: Creditors at 30 June 2017 7,010.00$

Creditors Net 1,28,168.00$

Notes 3

Cost of Sales

Stock on 1st July 2016 9,120.00$

Add: Purchase 31,155.00$

Less: Stock on 30th June 2017 9,750.00$

Notes 4 30,525.00$

Loan Repayment

Business Loan 8,500.00$

Less: Reduction of loan 3,000.00$

Net Loan Re-Payment 5,500.00$

Notes 5

Cost of Maintainance

Van 1,260.00$

Less: Business use 90% 1,134.00$

SUV 2,050.00$

Less: Business use 60% 1,230.00$

Total cost of Maintainance 2,364.00$

Notes 6

Mobile Bills 704.00$

Less: 90% Business Use 633.60$

Electricity Expenses 1,470.00$

Less: 80% Business Use 1,176.00$

Council Rates 517.00$

Less: 60% Business Use 310.20$

Notes 7

Repairs Expenses 1,780.00$

Add: Shop painting 150.00$

Add: Motor replacement expenses 140.00$

Total Repairs 2,070.00$

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

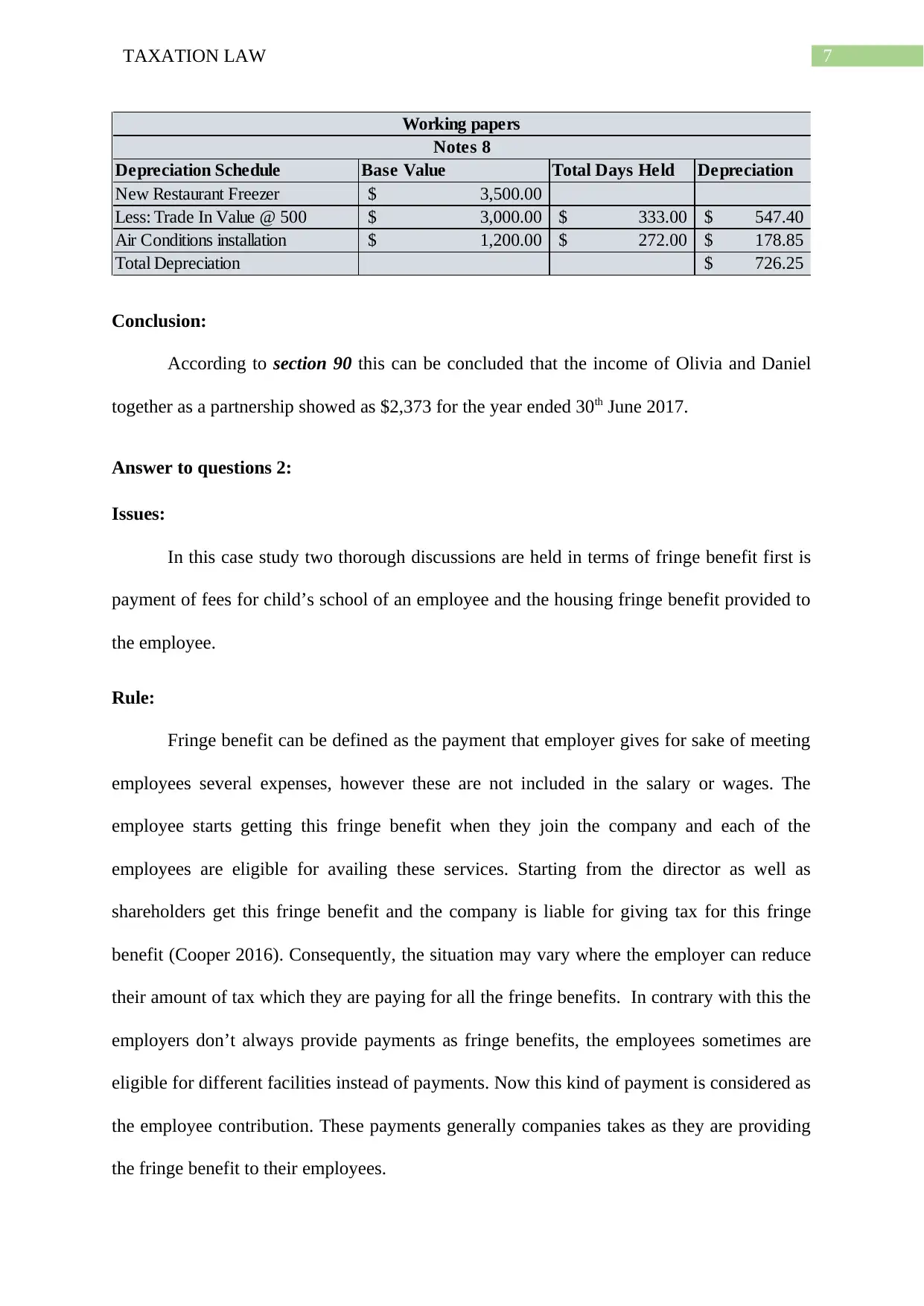

Depreciation Schedule Base Value Total Days Held Depreciation

New Restaurant Freezer 3,500.00$

Less: Trade In Value @ 500 3,000.00$ 333.00$ 547.40$

Air Conditions installation 1,200.00$ 272.00$ 178.85$

Total Depreciation 726.25$

Working papers

Notes 8

Conclusion:

According to section 90 this can be concluded that the income of Olivia and Daniel

together as a partnership showed as $2,373 for the year ended 30th June 2017.

Answer to questions 2:

Issues:

In this case study two thorough discussions are held in terms of fringe benefit first is

payment of fees for child’s school of an employee and the housing fringe benefit provided to

the employee.

Rule:

Fringe benefit can be defined as the payment that employer gives for sake of meeting

employees several expenses, however these are not included in the salary or wages. The

employee starts getting this fringe benefit when they join the company and each of the

employees are eligible for availing these services. Starting from the director as well as

shareholders get this fringe benefit and the company is liable for giving tax for this fringe

benefit (Cooper 2016). Consequently, the situation may vary where the employer can reduce

their amount of tax which they are paying for all the fringe benefits. In contrary with this the

employers don’t always provide payments as fringe benefits, the employees sometimes are

eligible for different facilities instead of payments. Now this kind of payment is considered as

the employee contribution. These payments generally companies takes as they are providing

the fringe benefit to their employees.

Depreciation Schedule Base Value Total Days Held Depreciation

New Restaurant Freezer 3,500.00$

Less: Trade In Value @ 500 3,000.00$ 333.00$ 547.40$

Air Conditions installation 1,200.00$ 272.00$ 178.85$

Total Depreciation 726.25$

Working papers

Notes 8

Conclusion:

According to section 90 this can be concluded that the income of Olivia and Daniel

together as a partnership showed as $2,373 for the year ended 30th June 2017.

Answer to questions 2:

Issues:

In this case study two thorough discussions are held in terms of fringe benefit first is

payment of fees for child’s school of an employee and the housing fringe benefit provided to

the employee.

Rule:

Fringe benefit can be defined as the payment that employer gives for sake of meeting

employees several expenses, however these are not included in the salary or wages. The

employee starts getting this fringe benefit when they join the company and each of the

employees are eligible for availing these services. Starting from the director as well as

shareholders get this fringe benefit and the company is liable for giving tax for this fringe

benefit (Cooper 2016). Consequently, the situation may vary where the employer can reduce

their amount of tax which they are paying for all the fringe benefits. In contrary with this the

employers don’t always provide payments as fringe benefits, the employees sometimes are

eligible for different facilities instead of payments. Now this kind of payment is considered as

the employee contribution. These payments generally companies takes as they are providing

the fringe benefit to their employees.

8TAXATION LAW

According to the taxation commissioner of “FC of T v J & G Knowles (2000)”, the

expense which is taken care by their company should be having materialistic relation

with. “sub-paragraph 65A (ii) of the FBTAA 1986” states that the if the child of the

employee is pursuing a full time education then the employer is liable to provide them the

deductions in terms of the fringe benefit calculated (Braverman, Marsden and Sadiq 2015).

The employee should be allowed this deduction as he is indulging his child into the full time

education.

Consequently, according to “section 25 of the FBTAA 1986” the housing fringe

benefit is coming into the picture when the employee is using a part of the house or apartment

owned by his company as a permanent residence. The housing fringe benefit can be a flat or

part of an apartment (Butler and Calcott 2018). The important aspect in this case is that if a

company is providing housing fringe benefit then the employee and the employee shares the

same rights to use the property. Additionally the rent value for these accommodations is

calculated depending upon the market value of the housing (Barry and Caron 2015). Hence,

the rental charges and rental properties are taxable for the employer in terms of the fringe

benefits which the employer is providing to their employees.

Application:

John is a senior executive in a company whose employer is paying $15,000 for his

kid’s schooling. According to “section 20 of FBTAA 1986” the concept of fringe benefit is

highlighted in this case study as the employer is liable here to pay the school fees of John’s

kid.

In accordance to the discussion of fringe benefit this highlighted in this section that

the payment of kid’s school fees is considered as the fringe benefit as John’s kid is pursuing a

full time education. Hence he is having materialistic relation to his expense. The employer of

According to the taxation commissioner of “FC of T v J & G Knowles (2000)”, the

expense which is taken care by their company should be having materialistic relation

with. “sub-paragraph 65A (ii) of the FBTAA 1986” states that the if the child of the

employee is pursuing a full time education then the employer is liable to provide them the

deductions in terms of the fringe benefit calculated (Braverman, Marsden and Sadiq 2015).

The employee should be allowed this deduction as he is indulging his child into the full time

education.

Consequently, according to “section 25 of the FBTAA 1986” the housing fringe

benefit is coming into the picture when the employee is using a part of the house or apartment

owned by his company as a permanent residence. The housing fringe benefit can be a flat or

part of an apartment (Butler and Calcott 2018). The important aspect in this case is that if a

company is providing housing fringe benefit then the employee and the employee shares the

same rights to use the property. Additionally the rent value for these accommodations is

calculated depending upon the market value of the housing (Barry and Caron 2015). Hence,

the rental charges and rental properties are taxable for the employer in terms of the fringe

benefits which the employer is providing to their employees.

Application:

John is a senior executive in a company whose employer is paying $15,000 for his

kid’s schooling. According to “section 20 of FBTAA 1986” the concept of fringe benefit is

highlighted in this case study as the employer is liable here to pay the school fees of John’s

kid.

In accordance to the discussion of fringe benefit this highlighted in this section that

the payment of kid’s school fees is considered as the fringe benefit as John’s kid is pursuing a

full time education. Hence he is having materialistic relation to his expense. The employer of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

John is liable in providing deductions in John materialist expense. According to “sub-

paragraph 65A (ii) of the FBTAA 1986” the employer is gaining one advantage, he is

allowed to reduce the deductions from the fringe benefit hence he has to pay less amount of

fringe benefit tax (Soled and Thomas 2016).

After discussing the scenario of education now if we discuss about the housing fringe

benefit, the market value of the house which John got from his employer is $800 per week

however, he is paying $100 per week. As John is using this part of house as permanent

residence hence John is liable to pay $100 per week to his employer which is lesser than the

market value of the property. As per “section 27 (1), FBTAA 1986”, John and employer

share the same rights for the rented house (Clemens, Kahn and Meer 2018). This fringe

benefit is considered as fringe rental allowance as John is using this property, he is liable for

the rent and this has to be his expense. According to the above discussions, the chargeable

fringe benefits are elaborated in the following tables:

Particulars Amount ($)

Rent Per Week 800.00$

Annualized Market Value 41,600.00$

(800 x 52 weeks)

Less: Employee’s Contribution

(100 x 52 weeks) 5,200.00$

Taxable Value 36,400.00$

Computation of Taxable value of rent

Conclusion:

The conclusion can be drawn that the employer reduces the fringe benefit tax by

reducing the value which is being paid by the employees. Hence the employer will be liable

here for paying the tax for housing fringe benefit and the expenses that he is providing to his

employees.

John is liable in providing deductions in John materialist expense. According to “sub-

paragraph 65A (ii) of the FBTAA 1986” the employer is gaining one advantage, he is

allowed to reduce the deductions from the fringe benefit hence he has to pay less amount of

fringe benefit tax (Soled and Thomas 2016).

After discussing the scenario of education now if we discuss about the housing fringe

benefit, the market value of the house which John got from his employer is $800 per week

however, he is paying $100 per week. As John is using this part of house as permanent

residence hence John is liable to pay $100 per week to his employer which is lesser than the

market value of the property. As per “section 27 (1), FBTAA 1986”, John and employer

share the same rights for the rented house (Clemens, Kahn and Meer 2018). This fringe

benefit is considered as fringe rental allowance as John is using this property, he is liable for

the rent and this has to be his expense. According to the above discussions, the chargeable

fringe benefits are elaborated in the following tables:

Particulars Amount ($)

Rent Per Week 800.00$

Annualized Market Value 41,600.00$

(800 x 52 weeks)

Less: Employee’s Contribution

(100 x 52 weeks) 5,200.00$

Taxable Value 36,400.00$

Computation of Taxable value of rent

Conclusion:

The conclusion can be drawn that the employer reduces the fringe benefit tax by

reducing the value which is being paid by the employees. Hence the employer will be liable

here for paying the tax for housing fringe benefit and the expenses that he is providing to his

employees.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Barry, J.M. and Caron, P.L., 2015. Tax regulation, transportation innovation, and the sharing

economy. U. Chi. L. Rev. Dialogue, 82, p.69.

Braverman, D., Marsden, S. and Sadiq, K., 2015. Assessing Taxpayer Response to

Legislative Changes: A Case Study of In-House Fringe Benefits Rules. J. Austl. Tax'n, 17,

p.1.

Butler, C. and Calcott, P., 2018. Optimal fringe benefit taxes: the implications of business

use. International Tax and Public Finance, 25(3), pp.654-672.

Clemens, J., Kahn, L.B. and Meer, J., 2018. The Minimum Wage, Fringe Benefits, and

Worker Welfare (No. w24635). National Bureau of Economic Research.

Cooper, R., 2016. How to tax cellphones in the workplace: fringe benefits. Tax Breaks

Newsletter, 2016(369), pp.4-6.

Kwall, J.L., 2019. The Federal Income Taxation of Corporations, Partnerships, Limited

Liability Companies and Their Owners, Part One.

Laing, S., 2015. Partnership Taxation 2015/16. Bloomsbury Publishing.

Lind, S.A. ed., 2015. Fundamentals of Partnership Taxation: Cases and Materials.

Foundation Press.

Schwidetzky, W., 2017. Partnership Tax Allocations: The Basics. Colo. Law., 46, p.39.

Soled, J.A. and Thomas, K.D., 2016. Revisiting the Taxation of Fringe Benefits. Wash. L.

Rev., 91, p.761.

References:

Barry, J.M. and Caron, P.L., 2015. Tax regulation, transportation innovation, and the sharing

economy. U. Chi. L. Rev. Dialogue, 82, p.69.

Braverman, D., Marsden, S. and Sadiq, K., 2015. Assessing Taxpayer Response to

Legislative Changes: A Case Study of In-House Fringe Benefits Rules. J. Austl. Tax'n, 17,

p.1.

Butler, C. and Calcott, P., 2018. Optimal fringe benefit taxes: the implications of business

use. International Tax and Public Finance, 25(3), pp.654-672.

Clemens, J., Kahn, L.B. and Meer, J., 2018. The Minimum Wage, Fringe Benefits, and

Worker Welfare (No. w24635). National Bureau of Economic Research.

Cooper, R., 2016. How to tax cellphones in the workplace: fringe benefits. Tax Breaks

Newsletter, 2016(369), pp.4-6.

Kwall, J.L., 2019. The Federal Income Taxation of Corporations, Partnerships, Limited

Liability Companies and Their Owners, Part One.

Laing, S., 2015. Partnership Taxation 2015/16. Bloomsbury Publishing.

Lind, S.A. ed., 2015. Fundamentals of Partnership Taxation: Cases and Materials.

Foundation Press.

Schwidetzky, W., 2017. Partnership Tax Allocations: The Basics. Colo. Law., 46, p.39.

Soled, J.A. and Thomas, K.D., 2016. Revisiting the Taxation of Fringe Benefits. Wash. L.

Rev., 91, p.761.

11TAXATION LAW

Tang, R. and Wan, J., 2015. Fringe benefits tax and fly-in fly-out arrangements: John Holland

Group Pty Ltd v Commissioner of Taxation. Australian Resources and Energy Law

Journal, 34(1), p.17.

Willis, A.B., 2014. Willis on Partnership Taxation. McGraw-Hill.

Willis, A.B., Pennell, J.S., Postlewaite, P.F. and Alexander, J.H., 2014. Partnership

taxation (pp. 131-16). Shepard's/McGraw-Hill.

Tang, R. and Wan, J., 2015. Fringe benefits tax and fly-in fly-out arrangements: John Holland

Group Pty Ltd v Commissioner of Taxation. Australian Resources and Energy Law

Journal, 34(1), p.17.

Willis, A.B., 2014. Willis on Partnership Taxation. McGraw-Hill.

Willis, A.B., Pennell, J.S., Postlewaite, P.F. and Alexander, J.H., 2014. Partnership

taxation (pp. 131-16). Shepard's/McGraw-Hill.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.