HI6028 Taxation Law: Partnership Income, Expenses & FBT Analysis

VerifiedAdded on 2023/04/21

|12

|2139

|206

Homework Assignment

AI Summary

This assignment provides a detailed analysis of taxation theory, practice, and law. It addresses two main questions: determining the net income for a partnership (Brekkie and Lunch and OZ Bottle Shop) in accordance with Section 90 of ITAA 1936, including allowable deductions and depreciation calculations, and determining the employer's liability regarding taxable fringe benefits (expense payments and housing) provided to staff, in accordance with Section 20 and Section 25 of FBTAA 1986. The document includes computations, working papers, and references to relevant legal sections and rulings. Desklib offers a range of solved assignments and resources for students.

Running head: TAXATION THEORY, PRACTICE AND LAW

Taxation Theory, Practice and Law

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Taxation Theory, Practice and Law

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION THEORY, PRACTICE AND LAW

Table of Contents

Answer to Question 1:................................................................................................................2

Issues:.....................................................................................................................................2

Application:............................................................................................................................2

Conclusion:............................................................................................................................6

Answer to Question 2:................................................................................................................7

Issues:.....................................................................................................................................7

Application:............................................................................................................................7

Conclusion:............................................................................................................................9

References:...............................................................................................................................10

Table of Contents

Answer to Question 1:................................................................................................................2

Issues:.....................................................................................................................................2

Application:............................................................................................................................2

Conclusion:............................................................................................................................6

Answer to Question 2:................................................................................................................7

Issues:.....................................................................................................................................7

Application:............................................................................................................................7

Conclusion:............................................................................................................................9

References:...............................................................................................................................10

2TAXATION THEORY, PRACTICE AND LAW

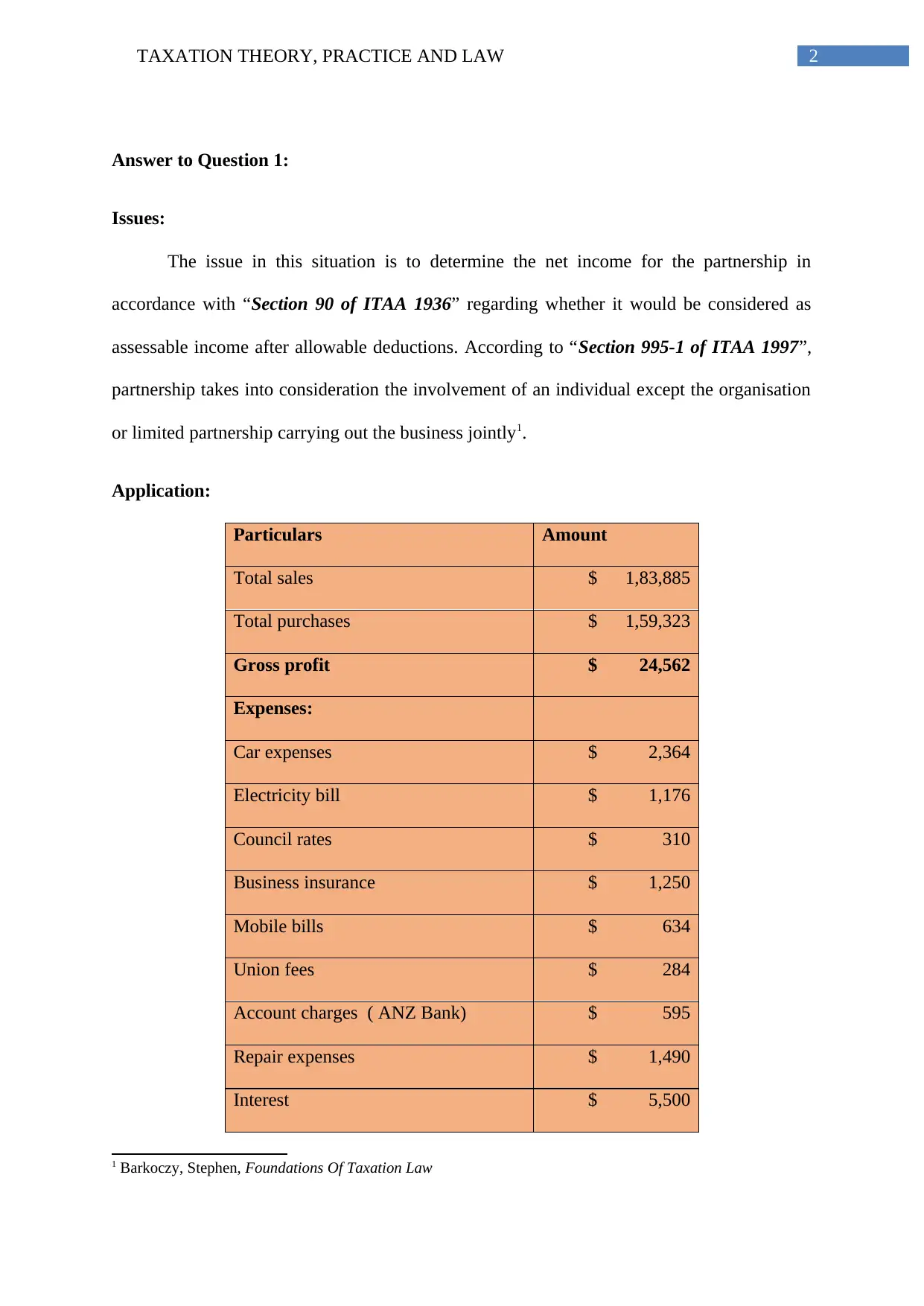

Answer to Question 1:

Issues:

The issue in this situation is to determine the net income for the partnership in

accordance with “Section 90 of ITAA 1936” regarding whether it would be considered as

assessable income after allowable deductions. According to “Section 995-1 of ITAA 1997”,

partnership takes into consideration the involvement of an individual except the organisation

or limited partnership carrying out the business jointly1.

Application:

Particulars Amount

Total sales $ 1,83,885

Total purchases $ 1,59,323

Gross profit $ 24,562

Expenses:

Car expenses $ 2,364

Electricity bill $ 1,176

Council rates $ 310

Business insurance $ 1,250

Mobile bills $ 634

Union fees $ 284

Account charges ( ANZ Bank) $ 595

Repair expenses $ 1,490

Interest $ 5,500

1 Barkoczy, Stephen, Foundations Of Taxation Law

Answer to Question 1:

Issues:

The issue in this situation is to determine the net income for the partnership in

accordance with “Section 90 of ITAA 1936” regarding whether it would be considered as

assessable income after allowable deductions. According to “Section 995-1 of ITAA 1997”,

partnership takes into consideration the involvement of an individual except the organisation

or limited partnership carrying out the business jointly1.

Application:

Particulars Amount

Total sales $ 1,83,885

Total purchases $ 1,59,323

Gross profit $ 24,562

Expenses:

Car expenses $ 2,364

Electricity bill $ 1,176

Council rates $ 310

Business insurance $ 1,250

Mobile bills $ 634

Union fees $ 284

Account charges ( ANZ Bank) $ 595

Repair expenses $ 1,490

Interest $ 5,500

1 Barkoczy, Stephen, Foundations Of Taxation Law

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION THEORY, PRACTICE AND LAW

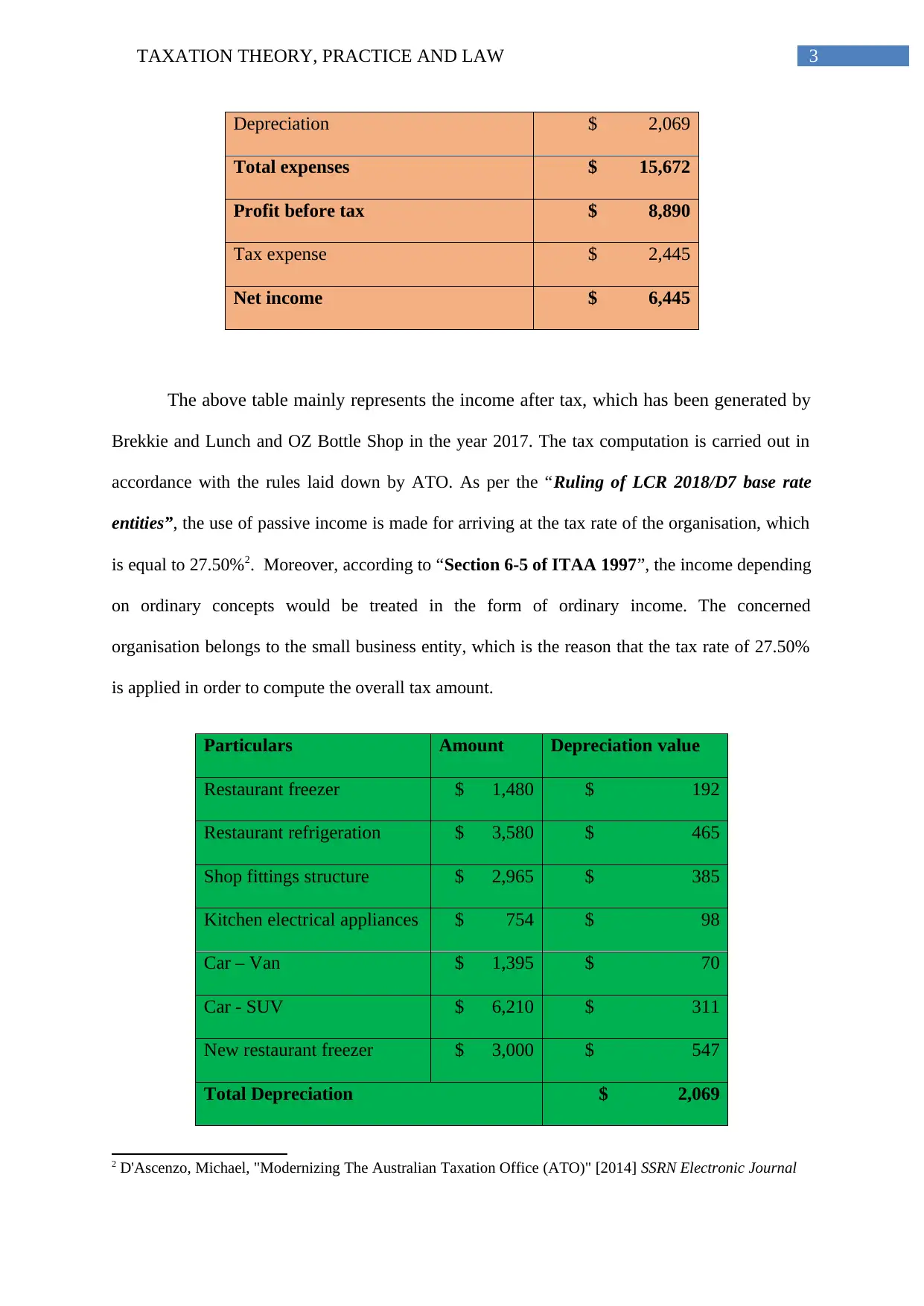

Depreciation $ 2,069

Total expenses $ 15,672

Profit before tax $ 8,890

Tax expense $ 2,445

Net income $ 6,445

The above table mainly represents the income after tax, which has been generated by

Brekkie and Lunch and OZ Bottle Shop in the year 2017. The tax computation is carried out in

accordance with the rules laid down by ATO. As per the “Ruling of LCR 2018/D7 base rate

entities”, the use of passive income is made for arriving at the tax rate of the organisation, which

is equal to 27.50%2. Moreover, according to “Section 6-5 of ITAA 1997”, the income depending

on ordinary concepts would be treated in the form of ordinary income. The concerned

organisation belongs to the small business entity, which is the reason that the tax rate of 27.50%

is applied in order to compute the overall tax amount.

Particulars Amount Depreciation value

Restaurant freezer $ 1,480 $ 192

Restaurant refrigeration $ 3,580 $ 465

Shop fittings structure $ 2,965 $ 385

Kitchen electrical appliances $ 754 $ 98

Car – Van $ 1,395 $ 70

Car - SUV $ 6,210 $ 311

New restaurant freezer $ 3,000 $ 547

Total Depreciation $ 2,069

2 D'Ascenzo, Michael, "Modernizing The Australian Taxation Office (ATO)" [2014] SSRN Electronic Journal

Depreciation $ 2,069

Total expenses $ 15,672

Profit before tax $ 8,890

Tax expense $ 2,445

Net income $ 6,445

The above table mainly represents the income after tax, which has been generated by

Brekkie and Lunch and OZ Bottle Shop in the year 2017. The tax computation is carried out in

accordance with the rules laid down by ATO. As per the “Ruling of LCR 2018/D7 base rate

entities”, the use of passive income is made for arriving at the tax rate of the organisation, which

is equal to 27.50%2. Moreover, according to “Section 6-5 of ITAA 1997”, the income depending

on ordinary concepts would be treated in the form of ordinary income. The concerned

organisation belongs to the small business entity, which is the reason that the tax rate of 27.50%

is applied in order to compute the overall tax amount.

Particulars Amount Depreciation value

Restaurant freezer $ 1,480 $ 192

Restaurant refrigeration $ 3,580 $ 465

Shop fittings structure $ 2,965 $ 385

Kitchen electrical appliances $ 754 $ 98

Car – Van $ 1,395 $ 70

Car - SUV $ 6,210 $ 311

New restaurant freezer $ 3,000 $ 547

Total Depreciation $ 2,069

2 D'Ascenzo, Michael, "Modernizing The Australian Taxation Office (ATO)" [2014] SSRN Electronic Journal

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION THEORY, PRACTICE AND LAW

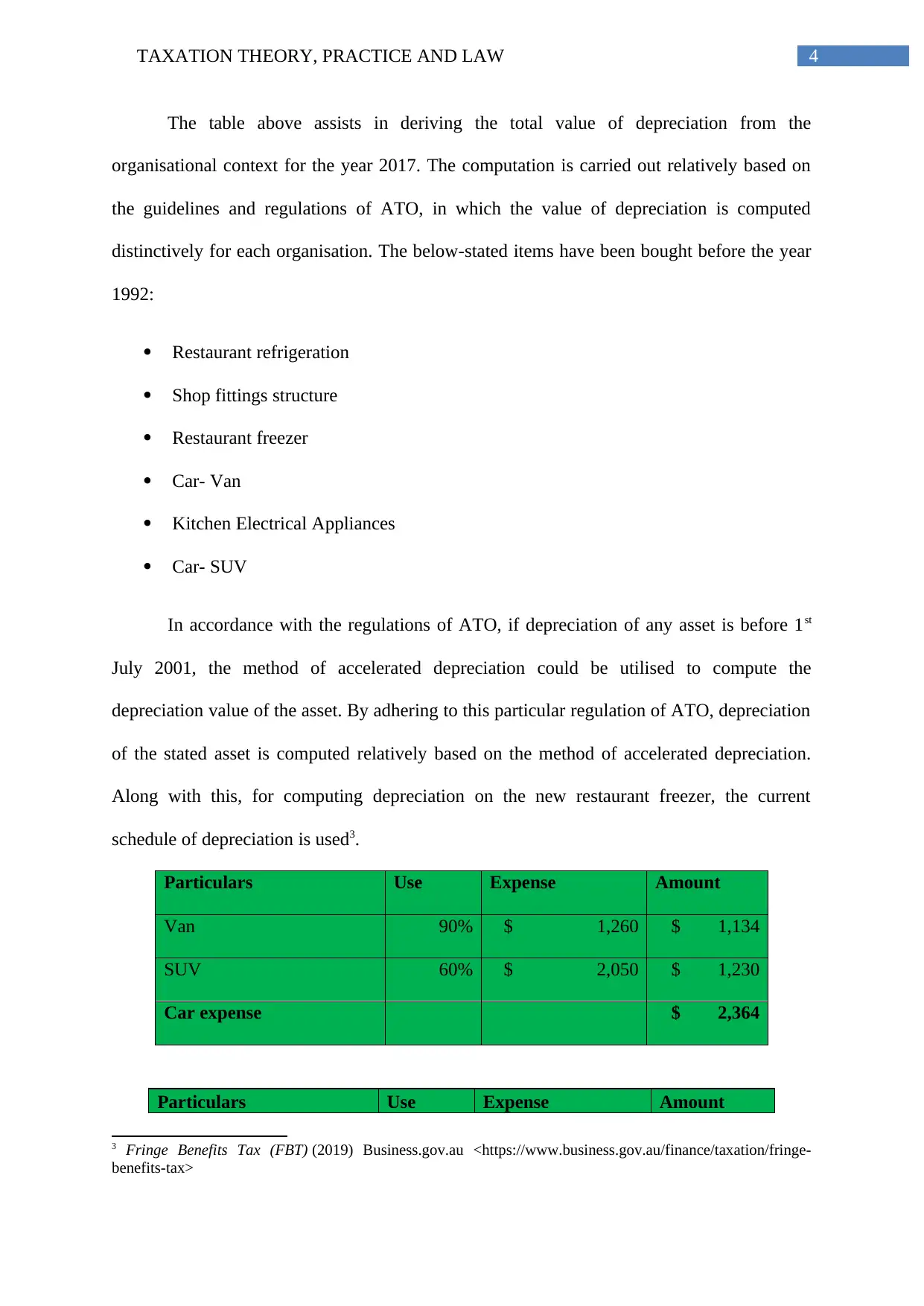

The table above assists in deriving the total value of depreciation from the

organisational context for the year 2017. The computation is carried out relatively based on

the guidelines and regulations of ATO, in which the value of depreciation is computed

distinctively for each organisation. The below-stated items have been bought before the year

1992:

Restaurant refrigeration

Shop fittings structure

Restaurant freezer

Car- Van

Kitchen Electrical Appliances

Car- SUV

In accordance with the regulations of ATO, if depreciation of any asset is before 1st

July 2001, the method of accelerated depreciation could be utilised to compute the

depreciation value of the asset. By adhering to this particular regulation of ATO, depreciation

of the stated asset is computed relatively based on the method of accelerated depreciation.

Along with this, for computing depreciation on the new restaurant freezer, the current

schedule of depreciation is used3.

Particulars Use Expense Amount

Van 90% $ 1,260 $ 1,134

SUV 60% $ 2,050 $ 1,230

Car expense $ 2,364

Particulars Use Expense Amount

3 Fringe Benefits Tax (FBT) (2019) Business.gov.au <https://www.business.gov.au/finance/taxation/fringe-

benefits-tax>

The table above assists in deriving the total value of depreciation from the

organisational context for the year 2017. The computation is carried out relatively based on

the guidelines and regulations of ATO, in which the value of depreciation is computed

distinctively for each organisation. The below-stated items have been bought before the year

1992:

Restaurant refrigeration

Shop fittings structure

Restaurant freezer

Car- Van

Kitchen Electrical Appliances

Car- SUV

In accordance with the regulations of ATO, if depreciation of any asset is before 1st

July 2001, the method of accelerated depreciation could be utilised to compute the

depreciation value of the asset. By adhering to this particular regulation of ATO, depreciation

of the stated asset is computed relatively based on the method of accelerated depreciation.

Along with this, for computing depreciation on the new restaurant freezer, the current

schedule of depreciation is used3.

Particulars Use Expense Amount

Van 90% $ 1,260 $ 1,134

SUV 60% $ 2,050 $ 1,230

Car expense $ 2,364

Particulars Use Expense Amount

3 Fringe Benefits Tax (FBT) (2019) Business.gov.au <https://www.business.gov.au/finance/taxation/fringe-

benefits-tax>

5TAXATION THEORY, PRACTICE AND LAW

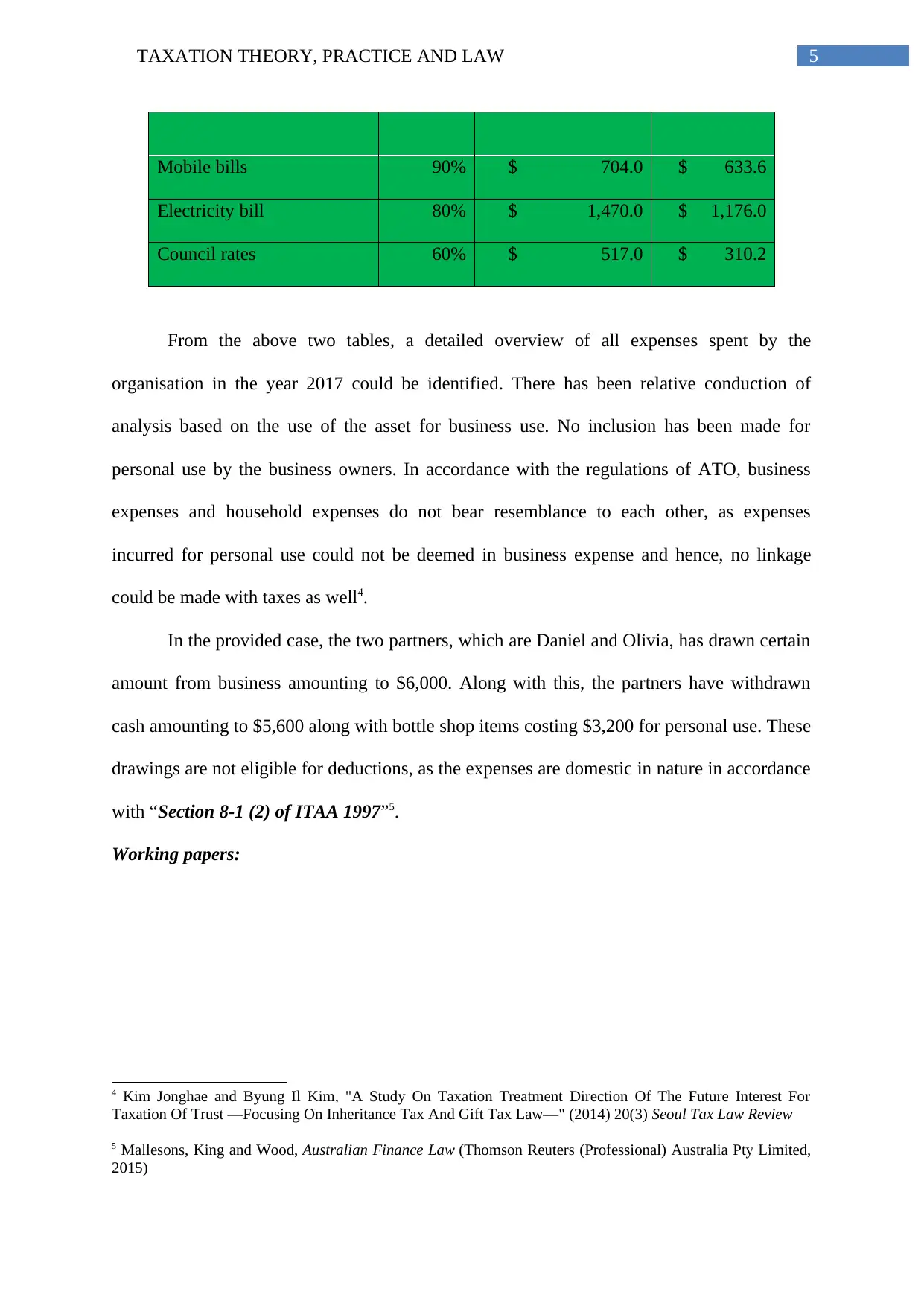

Mobile bills 90% $ 704.0 $ 633.6

Electricity bill 80% $ 1,470.0 $ 1,176.0

Council rates 60% $ 517.0 $ 310.2

From the above two tables, a detailed overview of all expenses spent by the

organisation in the year 2017 could be identified. There has been relative conduction of

analysis based on the use of the asset for business use. No inclusion has been made for

personal use by the business owners. In accordance with the regulations of ATO, business

expenses and household expenses do not bear resemblance to each other, as expenses

incurred for personal use could not be deemed in business expense and hence, no linkage

could be made with taxes as well4.

In the provided case, the two partners, which are Daniel and Olivia, has drawn certain

amount from business amounting to $6,000. Along with this, the partners have withdrawn

cash amounting to $5,600 along with bottle shop items costing $3,200 for personal use. These

drawings are not eligible for deductions, as the expenses are domestic in nature in accordance

with “Section 8-1 (2) of ITAA 1997”5.

Working papers:

4 Kim Jonghae and Byung Il Kim, "A Study On Taxation Treatment Direction Of The Future Interest For

Taxation Of Trust ―Focusing On Inheritance Tax And Gift Tax Law―" (2014) 20(3) Seoul Tax Law Review

5 Mallesons, King and Wood, Australian Finance Law (Thomson Reuters (Professional) Australia Pty Limited,

2015)

Mobile bills 90% $ 704.0 $ 633.6

Electricity bill 80% $ 1,470.0 $ 1,176.0

Council rates 60% $ 517.0 $ 310.2

From the above two tables, a detailed overview of all expenses spent by the

organisation in the year 2017 could be identified. There has been relative conduction of

analysis based on the use of the asset for business use. No inclusion has been made for

personal use by the business owners. In accordance with the regulations of ATO, business

expenses and household expenses do not bear resemblance to each other, as expenses

incurred for personal use could not be deemed in business expense and hence, no linkage

could be made with taxes as well4.

In the provided case, the two partners, which are Daniel and Olivia, has drawn certain

amount from business amounting to $6,000. Along with this, the partners have withdrawn

cash amounting to $5,600 along with bottle shop items costing $3,200 for personal use. These

drawings are not eligible for deductions, as the expenses are domestic in nature in accordance

with “Section 8-1 (2) of ITAA 1997”5.

Working papers:

4 Kim Jonghae and Byung Il Kim, "A Study On Taxation Treatment Direction Of The Future Interest For

Taxation Of Trust ―Focusing On Inheritance Tax And Gift Tax Law―" (2014) 20(3) Seoul Tax Law Review

5 Mallesons, King and Wood, Australian Finance Law (Thomson Reuters (Professional) Australia Pty Limited,

2015)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION THEORY, PRACTICE AND LAW

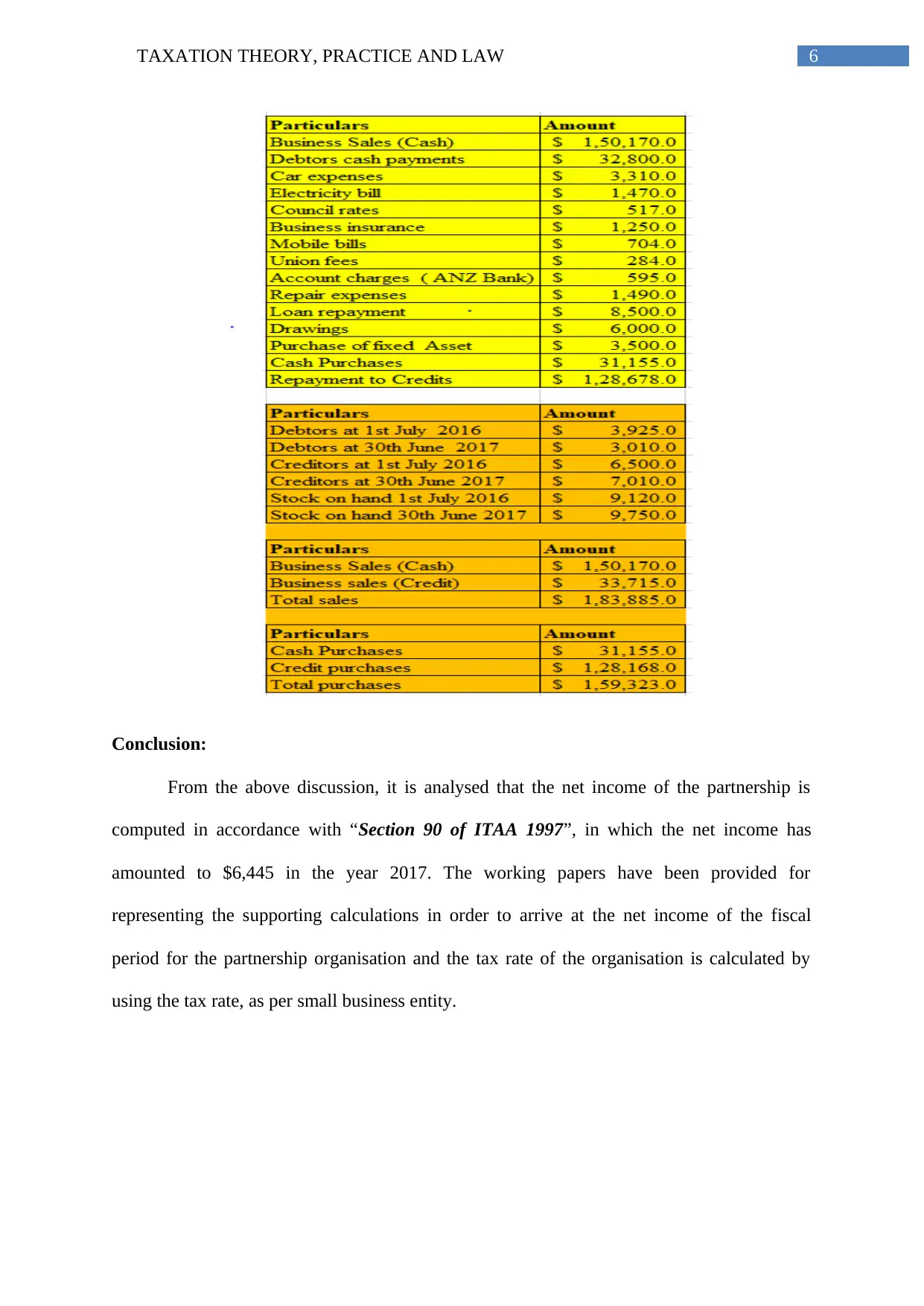

Conclusion:

From the above discussion, it is analysed that the net income of the partnership is

computed in accordance with “Section 90 of ITAA 1997”, in which the net income has

amounted to $6,445 in the year 2017. The working papers have been provided for

representing the supporting calculations in order to arrive at the net income of the fiscal

period for the partnership organisation and the tax rate of the organisation is calculated by

using the tax rate, as per small business entity.

Conclusion:

From the above discussion, it is analysed that the net income of the partnership is

computed in accordance with “Section 90 of ITAA 1997”, in which the net income has

amounted to $6,445 in the year 2017. The working papers have been provided for

representing the supporting calculations in order to arrive at the net income of the fiscal

period for the partnership organisation and the tax rate of the organisation is calculated by

using the tax rate, as per small business entity.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION THEORY, PRACTICE AND LAW

Answer to Question 2:

Issues:

The issue in this situation is to determine the liability of the employer associated with

the taxable amount of the benefits related to expense payment provided to the staff in

accordance with “Section 20 of FBTAA 1986”. Moreover, another issue is to determine the

consequences of the employer for taxation in accordance with “Section 25 of FBTAA 1986”

for providing housing fringe benefits to the staff6.

Application:

Fringe benefits are a significant part of business and it could be a useful method so

that quality staffs could be attracted. However, when an employer provides fringe benefits to

the staffs, the individual has to be aware of the tax obligations. Fringe benefits tax could be a

tax payable on the part of the employers for benefits paid to a staff or family member of the

staff in place of wages and salaries7. This is distinctive from income tax and it is computed

based on the provided taxable amount of the fringe benefits. For instance, an employee might

receive fringe benefits in the form of car, car parking, private expense payment and low loans

on interest. This is completely legal and a common reimbursement form that the business

organisations utilise for their employees8.

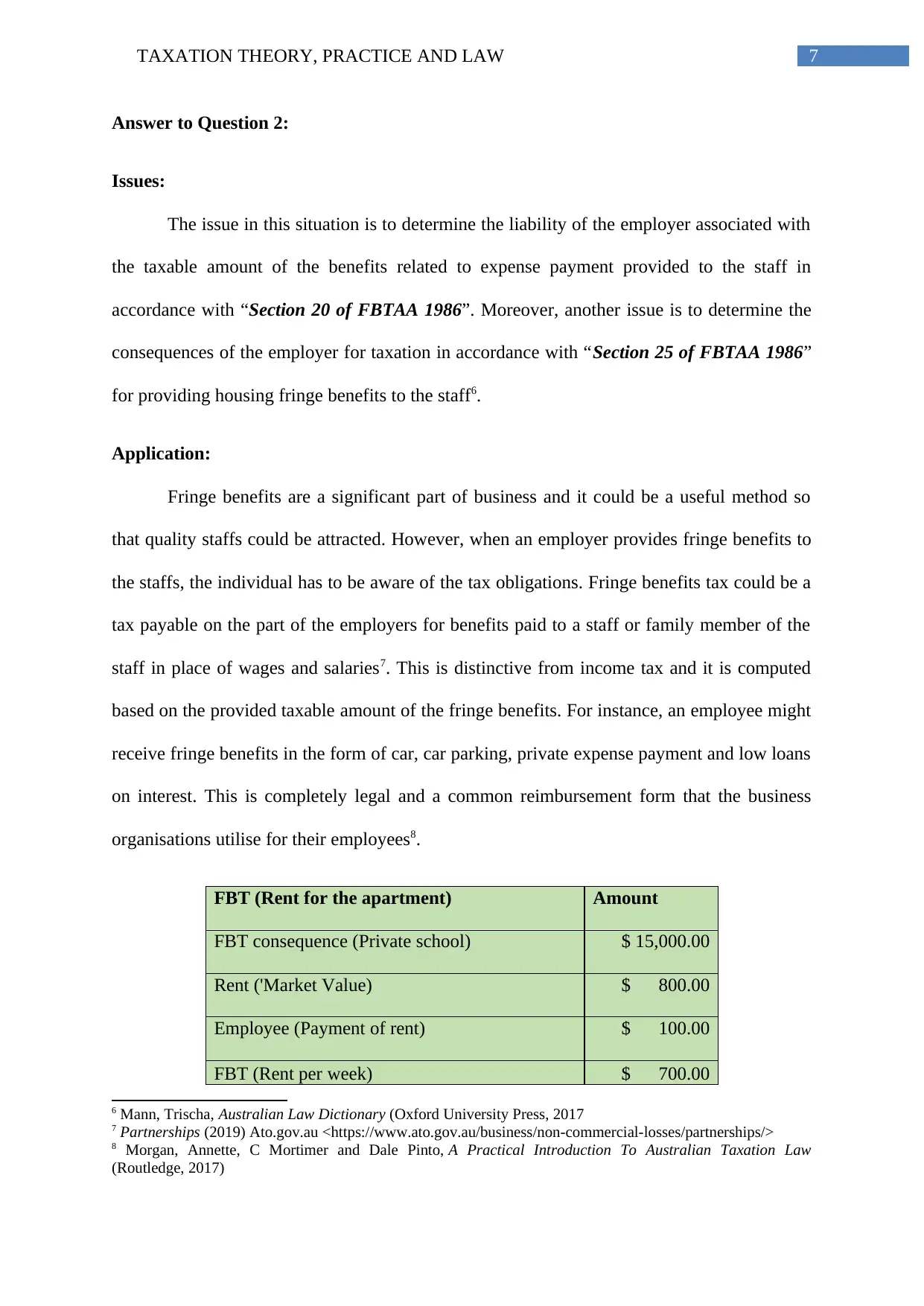

FBT (Rent for the apartment) Amount

FBT consequence (Private school) $ 15,000.00

Rent ('Market Value) $ 800.00

Employee (Payment of rent) $ 100.00

FBT (Rent per week) $ 700.00

6 Mann, Trischa, Australian Law Dictionary (Oxford University Press, 2017

7 Partnerships (2019) Ato.gov.au <https://www.ato.gov.au/business/non-commercial-losses/partnerships/>

8 Morgan, Annette, C Mortimer and Dale Pinto, A Practical Introduction To Australian Taxation Law

(Routledge, 2017)

Answer to Question 2:

Issues:

The issue in this situation is to determine the liability of the employer associated with

the taxable amount of the benefits related to expense payment provided to the staff in

accordance with “Section 20 of FBTAA 1986”. Moreover, another issue is to determine the

consequences of the employer for taxation in accordance with “Section 25 of FBTAA 1986”

for providing housing fringe benefits to the staff6.

Application:

Fringe benefits are a significant part of business and it could be a useful method so

that quality staffs could be attracted. However, when an employer provides fringe benefits to

the staffs, the individual has to be aware of the tax obligations. Fringe benefits tax could be a

tax payable on the part of the employers for benefits paid to a staff or family member of the

staff in place of wages and salaries7. This is distinctive from income tax and it is computed

based on the provided taxable amount of the fringe benefits. For instance, an employee might

receive fringe benefits in the form of car, car parking, private expense payment and low loans

on interest. This is completely legal and a common reimbursement form that the business

organisations utilise for their employees8.

FBT (Rent for the apartment) Amount

FBT consequence (Private school) $ 15,000.00

Rent ('Market Value) $ 800.00

Employee (Payment of rent) $ 100.00

FBT (Rent per week) $ 700.00

6 Mann, Trischa, Australian Law Dictionary (Oxford University Press, 2017

7 Partnerships (2019) Ato.gov.au <https://www.ato.gov.au/business/non-commercial-losses/partnerships/>

8 Morgan, Annette, C Mortimer and Dale Pinto, A Practical Introduction To Australian Taxation Law

(Routledge, 2017)

8TAXATION THEORY, PRACTICE AND LAW

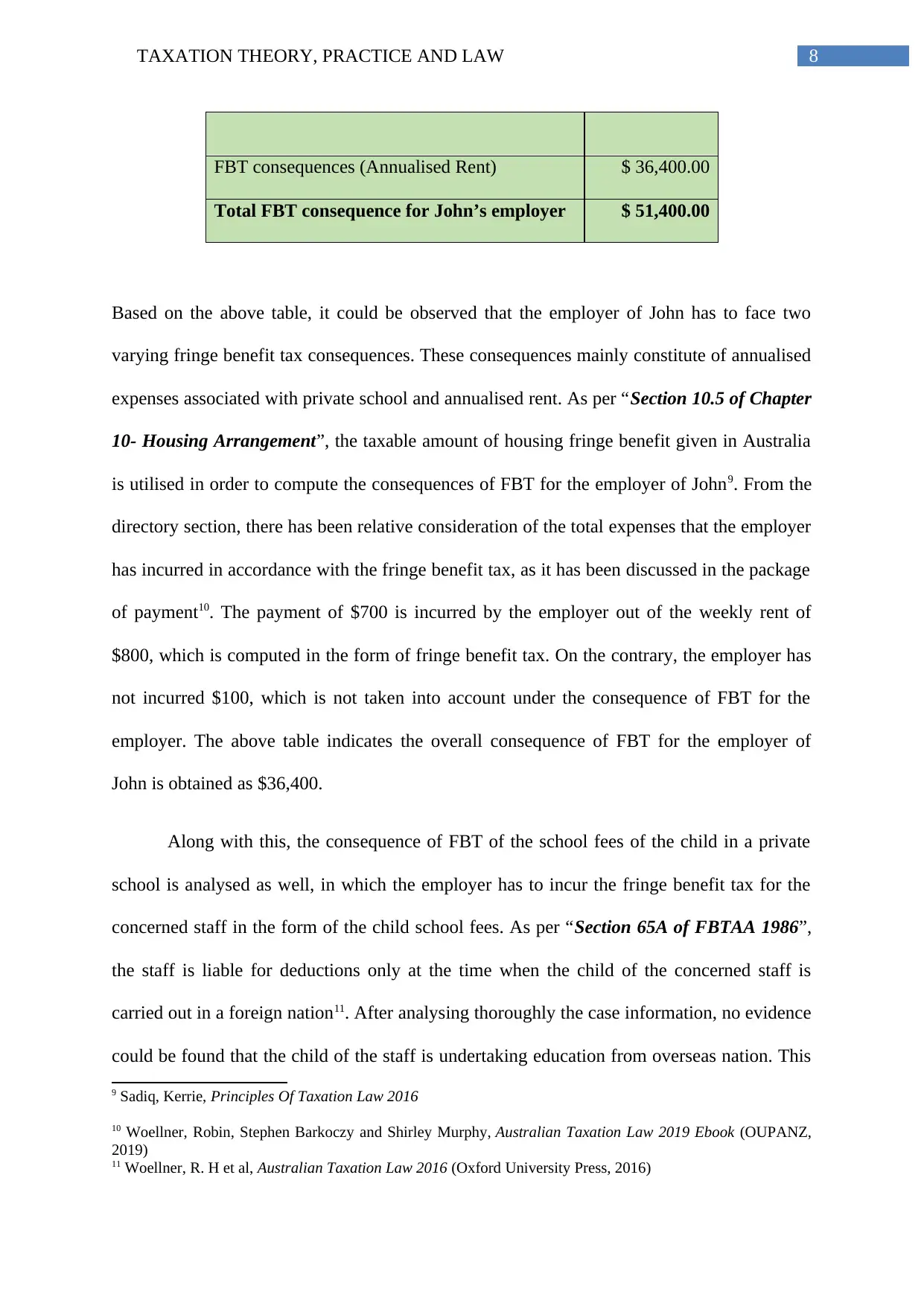

FBT consequences (Annualised Rent) $ 36,400.00

Total FBT consequence for John’s employer $ 51,400.00

Based on the above table, it could be observed that the employer of John has to face two

varying fringe benefit tax consequences. These consequences mainly constitute of annualised

expenses associated with private school and annualised rent. As per “Section 10.5 of Chapter

10- Housing Arrangement”, the taxable amount of housing fringe benefit given in Australia

is utilised in order to compute the consequences of FBT for the employer of John9. From the

directory section, there has been relative consideration of the total expenses that the employer

has incurred in accordance with the fringe benefit tax, as it has been discussed in the package

of payment10. The payment of $700 is incurred by the employer out of the weekly rent of

$800, which is computed in the form of fringe benefit tax. On the contrary, the employer has

not incurred $100, which is not taken into account under the consequence of FBT for the

employer. The above table indicates the overall consequence of FBT for the employer of

John is obtained as $36,400.

Along with this, the consequence of FBT of the school fees of the child in a private

school is analysed as well, in which the employer has to incur the fringe benefit tax for the

concerned staff in the form of the child school fees. As per “Section 65A of FBTAA 1986”,

the staff is liable for deductions only at the time when the child of the concerned staff is

carried out in a foreign nation11. After analysing thoroughly the case information, no evidence

could be found that the child of the staff is undertaking education from overseas nation. This

9 Sadiq, Kerrie, Principles Of Taxation Law 2016

10 Woellner, Robin, Stephen Barkoczy and Shirley Murphy, Australian Taxation Law 2019 Ebook (OUPANZ,

2019)

11 Woellner, R. H et al, Australian Taxation Law 2016 (Oxford University Press, 2016)

FBT consequences (Annualised Rent) $ 36,400.00

Total FBT consequence for John’s employer $ 51,400.00

Based on the above table, it could be observed that the employer of John has to face two

varying fringe benefit tax consequences. These consequences mainly constitute of annualised

expenses associated with private school and annualised rent. As per “Section 10.5 of Chapter

10- Housing Arrangement”, the taxable amount of housing fringe benefit given in Australia

is utilised in order to compute the consequences of FBT for the employer of John9. From the

directory section, there has been relative consideration of the total expenses that the employer

has incurred in accordance with the fringe benefit tax, as it has been discussed in the package

of payment10. The payment of $700 is incurred by the employer out of the weekly rent of

$800, which is computed in the form of fringe benefit tax. On the contrary, the employer has

not incurred $100, which is not taken into account under the consequence of FBT for the

employer. The above table indicates the overall consequence of FBT for the employer of

John is obtained as $36,400.

Along with this, the consequence of FBT of the school fees of the child in a private

school is analysed as well, in which the employer has to incur the fringe benefit tax for the

concerned staff in the form of the child school fees. As per “Section 65A of FBTAA 1986”,

the staff is liable for deductions only at the time when the child of the concerned staff is

carried out in a foreign nation11. After analysing thoroughly the case information, no evidence

could be found that the child of the staff is undertaking education from overseas nation. This

9 Sadiq, Kerrie, Principles Of Taxation Law 2016

10 Woellner, Robin, Stephen Barkoczy and Shirley Murphy, Australian Taxation Law 2019 Ebook (OUPANZ,

2019)

11 Woellner, R. H et al, Australian Taxation Law 2016 (Oxford University Press, 2016)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION THEORY, PRACTICE AND LAW

is the primary reason that no reduction is computed for the employer. Therefore, the total

FBT consequence of the employer is computed as $15,000 for the financial year that takes

into account the payment of school fees12. As a result, the overall consequence of FBT for the

employer of John is obtained as $51,400.

Conclusion:

As a portion of the package of remuneration, the consequences of FBT for the

employer of John takes into consideration the fringe benefit related to expense payment for

the school fees of the child as well as the housing benefit given to John in association with

the taxation year.

12 Woellner, R. H et al, Australian Taxation Law 2018 (Routledge, 2018)

is the primary reason that no reduction is computed for the employer. Therefore, the total

FBT consequence of the employer is computed as $15,000 for the financial year that takes

into account the payment of school fees12. As a result, the overall consequence of FBT for the

employer of John is obtained as $51,400.

Conclusion:

As a portion of the package of remuneration, the consequences of FBT for the

employer of John takes into consideration the fringe benefit related to expense payment for

the school fees of the child as well as the housing benefit given to John in association with

the taxation year.

12 Woellner, R. H et al, Australian Taxation Law 2018 (Routledge, 2018)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION THEORY, PRACTICE AND LAW

References:

Barkoczy, Stephen, Foundations Of Taxation Law

D'Ascenzo, Michael, "Modernizing The Australian Taxation Office (ATO)" [2014] SSRN

Electronic Journal

Fringe Benefits Tax (FBT) (2019) Business.gov.au

<https://www.business.gov.au/finance/taxation/fringe-benefits-tax>

Kim Jonghae and Byung Il Kim, "A Study On Taxation Treatment Direction Of The Future

Interest For Taxation Of Trust ―Focusing On Inheritance Tax And Gift Tax Law―" (2014)

20(3) Seoul Tax Law Review

Mallesons, King and Wood, Australian Finance Law (Thomson Reuters (Professional)

Australia Pty Limited, 2015)

Mann, Trischa, Australian Law Dictionary (Oxford University Press, 2017)

Morgan, Annette, C Mortimer and Dale Pinto, A Practical Introduction To Australian

Taxation Law (Routledge, 2017)

Partnerships (2019) Ato.gov.au

<https://www.ato.gov.au/business/non-commercial-losses/partnerships/>

Sadiq, Kerrie, Principles Of Taxation Law 2016

Woellner, R. H et al, Australian Taxation Law 2016 (Oxford University Press, 2016)

Woellner, R. H et al, Australian Taxation Law 2018 (Routledge, 2018)

References:

Barkoczy, Stephen, Foundations Of Taxation Law

D'Ascenzo, Michael, "Modernizing The Australian Taxation Office (ATO)" [2014] SSRN

Electronic Journal

Fringe Benefits Tax (FBT) (2019) Business.gov.au

<https://www.business.gov.au/finance/taxation/fringe-benefits-tax>

Kim Jonghae and Byung Il Kim, "A Study On Taxation Treatment Direction Of The Future

Interest For Taxation Of Trust ―Focusing On Inheritance Tax And Gift Tax Law―" (2014)

20(3) Seoul Tax Law Review

Mallesons, King and Wood, Australian Finance Law (Thomson Reuters (Professional)

Australia Pty Limited, 2015)

Mann, Trischa, Australian Law Dictionary (Oxford University Press, 2017)

Morgan, Annette, C Mortimer and Dale Pinto, A Practical Introduction To Australian

Taxation Law (Routledge, 2017)

Partnerships (2019) Ato.gov.au

<https://www.ato.gov.au/business/non-commercial-losses/partnerships/>

Sadiq, Kerrie, Principles Of Taxation Law 2016

Woellner, R. H et al, Australian Taxation Law 2016 (Oxford University Press, 2016)

Woellner, R. H et al, Australian Taxation Law 2018 (Routledge, 2018)

11TAXATION THEORY, PRACTICE AND LAW

Woellner, Robin, Stephen Barkoczy and Shirley Murphy, Australian Taxation Law 2019

Ebook (OUPANZ, 2019)

Woellner, Robin, Stephen Barkoczy and Shirley Murphy, Australian Taxation Law 2019

Ebook (OUPANZ, 2019)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.