HI6028 Taxation Theory: Partnership Tax Return & Fringe Benefits

VerifiedAdded on 2023/04/21

|8

|1622

|418

Report

AI Summary

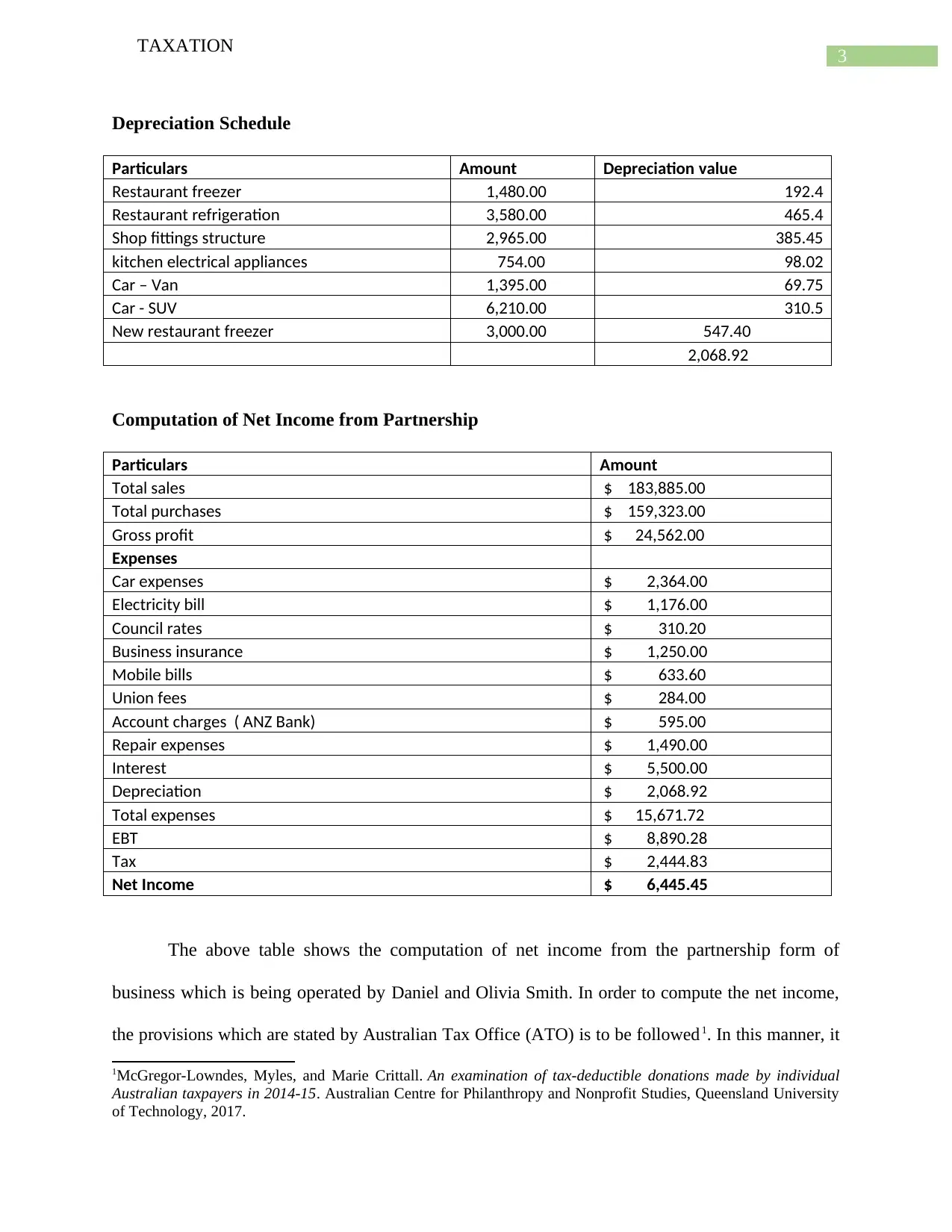

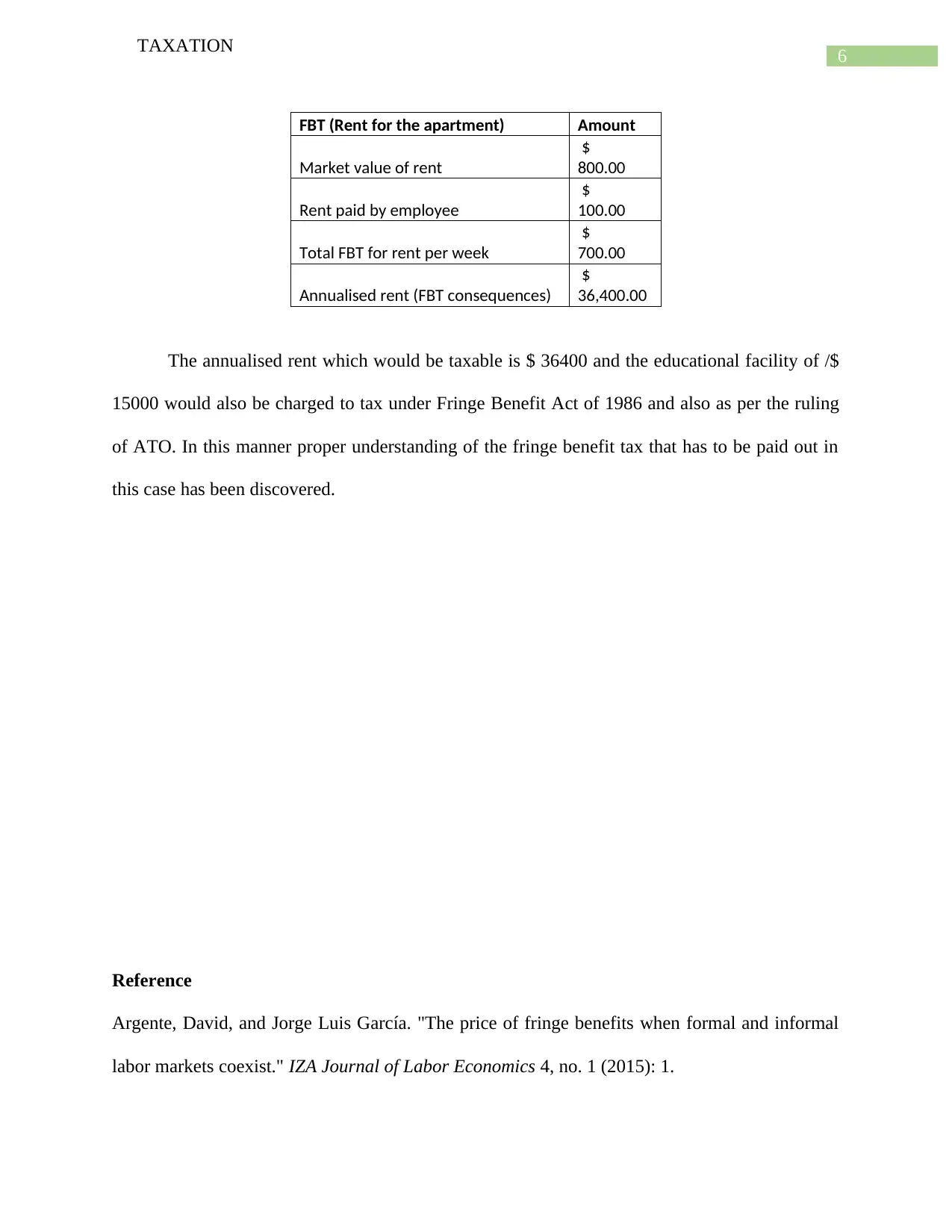

This assignment solution provides a detailed analysis of taxation principles, focusing on partnership tax returns and fringe benefit tax (FBT) implications. It begins with a computation of net income from a partnership business owned by Daniel and Olivia Smith, considering cash and credit sales, purchases, and depreciation of assets, adhering to Australian Tax Office (ATO) guidelines. The net income is calculated, factoring in allowable deductions and depreciation. The second part delves into fringe benefits, explaining their nature and taxability under Australian law, particularly the Fringe Benefit Act of 1986. It examines a case involving an employee, John, who receives educational assistance and housing from his employer, determining the FBT implications and calculating the taxable value of the housing benefit based on market value versus employee contribution.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.