Taxation: Partnership Income, FBT Consequences for John's Employer

VerifiedAdded on 2020/12/29

|9

|2145

|233

Homework Assignment

AI Summary

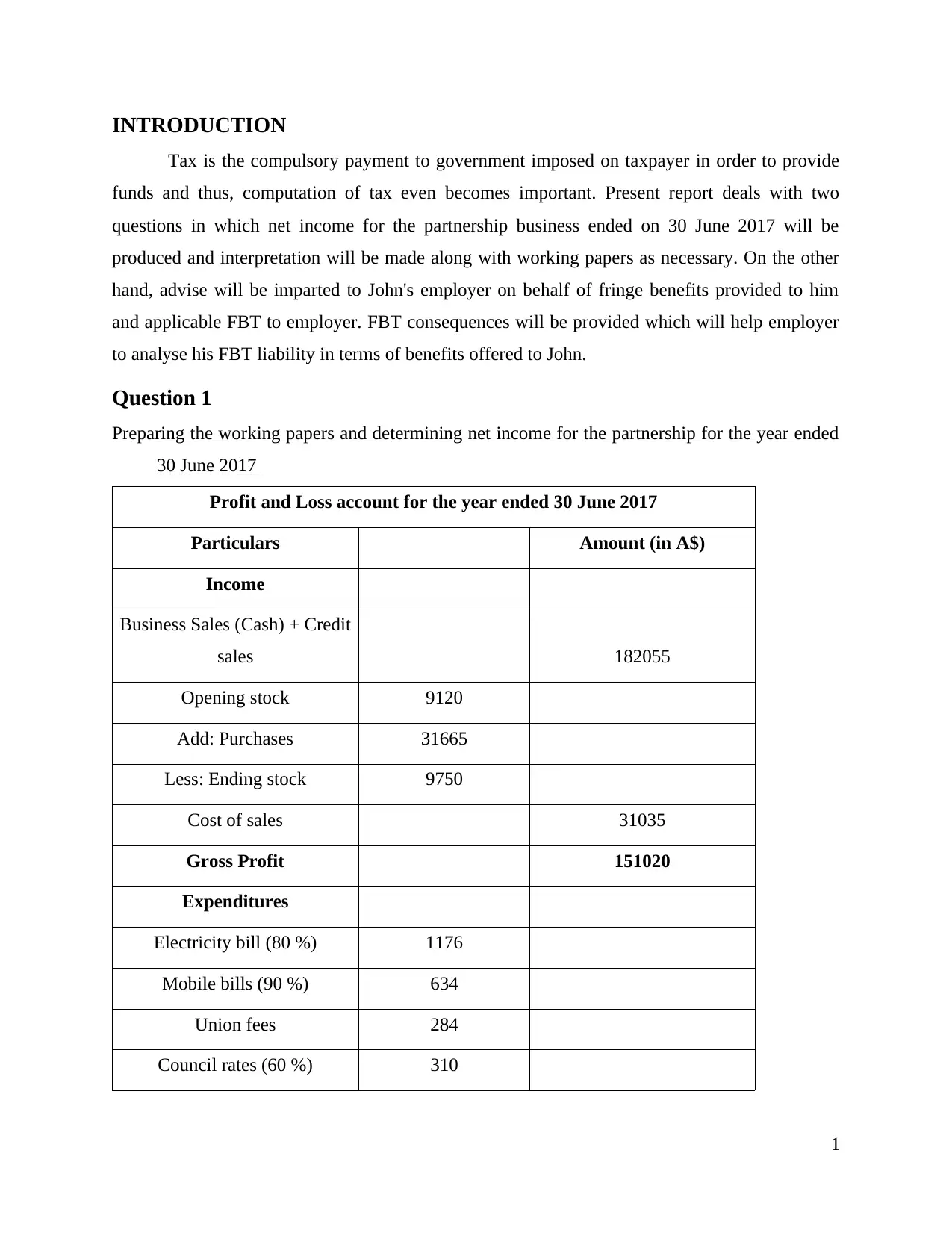

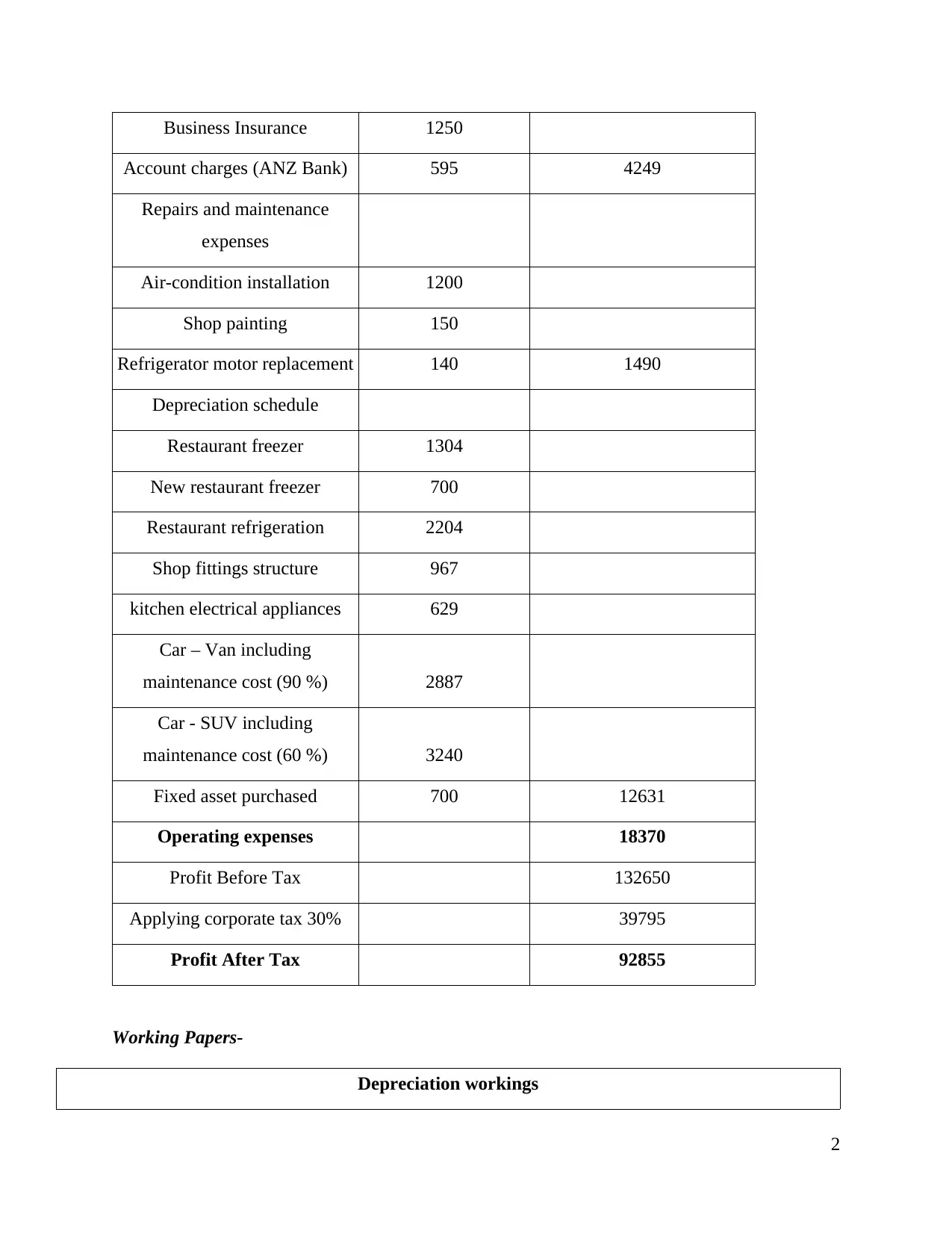

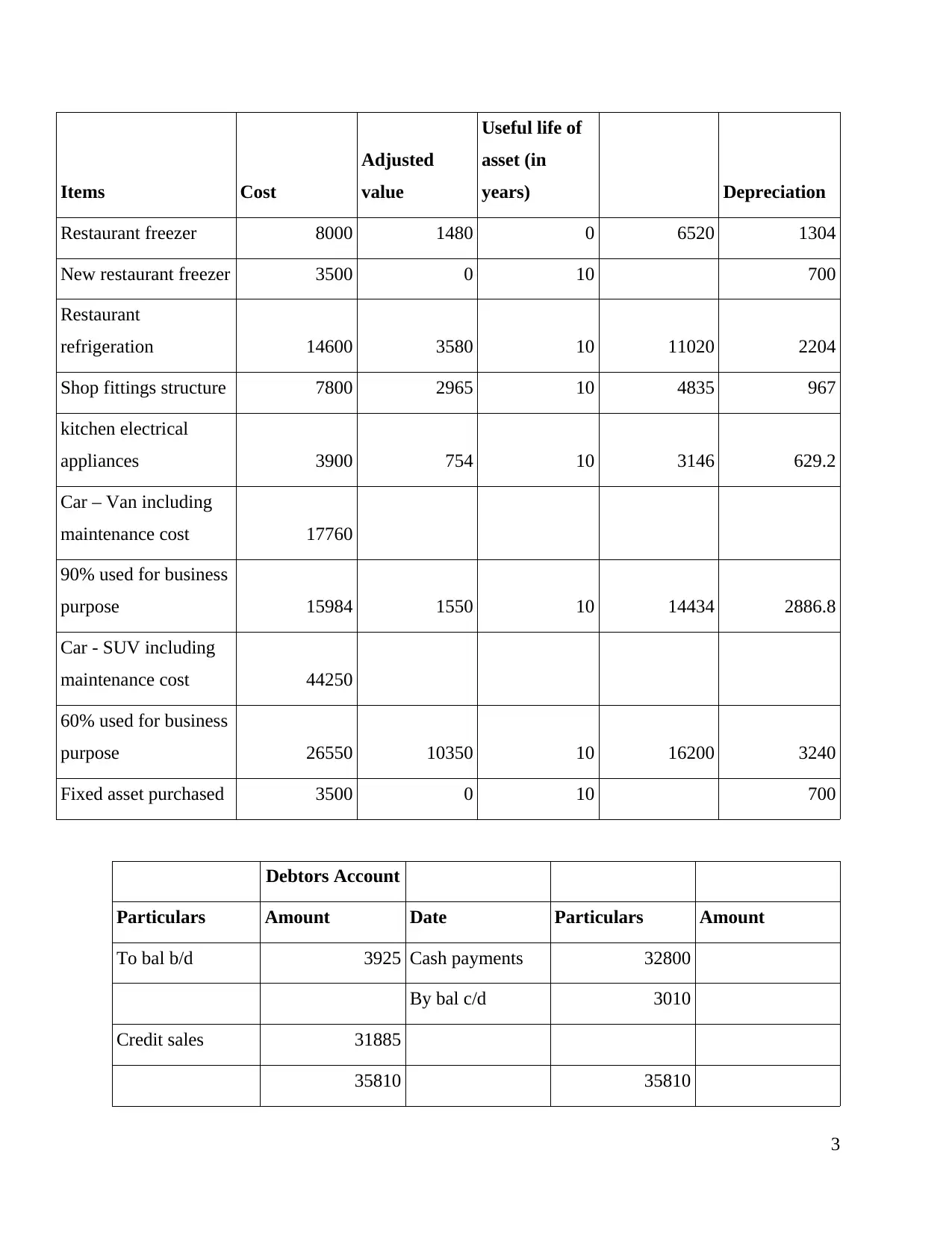

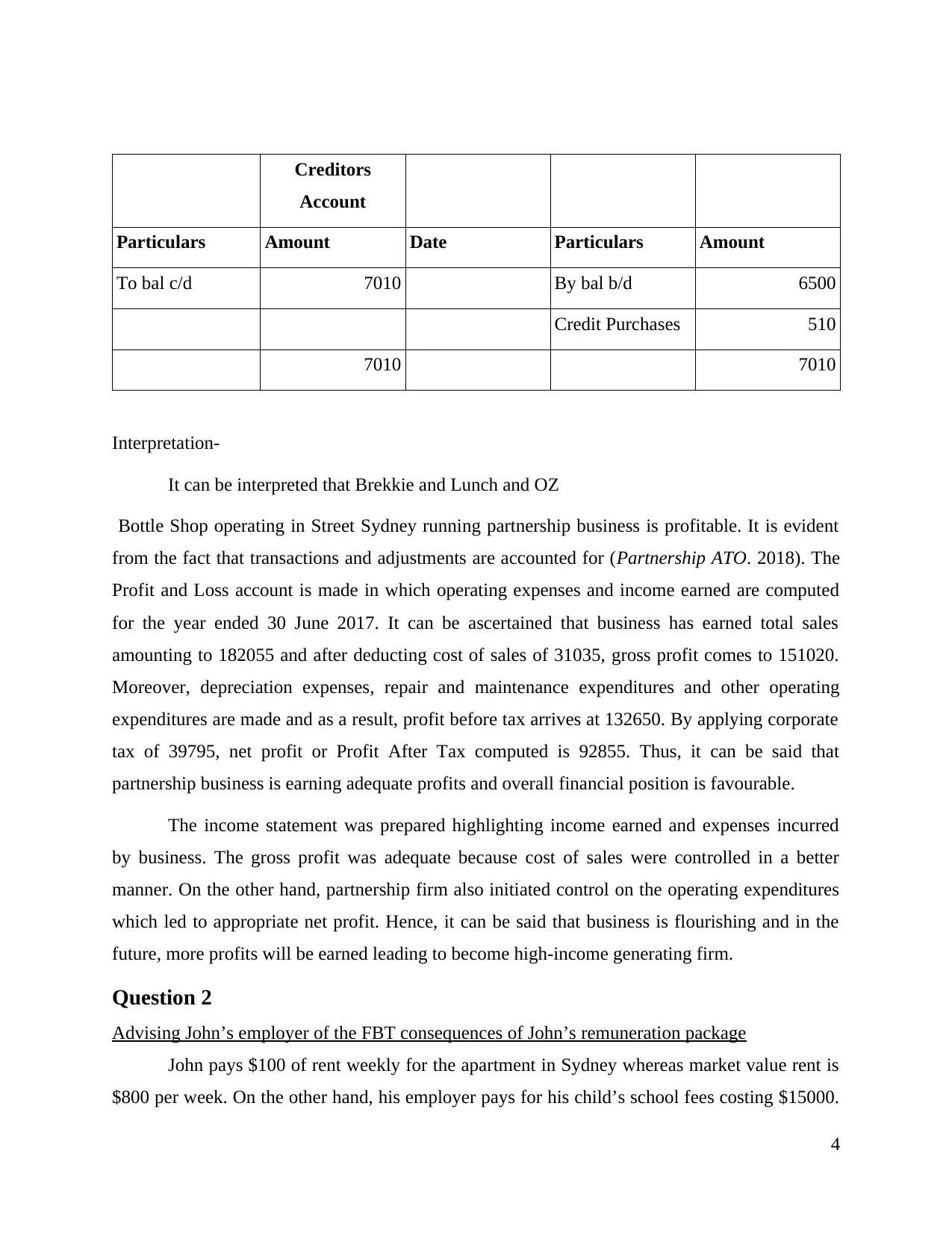

This assignment provides a comprehensive analysis of taxation, focusing on two key areas: calculating net income for a partnership business and advising an employer on the fringe benefits tax (FBT) consequences of an employee's remuneration package. The first part involves preparing working papers and determining the net income for Brekkie and Lunch and OZ Bottle Shop, a partnership operating in Sydney, for the year ended June 30, 2017. This includes constructing a profit and loss account, detailing income, cost of sales, operating expenses, and depreciation schedules to arrive at a profit before and after tax. The second part of the assignment advises John's employer on the FBT implications of providing benefits such as subsidized rent for an apartment and the payment of the employee's child's school fees. The analysis covers FBT consequences, including taxable values, reporting requirements, and potential tax liabilities. The report also highlights the importance of FBT in attracting and retaining employees, while also addressing various exemptions and deductions. The conclusion emphasizes the significance of tax in the economy and summarizes the key findings on partnership income and FBT implications.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.