Taxation Law Assignment on Income Tax, Partnership, and Avoidance

VerifiedAdded on 2023/06/05

|11

|2560

|243

Homework Assignment

AI Summary

This taxation law assignment addresses several key issues in Australian taxation. The first part examines the taxability of lottery winnings, concluding that the periodic payments are considered ordinary income subject to taxation under section 6-5, aligning with the ordinary concepts of income. The second part discusses the Westminster principle, emphasizing that courts should focus on the substance of transactions rather than solely on their form, and distinguishes between tax avoidance and tax evasion. The third part deals with the tax implications of a partnership between a husband and wife regarding investment property, concluding that, absent evidence of a formal partnership, the couple are co-owners and must share profits and losses equally, with private arrangements not altering their tax entitlements. The assignment references relevant case law and statutory provisions to support its conclusions.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to 1:...............................................................................................................................2

Answer to 2:...............................................................................................................................4

Answer 3:...................................................................................................................................4

Answer 4:...................................................................................................................................6

References:.................................................................................................................................9

Table of Contents

Answer to 1:...............................................................................................................................2

Answer to 2:...............................................................................................................................4

Answer 3:...................................................................................................................................4

Answer 4:...................................................................................................................................6

References:.................................................................................................................................9

2TAXATION LAW

Answer to 1:

Issue:

The case will address taxability of the annual receipts that the lottery winner receives

periodically and in a recurring manner. The issue would consider the tax position of the

lottery payment within the ordinary meaning of the income.

Rule:

In Australia the meaning of the income comprises of the earnings based on the

statutory and ordinary concepts. This generally includes the “section 6-5” that reflects

ordinary income as the earnings within the context of the ordinary concepts (Apps 2015). The

income as per the ordinary concepts evidently comprises of the employment, income from the

running of the business and from the performance of the services. When a taxpayer receives a

receipt from the lottery as the one-off prize are not treated as the income because they are

treated as the windfall gains (Ismer and Jescheck 2017). There are several taxpayers that have

put forward their argument that their activities does not attracts tax liability and hence not

taxable as the ordinary income.

The meaning of the ordinary income is dependent to certain extent on the natural

meaning of the term and also by the interpretation of the court in “Scott v CT (1935)”. In

judging the nature of the income noteworthy emphasis has been placed on the discussion of

the term income (Whittenburg, Gill and Altus-Buller 2015). The attributes of the income

includes the amount that represents gains from the business. Another attributes of income

includes the amounts that are received as the reward for the services rendered. The court in

“Commissioner of Taxation v Stone (2002)” held that the amounts that are gains from the

items that may have possessed the nature of income if it has been derived.

Answer to 1:

Issue:

The case will address taxability of the annual receipts that the lottery winner receives

periodically and in a recurring manner. The issue would consider the tax position of the

lottery payment within the ordinary meaning of the income.

Rule:

In Australia the meaning of the income comprises of the earnings based on the

statutory and ordinary concepts. This generally includes the “section 6-5” that reflects

ordinary income as the earnings within the context of the ordinary concepts (Apps 2015). The

income as per the ordinary concepts evidently comprises of the employment, income from the

running of the business and from the performance of the services. When a taxpayer receives a

receipt from the lottery as the one-off prize are not treated as the income because they are

treated as the windfall gains (Ismer and Jescheck 2017). There are several taxpayers that have

put forward their argument that their activities does not attracts tax liability and hence not

taxable as the ordinary income.

The meaning of the ordinary income is dependent to certain extent on the natural

meaning of the term and also by the interpretation of the court in “Scott v CT (1935)”. In

judging the nature of the income noteworthy emphasis has been placed on the discussion of

the term income (Whittenburg, Gill and Altus-Buller 2015). The attributes of the income

includes the amount that represents gains from the business. Another attributes of income

includes the amounts that are received as the reward for the services rendered. The court in

“Commissioner of Taxation v Stone (2002)” held that the amounts that are gains from the

items that may have possessed the nature of income if it has been derived.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Along with these factors there are the number of other common law that attributes

have been identified which helps in determining what constitutes the income. These includes

the decision in “FCT v Dixon (1952) 86 CLR 540” whether the receipts are earned or

whether the receipt are received periodically or in recurrence manner.

In ascertaining whether the payment is the income, the law court have created three

vital principles. This includes whether the payment should be treated as the income and must

be ascertained in agreement with the ordinary meaning (Kudrna 2016). Secondly, whether the

payment that is received as the income will be reliant on the close examination of the specific

facts and looking into the character of the payment that is received by the recipient. The third

test includes whether the payment should be made objectively.

Application:

This case requires significant emphasis on the annual payment made by the lotteries

to the winner. The payment made by lotteries commission is on the annual basis and requires

close examination of the specific facts and looking into the character of the payment that is

received by the recipient.

By the interpretation of the court in “Scott v CT (1935)” the $50,000 yearly payment

reflects ordinary income as the earnings within the context of the ordinary concepts (Chen

2017). The attributes of the income includes the amount that represents gains for the

recipient.

In context of the judgement made in the “Commissioner of Taxation v Stone (2002)”

the amount of $50,000 is the item of gains for the winner of the lottery (Cachia 2017).

Emphasis can be placed in the decision of court in “FCT v Dixon (1952) 86 CLR 540” to

explain that the sum of $50,000 because the sum was received periodically or in recurrence

manner.

Along with these factors there are the number of other common law that attributes

have been identified which helps in determining what constitutes the income. These includes

the decision in “FCT v Dixon (1952) 86 CLR 540” whether the receipts are earned or

whether the receipt are received periodically or in recurrence manner.

In ascertaining whether the payment is the income, the law court have created three

vital principles. This includes whether the payment should be treated as the income and must

be ascertained in agreement with the ordinary meaning (Kudrna 2016). Secondly, whether the

payment that is received as the income will be reliant on the close examination of the specific

facts and looking into the character of the payment that is received by the recipient. The third

test includes whether the payment should be made objectively.

Application:

This case requires significant emphasis on the annual payment made by the lotteries

to the winner. The payment made by lotteries commission is on the annual basis and requires

close examination of the specific facts and looking into the character of the payment that is

received by the recipient.

By the interpretation of the court in “Scott v CT (1935)” the $50,000 yearly payment

reflects ordinary income as the earnings within the context of the ordinary concepts (Chen

2017). The attributes of the income includes the amount that represents gains for the

recipient.

In context of the judgement made in the “Commissioner of Taxation v Stone (2002)”

the amount of $50,000 is the item of gains for the winner of the lottery (Cachia 2017).

Emphasis can be placed in the decision of court in “FCT v Dixon (1952) 86 CLR 540” to

explain that the sum of $50,000 because the sum was received periodically or in recurrence

manner.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Conclusion:

The case can be concluded under section 6-5 the payment is an income as per the

ordinary concepts and will be considered for taxation purpose. This is because the payment

reflects ordinary income as the earnings is surrounded by the context of the ordinary

concepts.

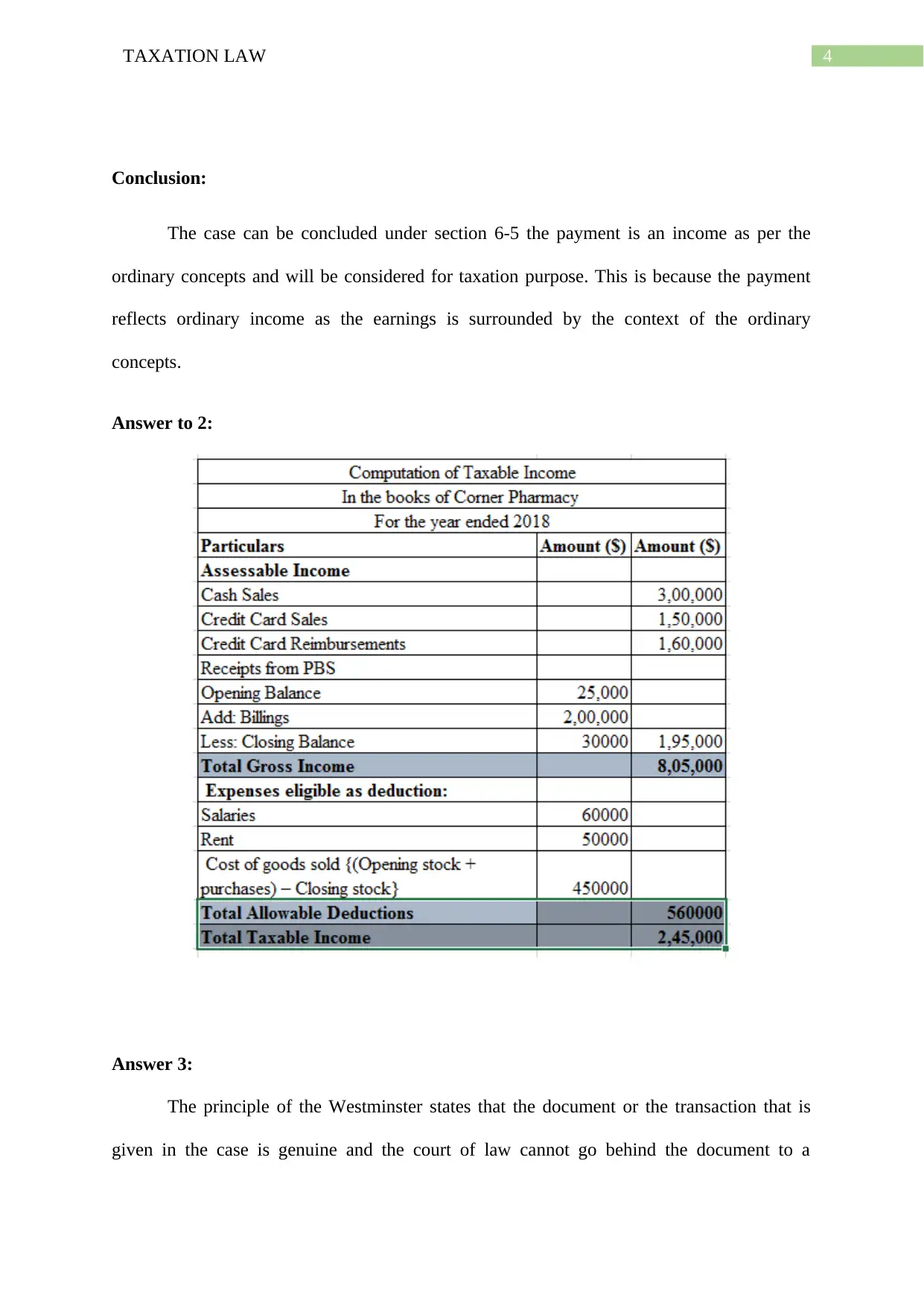

Answer to 2:

Answer 3:

The principle of the Westminster states that the document or the transaction that is

given in the case is genuine and the court of law cannot go behind the document to a

Conclusion:

The case can be concluded under section 6-5 the payment is an income as per the

ordinary concepts and will be considered for taxation purpose. This is because the payment

reflects ordinary income as the earnings is surrounded by the context of the ordinary

concepts.

Answer to 2:

Answer 3:

The principle of the Westminster states that the document or the transaction that is

given in the case is genuine and the court of law cannot go behind the document to a

5TAXATION LAW

particular hypothetical underlying material (Breen 2015). The principle has been reiterated in

subsequent English courts for judgements as the cardinal principle. In this case the gardener

of the duke was paid on weekly basis however to reduce the taxation liability the solicitors of

the duke made the deed in which the duke said that the earnings cannot be classified as the

real wages rather amounted as the yearly payment which was payable on the basis of weekly

instalments.

The judges in their opinion expressed that in revenues cases the court can ignore the

doctrine of the legal position and take into the regard the matter of substance (Aramayo

2016). The matter of substance in this case was the annuitant that was under the service of

Duke for something that was equivalent to his previous salary or wages. The case of

Westminster laid down the statutory interpretation instead of imposing the doctrine of tax

avoidance. Furthermore the court held that the principle of the Westminster does not forces

the court in looking into the document or the transaction that are under isolation from the

context to which it belonged.

Reference to the judgement can be made to state that transactions should be looked

just with a blinkers, it may be isolated to any context to which the transactions properly

belonged (Ohms and Olesen 2018). The duty of the court lies in determining the lawful

nature of the transactions that are sought for taxation purpose or the combination of taxation

from the series of transactions. The principles from the case of Westminster laid down that a

taxpayer had the right of administering their taxation affairs in order to reduce the taxation

and furthermore even though the purpose or the object of the transaction was to avoid the

taxation. This would certainly not invalidate the transactions until and unless the provision of

anti-avoidance is applied (Alldridge 2015). If it is noticed that the document or the

transaction is genuine and not fake under the traditional terms, the court will have follow the

forms of the transactions. The case analysis can be interpreted by stating that if there are any

particular hypothetical underlying material (Breen 2015). The principle has been reiterated in

subsequent English courts for judgements as the cardinal principle. In this case the gardener

of the duke was paid on weekly basis however to reduce the taxation liability the solicitors of

the duke made the deed in which the duke said that the earnings cannot be classified as the

real wages rather amounted as the yearly payment which was payable on the basis of weekly

instalments.

The judges in their opinion expressed that in revenues cases the court can ignore the

doctrine of the legal position and take into the regard the matter of substance (Aramayo

2016). The matter of substance in this case was the annuitant that was under the service of

Duke for something that was equivalent to his previous salary or wages. The case of

Westminster laid down the statutory interpretation instead of imposing the doctrine of tax

avoidance. Furthermore the court held that the principle of the Westminster does not forces

the court in looking into the document or the transaction that are under isolation from the

context to which it belonged.

Reference to the judgement can be made to state that transactions should be looked

just with a blinkers, it may be isolated to any context to which the transactions properly

belonged (Ohms and Olesen 2018). The duty of the court lies in determining the lawful

nature of the transactions that are sought for taxation purpose or the combination of taxation

from the series of transactions. The principles from the case of Westminster laid down that a

taxpayer had the right of administering their taxation affairs in order to reduce the taxation

and furthermore even though the purpose or the object of the transaction was to avoid the

taxation. This would certainly not invalidate the transactions until and unless the provision of

anti-avoidance is applied (Alldridge 2015). If it is noticed that the document or the

transaction is genuine and not fake under the traditional terms, the court will have follow the

forms of the transactions. The case analysis can be interpreted by stating that if there are any

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

two methods through which the transaction can effected and they result in difference in

consequences of taxation, the taxpayer can freely choose to adopt the method that would

result in lesser liability. The Westminster in the current situation eventually won the case.

The above stated discussion provides a clear difference between the tax avoidance and

tax evasion is yet prevalent in Australia. With the absence of any legislative guidelines there

is bound to be uncertainty. However to say that the principle of Westminster has been

escaped in Australia is a very tall statement and yet to be accepted in Australia (Rigoni 2017).

The case eventually provides the judges has placed their focus on the principle of statutory

interpretation instead of focusing on the overarching doctrine of anti-avoidance that is applied

on the taxation laws. The approach adopted in Ramsey is largely concerned with the statutory

interpretation of the avoidance of tax and the principles that is laid down in the case of

Westminster cannot be entirely said that it is go-by. Australian has undertaken general anti-

avoidance legislation that contains certain specific rules which would frustrate the tax payers

in exploiting the regimes of taxation. Currently the anti-avoidance rules that has been adopted

in Australia stipulates that the arrangements that have the purpose of tax avoidance will be

considered as void.

Answer 4:

Issue:

The issue in this case will be assessing the relationship of partnership between the

husband and the wife for division of net income and loss reported from the investment

property.

Rule:

The term partnership under the “Partnership Act section 1” states that the

relationship that is subsisting among the person that are carrying on the business under the

two methods through which the transaction can effected and they result in difference in

consequences of taxation, the taxpayer can freely choose to adopt the method that would

result in lesser liability. The Westminster in the current situation eventually won the case.

The above stated discussion provides a clear difference between the tax avoidance and

tax evasion is yet prevalent in Australia. With the absence of any legislative guidelines there

is bound to be uncertainty. However to say that the principle of Westminster has been

escaped in Australia is a very tall statement and yet to be accepted in Australia (Rigoni 2017).

The case eventually provides the judges has placed their focus on the principle of statutory

interpretation instead of focusing on the overarching doctrine of anti-avoidance that is applied

on the taxation laws. The approach adopted in Ramsey is largely concerned with the statutory

interpretation of the avoidance of tax and the principles that is laid down in the case of

Westminster cannot be entirely said that it is go-by. Australian has undertaken general anti-

avoidance legislation that contains certain specific rules which would frustrate the tax payers

in exploiting the regimes of taxation. Currently the anti-avoidance rules that has been adopted

in Australia stipulates that the arrangements that have the purpose of tax avoidance will be

considered as void.

Answer 4:

Issue:

The issue in this case will be assessing the relationship of partnership between the

husband and the wife for division of net income and loss reported from the investment

property.

Rule:

The term partnership under the “Partnership Act section 1” states that the

relationship that is subsisting among the person that are carrying on the business under the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

common intention of earning profits. The relationship of partnership is generally regarded as

the contractual (Coffee, Sale and Henderson 2015). Whether the partnership exists between

the parties should be taken to have intended, as understood not based on the terms of their

express agreement but based on the conduct towards one another all through the course of

performing of business. All the relevant facts and relevant situations of partnership should be

considered among the partners. An important statutory rules of co-ownership of the property

together with the joint tenancy do not itself establish a partnership as anything which is so

owned. The co-owners of the property employ the partnership rules with the objective of

profit and share the profits obtained through their employment.

As per the “section 51” no deduction is merely permitted by the virtue of the

agreement made among the taxpayer and his wife to indemnify their spouse for any kind of

losses (Lincoln 2017). It is regarded as the term of arrangement where the taxpayer usually

give away the income to their wife and does not includes any conditions of deductibility

under the “section 51 (1)”.

They court in “McDonald v FC of T (1987)” stated that there was no kind of

partnership between the parties in relation to the general law (Collins and Bey 2016). There

was only the mere investment in the property instead of partnership in their properties or their

profits. As the result of absence of any evidence, by virtue of their co-ownership they must

share profits and losses on equal basis. Their private arrangement cannot alter their respective

entitlement for the purpose of income tax.

Application:

The taxpayer here are Joseph and Jane that are owners of the property bought for

investment purpose. All the relevant facts and relevant situations of partnership between

Joseph and Jane has been considered. The co-owners of the property here Joseph and Jane

common intention of earning profits. The relationship of partnership is generally regarded as

the contractual (Coffee, Sale and Henderson 2015). Whether the partnership exists between

the parties should be taken to have intended, as understood not based on the terms of their

express agreement but based on the conduct towards one another all through the course of

performing of business. All the relevant facts and relevant situations of partnership should be

considered among the partners. An important statutory rules of co-ownership of the property

together with the joint tenancy do not itself establish a partnership as anything which is so

owned. The co-owners of the property employ the partnership rules with the objective of

profit and share the profits obtained through their employment.

As per the “section 51” no deduction is merely permitted by the virtue of the

agreement made among the taxpayer and his wife to indemnify their spouse for any kind of

losses (Lincoln 2017). It is regarded as the term of arrangement where the taxpayer usually

give away the income to their wife and does not includes any conditions of deductibility

under the “section 51 (1)”.

They court in “McDonald v FC of T (1987)” stated that there was no kind of

partnership between the parties in relation to the general law (Collins and Bey 2016). There

was only the mere investment in the property instead of partnership in their properties or their

profits. As the result of absence of any evidence, by virtue of their co-ownership they must

share profits and losses on equal basis. Their private arrangement cannot alter their respective

entitlement for the purpose of income tax.

Application:

The taxpayer here are Joseph and Jane that are owners of the property bought for

investment purpose. All the relevant facts and relevant situations of partnership between

Joseph and Jane has been considered. The co-owners of the property here Joseph and Jane

8TAXATION LAW

employed the partnership rules with the objective of profit and share the profits obtained

through their employment (Kanda and Levmore 2015). As per the “section 51” no deduction

is merely permitted by the virtue of the agreement made between Joseph and his wife to

indemnify his spouse for the losses of $40,000.

The arrangement between Joseph and his wife is regarded as the term of arrangement

where the taxpayer usually give away the income to his wife. Applying the principles of

“McDonald v FC of T (1987)” there was no kind of partnership between the husband and

wife in relation to the general law (Rabkin and Johnson 2016). There was only the mere

investment in the property by Joseph and Jane instead of partnership in their properties or

their incomes. In the absenteeism of any evidence, by virtue of their co-ownership Joseph and

Jane must share losses of $40,000 on equal basis. The private arrangement among the couples

cannot alter their respective entitlement for the purpose of income tax.

If they decide to sell the property any capital gains or capital loss thereof should be

shared equally as their private arraignment of sharing profits is void.

Conclusion:

The present case is merely related to the co-ownership rather than considering it as

partnerships. Their private entitlements is a merely partnership for income tax purpose.

employed the partnership rules with the objective of profit and share the profits obtained

through their employment (Kanda and Levmore 2015). As per the “section 51” no deduction

is merely permitted by the virtue of the agreement made between Joseph and his wife to

indemnify his spouse for the losses of $40,000.

The arrangement between Joseph and his wife is regarded as the term of arrangement

where the taxpayer usually give away the income to his wife. Applying the principles of

“McDonald v FC of T (1987)” there was no kind of partnership between the husband and

wife in relation to the general law (Rabkin and Johnson 2016). There was only the mere

investment in the property by Joseph and Jane instead of partnership in their properties or

their incomes. In the absenteeism of any evidence, by virtue of their co-ownership Joseph and

Jane must share losses of $40,000 on equal basis. The private arrangement among the couples

cannot alter their respective entitlement for the purpose of income tax.

If they decide to sell the property any capital gains or capital loss thereof should be

shared equally as their private arraignment of sharing profits is void.

Conclusion:

The present case is merely related to the co-ownership rather than considering it as

partnerships. Their private entitlements is a merely partnership for income tax purpose.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

References:

Alldridge, P., 2015. 13. Tax avoidance, tax evasion, money laundering and the problem of

‘offshore’. Greed, Corruption, and the Modern State: Essays in Political Economy, p.317.

Apps, P., 2015. The Central Role of a Well-Designed Income Tax in the Modern

Economy. Austl. Tax F., 30, p.845.

Aramayo, S.V., 2016. A Common GAAR to Protect the Harmonized Corporate Tax Base:

More Chaos in the Labyrinth. EC Tax Review, 25(1), pp.4-17.

Breen, O., 2015. Trustee Liability for Breach of Trust in the Common Law World.

Cachia, F., 2017. Aggressive Tax Planning: An Analysis from an EU Perspective. EC Tax

Review, 26(5), pp.257-273.

Chen, S., 2017. Do investors value corporate tax return information? Evidence from

Australia (Doctoral dissertation).

Coffee Jr, J.C., Sale, H. and Henderson, M.T., 2015. Securities regulation: Cases and

materials.

Collins, J.M. and Bey, R.P., 2016. The master limited partnership: an alternative to the

corporation. Financial Management, pp.5-14.

Ismer, R. and Jescheck, C., 2017. The Substantive Scope of Tax Treaties in a Post-BEPS

World: Article 2 OECD MC (Taxes Covered) and the Rise of New Taxes. Intertax, 45(5),

pp.382-390.

Kanda, H. and Levmore, S., 2015. Taxes, Agency Costs, and the Price of

Incorporation. Virginia Law Review, pp.211-256.

References:

Alldridge, P., 2015. 13. Tax avoidance, tax evasion, money laundering and the problem of

‘offshore’. Greed, Corruption, and the Modern State: Essays in Political Economy, p.317.

Apps, P., 2015. The Central Role of a Well-Designed Income Tax in the Modern

Economy. Austl. Tax F., 30, p.845.

Aramayo, S.V., 2016. A Common GAAR to Protect the Harmonized Corporate Tax Base:

More Chaos in the Labyrinth. EC Tax Review, 25(1), pp.4-17.

Breen, O., 2015. Trustee Liability for Breach of Trust in the Common Law World.

Cachia, F., 2017. Aggressive Tax Planning: An Analysis from an EU Perspective. EC Tax

Review, 26(5), pp.257-273.

Chen, S., 2017. Do investors value corporate tax return information? Evidence from

Australia (Doctoral dissertation).

Coffee Jr, J.C., Sale, H. and Henderson, M.T., 2015. Securities regulation: Cases and

materials.

Collins, J.M. and Bey, R.P., 2016. The master limited partnership: an alternative to the

corporation. Financial Management, pp.5-14.

Ismer, R. and Jescheck, C., 2017. The Substantive Scope of Tax Treaties in a Post-BEPS

World: Article 2 OECD MC (Taxes Covered) and the Rise of New Taxes. Intertax, 45(5),

pp.382-390.

Kanda, H. and Levmore, S., 2015. Taxes, Agency Costs, and the Price of

Incorporation. Virginia Law Review, pp.211-256.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Kudrna, G., 2016. Economy-wide effects of means-tested pensions: The case of

Australia. The Journal of the Economics of Ageing, 7, pp.17-29.

Lincoln, I.V., 2017. What are the Implications for Partnerships and Partnership Taxation

Under the Republican Proposals for Tax Reform.

Ohms, C. and Olesen, K., 2018. UBS AG v. IRC, DB Group Services (UK) Ltd v. IRC:

Fiscal Nullity and the Supreme Court. Statute Law Review.

Rabkin, J. and Johnson, M.H., 2016 The Partnership Under the Federal Tax Laws. Harv. L.

Rev., 55, p.909.

Rigoni, J.M.D.M., 2017. The International Tax Regime in the Twenty-First Century: The

Emergence of a Third Stage. Intertax, 45(3), pp.205-218.

Whittenburg, G.E., Gill, S. and Altus-Buller, M., 2015. Income Tax Fundamentals 2016.

Nelson Education.

Kudrna, G., 2016. Economy-wide effects of means-tested pensions: The case of

Australia. The Journal of the Economics of Ageing, 7, pp.17-29.

Lincoln, I.V., 2017. What are the Implications for Partnerships and Partnership Taxation

Under the Republican Proposals for Tax Reform.

Ohms, C. and Olesen, K., 2018. UBS AG v. IRC, DB Group Services (UK) Ltd v. IRC:

Fiscal Nullity and the Supreme Court. Statute Law Review.

Rabkin, J. and Johnson, M.H., 2016 The Partnership Under the Federal Tax Laws. Harv. L.

Rev., 55, p.909.

Rigoni, J.M.D.M., 2017. The International Tax Regime in the Twenty-First Century: The

Emergence of a Third Stage. Intertax, 45(3), pp.205-218.

Whittenburg, G.E., Gill, S. and Altus-Buller, M., 2015. Income Tax Fundamentals 2016.

Nelson Education.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.