Taxation Theory, Practice and Law Assignment - Finance Module

VerifiedAdded on 2020/04/07

|15

|2663

|373

Homework Assignment

AI Summary

This document presents a comprehensive solution to a Taxation Theory, Practice and Law assignment, addressing various aspects of tax law and financial principles. The assignment analyzes case studies focusing on capital gains and losses, fringe benefits tax, and loss distribution from rental property, referencing relevant sections of the ITAA 1997 and Taxation Rulings. It also examines tax avoidance strategies and the assessment of income from the sale of felled timber, providing detailed explanations and conclusions for each issue. The solution incorporates legal precedents and rulings, offering a thorough understanding of the complexities of taxation.

Running head: TAXATION THEORY, PRACTICE AND LAW

Taxation Theory, Practice and Law

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Taxation Theory, Practice and Law

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION THEORY, PRACTICE AND LAW

Table of Contents

Answer to Question 1:.....................................................................................................................3

Issue:............................................................................................................................................3

Laws:............................................................................................................................................3

Application:.................................................................................................................................4

Conclusion:..................................................................................................................................5

Answer to Question 2:.....................................................................................................................5

Issue:............................................................................................................................................5

Laws:............................................................................................................................................5

Application:.................................................................................................................................5

Conclusion:..................................................................................................................................8

Answer to Question 3:.....................................................................................................................8

Issue:............................................................................................................................................8

Laws:............................................................................................................................................8

Application:.................................................................................................................................8

Conclusion:................................................................................................................................10

Answer to Question 4:...................................................................................................................10

Answer to Question 5:...................................................................................................................11

Issue:..........................................................................................................................................11

Table of Contents

Answer to Question 1:.....................................................................................................................3

Issue:............................................................................................................................................3

Laws:............................................................................................................................................3

Application:.................................................................................................................................4

Conclusion:..................................................................................................................................5

Answer to Question 2:.....................................................................................................................5

Issue:............................................................................................................................................5

Laws:............................................................................................................................................5

Application:.................................................................................................................................5

Conclusion:..................................................................................................................................8

Answer to Question 3:.....................................................................................................................8

Issue:............................................................................................................................................8

Laws:............................................................................................................................................8

Application:.................................................................................................................................8

Conclusion:................................................................................................................................10

Answer to Question 4:...................................................................................................................10

Answer to Question 5:...................................................................................................................11

Issue:..........................................................................................................................................11

2TAXATION THEORY, PRACTICE AND LAW

Laws:..........................................................................................................................................11

Application:...............................................................................................................................11

Conclusion:................................................................................................................................12

References:....................................................................................................................................13

Laws:..........................................................................................................................................11

Application:...............................................................................................................................11

Conclusion:................................................................................................................................12

References:....................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION THEORY, PRACTICE AND LAW

Answer to Question 1:

Issue:

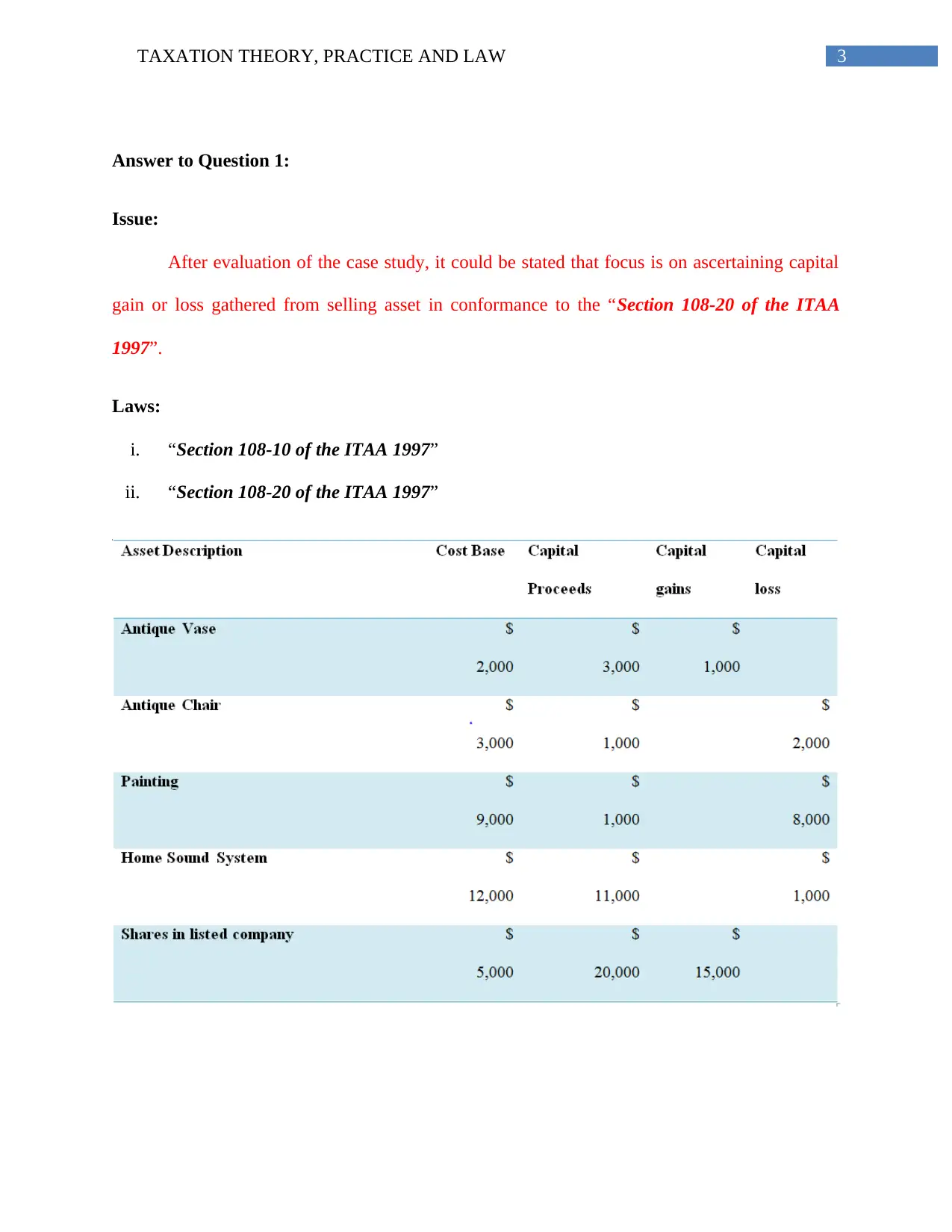

After evaluation of the case study, it could be stated that focus is on ascertaining capital

gain or loss gathered from selling asset in conformance to the “Section 108-20 of the ITAA

1997”.

Laws:

i. “Section 108-10 of the ITAA 1997”

ii. “Section 108-20 of the ITAA 1997”

Answer to Question 1:

Issue:

After evaluation of the case study, it could be stated that focus is on ascertaining capital

gain or loss gathered from selling asset in conformance to the “Section 108-20 of the ITAA

1997”.

Laws:

i. “Section 108-10 of the ITAA 1997”

ii. “Section 108-20 of the ITAA 1997”

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION THEORY, PRACTICE AND LAW

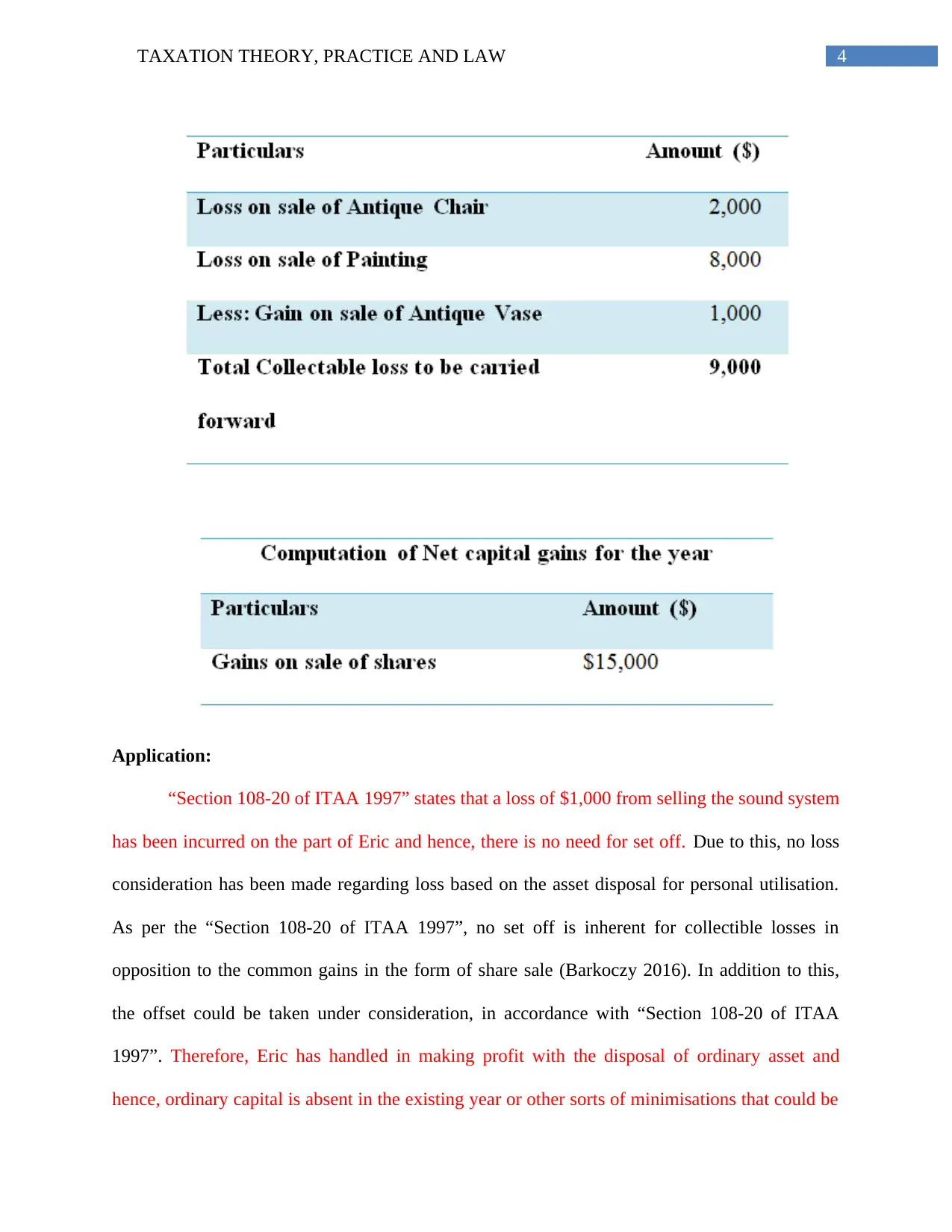

Application:

“Section 108-20 of ITAA 1997” states that a loss of $1,000 from selling the sound system

has been incurred on the part of Eric and hence, there is no need for set off. Due to this, no loss

consideration has been made regarding loss based on the asset disposal for personal utilisation.

As per the “Section 108-20 of ITAA 1997”, no set off is inherent for collectible losses in

opposition to the common gains in the form of share sale (Barkoczy 2016). In addition to this,

the offset could be taken under consideration, in accordance with “Section 108-20 of ITAA

1997”. Therefore, Eric has handled in making profit with the disposal of ordinary asset and

hence, ordinary capital is absent in the existing year or other sorts of minimisations that could be

Application:

“Section 108-20 of ITAA 1997” states that a loss of $1,000 from selling the sound system

has been incurred on the part of Eric and hence, there is no need for set off. Due to this, no loss

consideration has been made regarding loss based on the asset disposal for personal utilisation.

As per the “Section 108-20 of ITAA 1997”, no set off is inherent for collectible losses in

opposition to the common gains in the form of share sale (Barkoczy 2016). In addition to this,

the offset could be taken under consideration, in accordance with “Section 108-20 of ITAA

1997”. Therefore, Eric has handled in making profit with the disposal of ordinary asset and

hence, ordinary capital is absent in the existing year or other sorts of minimisations that could be

5TAXATION THEORY, PRACTICE AND LAW

applied (Snape and De Souza 2016). $15,000 has been obtained as the overall capital gain in the

context of Eric.

Conclusion:

Based on the above discussion, it could be concluded that the entire loss could not be

offset on the part of Eric, which are obtained from the collectibles. This is because the profit is

earned through disposal of the ordinary assets solely.

Answer to Question 2:

Issue:

Based on the case study, it could be stated that the particular issue focuses on ascertaining

the fringe benefits tax with adherence to the “Taxation Ruling of TR 93/6”.

Laws:

i. “Taxation Ruling of TR 93/6”

Application:

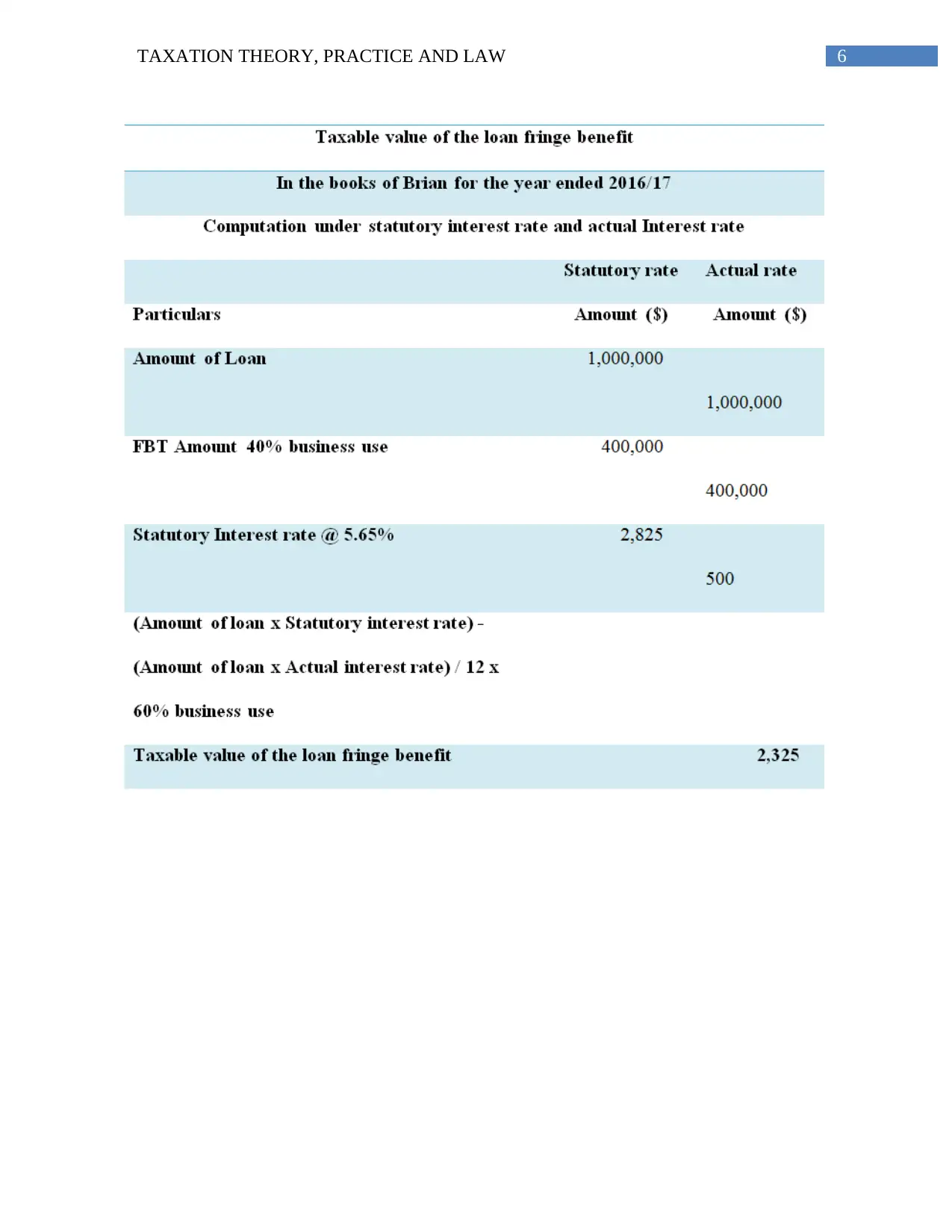

Computation of fringe tax benefits (FBT):

applied (Snape and De Souza 2016). $15,000 has been obtained as the overall capital gain in the

context of Eric.

Conclusion:

Based on the above discussion, it could be concluded that the entire loss could not be

offset on the part of Eric, which are obtained from the collectibles. This is because the profit is

earned through disposal of the ordinary assets solely.

Answer to Question 2:

Issue:

Based on the case study, it could be stated that the particular issue focuses on ascertaining

the fringe benefits tax with adherence to the “Taxation Ruling of TR 93/6”.

Laws:

i. “Taxation Ruling of TR 93/6”

Application:

Computation of fringe tax benefits (FBT):

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION THEORY, PRACTICE AND LAW

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION THEORY, PRACTICE AND LAW

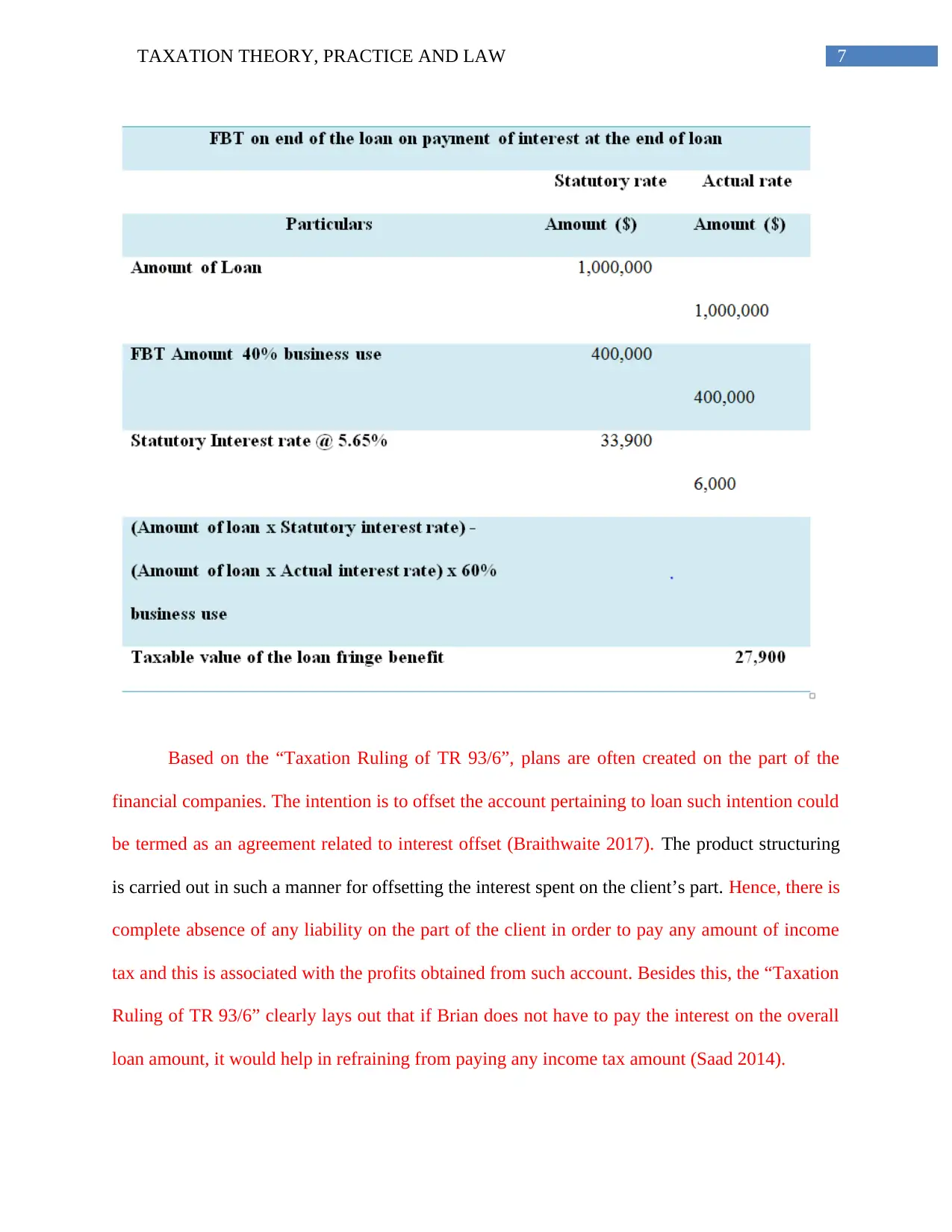

Based on the “Taxation Ruling of TR 93/6”, plans are often created on the part of the

financial companies. The intention is to offset the account pertaining to loan such intention could

be termed as an agreement related to interest offset (Braithwaite 2017). The product structuring

is carried out in such a manner for offsetting the interest spent on the client’s part. Hence, there is

complete absence of any liability on the part of the client in order to pay any amount of income

tax and this is associated with the profits obtained from such account. Besides this, the “Taxation

Ruling of TR 93/6” clearly lays out that if Brian does not have to pay the interest on the overall

loan amount, it would help in refraining from paying any income tax amount (Saad 2014).

Based on the “Taxation Ruling of TR 93/6”, plans are often created on the part of the

financial companies. The intention is to offset the account pertaining to loan such intention could

be termed as an agreement related to interest offset (Braithwaite 2017). The product structuring

is carried out in such a manner for offsetting the interest spent on the client’s part. Hence, there is

complete absence of any liability on the part of the client in order to pay any amount of income

tax and this is associated with the profits obtained from such account. Besides this, the “Taxation

Ruling of TR 93/6” clearly lays out that if Brian does not have to pay the interest on the overall

loan amount, it would help in refraining from paying any income tax amount (Saad 2014).

8TAXATION THEORY, PRACTICE AND LAW

Conclusion:

Based on the above evaluation, it is evident that there is no need for Brian to pay any

liability of income tax, if the bank excuses the individual to refrain from repaying the overall

interest amount on loan.

Answer to Question 3:

Issue:

After critical assessment of the provided case, it has been evaluated that this particular

issue deals with the loss distribution accumulated from rental property. Jack and Jill jointly own

the stated rental property, as identified from the case study.

Laws:

“Taxation Ruling of TR 93/32”

“Section 51 of ITAA 1997”

“F.C. of T v McDonald (1987)”

Application:

Based on the “Taxation Ruling of TR 93/32”, it could be stated that description has been

provided in relation to divisionary loss or gain from the property between the above two stated

owners (Taylor and Richardson 2013). Besides this, the ruling is taken into account mainly with

analysing the taxable condition of the owners, which could not be held accountable to conduct

the values pertaining to actions. The present scenario of Jack and Jill takes into account

assessment of the taxable condition in relation to the rental property. Jill is the owner of 90% of

the rental property and Jack is the owner of the remaining 10% of the rental property.

Conclusion:

Based on the above evaluation, it is evident that there is no need for Brian to pay any

liability of income tax, if the bank excuses the individual to refrain from repaying the overall

interest amount on loan.

Answer to Question 3:

Issue:

After critical assessment of the provided case, it has been evaluated that this particular

issue deals with the loss distribution accumulated from rental property. Jack and Jill jointly own

the stated rental property, as identified from the case study.

Laws:

“Taxation Ruling of TR 93/32”

“Section 51 of ITAA 1997”

“F.C. of T v McDonald (1987)”

Application:

Based on the “Taxation Ruling of TR 93/32”, it could be stated that description has been

provided in relation to divisionary loss or gain from the property between the above two stated

owners (Taylor and Richardson 2013). Besides this, the ruling is taken into account mainly with

analysing the taxable condition of the owners, which could not be held accountable to conduct

the values pertaining to actions. The present scenario of Jack and Jill takes into account

assessment of the taxable condition in relation to the rental property. Jill is the owner of 90% of

the rental property and Jack is the owner of the remaining 10% of the rental property.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION THEORY, PRACTICE AND LAW

According to the “Taxation Ruling TR 92/32”, the shared ownership of the property is

adjudged as income tax partnership. However, this could not be considered as a sole partnership

under the general law along with the ownership accounts to carry out value for any business

practice. According to the case study, shared partnership is called the partnership for satisfying

the income tax purpose only (Petty et al. 2015). The loss suffered due to the property is managed

through shared property ownership along with the apportionment of gains accumulated from

losses and partnership. The existing scenario of Jack and Jill denotes the joint ownership

between these two persons in relation to rental property depending on income tax. In addition,

this could not be considered as partnership in line with the general law (Novikov, Ling and

Kordzakhia 2014).

As per the “Taxation Ruling of TR 92/32”, the joint property owners could not be stated

as partners, since the general law does not permit the same. The provided case clearly lays out

that agreement could be made either orally or in writing and there would be absence of any

impact on the shared value of the gain or loss obtained from such property. Henceforth, Jill and

Jack would cling on to the asset in the form of shared renters based on a sole common influential

dynamic (Lang 2014).

It has been observed from “F.C. of T v McDonald (1987) ATR 957” that the person

incurring tax and his wife have the legal right on two strata units. These units are associated with

the title in the form of joint renters. There has been an inveterate agreement between the two

parties and the agreement states that 25% of the overall income would be handed over to Mr

McDonald and the remaining would be provided to Mrs McDonald. In this particular case, Mr

McDonald needs to bear the entire loss amount (Bird and Zolt 2014).

According to the “Taxation Ruling TR 92/32”, the shared ownership of the property is

adjudged as income tax partnership. However, this could not be considered as a sole partnership

under the general law along with the ownership accounts to carry out value for any business

practice. According to the case study, shared partnership is called the partnership for satisfying

the income tax purpose only (Petty et al. 2015). The loss suffered due to the property is managed

through shared property ownership along with the apportionment of gains accumulated from

losses and partnership. The existing scenario of Jack and Jill denotes the joint ownership

between these two persons in relation to rental property depending on income tax. In addition,

this could not be considered as partnership in line with the general law (Novikov, Ling and

Kordzakhia 2014).

As per the “Taxation Ruling of TR 92/32”, the joint property owners could not be stated

as partners, since the general law does not permit the same. The provided case clearly lays out

that agreement could be made either orally or in writing and there would be absence of any

impact on the shared value of the gain or loss obtained from such property. Henceforth, Jill and

Jack would cling on to the asset in the form of shared renters based on a sole common influential

dynamic (Lang 2014).

It has been observed from “F.C. of T v McDonald (1987) ATR 957” that the person

incurring tax and his wife have the legal right on two strata units. These units are associated with

the title in the form of joint renters. There has been an inveterate agreement between the two

parties and the agreement states that 25% of the overall income would be handed over to Mr

McDonald and the remaining would be provided to Mrs McDonald. In this particular case, Mr

McDonald needs to bear the entire loss amount (Bird and Zolt 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION THEORY, PRACTICE AND LAW

Conclusion:

The above evaluation clearly states that the loss needs to be allocated equally on the part

of Jack and Jill, and shared ownership could not be taken into account in the form of partnership

business.

Answer to Question 4:

The incidence associated with avoiding tax is laid and this is adhered to the “IRC v Duke

of Westminster [1936] AC 1”. The formulation of a doctrine is inherent in this case and it

denotes all individuals are permitted for affair orders in order to allow the taxation assignment

and this has been depicted in the Fitting Act. Such distribution of taxation is lower as opposed to

the same (Douglas et al. 2014). There has been depiction of court instance in future phases,

which are greatly restrictive and these are adopted in accordance with the “WT Ramsay v IRC

principle”. The transaction has been pre-arranged artificially and the provision of service is for

commercial purpose (Davis et al. 2015). The effective regulation is to impose tax for extension

of the transactions as entire fact.

In the current situation, the principles within nation represent that if an individual

achieves success in obtaining the outcomes, the Inland Revenue might be of the move and they

could not be allowed to spend any increased amount of tax (Kerin and Findlay 2015). Excepting

this, the organisations and individuals are enabled to modify the financial reports in relation to

stagnant objectives for reducing the liabilities of tax depending on the overall tax structure.

Conclusion:

The above evaluation clearly states that the loss needs to be allocated equally on the part

of Jack and Jill, and shared ownership could not be taken into account in the form of partnership

business.

Answer to Question 4:

The incidence associated with avoiding tax is laid and this is adhered to the “IRC v Duke

of Westminster [1936] AC 1”. The formulation of a doctrine is inherent in this case and it

denotes all individuals are permitted for affair orders in order to allow the taxation assignment

and this has been depicted in the Fitting Act. Such distribution of taxation is lower as opposed to

the same (Douglas et al. 2014). There has been depiction of court instance in future phases,

which are greatly restrictive and these are adopted in accordance with the “WT Ramsay v IRC

principle”. The transaction has been pre-arranged artificially and the provision of service is for

commercial purpose (Davis et al. 2015). The effective regulation is to impose tax for extension

of the transactions as entire fact.

In the current situation, the principles within nation represent that if an individual

achieves success in obtaining the outcomes, the Inland Revenue might be of the move and they

could not be allowed to spend any increased amount of tax (Kerin and Findlay 2015). Excepting

this, the organisations and individuals are enabled to modify the financial reports in relation to

stagnant objectives for reducing the liabilities of tax depending on the overall tax structure.

11TAXATION THEORY, PRACTICE AND LAW

Answer to Question 5:

Issue:

According to the current situation, the income assessment from sale of felled timber is

analysed according to “Subsection 6(1) of the Income Tax Assessment Act 1936”.

Laws:

“McCauley v The Federal Commissioner of Taxation”

“Subsection 6(1) of the Income Tax Assessment Act 1936”

Application:

In the existing situation, it has been observed that Bill owns a large land where large pine

trees are present. Bill aimed to use the land in order to graze sheep, as the intention is to clear the

same. The individual has found out a logging firm that pay $1,000 for every 100 metres of

timber. In exchange of this transaction, the firm could obtain a portion of the property of Bill.

According to the “Taxation Ruling TR 95/6”, the consequences of income tax have been laid out

in relation to the generation of primary activities of forestry and production (Richardson, Taylor

and Lanis 2013). Such ruling gives the limit to which the receipts have been gathered from

selling timber. Such aspect constitutes of assessable income in ascertaining whether there is

involvement of the taxpayers into the activities of primary sector. According to “Subsection 6 (1)

of the Income Tax Assessment Act 1936”, there is involvement of the taxpayers into the

activities of forest operations considered as the primary sector.

In compliance with “Subsection 6 (1) of the Income Tax Assessment Act 1936”, the

primary production is explained as the planting of trees within plantation required for felling

forest (Tran-Nam, Evans and Lignier 2014). As observed from the case study, Bill is considered

Answer to Question 5:

Issue:

According to the current situation, the income assessment from sale of felled timber is

analysed according to “Subsection 6(1) of the Income Tax Assessment Act 1936”.

Laws:

“McCauley v The Federal Commissioner of Taxation”

“Subsection 6(1) of the Income Tax Assessment Act 1936”

Application:

In the existing situation, it has been observed that Bill owns a large land where large pine

trees are present. Bill aimed to use the land in order to graze sheep, as the intention is to clear the

same. The individual has found out a logging firm that pay $1,000 for every 100 metres of

timber. In exchange of this transaction, the firm could obtain a portion of the property of Bill.

According to the “Taxation Ruling TR 95/6”, the consequences of income tax have been laid out

in relation to the generation of primary activities of forestry and production (Richardson, Taylor

and Lanis 2013). Such ruling gives the limit to which the receipts have been gathered from

selling timber. Such aspect constitutes of assessable income in ascertaining whether there is

involvement of the taxpayers into the activities of primary sector. According to “Subsection 6 (1)

of the Income Tax Assessment Act 1936”, there is involvement of the taxpayers into the

activities of forest operations considered as the primary sector.

In compliance with “Subsection 6 (1) of the Income Tax Assessment Act 1936”, the

primary production is explained as the planting of trees within plantation required for felling

forest (Tran-Nam, Evans and Lignier 2014). As observed from the case study, Bill is considered

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.