Taxation Theory, Practice, and Law: Comprehensive Report and Analysis

VerifiedAdded on 2020/06/04

|9

|2252

|38

Report

AI Summary

This report provides a detailed analysis of taxation theory, practice, and law through the examination of several case studies. The report begins by exploring capital gains tax, analyzing how it applies to the sale of assets held for varying periods, and the tax implications for individuals. It then delves into the intricacies of fringe benefits tax, explaining how these benefits are calculated and taxed, including loan benefits and interest rates. The report also examines tax avoidance strategies, such as those involving contracts and the allocation of income, highlighting the legal and practical aspects. Furthermore, it explores the taxation of revenue generated from forest operations, differentiating between those who actively engage in these operations and those who receive income from timber sales. The report utilizes case studies, supporting evidence, and critical analysis to offer a comprehensive understanding of the subject matter, referencing relevant tax laws and policies. The report concludes by summarizing key findings and implications of the various taxation scenarios discussed.

Taxation Theory, Practice

and Law

and Law

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Question 1........................................................................................................................................1

Introduction.................................................................................................................................1

Critical analysis...........................................................................................................................1

Supporting evidence....................................................................................................................1

Conclusion...................................................................................................................................2

Question 2........................................................................................................................................2

Introduction ................................................................................................................................2

Critical analysis...........................................................................................................................2

Supportive evidence....................................................................................................................3

Conclusion...................................................................................................................................3

Question 3........................................................................................................................................4

Introduction.................................................................................................................................4

Critical analysis...........................................................................................................................4

Supporting evidence....................................................................................................................4

Conclusion...................................................................................................................................4

Question 4........................................................................................................................................4

Introduction.................................................................................................................................4

Critical analysis...........................................................................................................................5

Supporting evidence....................................................................................................................5

Conclusion...................................................................................................................................5

Question 5........................................................................................................................................5

Introduction.................................................................................................................................5

Critical analysis...........................................................................................................................5

Supporting evidence....................................................................................................................6

Conclusion...................................................................................................................................6

REFERENCES................................................................................................................................7

Question 1........................................................................................................................................1

Introduction.................................................................................................................................1

Critical analysis...........................................................................................................................1

Supporting evidence....................................................................................................................1

Conclusion...................................................................................................................................2

Question 2........................................................................................................................................2

Introduction ................................................................................................................................2

Critical analysis...........................................................................................................................2

Supportive evidence....................................................................................................................3

Conclusion...................................................................................................................................3

Question 3........................................................................................................................................4

Introduction.................................................................................................................................4

Critical analysis...........................................................................................................................4

Supporting evidence....................................................................................................................4

Conclusion...................................................................................................................................4

Question 4........................................................................................................................................4

Introduction.................................................................................................................................4

Critical analysis...........................................................................................................................5

Supporting evidence....................................................................................................................5

Conclusion...................................................................................................................................5

Question 5........................................................................................................................................5

Introduction.................................................................................................................................5

Critical analysis...........................................................................................................................5

Supporting evidence....................................................................................................................6

Conclusion...................................................................................................................................6

REFERENCES................................................................................................................................7

Question 1.

Introduction

In order to gain capital, profit is the important aspect which arise after selling of assets. It

can be done in two ways such as long and short run. It is performed for more than 36 months so

that long term gain will be arise. Hereafter, tax is payable to assess cost of the acquisition and tax

is made. When assets is acquired for less than 36 months, tax will be imposed directly.

Critical analysis

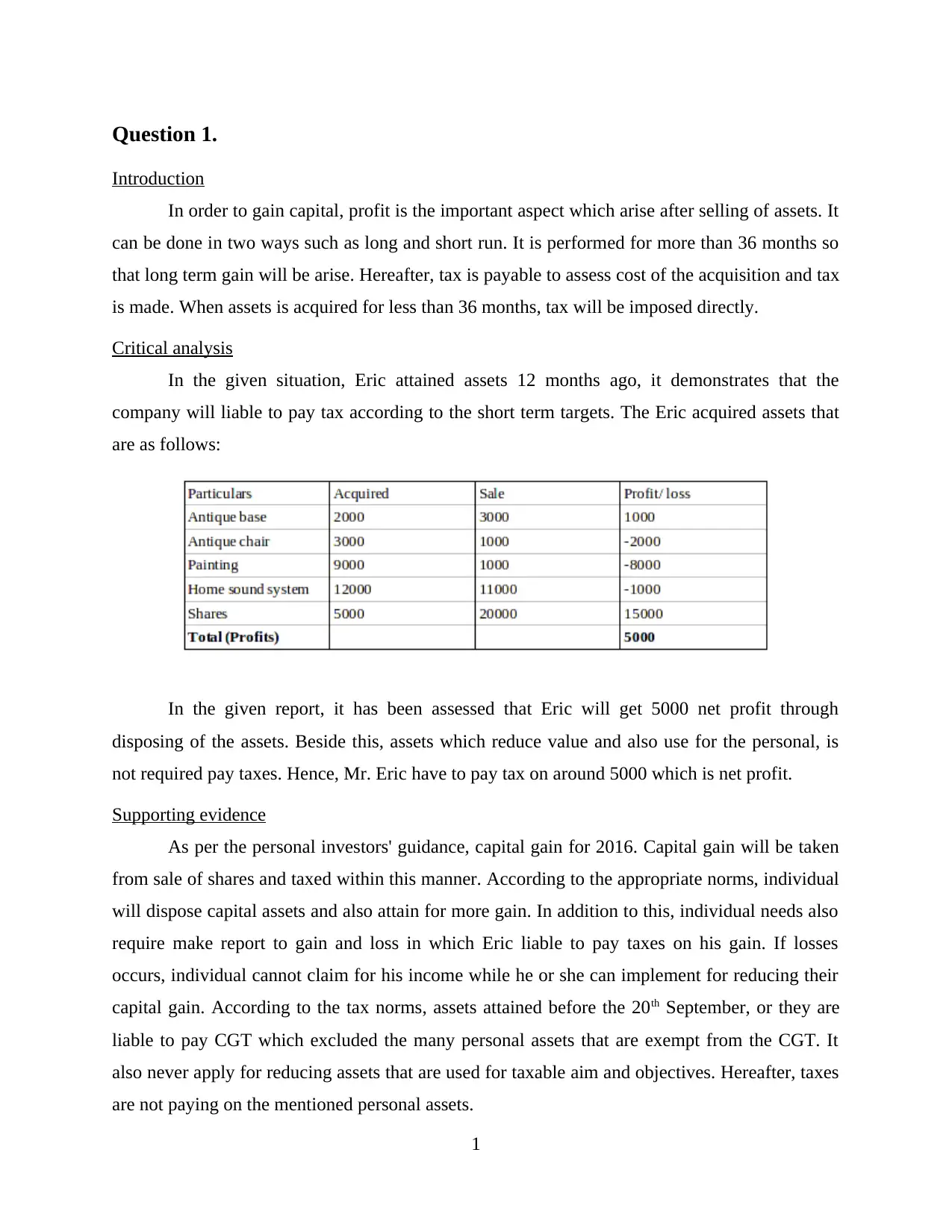

In the given situation, Eric attained assets 12 months ago, it demonstrates that the

company will liable to pay tax according to the short term targets. The Eric acquired assets that

are as follows:

In the given report, it has been assessed that Eric will get 5000 net profit through

disposing of the assets. Beside this, assets which reduce value and also use for the personal, is

not required pay taxes. Hence, Mr. Eric have to pay tax on around 5000 which is net profit.

Supporting evidence

As per the personal investors' guidance, capital gain for 2016. Capital gain will be taken

from sale of shares and taxed within this manner. According to the appropriate norms, individual

will dispose capital assets and also attain for more gain. In addition to this, individual needs also

require make report to gain and loss in which Eric liable to pay taxes on his gain. If losses

occurs, individual cannot claim for his income while he or she can implement for reducing their

capital gain. According to the tax norms, assets attained before the 20th September, or they are

liable to pay CGT which excluded the many personal assets that are exempt from the CGT. It

also never apply for reducing assets that are used for taxable aim and objectives. Hereafter, taxes

are not paying on the mentioned personal assets.

1

Introduction

In order to gain capital, profit is the important aspect which arise after selling of assets. It

can be done in two ways such as long and short run. It is performed for more than 36 months so

that long term gain will be arise. Hereafter, tax is payable to assess cost of the acquisition and tax

is made. When assets is acquired for less than 36 months, tax will be imposed directly.

Critical analysis

In the given situation, Eric attained assets 12 months ago, it demonstrates that the

company will liable to pay tax according to the short term targets. The Eric acquired assets that

are as follows:

In the given report, it has been assessed that Eric will get 5000 net profit through

disposing of the assets. Beside this, assets which reduce value and also use for the personal, is

not required pay taxes. Hence, Mr. Eric have to pay tax on around 5000 which is net profit.

Supporting evidence

As per the personal investors' guidance, capital gain for 2016. Capital gain will be taken

from sale of shares and taxed within this manner. According to the appropriate norms, individual

will dispose capital assets and also attain for more gain. In addition to this, individual needs also

require make report to gain and loss in which Eric liable to pay taxes on his gain. If losses

occurs, individual cannot claim for his income while he or she can implement for reducing their

capital gain. According to the tax norms, assets attained before the 20th September, or they are

liable to pay CGT which excluded the many personal assets that are exempt from the CGT. It

also never apply for reducing assets that are used for taxable aim and objectives. Hereafter, taxes

are not paying on the mentioned personal assets.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Conclusion

In this report, it can be summarized that capital gain taxes payable according to the norms

that are included in income tax laws. Therefore, first time assessment require for disposing value

and then it will be reduce cost of attained in the best aspect.

Question 2.

Introduction

With the help of fringe, there are many benefits determines towards employers which

gives positive results to employees. These benefits excluded salary and wages packages. It is also

different from the income and calculate apart from income tax. On the valuable fringe benefits,

loan can be discussed to create several benefits at workplace. Brian employer provided three year

loan on the basis of @1% tax per annum. It assists to reduce actual benchmark rate.

Critical analysis

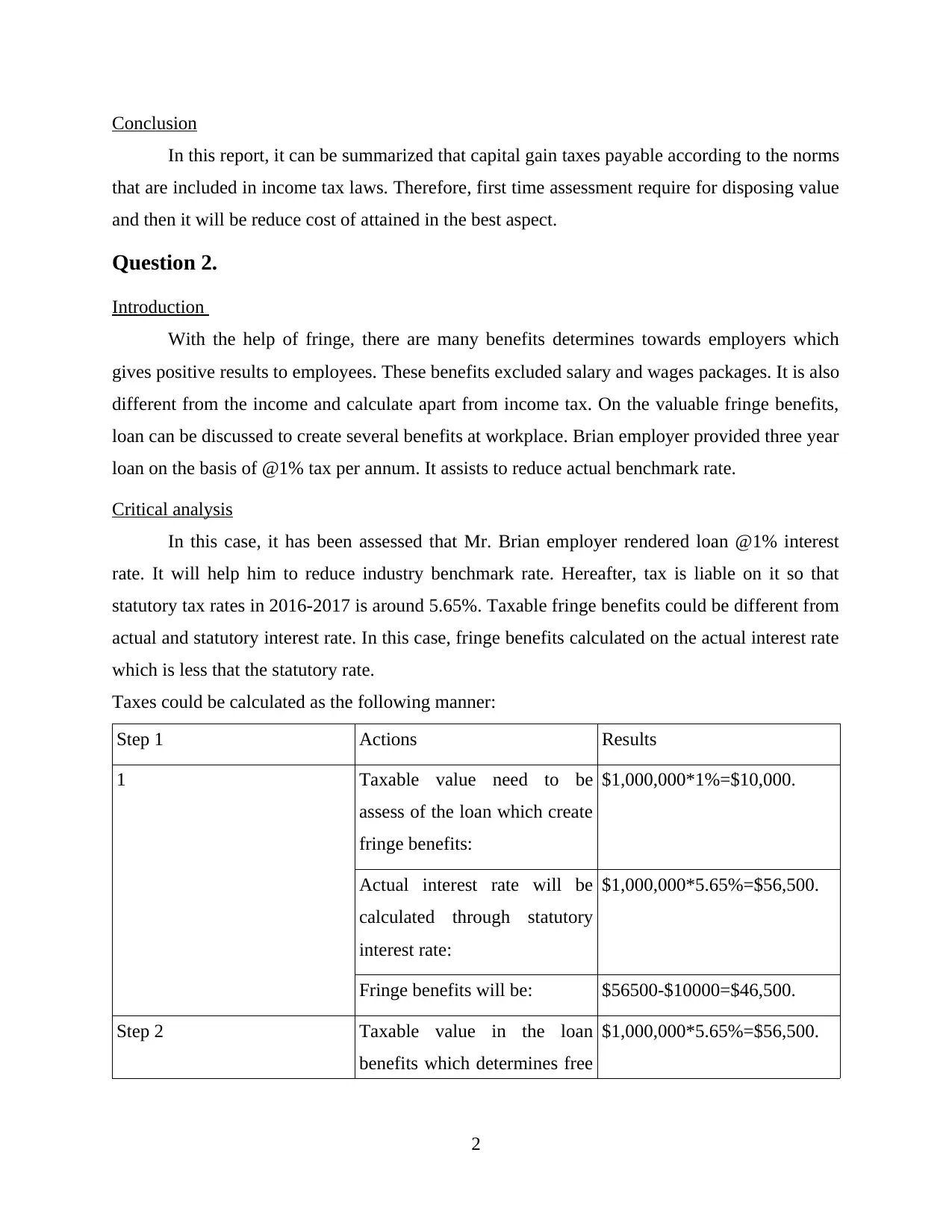

In this case, it has been assessed that Mr. Brian employer rendered loan @1% interest

rate. It will help him to reduce industry benchmark rate. Hereafter, tax is liable on it so that

statutory tax rates in 2016-2017 is around 5.65%. Taxable fringe benefits could be different from

actual and statutory interest rate. In this case, fringe benefits calculated on the actual interest rate

which is less that the statutory rate.

Taxes could be calculated as the following manner:

Step 1 Actions Results

1 Taxable value need to be

assess of the loan which create

fringe benefits:

$1,000,000*1%=$10,000.

Actual interest rate will be

calculated through statutory

interest rate:

$1,000,000*5.65%=$56,500.

Fringe benefits will be: $56500-$10000=$46,500.

Step 2 Taxable value in the loan

benefits which determines free

$1,000,000*5.65%=$56,500.

2

In this report, it can be summarized that capital gain taxes payable according to the norms

that are included in income tax laws. Therefore, first time assessment require for disposing value

and then it will be reduce cost of attained in the best aspect.

Question 2.

Introduction

With the help of fringe, there are many benefits determines towards employers which

gives positive results to employees. These benefits excluded salary and wages packages. It is also

different from the income and calculate apart from income tax. On the valuable fringe benefits,

loan can be discussed to create several benefits at workplace. Brian employer provided three year

loan on the basis of @1% tax per annum. It assists to reduce actual benchmark rate.

Critical analysis

In this case, it has been assessed that Mr. Brian employer rendered loan @1% interest

rate. It will help him to reduce industry benchmark rate. Hereafter, tax is liable on it so that

statutory tax rates in 2016-2017 is around 5.65%. Taxable fringe benefits could be different from

actual and statutory interest rate. In this case, fringe benefits calculated on the actual interest rate

which is less that the statutory rate.

Taxes could be calculated as the following manner:

Step 1 Actions Results

1 Taxable value need to be

assess of the loan which create

fringe benefits:

$1,000,000*1%=$10,000.

Actual interest rate will be

calculated through statutory

interest rate:

$1,000,000*5.65%=$56,500.

Fringe benefits will be: $56500-$10000=$46,500.

Step 2 Taxable value in the loan

benefits which determines free

$1,000,000*5.65%=$56,500.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

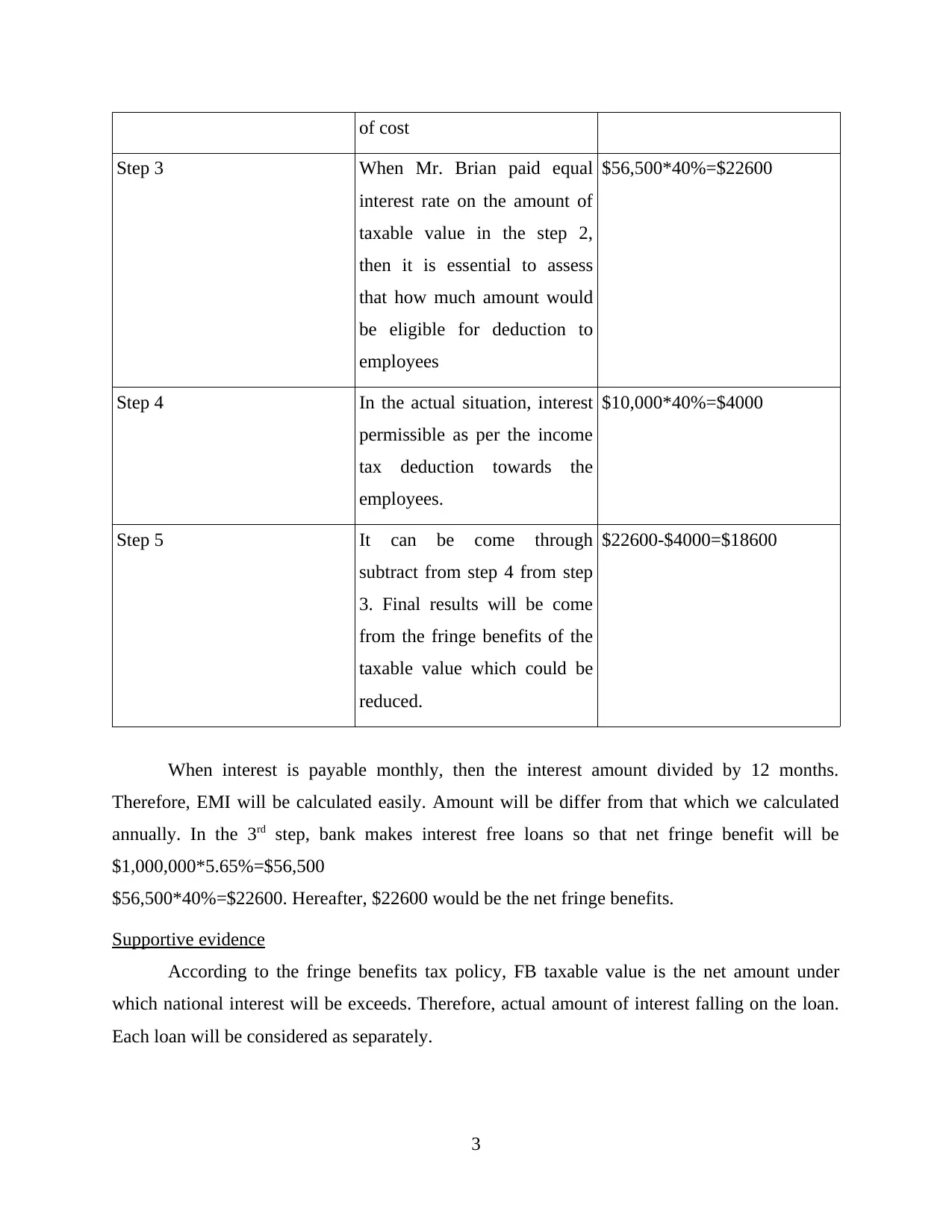

of cost

Step 3 When Mr. Brian paid equal

interest rate on the amount of

taxable value in the step 2,

then it is essential to assess

that how much amount would

be eligible for deduction to

employees

$56,500*40%=$22600

Step 4 In the actual situation, interest

permissible as per the income

tax deduction towards the

employees.

$10,000*40%=$4000

Step 5 It can be come through

subtract from step 4 from step

3. Final results will be come

from the fringe benefits of the

taxable value which could be

reduced.

$22600-$4000=$18600

When interest is payable monthly, then the interest amount divided by 12 months.

Therefore, EMI will be calculated easily. Amount will be differ from that which we calculated

annually. In the 3rd step, bank makes interest free loans so that net fringe benefit will be

$1,000,000*5.65%=$56,500

$56,500*40%=$22600. Hereafter, $22600 would be the net fringe benefits.

Supportive evidence

According to the fringe benefits tax policy, FB taxable value is the net amount under

which national interest will be exceeds. Therefore, actual amount of interest falling on the loan.

Each loan will be considered as separately.

3

Step 3 When Mr. Brian paid equal

interest rate on the amount of

taxable value in the step 2,

then it is essential to assess

that how much amount would

be eligible for deduction to

employees

$56,500*40%=$22600

Step 4 In the actual situation, interest

permissible as per the income

tax deduction towards the

employees.

$10,000*40%=$4000

Step 5 It can be come through

subtract from step 4 from step

3. Final results will be come

from the fringe benefits of the

taxable value which could be

reduced.

$22600-$4000=$18600

When interest is payable monthly, then the interest amount divided by 12 months.

Therefore, EMI will be calculated easily. Amount will be differ from that which we calculated

annually. In the 3rd step, bank makes interest free loans so that net fringe benefit will be

$1,000,000*5.65%=$56,500

$56,500*40%=$22600. Hereafter, $22600 would be the net fringe benefits.

Supportive evidence

According to the fringe benefits tax policy, FB taxable value is the net amount under

which national interest will be exceeds. Therefore, actual amount of interest falling on the loan.

Each loan will be considered as separately.

3

Conclusion

Fringe benefits are those which allotted by the employer towards employees. On the

behalf of this, employee paid tax on fringe benefit taxable amount. In addition to this, employee

need to reduce fringe benefits taxable value which is notional interest on loan. It will be

permissible as income tax deduction towards employees.

Question 3

Introduction

In this case, Jack and Jill borrowed amount for purchasing rental properly. They both

agreeing to make contract for which they agreed to share profit in ratio of 9:1. The loss is to be

bear by the Jack only. It makes for the purpose to avoid liability. In the last year, property occur

$10000 loss.

Critical analysis

In this case, people made contract to avoid tax liabilities. As results, it has been seen that

Jill housewife which is dependent lady (Verdier and Voeten, 2014). Therefore, her income

clubbed under the Jack assessment. Hence, covenant is made for lowering tax liabilities and

income which is covered by Jack. If the property incurred loss in last year, such loss will be carry

forward for the last year.

Supporting evidence

According to the tax laws of the nation, one person cannot make benefits for which they

are talk about. As results, tax is to be paid to gain capital amount which going to entitle.

Conclusion

In this give case, it can be concluded that tax is paid by Jack on capital gain for what he

earns from assets. In the last year, loss also set off form to gain capital and arise for the sale of

assets (Capital gain tax on property. 2017).

Question 4

Introduction

As per the Duke of Westminster's, it is based on the tax avoidance, they executed that

deed of conveyance is lad to servant which includes national helpers, gardeners, etc. In the

special deed, Duke decided to pay some amount for those services which he was rendering

4

Fringe benefits are those which allotted by the employer towards employees. On the

behalf of this, employee paid tax on fringe benefit taxable amount. In addition to this, employee

need to reduce fringe benefits taxable value which is notional interest on loan. It will be

permissible as income tax deduction towards employees.

Question 3

Introduction

In this case, Jack and Jill borrowed amount for purchasing rental properly. They both

agreeing to make contract for which they agreed to share profit in ratio of 9:1. The loss is to be

bear by the Jack only. It makes for the purpose to avoid liability. In the last year, property occur

$10000 loss.

Critical analysis

In this case, people made contract to avoid tax liabilities. As results, it has been seen that

Jill housewife which is dependent lady (Verdier and Voeten, 2014). Therefore, her income

clubbed under the Jack assessment. Hence, covenant is made for lowering tax liabilities and

income which is covered by Jack. If the property incurred loss in last year, such loss will be carry

forward for the last year.

Supporting evidence

According to the tax laws of the nation, one person cannot make benefits for which they

are talk about. As results, tax is to be paid to gain capital amount which going to entitle.

Conclusion

In this give case, it can be concluded that tax is paid by Jack on capital gain for what he

earns from assets. In the last year, loss also set off form to gain capital and arise for the sale of

assets (Capital gain tax on property. 2017).

Question 4

Introduction

As per the Duke of Westminster's, it is based on the tax avoidance, they executed that

deed of conveyance is lad to servant which includes national helpers, gardeners, etc. In the

special deed, Duke decided to pay some amount for those services which he was rendering

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Valente, 2017). In the written letter, it need to be send to the servants which pay for

remuneration on priority. Further, services performed by servant as the domestic helper. In this

analysing situations, Duke decided to claim for payment for tax deduction in preparation for tax

avoidance.

Critical analysis

This deed is known as the contract for same as the legal document that require for mutual

consents for more than one people (Davis, Guenther and Williams, 2015). It is generally used to

give perfect ways to transfer such property. Basic relation in deed and contract is that deed is

which written and design from third party sealed. An agreement must be require make contract

that is not needed to be enforceable. In the several cases, deed make for long term duration as the

easy contract.

Supporting evidence

As per the above case, major issues lies on the deed of written agreements which seen or

burned under the employment contract. Duke not pay to the gardeners and servants as per weekly

wages. Therefore, monthly salary is mentioned under the employment contract (Dafflon, 2015).

There is no consideration needed or made towards contract which said to be one major factors in

development.

Conclusion

The overall case recommended about the tax avoidance which could be allow in long

term cases in which enactment law followed. In this way, principles amount of the specific

format of the agreements can reduce tax liabilities (Posner, 2014).

Question 5

Introduction

Revenue is the generated through giving land to produce timber. It has been done through

cutting different pine trees. In this way, it has been found that Mr. Bill wants to clear land. In this

way, company paying him $1000 for the timber of 100 meters. It could be comes for taxation

ruling 95/6. Primary production and forestry, covers the receipts' comes from the sale of timber

that make accessible income (Dietsch and Rixen, 2014).

5

remuneration on priority. Further, services performed by servant as the domestic helper. In this

analysing situations, Duke decided to claim for payment for tax deduction in preparation for tax

avoidance.

Critical analysis

This deed is known as the contract for same as the legal document that require for mutual

consents for more than one people (Davis, Guenther and Williams, 2015). It is generally used to

give perfect ways to transfer such property. Basic relation in deed and contract is that deed is

which written and design from third party sealed. An agreement must be require make contract

that is not needed to be enforceable. In the several cases, deed make for long term duration as the

easy contract.

Supporting evidence

As per the above case, major issues lies on the deed of written agreements which seen or

burned under the employment contract. Duke not pay to the gardeners and servants as per weekly

wages. Therefore, monthly salary is mentioned under the employment contract (Dafflon, 2015).

There is no consideration needed or made towards contract which said to be one major factors in

development.

Conclusion

The overall case recommended about the tax avoidance which could be allow in long

term cases in which enactment law followed. In this way, principles amount of the specific

format of the agreements can reduce tax liabilities (Posner, 2014).

Question 5

Introduction

Revenue is the generated through giving land to produce timber. It has been done through

cutting different pine trees. In this way, it has been found that Mr. Bill wants to clear land. In this

way, company paying him $1000 for the timber of 100 meters. It could be comes for taxation

ruling 95/6. Primary production and forestry, covers the receipts' comes from the sale of timber

that make accessible income (Dietsch and Rixen, 2014).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Critical analysis

In this case, Mr. Bill not engaged with forest operations but ultimately engage in order to

dispose the operations. Therefore, he is not liable to pay taxes on the amount which he gets from

the company (Mumford, 2017). In this activity, forest operations are not covered. Beside this,

Mr, Bill will get $50000 lump sump amount to pre assumed the assessable amount. In this

activity, forest operations included and liable to pay taxes which reflect to the answer.

Supporting evidence

In these circumstances' taxation ruling and its applicable things need to be included for a

person who not occupied for the selling of forest operations. If any person receives loyalty for

removing the trees from the land, he never comes under the conducting operations for forest

(Stiglitz and Rosengard, 2015).

Conclusion

From the above case, it can be observed that Mr. Bill not carrying forest operations at

first time. Therefore, revenue earned by them which would not be liable to pay taxes. In the other

case, Mr Bill getting $50000 for permitting logging company.

6

In this case, Mr. Bill not engaged with forest operations but ultimately engage in order to

dispose the operations. Therefore, he is not liable to pay taxes on the amount which he gets from

the company (Mumford, 2017). In this activity, forest operations are not covered. Beside this,

Mr, Bill will get $50000 lump sump amount to pre assumed the assessable amount. In this

activity, forest operations included and liable to pay taxes which reflect to the answer.

Supporting evidence

In these circumstances' taxation ruling and its applicable things need to be included for a

person who not occupied for the selling of forest operations. If any person receives loyalty for

removing the trees from the land, he never comes under the conducting operations for forest

(Stiglitz and Rosengard, 2015).

Conclusion

From the above case, it can be observed that Mr. Bill not carrying forest operations at

first time. Therefore, revenue earned by them which would not be liable to pay taxes. In the other

case, Mr Bill getting $50000 for permitting logging company.

6

REFERENCES

Books and Journals

Dafflon, B., 2015. The assignment of functions to decentralized government: from theory to

practice. Handbook of multilevel finance, Edward Elgar, Cheltenham, pp.163-199.

Davis, A.K., Guenther, D.A. and Williams, B.M., 2015. Do socially responsible firms pay more

taxes?. The Accounting Review. 91(1). pp.47-68.

Dietsch, P. and Rixen, T., 2014. Tax competition and global background justice. Journal of

Political Philosophy. 22(2). pp.150-177.

Mumford, A., 2017. Taxing culture: towards a theory of tax collection law. Routledge.

Posner, R.A., 2014. Economic analysis of law. Wolters Kluwer Law & Business.

Stiglitz, J.E. and Rosengard, J.K., 2015. Economics of the Public Sector: Fourth International

Student Edition. WW Norton & Company.

Valente, C., 2017. The theory and practice of revolt in medieval England. Routledge.

Verdier, P.H. and Voeten, E., 2014. Precedent, compliance, and change in customary

international law: An explanatory theory. American Journal of International Law. 108(3).

pp.389-434.

Online

Capital gain tax on property. 2017. [Online]. Available

through:<http://www.which.co.uk/money/tax/capital-gains-tax/guides/capital-gains-tax-

on-property>. [Accessed on 18 th September, 2017].

7

Books and Journals

Dafflon, B., 2015. The assignment of functions to decentralized government: from theory to

practice. Handbook of multilevel finance, Edward Elgar, Cheltenham, pp.163-199.

Davis, A.K., Guenther, D.A. and Williams, B.M., 2015. Do socially responsible firms pay more

taxes?. The Accounting Review. 91(1). pp.47-68.

Dietsch, P. and Rixen, T., 2014. Tax competition and global background justice. Journal of

Political Philosophy. 22(2). pp.150-177.

Mumford, A., 2017. Taxing culture: towards a theory of tax collection law. Routledge.

Posner, R.A., 2014. Economic analysis of law. Wolters Kluwer Law & Business.

Stiglitz, J.E. and Rosengard, J.K., 2015. Economics of the Public Sector: Fourth International

Student Edition. WW Norton & Company.

Valente, C., 2017. The theory and practice of revolt in medieval England. Routledge.

Verdier, P.H. and Voeten, E., 2014. Precedent, compliance, and change in customary

international law: An explanatory theory. American Journal of International Law. 108(3).

pp.389-434.

Online

Capital gain tax on property. 2017. [Online]. Available

through:<http://www.which.co.uk/money/tax/capital-gains-tax/guides/capital-gains-tax-

on-property>. [Accessed on 18 th September, 2017].

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.