Taxation Laws and Principles: Australian Tax System Analysis

VerifiedAdded on 2020/02/19

|11

|3557

|31

Homework Assignment

AI Summary

This assignment delves into the Australian taxation system, utilizing five case studies to illustrate the implications of taxation laws and principles. The analysis considers the Income Tax Assessment Act 1997 and relevant legislation. Task 1 examines short-term capital gains or losses. Task 2 assesses fringe benefits tax related to a bank executive's loan. Task 3 explores partnership taxation between a couple. Task 4 analyzes the IRC vs. Duke of Westminster case, focusing on tax deductibility. The assignment provides a comprehensive understanding of various aspects of Australian taxation, including capital gains, fringe benefits, partnership agreements, and legal precedents.

TAXATION LAWS AND PRINCIPLES

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of contents

Introduction......................................................................................................................................3

Task 1...............................................................................................................................................3

Task 2...............................................................................................................................................4

Task 3...............................................................................................................................................5

Task 4...............................................................................................................................................7

Task 5...............................................................................................................................................8

Conclusion.......................................................................................................................................9

Reference list.................................................................................................................................10

2

Introduction......................................................................................................................................3

Task 1...............................................................................................................................................3

Task 2...............................................................................................................................................4

Task 3...............................................................................................................................................5

Task 4...............................................................................................................................................7

Task 5...............................................................................................................................................8

Conclusion.......................................................................................................................................9

Reference list.................................................................................................................................10

2

Introduction

In the study, it has been decided to show the taxation system of Australia, taking the help of the

five different case studies. With this given case reference, it is said to obtain complete sense of

implication of taxation as well as it has been decided that the principles of governing body and

certain legislation to be reviewed for the purpose of reconciling the rules and laws with that of

the case studies. In addition, principles laid in the Income Tax Assessment Act 1997 of Australia

will also be considered for the fine judgment of the case references.

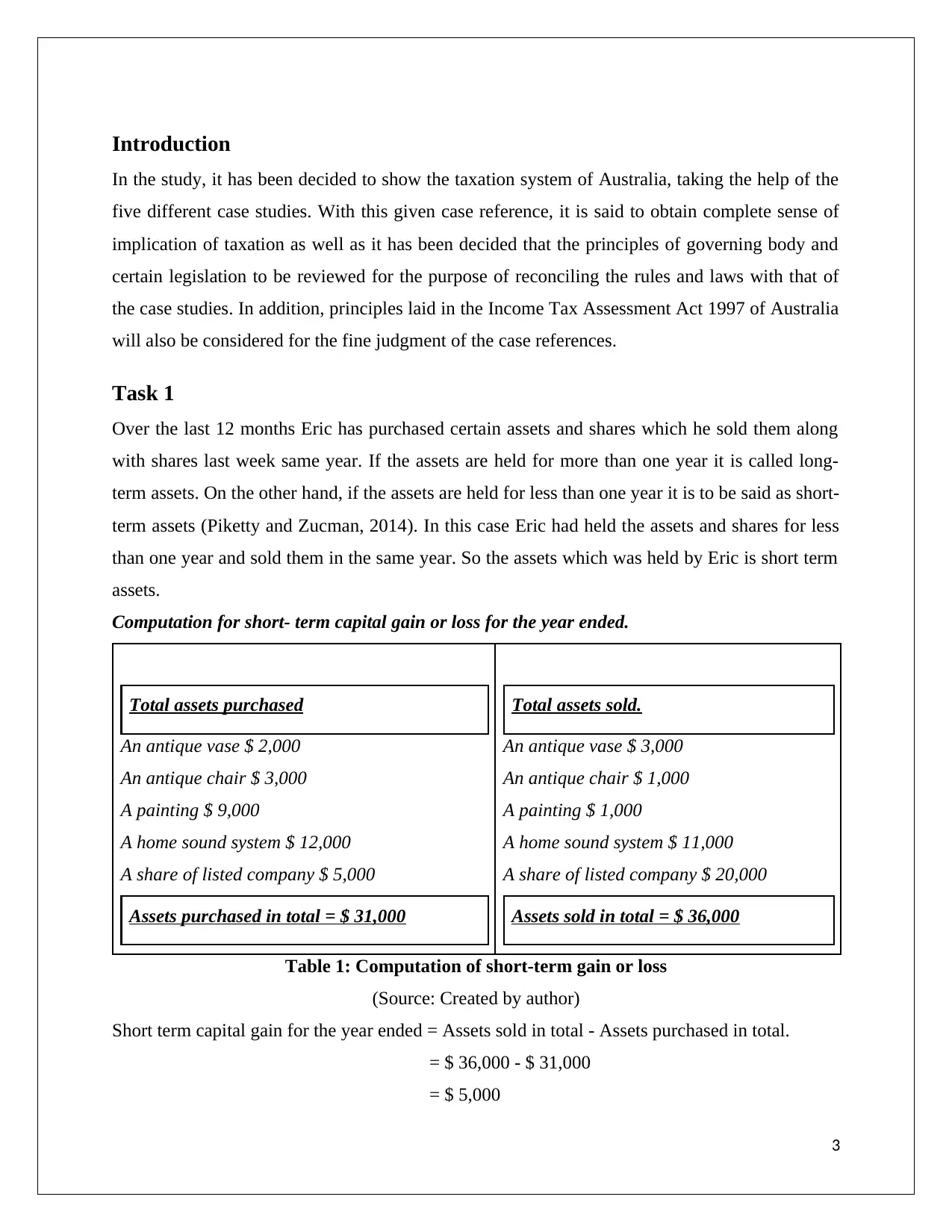

Task 1

Over the last 12 months Eric has purchased certain assets and shares which he sold them along

with shares last week same year. If the assets are held for more than one year it is called long-

term assets. On the other hand, if the assets are held for less than one year it is to be said as short-

term assets (Piketty and Zucman, 2014). In this case Eric had held the assets and shares for less

than one year and sold them in the same year. So the assets which was held by Eric is short term

assets.

Computation for short- term capital gain or loss for the year ended.

Total assets purchased

An antique vase $ 2,000

An antique chair $ 3,000

A painting $ 9,000

A home sound system $ 12,000

A share of listed company $ 5,000

Assets purchased in total = $ 31,000

Total assets sold.

An antique vase $ 3,000

An antique chair $ 1,000

A painting $ 1,000

A home sound system $ 11,000

A share of listed company $ 20,000

Assets sold in total = $ 36,000

Table 1: Computation of short-term gain or loss

(Source: Created by author)

Short term capital gain for the year ended = Assets sold in total - Assets purchased in total.

= $ 36,000 - $ 31,000

= $ 5,000

3

In the study, it has been decided to show the taxation system of Australia, taking the help of the

five different case studies. With this given case reference, it is said to obtain complete sense of

implication of taxation as well as it has been decided that the principles of governing body and

certain legislation to be reviewed for the purpose of reconciling the rules and laws with that of

the case studies. In addition, principles laid in the Income Tax Assessment Act 1997 of Australia

will also be considered for the fine judgment of the case references.

Task 1

Over the last 12 months Eric has purchased certain assets and shares which he sold them along

with shares last week same year. If the assets are held for more than one year it is called long-

term assets. On the other hand, if the assets are held for less than one year it is to be said as short-

term assets (Piketty and Zucman, 2014). In this case Eric had held the assets and shares for less

than one year and sold them in the same year. So the assets which was held by Eric is short term

assets.

Computation for short- term capital gain or loss for the year ended.

Total assets purchased

An antique vase $ 2,000

An antique chair $ 3,000

A painting $ 9,000

A home sound system $ 12,000

A share of listed company $ 5,000

Assets purchased in total = $ 31,000

Total assets sold.

An antique vase $ 3,000

An antique chair $ 1,000

A painting $ 1,000

A home sound system $ 11,000

A share of listed company $ 20,000

Assets sold in total = $ 36,000

Table 1: Computation of short-term gain or loss

(Source: Created by author)

Short term capital gain for the year ended = Assets sold in total - Assets purchased in total.

= $ 36,000 - $ 31,000

= $ 5,000

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

So, it can be seen that the assets which were held by Eric was short term assets because the year

in which he purchased the assets, he sold the assets in the same year.

Task 2

In the study, it is said that Brian is a bank executive and he will be provided by three-year loan of

$1m as a part of his remuneration provided, and the interest rate will be 1% pa (payable in

monthly installments). In addition is also said that the loan has been provided on 1 April 2016

(Williams, 2016).

Brian will use 40% of his loan for income producing purpose and for meeting all his obligation

to interest payment. It is also said that the fringe benefit in the loan for the year 2016-2017 was

received by Brian. The computation of the taxable income of Brian for the year 30 June 2017 is

done below:

Amount of loan = $ 1m

Actual rate of interest on loan in Australia is 15%

Date on which loan was provided = 1April 2016

Rate of interest = 1%

Mode of payment = monthly installments.

Loan amount = 40% of $ 1 million = $ 4, 00,000.

Calculation of installments for 15 months = ($ 1, 00,000*1% / 12 months)* 15 months.

= ($ 10,000 / 12 months) * 15 months

= $ 12,500.

Calculating taxable income for the year ended 2016-17

Revenue

LESS:

Expenditures = $ 0.4 million

Interest on installments = $ 0.01 million

Actual installments = $ 0.25 million

Total = $ 0.34 million

In this study, it has been found that the amount of tax that Brian has to pay upon his taxable

income is $0.34 million and the monthly installment (interest + principle) on the loan is $ 0.26

million. It can be seen that Brian has to pay for installment and because of this his taxable

4

in which he purchased the assets, he sold the assets in the same year.

Task 2

In the study, it is said that Brian is a bank executive and he will be provided by three-year loan of

$1m as a part of his remuneration provided, and the interest rate will be 1% pa (payable in

monthly installments). In addition is also said that the loan has been provided on 1 April 2016

(Williams, 2016).

Brian will use 40% of his loan for income producing purpose and for meeting all his obligation

to interest payment. It is also said that the fringe benefit in the loan for the year 2016-2017 was

received by Brian. The computation of the taxable income of Brian for the year 30 June 2017 is

done below:

Amount of loan = $ 1m

Actual rate of interest on loan in Australia is 15%

Date on which loan was provided = 1April 2016

Rate of interest = 1%

Mode of payment = monthly installments.

Loan amount = 40% of $ 1 million = $ 4, 00,000.

Calculation of installments for 15 months = ($ 1, 00,000*1% / 12 months)* 15 months.

= ($ 10,000 / 12 months) * 15 months

= $ 12,500.

Calculating taxable income for the year ended 2016-17

Revenue

LESS:

Expenditures = $ 0.4 million

Interest on installments = $ 0.01 million

Actual installments = $ 0.25 million

Total = $ 0.34 million

In this study, it has been found that the amount of tax that Brian has to pay upon his taxable

income is $0.34 million and the monthly installment (interest + principle) on the loan is $ 0.26

million. It can be seen that Brian has to pay for installment and because of this his taxable

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

income has reduced by $0.26 million. On the other hand, his taxable income will be different if

he has to repay the installment at the end of the year (Allen et al. 2014).

The calculation is done below:

Revenue

LESS:

Expenditure = $0.4 million

Total = $0.6 million

Therefore, it can be seen that the repayment of the installment on monthly basis is favorable for

Brian because if he repays the installment on monthly basis he has to pay tax on $0.34 million.

On the other hand, he has to pay tax on $0.6 million which is very high (Forrest, 2014).

However, Brian can pay only the principal amount if the bank release from repaying interest on

loan. In this case Brian cannot claim the fringe benefit on the loan, because his expenditure has

dropped slightly and he must pay tax on the taxable income, which is calculated below.

Computation of taxable income for the year ended 2016-17

Revenue = $ 1 million

LESS;

Expenditure = $0.4 million

Interest on installment = $0.25 million

Total = $0.35 million

Therefore, it is clear that Brian has to pay tax on three different tax.

If he was released from paying the interest on loan, then he has to pay tax on $0.35 million. On

the other hand if he has to pay both principal and interest he has to pay tax on $0.34 million. And

if he pay the installment at the end of the year he has to pay tax on $0.6 million.

Task 3

Jack is an architect and his wife Jill a housewife wanted to purchase a property as joint tenants so

they together borrowed money. Both husband and wife entered into a written agreement that if

profit occurs 10% of the profit will be entitled to jack and the remaining 90% to his wife Jill

(Corones, 2014). It is also written that if any loss occurs jack has to entitle 100% of the loss.

However jack has to bear the whole loss (100%) as per the agreement because last year the

property generated loss of $ 10,000.

5

he has to repay the installment at the end of the year (Allen et al. 2014).

The calculation is done below:

Revenue

LESS:

Expenditure = $0.4 million

Total = $0.6 million

Therefore, it can be seen that the repayment of the installment on monthly basis is favorable for

Brian because if he repays the installment on monthly basis he has to pay tax on $0.34 million.

On the other hand, he has to pay tax on $0.6 million which is very high (Forrest, 2014).

However, Brian can pay only the principal amount if the bank release from repaying interest on

loan. In this case Brian cannot claim the fringe benefit on the loan, because his expenditure has

dropped slightly and he must pay tax on the taxable income, which is calculated below.

Computation of taxable income for the year ended 2016-17

Revenue = $ 1 million

LESS;

Expenditure = $0.4 million

Interest on installment = $0.25 million

Total = $0.35 million

Therefore, it is clear that Brian has to pay tax on three different tax.

If he was released from paying the interest on loan, then he has to pay tax on $0.35 million. On

the other hand if he has to pay both principal and interest he has to pay tax on $0.34 million. And

if he pay the installment at the end of the year he has to pay tax on $0.6 million.

Task 3

Jack is an architect and his wife Jill a housewife wanted to purchase a property as joint tenants so

they together borrowed money. Both husband and wife entered into a written agreement that if

profit occurs 10% of the profit will be entitled to jack and the remaining 90% to his wife Jill

(Corones, 2014). It is also written that if any loss occurs jack has to entitle 100% of the loss.

However jack has to bear the whole loss (100%) as per the agreement because last year the

property generated loss of $ 10,000.

5

According to Section 35(2) of Relationship Act 2008, on the ground of Relationship of co-

tenancy a person cannot be a domestic partner of another person (Becker, 2015). According to

Section 5(1) of Partnership Act 1958, relationship between two or more parties is defined as

partnership whose aim is to earn profit and carrying on the same business. Australian Partnership

Act likewise depicts the idea of association in the event of joint occupancy and gives certain

arrangements in regards to the idea of tenure or property identified with the joint tenure, where it

is said that Joint inhabitants residency in like way joint property ordinary property or part

proprietorship does not of itself influence an association as to anything so to held or had whether

the occupants or proprietors do or don't share any advantages made by the usage thereof

(Bennett, 2016). In addition, the receipt by a man of an offer of the advantages of a business is at

first sight affirm that that individual is an associate in the business, however the receipt of such

an offer or of a portion subordinate upon or contrasting with the advantages of a business does

not of itself make that individual an accessory in the business.

However, for this situation it has been discovered that Jack and Jill have household relationship

and came into an agreement of joint tenure where both are qualified for benefit of 1:9 proportion,

however if there should arise an occurrence of misfortune just a single accomplice is qualified

for bear everything of misfortune (Palmer et al. 2015). Regarding the arrangements made in

Relationship Act and Partnership Act, one might say that Jack and Jill are no uncertainty in

residential relationship yet if there should arise an occurrence of relationship of Joint occupancy,

Partnership Act gets pulled in, where they are thought to be in association connection since the

idea of business is same, likewise both are qualified for benefit, however in the event of

misfortune, just Jack needs to shoulder the entire misfortune. Truth be told, in association act,

arrangement for organization is given that every one of the accomplices are qualified for benefit

and not misfortune. In the event that any accomplice alone bears the entire misfortune yet in

addition gets offer of benefit will be likewise be called accomplice.

In this manner, the loss of $ 10,000 will totally be borne by Jack and he is qualified for get tax

reduction on misfortune for the year finished. On the other side, if both the accomplices choose

to offer the property, they initially need to recuperate misfortune emerged from that property

then they can offer the property. Nonetheless, for this situation, there is no degree for

recuperation of misfortune, along these lines they need to offer the property for capital

6

tenancy a person cannot be a domestic partner of another person (Becker, 2015). According to

Section 5(1) of Partnership Act 1958, relationship between two or more parties is defined as

partnership whose aim is to earn profit and carrying on the same business. Australian Partnership

Act likewise depicts the idea of association in the event of joint occupancy and gives certain

arrangements in regards to the idea of tenure or property identified with the joint tenure, where it

is said that Joint inhabitants residency in like way joint property ordinary property or part

proprietorship does not of itself influence an association as to anything so to held or had whether

the occupants or proprietors do or don't share any advantages made by the usage thereof

(Bennett, 2016). In addition, the receipt by a man of an offer of the advantages of a business is at

first sight affirm that that individual is an associate in the business, however the receipt of such

an offer or of a portion subordinate upon or contrasting with the advantages of a business does

not of itself make that individual an accessory in the business.

However, for this situation it has been discovered that Jack and Jill have household relationship

and came into an agreement of joint tenure where both are qualified for benefit of 1:9 proportion,

however if there should arise an occurrence of misfortune just a single accomplice is qualified

for bear everything of misfortune (Palmer et al. 2015). Regarding the arrangements made in

Relationship Act and Partnership Act, one might say that Jack and Jill are no uncertainty in

residential relationship yet if there should arise an occurrence of relationship of Joint occupancy,

Partnership Act gets pulled in, where they are thought to be in association connection since the

idea of business is same, likewise both are qualified for benefit, however in the event of

misfortune, just Jack needs to shoulder the entire misfortune. Truth be told, in association act,

arrangement for organization is given that every one of the accomplices are qualified for benefit

and not misfortune. In the event that any accomplice alone bears the entire misfortune yet in

addition gets offer of benefit will be likewise be called accomplice.

In this manner, the loss of $ 10,000 will totally be borne by Jack and he is qualified for get tax

reduction on misfortune for the year finished. On the other side, if both the accomplices choose

to offer the property, they initially need to recuperate misfortune emerged from that property

then they can offer the property. Nonetheless, for this situation, there is no degree for

recuperation of misfortune, along these lines they need to offer the property for capital

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

misfortune (Latimer, 2016). Further, this capital misfortune will be balanced with the long haul

or here and now capital pick up.

Task 4

The things that held in the case of IRC vs. Duke of Westminster 1936

Duke planned a legal documents with people and making effective use of it in which he made a

legal contract to pay them weekly sum total for a time of seven years or the joint existence of the

meeting. The legal documents (Deeds) tells that the installments were made in acceptance of the

past organization reliably provided to the Duke and that the Duke wanted to make an agreement

for the single despite that he may process in the Duke’s organization or may stop to work for

Duke (Evans, 2015). Letters of explanation were sent to the workers for clarifying him that he

could maintain the full payment for future work however and that was normal by and by that he

would satisfy with the harmony made by the legal document in addition to such sum total and

may be supreme to convey the sum total of installments up to the payment he had of late been

getting or the level of pay. The payee at the time the legal contract was put into effect was

receiving compensation or settled wages and after carrying out the legal contract begin in the

Duke business and keep on getting such sum total as, pay payable before the legal document,

invented the measure of the wages or with the whole required to pay by the legal documents.

Issues held in this case

Just in case, the sum paid under the legal documents consider in the atmosphere which the

people were in the Duke’s use were something for the process, they were not allowable in

figuring the Duke’s risk for tax. Again the all total of the yearly installment, they are deductible

(allowable). At some point, in case the issue was installed under the legal contract payment for

administrations or not. It was unable to challenge that if the legal documents were transported

into reality in order to make Duke to reduce his surtax duty (Bloom, 2015).

The disposition

The payment was not benefit for regulation. Three of the five Lords comes to an end that the

letter was not a contract, only an action of hope or prediction and the four of the five Lords

comes to an end that even if it was a contract, it was nothing more than contract that the person’s

salary for the future service will not be the full salary but only the additional sum referred to the

letter. The fifth Lord comes to an end that legal document and the letter should be viewed

7

or here and now capital pick up.

Task 4

The things that held in the case of IRC vs. Duke of Westminster 1936

Duke planned a legal documents with people and making effective use of it in which he made a

legal contract to pay them weekly sum total for a time of seven years or the joint existence of the

meeting. The legal documents (Deeds) tells that the installments were made in acceptance of the

past organization reliably provided to the Duke and that the Duke wanted to make an agreement

for the single despite that he may process in the Duke’s organization or may stop to work for

Duke (Evans, 2015). Letters of explanation were sent to the workers for clarifying him that he

could maintain the full payment for future work however and that was normal by and by that he

would satisfy with the harmony made by the legal document in addition to such sum total and

may be supreme to convey the sum total of installments up to the payment he had of late been

getting or the level of pay. The payee at the time the legal contract was put into effect was

receiving compensation or settled wages and after carrying out the legal contract begin in the

Duke business and keep on getting such sum total as, pay payable before the legal document,

invented the measure of the wages or with the whole required to pay by the legal documents.

Issues held in this case

Just in case, the sum paid under the legal documents consider in the atmosphere which the

people were in the Duke’s use were something for the process, they were not allowable in

figuring the Duke’s risk for tax. Again the all total of the yearly installment, they are deductible

(allowable). At some point, in case the issue was installed under the legal contract payment for

administrations or not. It was unable to challenge that if the legal documents were transported

into reality in order to make Duke to reduce his surtax duty (Bloom, 2015).

The disposition

The payment was not benefit for regulation. Three of the five Lords comes to an end that the

letter was not a contract, only an action of hope or prediction and the four of the five Lords

comes to an end that even if it was a contract, it was nothing more than contract that the person’s

salary for the future service will not be the full salary but only the additional sum referred to the

letter. The fifth Lord comes to an end that legal document and the letter should be viewed

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

together as a simply maintaining the existing contract of service rather than radically altering it

(AbdulRazaq and Adam, 2015).

All of the Lords rejected the statement that in income cases there is a belief that the court may

ignore the legal position and regard the material of the matter. The material is that which results

from the legal rights and responsibility of the parties discover upon the ordinary legal principle.

Principles established in the case of Duke of Westminster

There is a particular crime identifying with the “false avoidance of wages impose” in the Taxes

Act, which was presented at first in 2000. Be that as it may, this law that has passed is not very

time consuming , as the income regularly want to depend on the traditional base law when the

indict.

Sometimes, you may find that the citizen is charged with a crime under the Thief Act for false

recording yet the greater part of tax delay case is carry under the regular law criminal crime of

deceive society general income (Behagg, 2016). There is no big penalty for such a crime for such

an illegal act if found responsible by law so as suspect could be convicted to life imprisonment

and in additional have to refund the income. The past Chancellor, Dennis Healey largely draw

the division between levy cheat and and tax delay has been “the depth of the jailor sector”.

Task 5

In this case, Bill owns a land and he want to graze his sheep on that land. But the difficult path is

the land has tall pine trees which he need to clear. Later he found that a logging company is

ready to pay him $ 1000 per 100 meter of timber which the logging company will cut from his

land. According to the Sales of Good Act 1954 in Australia, the contract of sale can be made

partly in writing and partly by oral agreement or without seal (Hayward, 2016). If both the

parties agree with each other than the price in the contract of sale will be fixed. In the other

words, both the parties must follow some rules regarding purchase and selling to get into the

contract. But the problem is that the after fulfilling the seller's need the buyer may not get the

payment. Now in this study, the seller who will be getting paid by the logging company for the

clearance of the tree from his land will be considered as Bill. He will get good amount if the Bill

agrees upon the payment offered to him by the company (Gordon, 2014). Thus, it is assumed that

the timber cover 4500 meter and the measurement of the Bill’s land will be in meter then he will

get,

8

(AbdulRazaq and Adam, 2015).

All of the Lords rejected the statement that in income cases there is a belief that the court may

ignore the legal position and regard the material of the matter. The material is that which results

from the legal rights and responsibility of the parties discover upon the ordinary legal principle.

Principles established in the case of Duke of Westminster

There is a particular crime identifying with the “false avoidance of wages impose” in the Taxes

Act, which was presented at first in 2000. Be that as it may, this law that has passed is not very

time consuming , as the income regularly want to depend on the traditional base law when the

indict.

Sometimes, you may find that the citizen is charged with a crime under the Thief Act for false

recording yet the greater part of tax delay case is carry under the regular law criminal crime of

deceive society general income (Behagg, 2016). There is no big penalty for such a crime for such

an illegal act if found responsible by law so as suspect could be convicted to life imprisonment

and in additional have to refund the income. The past Chancellor, Dennis Healey largely draw

the division between levy cheat and and tax delay has been “the depth of the jailor sector”.

Task 5

In this case, Bill owns a land and he want to graze his sheep on that land. But the difficult path is

the land has tall pine trees which he need to clear. Later he found that a logging company is

ready to pay him $ 1000 per 100 meter of timber which the logging company will cut from his

land. According to the Sales of Good Act 1954 in Australia, the contract of sale can be made

partly in writing and partly by oral agreement or without seal (Hayward, 2016). If both the

parties agree with each other than the price in the contract of sale will be fixed. In the other

words, both the parties must follow some rules regarding purchase and selling to get into the

contract. But the problem is that the after fulfilling the seller's need the buyer may not get the

payment. Now in this study, the seller who will be getting paid by the logging company for the

clearance of the tree from his land will be considered as Bill. He will get good amount if the Bill

agrees upon the payment offered to him by the company (Gordon, 2014). Thus, it is assumed that

the timber cover 4500 meter and the measurement of the Bill’s land will be in meter then he will

get,

8

For 100 meter Bill will be paid $ 1,000

For 1 meter Bill will be paid $(1,000/100) = $10

So for 4500 meters of land Bill will give = $(4500*10) = $ 45,000

Thus, we can see by the calculation that the company will be giving $ 45,000 to Bill for the

clearance of 4500 meter of timber. Thus, without investing any fund, Bill is getting a huge

amount from the logging company and can be a better deal.

The case has been found in the phrase is that Bill will give an amount of $ 50,000 by the logging

company for clearing the timber as per the requirement of Bill. For the clearance the company is

paying him a large amount, what if where both parties have no idea about how much area the

timber cover does or how much timber the company need and the owner of the land agrees on it.

In this case it can happen that Bill is getting more amount for less timber or the company is

giving less amount for the timber that is covering the land. It can be said that for one of the either

parties the deal may or may not be profitable (Greiner, 2014).

Therefore, according to survey, from the above case it can be said that if the company offered

Bill a lump sum $ 50,000 will be the best deal for clearance of timber. But on other hand if Bill

gets ready to get paid $ 1000 meter of every 100 meter then it would be loss because he will be

getting $ 45000 for 4500 meter land that the timber covers as per the calculations.

Conclusion

Attempts have been made to describe different case references with respect to the taxation law.

Based on the details it can be see that in the first case Eric has obtain capital gain of $ 5000 and

in the second case it is calculated that Brian has to pay tax on $ 0.6 million if the installment was

paid at the end of the loan tenure.

9

For 1 meter Bill will be paid $(1,000/100) = $10

So for 4500 meters of land Bill will give = $(4500*10) = $ 45,000

Thus, we can see by the calculation that the company will be giving $ 45,000 to Bill for the

clearance of 4500 meter of timber. Thus, without investing any fund, Bill is getting a huge

amount from the logging company and can be a better deal.

The case has been found in the phrase is that Bill will give an amount of $ 50,000 by the logging

company for clearing the timber as per the requirement of Bill. For the clearance the company is

paying him a large amount, what if where both parties have no idea about how much area the

timber cover does or how much timber the company need and the owner of the land agrees on it.

In this case it can happen that Bill is getting more amount for less timber or the company is

giving less amount for the timber that is covering the land. It can be said that for one of the either

parties the deal may or may not be profitable (Greiner, 2014).

Therefore, according to survey, from the above case it can be said that if the company offered

Bill a lump sum $ 50,000 will be the best deal for clearance of timber. But on other hand if Bill

gets ready to get paid $ 1000 meter of every 100 meter then it would be loss because he will be

getting $ 45000 for 4500 meter land that the timber covers as per the calculations.

Conclusion

Attempts have been made to describe different case references with respect to the taxation law.

Based on the details it can be see that in the first case Eric has obtain capital gain of $ 5000 and

in the second case it is calculated that Brian has to pay tax on $ 0.6 million if the installment was

paid at the end of the loan tenure.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Reference list

AbdulRazaq, M.T. and Adam, K.I. (2015). Anti-Avoidance Legislations: Issues & Doubts in the

Application of Tax Rules in Nigeria. AGORA Int'l J. Jurid. Sci., p.1.

Allen, F., Hryckiewicz, A., Kowalewski, O. and Tümer-Alkan, G. (2014). Transmission of

financial shocks in loan and deposit markets: Role of interbank borrowing and market

monitoring. Journal of Financial Stability, 15, pp.112-126.

Becker, J. (2015). The Relation of Article 9 Paragraph 1 German Double Taxation Treaties to

Domestic Tax Law and the Consequences for Current Value Depreciation under Section 1

Paragraph 1: Foreign Tax Act. Intertax, 43(10), pp.589-594.

Behagg, C. (2016). Tax Inversions: Time to Take a Look in the Mirror Reflections on the

Inversion Phenomenon. Intertax, 44(2), pp.130-145.

Bennett, R.J. (2016). Interpreting business partnerships in late Victorian Britain. The Economic

History Review, 69(4), pp.1199-1227.

Bloom, D. (2015). Tax avoidance-a view from the dark side. Melb. UL Rev., 39, p.950.

Corones, S.G. (2014). Competition law in Australia. Thomson Reuters Australia, Limited.

Evans, S. (2015). It's' Clean Hands' Again: The Dirtiness of Not Paying Tax Considered in the

Supreme Court.

Forrest, C. (2014). Immunity from seizure and suit in Australia: the protection of cultural objects

on Loan Act 2013. International Journal of Cultural Property, 21(2), pp.143-172.

Gordon, B. (2014). Acceptance by conduct in ecommerce transactions in Australia. Commercial

Law Quarterly: The Journal of the Commercial Law Association of Australia, 28(2), p.3.

Greiner, R. (2014). Environmental duty of care: from ethical principle towards a code of practice

for the grazing industry in Queensland (Australia). Journal of agricultural and environmental

ethics, 27(4), pp.527-547.

Hayward, B. (2016). What's in a Name: Software, Digital Products, and the Sale of

Goods. Sydney L. Rev., 38, p.441.

Latimer, P. (2016). Repudiation of Partnership Contracts.

Palmer, J., Instone, L., Mee, K.J., Williams, M. and Vaughan, N. (2015). Green tenants:

practicing a sustainability ethics for the rental housing sector. Local Environment, 20(8), pp.923-

939.

10

AbdulRazaq, M.T. and Adam, K.I. (2015). Anti-Avoidance Legislations: Issues & Doubts in the

Application of Tax Rules in Nigeria. AGORA Int'l J. Jurid. Sci., p.1.

Allen, F., Hryckiewicz, A., Kowalewski, O. and Tümer-Alkan, G. (2014). Transmission of

financial shocks in loan and deposit markets: Role of interbank borrowing and market

monitoring. Journal of Financial Stability, 15, pp.112-126.

Becker, J. (2015). The Relation of Article 9 Paragraph 1 German Double Taxation Treaties to

Domestic Tax Law and the Consequences for Current Value Depreciation under Section 1

Paragraph 1: Foreign Tax Act. Intertax, 43(10), pp.589-594.

Behagg, C. (2016). Tax Inversions: Time to Take a Look in the Mirror Reflections on the

Inversion Phenomenon. Intertax, 44(2), pp.130-145.

Bennett, R.J. (2016). Interpreting business partnerships in late Victorian Britain. The Economic

History Review, 69(4), pp.1199-1227.

Bloom, D. (2015). Tax avoidance-a view from the dark side. Melb. UL Rev., 39, p.950.

Corones, S.G. (2014). Competition law in Australia. Thomson Reuters Australia, Limited.

Evans, S. (2015). It's' Clean Hands' Again: The Dirtiness of Not Paying Tax Considered in the

Supreme Court.

Forrest, C. (2014). Immunity from seizure and suit in Australia: the protection of cultural objects

on Loan Act 2013. International Journal of Cultural Property, 21(2), pp.143-172.

Gordon, B. (2014). Acceptance by conduct in ecommerce transactions in Australia. Commercial

Law Quarterly: The Journal of the Commercial Law Association of Australia, 28(2), p.3.

Greiner, R. (2014). Environmental duty of care: from ethical principle towards a code of practice

for the grazing industry in Queensland (Australia). Journal of agricultural and environmental

ethics, 27(4), pp.527-547.

Hayward, B. (2016). What's in a Name: Software, Digital Products, and the Sale of

Goods. Sydney L. Rev., 38, p.441.

Latimer, P. (2016). Repudiation of Partnership Contracts.

Palmer, J., Instone, L., Mee, K.J., Williams, M. and Vaughan, N. (2015). Green tenants:

practicing a sustainability ethics for the rental housing sector. Local Environment, 20(8), pp.923-

939.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Piketty, T. and Zucman, G. (2014). Capital is back: Wealth-income ratios in rich countries 1700–

2010. The Quarterly Journal of Economics, 129(3), pp.1255-1310.

Williams, B. (2016). The impact of non-interest income on bank risk in Australia. Journal of

Banking & Finance, 73, pp.16-37.

11

2010. The Quarterly Journal of Economics, 129(3), pp.1255-1310.

Williams, B. (2016). The impact of non-interest income on bank risk in Australia. Journal of

Banking & Finance, 73, pp.16-37.

11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.