Taxation Principles and Practice Report: UK Taxation System Analysis

VerifiedAdded on 2023/06/11

|13

|4446

|390

Report

AI Summary

This report delves into the principles of taxation, examining how governments utilize different taxes to fulfill their core functions, including lawmaking, ensuring domestic tranquility, providing defense, and promoting welfare. It differentiates between direct and tax expenditures, highlighting their respective roles in public finance. The report further analyzes tax avoidance and tax evasion, exploring strategies employed by multinational corporations (MNCs) to minimize their tax liabilities, such as IP structuring, thin capitalization, and the use of validity schemes. It also discusses specific measures implemented by the UK government, including those from HMRC and GAAR, to combat tax avoidance. Finally, the report incorporates a reflective analysis using the Gibbs reflective model to synthesize the lessons learned from the assignment preparation, including benefits and difficulties faced, providing a comprehensive overview of the subject matter.

Taxation Principles and

Practice

Practice

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

Explaining how government use different taxes to fulfil its four main functions.......................3

The differences between direct expenditure and tax expenditure................................................4

Difference between tax avoidance and tax evasion. Three ways by which MNCs avoid or

minimize taxes.............................................................................................................................6

Discussing two measures imposed by the UK government to combat tax avoidance.................7

PART B............................................................................................................................................9

Providing report on the lessons learnt from preparation of the assignment along with the

benefits and difficulties faced......................................................................................................9

Giving reflection for the lesson learnt from the formulation of the assessment........................10

CONCLUSION..............................................................................................................................11

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

Explaining how government use different taxes to fulfil its four main functions.......................3

The differences between direct expenditure and tax expenditure................................................4

Difference between tax avoidance and tax evasion. Three ways by which MNCs avoid or

minimize taxes.............................................................................................................................6

Discussing two measures imposed by the UK government to combat tax avoidance.................7

PART B............................................................................................................................................9

Providing report on the lessons learnt from preparation of the assignment along with the

benefits and difficulties faced......................................................................................................9

Giving reflection for the lesson learnt from the formulation of the assessment........................10

CONCLUSION..............................................................................................................................11

REFERENCES................................................................................................................................1

INTRODUCTION

Taxation principles are the guidelines that are used by governing entity to use while

devising a system of taxation. This report will highlight how government uses the different taxes

to fulfil its main functions of making laws, ensuring domestic tranquillity, providing defence and

promotion of welfare through justice. The report will outline the differences between the tax

expenditures and direct expenditures. Further, the report will evaluate the measures like IP

structuring, thin capitalization and validity of schemes that are implied by the MNCs to avoid or

minimize taxes. In addition, the measures of HMRC and GAAR by the UK government to

combat the tax avoidance will be discussed. The report will provide a brief reflective report using

Gibbs reflective model to demonstrate the lesson from the module.

PART A

Explaining how government use different taxes to fulfil its four main functions

There are different kinds of the taxes which are basically imposed by the government on

organizations and individuals. The main reason behind imposing the taxes is to get sufficient

amount of funds for accomplishing requirements of different functions. The functions which are

executed by the UK government includes making laws, insuring domestic tranquility, providing

common defence, promoting general welfare, establishing justice, etc. In addition to this, it can

be specified that the major four functions of the government that is executed includes allocation,

distribution, economic growth and stabilization.

From the assessment it can be interpreted that there are distinct form of the taxes that is

imposed which includes income, property, capital gain, UK inherent and value added (Best and

Kleven, 2018). The other form of the taxes which are implemented by government for

accomplishing its requirement through insurance premium, stamp, land, petroleum,

environmental, custom and excise duties. ,Some taxes are considered to be progressive pattern of

charging in which higher income generating are pay at greater rate. With help of the different

types of the taxes the government largely pay attention on developing the significant tactic so

that good welfare for citizen can be formulated.

The main course of action is exerted is to offer public service such as NHS, schools and

pensions, etc. these are the activities that are basically taken into consideration by the

government in UK to get the significant ability to achieve higher level working conditions in the

country. There are various aspects such as offering god schooling and pensions aids the citizen to

Taxation principles are the guidelines that are used by governing entity to use while

devising a system of taxation. This report will highlight how government uses the different taxes

to fulfil its main functions of making laws, ensuring domestic tranquillity, providing defence and

promotion of welfare through justice. The report will outline the differences between the tax

expenditures and direct expenditures. Further, the report will evaluate the measures like IP

structuring, thin capitalization and validity of schemes that are implied by the MNCs to avoid or

minimize taxes. In addition, the measures of HMRC and GAAR by the UK government to

combat the tax avoidance will be discussed. The report will provide a brief reflective report using

Gibbs reflective model to demonstrate the lesson from the module.

PART A

Explaining how government use different taxes to fulfil its four main functions

There are different kinds of the taxes which are basically imposed by the government on

organizations and individuals. The main reason behind imposing the taxes is to get sufficient

amount of funds for accomplishing requirements of different functions. The functions which are

executed by the UK government includes making laws, insuring domestic tranquility, providing

common defence, promoting general welfare, establishing justice, etc. In addition to this, it can

be specified that the major four functions of the government that is executed includes allocation,

distribution, economic growth and stabilization.

From the assessment it can be interpreted that there are distinct form of the taxes that is

imposed which includes income, property, capital gain, UK inherent and value added (Best and

Kleven, 2018). The other form of the taxes which are implemented by government for

accomplishing its requirement through insurance premium, stamp, land, petroleum,

environmental, custom and excise duties. ,Some taxes are considered to be progressive pattern of

charging in which higher income generating are pay at greater rate. With help of the different

types of the taxes the government largely pay attention on developing the significant tactic so

that good welfare for citizen can be formulated.

The main course of action is exerted is to offer public service such as NHS, schools and

pensions, etc. these are the activities that are basically taken into consideration by the

government in UK to get the significant ability to achieve higher level working conditions in the

country. There are various aspects such as offering god schooling and pensions aids the citizen to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

receive god standard of living. On the basis of this, it can be interpreted that these form of

activities contributes in economic development.

For providing security and defense to the common people of country it is important for

the government to have funds that can be used for hiring and managing the day to day practices

of such departments (Advani, Chamberlain and Summers, 2020). In order to have effective

defensive system in the country it is highly essential to maintain significant level of funds that

can be generated by enforcing citizen to pay personal, business, etc. so that reliable and higher

advanced technologies to improve the overall performance can become possible. In order to

establish the justice system which is highly effective and required to be taken into consideration

for ensuring that no biasses and fair functioning is exerted. It is the responsibilities of UK

government to have significant pattern by employment opportunities in the country so that

relevant level of income generating capacity can be obtained by people. Maintaining effective

collaboration among all the public departments of the country etc. in order to have better

functioning in turn higher functioning to maintain good level of productivity that all contributes

in economic development.

On the basis of this, it can be interpreted that thee are distinct type of functions which are

implemented and managed by government. For a gaining significant level of efficiency and

effectiveness it is important for the government to have reliable income sources so that meeting

such requirements with maintaining four canons of taxes such as equity, certainty, convenience

and economy. In this manner, government uses different taxes to accomplish h its for main

functions as mentioned.

The differences between direct expenditure and tax expenditure

Direct Expenditure

These are the traditional ways of spending for public through which public resources are

directly transferred to beneficiaries.

The value of transfer being an integral part of the budget act.

Direct expenses are the expenses that are identified with and allocated to cost centres or

cost units.

The government uses direct spending in order to support its policies.

When government takes money from taxpayers and give that money to spend to others

for specific purposes it is called direct expenditure (Deb and et.al., 2018).

activities contributes in economic development.

For providing security and defense to the common people of country it is important for

the government to have funds that can be used for hiring and managing the day to day practices

of such departments (Advani, Chamberlain and Summers, 2020). In order to have effective

defensive system in the country it is highly essential to maintain significant level of funds that

can be generated by enforcing citizen to pay personal, business, etc. so that reliable and higher

advanced technologies to improve the overall performance can become possible. In order to

establish the justice system which is highly effective and required to be taken into consideration

for ensuring that no biasses and fair functioning is exerted. It is the responsibilities of UK

government to have significant pattern by employment opportunities in the country so that

relevant level of income generating capacity can be obtained by people. Maintaining effective

collaboration among all the public departments of the country etc. in order to have better

functioning in turn higher functioning to maintain good level of productivity that all contributes

in economic development.

On the basis of this, it can be interpreted that thee are distinct type of functions which are

implemented and managed by government. For a gaining significant level of efficiency and

effectiveness it is important for the government to have reliable income sources so that meeting

such requirements with maintaining four canons of taxes such as equity, certainty, convenience

and economy. In this manner, government uses different taxes to accomplish h its for main

functions as mentioned.

The differences between direct expenditure and tax expenditure

Direct Expenditure

These are the traditional ways of spending for public through which public resources are

directly transferred to beneficiaries.

The value of transfer being an integral part of the budget act.

Direct expenses are the expenses that are identified with and allocated to cost centres or

cost units.

The government uses direct spending in order to support its policies.

When government takes money from taxpayers and give that money to spend to others

for specific purposes it is called direct expenditure (Deb and et.al., 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

These are expenses other than the direct materials costs and direct labour cost.

These expenses are categorized as variable expenses that means they vary in value in

accordance to the change (increase or decrease) in volume of production.

Identified based on work order. Allocation to the total amount of cost centres or work

orders.

The prime cost of the product includes direct expenses.

For controlling direct expenses budgets are prepared in accordance to the volume of

output budgeted given by the production volume budget. The budget prepared indicates

the direct expenses' physical volume that are required.

When standards are fixed item by item direct expenses are listed compared to actual costs

that are incurred regarding the standards that are set up. Thus, forms the basis for

controlling direct expenses.

Examples of direct expenses are carriage and materials that are bought for specific jobs,

expenses occurred on experiments being carried out before taking up the concerned job. Basic sliding fee child care program, Minnesota family investment program, Minnesota

long term program, various Minnesota Housing Finance Agency programs are the direct

expenditure programs.

Tax Expenditure

Tax expenditures are the tax code's special provisions such as exclusions, deductions,

credits, deferrals, and tax rates. These special provisions are for the benefit of particular

activities or groups of taxpayers.

Tax liability of selected taxpayers reduces through special preferential tax structures for

pursuing specific social and economic objectives of the policy (Miller and Bogui, 2019).

These are the losses to public revenue as a result of special allowances and relief that is

given to varied categories of taxpayers because of the economic and social policies by the

government for the betterment of the society.

Tax expenditure is utilized by government in support to its policies.

Instead of directly giving the money, it is transferred by the government through lowering

the taxes for an individual or company.

The tax expenditures cost varies from year to year in accordance to the level to the

economic activities in the country.

These expenses are categorized as variable expenses that means they vary in value in

accordance to the change (increase or decrease) in volume of production.

Identified based on work order. Allocation to the total amount of cost centres or work

orders.

The prime cost of the product includes direct expenses.

For controlling direct expenses budgets are prepared in accordance to the volume of

output budgeted given by the production volume budget. The budget prepared indicates

the direct expenses' physical volume that are required.

When standards are fixed item by item direct expenses are listed compared to actual costs

that are incurred regarding the standards that are set up. Thus, forms the basis for

controlling direct expenses.

Examples of direct expenses are carriage and materials that are bought for specific jobs,

expenses occurred on experiments being carried out before taking up the concerned job. Basic sliding fee child care program, Minnesota family investment program, Minnesota

long term program, various Minnesota Housing Finance Agency programs are the direct

expenditure programs.

Tax Expenditure

Tax expenditures are the tax code's special provisions such as exclusions, deductions,

credits, deferrals, and tax rates. These special provisions are for the benefit of particular

activities or groups of taxpayers.

Tax liability of selected taxpayers reduces through special preferential tax structures for

pursuing specific social and economic objectives of the policy (Miller and Bogui, 2019).

These are the losses to public revenue as a result of special allowances and relief that is

given to varied categories of taxpayers because of the economic and social policies by the

government for the betterment of the society.

Tax expenditure is utilized by government in support to its policies.

Instead of directly giving the money, it is transferred by the government through lowering

the taxes for an individual or company.

The tax expenditures cost varies from year to year in accordance to the level to the

economic activities in the country.

Tax expenditures are done on diverse groups that are usually large and very complex.

Income tax credit, refundable dependent care credit, working family tax credit, long-term

care insurance income tax credit, TIF housing districts, special property tax classification,

sales tax exemption for building materials, etc., Income tax exemption for interest on

bonds issued by Minnesota governments are the examples of tax expenditure programs.

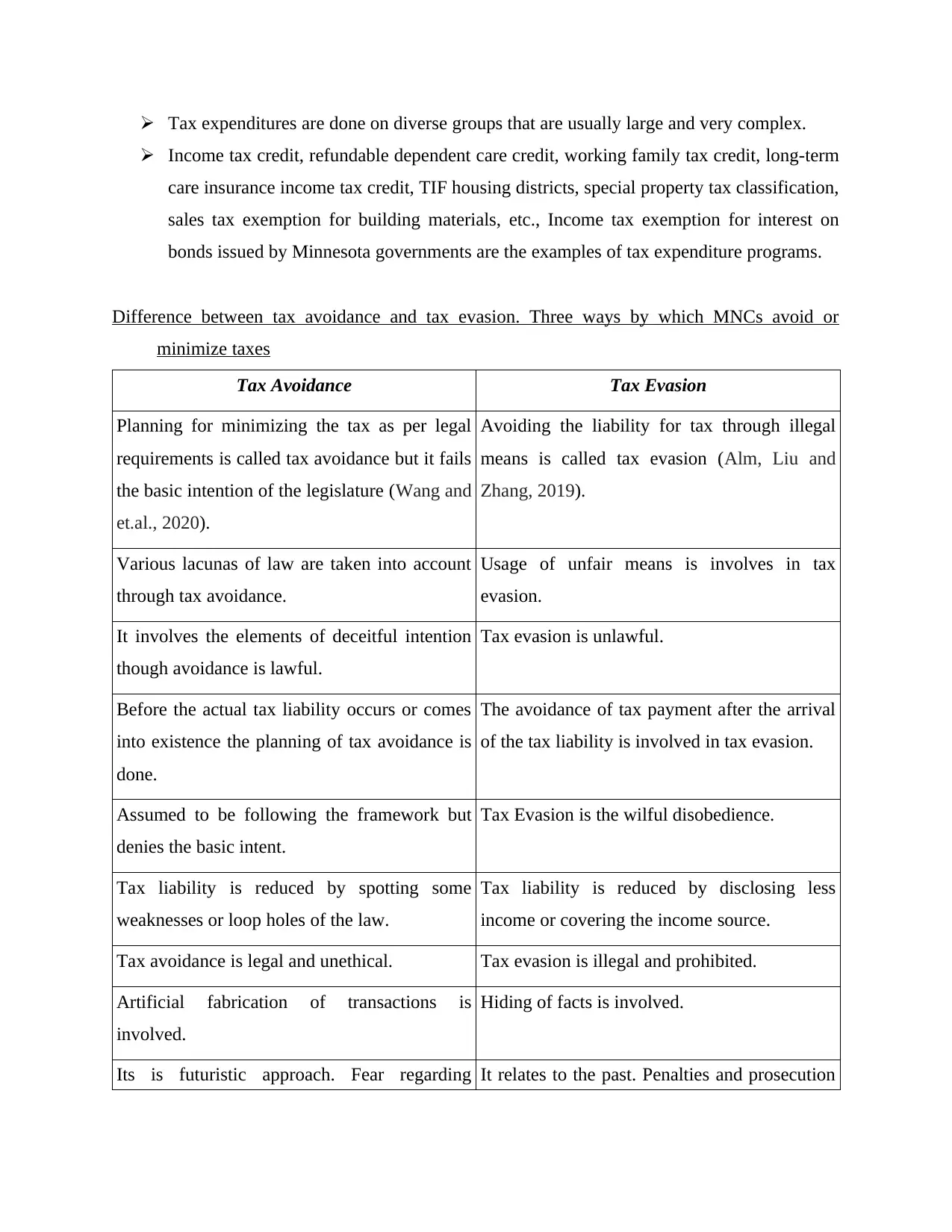

Difference between tax avoidance and tax evasion. Three ways by which MNCs avoid or

minimize taxes

Tax Avoidance Tax Evasion

Planning for minimizing the tax as per legal

requirements is called tax avoidance but it fails

the basic intention of the legislature (Wang and

et.al., 2020).

Avoiding the liability for tax through illegal

means is called tax evasion (Alm, Liu and

Zhang, 2019).

Various lacunas of law are taken into account

through tax avoidance.

Usage of unfair means is involves in tax

evasion.

It involves the elements of deceitful intention

though avoidance is lawful.

Tax evasion is unlawful.

Before the actual tax liability occurs or comes

into existence the planning of tax avoidance is

done.

The avoidance of tax payment after the arrival

of the tax liability is involved in tax evasion.

Assumed to be following the framework but

denies the basic intent.

Tax Evasion is the wilful disobedience.

Tax liability is reduced by spotting some

weaknesses or loop holes of the law.

Tax liability is reduced by disclosing less

income or covering the income source.

Tax avoidance is legal and unethical. Tax evasion is illegal and prohibited.

Artificial fabrication of transactions is

involved.

Hiding of facts is involved.

Its is futuristic approach. Fear regarding It relates to the past. Penalties and prosecution

Income tax credit, refundable dependent care credit, working family tax credit, long-term

care insurance income tax credit, TIF housing districts, special property tax classification,

sales tax exemption for building materials, etc., Income tax exemption for interest on

bonds issued by Minnesota governments are the examples of tax expenditure programs.

Difference between tax avoidance and tax evasion. Three ways by which MNCs avoid or

minimize taxes

Tax Avoidance Tax Evasion

Planning for minimizing the tax as per legal

requirements is called tax avoidance but it fails

the basic intention of the legislature (Wang and

et.al., 2020).

Avoiding the liability for tax through illegal

means is called tax evasion (Alm, Liu and

Zhang, 2019).

Various lacunas of law are taken into account

through tax avoidance.

Usage of unfair means is involves in tax

evasion.

It involves the elements of deceitful intention

though avoidance is lawful.

Tax evasion is unlawful.

Before the actual tax liability occurs or comes

into existence the planning of tax avoidance is

done.

The avoidance of tax payment after the arrival

of the tax liability is involved in tax evasion.

Assumed to be following the framework but

denies the basic intent.

Tax Evasion is the wilful disobedience.

Tax liability is reduced by spotting some

weaknesses or loop holes of the law.

Tax liability is reduced by disclosing less

income or covering the income source.

Tax avoidance is legal and unethical. Tax evasion is illegal and prohibited.

Artificial fabrication of transactions is

involved.

Hiding of facts is involved.

Its is futuristic approach. Fear regarding It relates to the past. Penalties and prosecution

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

imposition of penalties and prosecutions. related fear.

Ways by which Multinationals avoid taxes

IP Structuring: In IP structuring strategy the structure of business in made in such a

manner that all its valuable patents and technical knowledge or expertise are owned by any of the

subsidiary operating in a low tax jurisdiction. It means all the IP rights belonging to a MNC

group are centred in an entity that is registered in a country with low taxes (Neubig and Wunsch-

Vincent, 2018). Companies that deals in the segment of consumer goods also misuse this

structure. Some companies get their brand registered in the regions with low tax jurisdictions and

make payment for the royalty to the company of low tax jurisdiction for using the brand. The

profits of domestic company are used for the royalty expenses. Also, the promoting and

marketing expenses are made from the profits of domestic country.

Thin Capitalization: Thin capitalization is a state by which a relatively high level of debt

exist in a company as compared to its equity. In high tax jurisdictions such as in United

Kingdom, The United States, India and France capital is required for purchasing assets and

growth of business. Thin capitalization strategy is used for concentrating capital in non-taxable.

The capital is concentrated in tax exempt and tax exempted group companies give debt to

operational companies. Interest is received by exempt companies from operational companies.

This results in increased capital for tax heaven companies and reduced profits declaration by the

operational companies. Vicious circle is created by thin capitalization (Prastiwi and Ratnasari,

2019). For instance, when a UK company borrows money from a related company located in tax

exempt country, the payment of interest additionally increase the shell company's capital in tax

haven. And the interest payment by UK company further reduces the profits of the company,

resulting in inability of UK company in building capital from profit. Thus, through its strategy

MNCs try to avoid the tax to be paid by the company.

Validity of the Schemes: In the tax consultancy field validity schemes are open secrets.

These schemes create a structure that is considered by economists as the side effect of

globalization. Anti Abuse provisions have been brought by the governments over the recent year

in counter to these schemes (De Simone, Stomberg and Williams, 2020). As a result of anti

abuse provisions risk of litigation and reputation increased in the last decade.

Ways by which Multinationals avoid taxes

IP Structuring: In IP structuring strategy the structure of business in made in such a

manner that all its valuable patents and technical knowledge or expertise are owned by any of the

subsidiary operating in a low tax jurisdiction. It means all the IP rights belonging to a MNC

group are centred in an entity that is registered in a country with low taxes (Neubig and Wunsch-

Vincent, 2018). Companies that deals in the segment of consumer goods also misuse this

structure. Some companies get their brand registered in the regions with low tax jurisdictions and

make payment for the royalty to the company of low tax jurisdiction for using the brand. The

profits of domestic company are used for the royalty expenses. Also, the promoting and

marketing expenses are made from the profits of domestic country.

Thin Capitalization: Thin capitalization is a state by which a relatively high level of debt

exist in a company as compared to its equity. In high tax jurisdictions such as in United

Kingdom, The United States, India and France capital is required for purchasing assets and

growth of business. Thin capitalization strategy is used for concentrating capital in non-taxable.

The capital is concentrated in tax exempt and tax exempted group companies give debt to

operational companies. Interest is received by exempt companies from operational companies.

This results in increased capital for tax heaven companies and reduced profits declaration by the

operational companies. Vicious circle is created by thin capitalization (Prastiwi and Ratnasari,

2019). For instance, when a UK company borrows money from a related company located in tax

exempt country, the payment of interest additionally increase the shell company's capital in tax

haven. And the interest payment by UK company further reduces the profits of the company,

resulting in inability of UK company in building capital from profit. Thus, through its strategy

MNCs try to avoid the tax to be paid by the company.

Validity of the Schemes: In the tax consultancy field validity schemes are open secrets.

These schemes create a structure that is considered by economists as the side effect of

globalization. Anti Abuse provisions have been brought by the governments over the recent year

in counter to these schemes (De Simone, Stomberg and Williams, 2020). As a result of anti

abuse provisions risk of litigation and reputation increased in the last decade.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Discussing two measures imposed by the UK government to combat tax avoidance

Tax avoidance refers to the utilizing the legal method to minimize h the amount of h

income owned by person and organization (Salhi, Al Jabr and Jarboui, 2020). There are various

types of the actions which are basically executed by the individuals for having ability to avoid

tax paying by deliberating h r under-reporting, keeping two sets of books, claiming false

deductions on return, personal expenses, transferring assets, etc. these are the activities which are

taken into practice by individuals for indulging into tax avoidance. In addition to this, for

producing the advantages there is involvement of artificial intelligence transaction that impact

the functioning of government.

For overcoming and mitigating such courses of actions, government of UK has taken

significant strategy implementation in turn positive results can be derived. The one of the

significant approach that has been outlined by UK government comprises having HMRC strategy

is concerned with Her majesty's revenue and customs which is responsible for collecting taxes,

paying child benefits, enforcing tax, payment of minimum wage by employer (Tax avoidance

schemes currently in the spotlight, 2022). The particular strategy is helpful for government to

maintain fairness, consistency across the board for addressing cross culture behaviours. The

customer group for the particular strategy include s larger, mid sized, small, individual, wealthy

and criminals. It pays attention on having strongly compliance by promoting customer's

relationship with this. In order to avoid non-compliance as early as possible it responds strongly

to deliberate vi spotting mistakes, fraudulent claim, personalize online service and automated

calculations. There is focus provided on identifying and targeting the areas of the greatest risk

which can cheat system. There is higher level of focus provided on gaining the significant

approach to solve disputes so that higher ability to gain appropriate level of convenient to deal

with tax avoidance.

There are few other schemes as well that is taken into practice for dealing with the tax

avoidance which involves general anti abuse rule, etc. which provides assistance in gaining the

information regarding the schemes. GAAR (General Anti Abuse Rule) guidance is helpful in

recognizing tax arrangements and the processes for counteracting them. It is one of the

significant approach that is taken into practice by UK government for counteract tax advantages

arising from tax arrangements that are abusive. It imposes the rules across number of taxes which

are taken in HRMC's favour. This is applicable to income, capital, corporation, inherent and

Tax avoidance refers to the utilizing the legal method to minimize h the amount of h

income owned by person and organization (Salhi, Al Jabr and Jarboui, 2020). There are various

types of the actions which are basically executed by the individuals for having ability to avoid

tax paying by deliberating h r under-reporting, keeping two sets of books, claiming false

deductions on return, personal expenses, transferring assets, etc. these are the activities which are

taken into practice by individuals for indulging into tax avoidance. In addition to this, for

producing the advantages there is involvement of artificial intelligence transaction that impact

the functioning of government.

For overcoming and mitigating such courses of actions, government of UK has taken

significant strategy implementation in turn positive results can be derived. The one of the

significant approach that has been outlined by UK government comprises having HMRC strategy

is concerned with Her majesty's revenue and customs which is responsible for collecting taxes,

paying child benefits, enforcing tax, payment of minimum wage by employer (Tax avoidance

schemes currently in the spotlight, 2022). The particular strategy is helpful for government to

maintain fairness, consistency across the board for addressing cross culture behaviours. The

customer group for the particular strategy include s larger, mid sized, small, individual, wealthy

and criminals. It pays attention on having strongly compliance by promoting customer's

relationship with this. In order to avoid non-compliance as early as possible it responds strongly

to deliberate vi spotting mistakes, fraudulent claim, personalize online service and automated

calculations. There is focus provided on identifying and targeting the areas of the greatest risk

which can cheat system. There is higher level of focus provided on gaining the significant

approach to solve disputes so that higher ability to gain appropriate level of convenient to deal

with tax avoidance.

There are few other schemes as well that is taken into practice for dealing with the tax

avoidance which involves general anti abuse rule, etc. which provides assistance in gaining the

information regarding the schemes. GAAR (General Anti Abuse Rule) guidance is helpful in

recognizing tax arrangements and the processes for counteracting them. It is one of the

significant approach that is taken into practice by UK government for counteract tax advantages

arising from tax arrangements that are abusive. It imposes the rules across number of taxes which

are taken in HRMC's favour. This is applicable to income, capital, corporation, inherent and

stamp duty land tax. It conducts the interactions with penalities for enablers of defeated tax

avoidance schemes. In addition, this, the main objective of the particular approach is to apply

rules for counteract tax benefits that are arising from m artificial tax arrangements. From the

assessment of the apicultural strategy that is executed by the UK government includes that

having effective ability to deal with abusive tax arrangements for having fair & consistent

functioning.

Through HMRC and GAAR the governing authority implies the measure to control the

tax avoidance by the individuals and the MNCs and corporates. These two strategies are used at

global level by the governments of different nations. By these the governments of the various

countries makes sure that the tax is paid to the government of the country in which the actual

operations of the companies are being carried out. Penalties are imposed on the defaulters or

unethical advantage seekers. These measures aim at bringing transparency and ethnicity in the

procedures of tax collection.

PART B

Providing report on the lessons learnt from preparation of the assignment along with the benefits

and difficulties faced

Gibbs reflective model is one of the significant theory that is related with having six

stages such as descriptions, feelings, evaluation, analysis, conclusion and action plan (Gibbs'

Reflective Cycle, 2022). There are different types of organization which operate in UK and

conducts the activities like tax avoidance and evasion. I have come to know that tax avoidance

and evasion provides the benefits to individuals but has negative impact on government

efficiency, there are different types of the measures which are taken into consideration for

dealing with such unethical practices. I have felt that there it is important for the individuals and

government to give emphasis on paying tax as it helps to full requirement of different functions.

In my opinion that it is responsibility of organizations to comply with their social, legal and

ethical requirement via paying tax.

I have evaluated that there are various skills that has helped me to meet the needs of

particular assignment such as effective research, analytical, communication and decision-

making. These have contributed in conducting effective gathering of information such as

different taxes imposed by government, distinguish between direct and tax expenditure, three

distinct measures used to avoid or minimize taxes and two actions taken for combating tax

avoidance schemes. In addition, this, the main objective of the particular approach is to apply

rules for counteract tax benefits that are arising from m artificial tax arrangements. From the

assessment of the apicultural strategy that is executed by the UK government includes that

having effective ability to deal with abusive tax arrangements for having fair & consistent

functioning.

Through HMRC and GAAR the governing authority implies the measure to control the

tax avoidance by the individuals and the MNCs and corporates. These two strategies are used at

global level by the governments of different nations. By these the governments of the various

countries makes sure that the tax is paid to the government of the country in which the actual

operations of the companies are being carried out. Penalties are imposed on the defaulters or

unethical advantage seekers. These measures aim at bringing transparency and ethnicity in the

procedures of tax collection.

PART B

Providing report on the lessons learnt from preparation of the assignment along with the benefits

and difficulties faced

Gibbs reflective model is one of the significant theory that is related with having six

stages such as descriptions, feelings, evaluation, analysis, conclusion and action plan (Gibbs'

Reflective Cycle, 2022). There are different types of organization which operate in UK and

conducts the activities like tax avoidance and evasion. I have come to know that tax avoidance

and evasion provides the benefits to individuals but has negative impact on government

efficiency, there are different types of the measures which are taken into consideration for

dealing with such unethical practices. I have felt that there it is important for the individuals and

government to give emphasis on paying tax as it helps to full requirement of different functions.

In my opinion that it is responsibility of organizations to comply with their social, legal and

ethical requirement via paying tax.

I have evaluated that there are various skills that has helped me to meet the needs of

particular assignment such as effective research, analytical, communication and decision-

making. These have contributed in conducting effective gathering of information such as

different taxes imposed by government, distinguish between direct and tax expenditure, three

distinct measures used to avoid or minimize taxes and two actions taken for combating tax

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

avoidance. Presenting the information in corrective form has become possible for m with help of

good communication and critical thinking. With help of logical and analytical rationale has aided

me to review information in depth manner so that corrective meaning can be drawn. The

decision-making skills helped to choose the corrective data for making the study more reliable

and valid.

I have analyzed that, there are few lacking areas as well which are required to be

improved in respect to gain significant ability of improvement. The set of weaknesses comprises

lack of time management, organizing and low well verse in technology. I have experienced

difficulty in using different functions to gather information with maintaining ease. In addition to

this, unable to coordinate with the time provided for accomplishing the target of completing

study. There were difficulty in managing tasks precisely so that proper structure can be obtained.

In m my views lack of organizing has lead to ineffective time management difficulty which is

required to be improved.

On the basis of this, it can be concluded that with help of the set of strengths such as

effective communication, analytical, etc. skills I have made good reliable study. In addition to

this, I will implement action plan for time management and organizing such as prioritizing

activities, setting limits for completing task, etc. For improving technological knowledge

emphasis on having courses and involving into practical exposure will be conducted by me to

achieve better performance.

Giving reflection for the lesson learnt from the formulation of the assessment

Gibbs is reliable model that are highly taken into procedure for expressing the views

regarding particular experience through distinction into six different parts (Chang, 2019). This

involves expressing via giving information about description of situation, feelings obtained,

evaluation & analysis, concluding and taking action plan. There are distinct form of the

enterprises that operates in distinct patter which require coordinating with ethical requirements

via paying accurate taxes on time. In my opinion there are distinct types of taxes which are

imposed by the governments so that appropriate accomplishment of its function can become

possible. Tax paying is mandatory as per the given criteria of income earning which is referred

as expenditure by individuals and organizations in respect to eliminate incurring of expenses

firm focuses on tax avoidance & evasion that tend to offer benefits.

good communication and critical thinking. With help of logical and analytical rationale has aided

me to review information in depth manner so that corrective meaning can be drawn. The

decision-making skills helped to choose the corrective data for making the study more reliable

and valid.

I have analyzed that, there are few lacking areas as well which are required to be

improved in respect to gain significant ability of improvement. The set of weaknesses comprises

lack of time management, organizing and low well verse in technology. I have experienced

difficulty in using different functions to gather information with maintaining ease. In addition to

this, unable to coordinate with the time provided for accomplishing the target of completing

study. There were difficulty in managing tasks precisely so that proper structure can be obtained.

In m my views lack of organizing has lead to ineffective time management difficulty which is

required to be improved.

On the basis of this, it can be concluded that with help of the set of strengths such as

effective communication, analytical, etc. skills I have made good reliable study. In addition to

this, I will implement action plan for time management and organizing such as prioritizing

activities, setting limits for completing task, etc. For improving technological knowledge

emphasis on having courses and involving into practical exposure will be conducted by me to

achieve better performance.

Giving reflection for the lesson learnt from the formulation of the assessment

Gibbs is reliable model that are highly taken into procedure for expressing the views

regarding particular experience through distinction into six different parts (Chang, 2019). This

involves expressing via giving information about description of situation, feelings obtained,

evaluation & analysis, concluding and taking action plan. There are distinct form of the

enterprises that operates in distinct patter which require coordinating with ethical requirements

via paying accurate taxes on time. In my opinion there are distinct types of taxes which are

imposed by the governments so that appropriate accomplishment of its function can become

possible. Tax paying is mandatory as per the given criteria of income earning which is referred

as expenditure by individuals and organizations in respect to eliminate incurring of expenses

firm focuses on tax avoidance & evasion that tend to offer benefits.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

I have got feeling that in order to get proper economic development it is essential fro the

companies to pay off their tax liabilities so that significant growth for citizen can become

possible. For this purpose meeting the tax liabilities in precise and fair manner is crucial

according to me so that greater government support for development can be received (Menekse,

2020). I have evaluated that there are set of strengths which has provided me assistance to

complete wok in effective work. This comprises having effective presentation & research tactic,

having higher level of concentration for paying attention on each detail and gaining significant

time management. These all has contributed me to develop highly valid study via referring each

crucial points so that significant knowledge can developed. From the analysis, I have analysed

that there are various aspects which severed as weaker areas that involves lack of communication

,organizing and creative problem solving. On the basis of this, it can be interpreted that these are

required to be modified in respect to make changes so that higher effective performance for

further activities can become possible.

It can be concluded that having effective understanding of taxation is important in

respect to meet the ethical conducting that government has taken different kinds of action for

avoiding irrelevant practices like tax evasion & avoidance for receiving personal benefits. In my

view there is need of taking reliable improvement actions so that higher level of performance to

coordinate with changing circumstances via gaining competitive advantages can become

possible. The action plan which I will implement to get improved communication skill having

reliable tutorials, indulging into communication based competition, etc. can provide assistance.

In addition to this, Organizing can be modified by having appropriate identification of prioritize

activity so that managing in appropriate formate exertion become possible. For improving the

creative problem solving approach in me, the major course of action which can be taken into

process involves having significant participation in case solving activities, getting relevant

pattern of knowledge of different method to resolve issues, etc. On the basis of this it can be

interpreted that these all improvement can help in gaining greater level of knowledge.

CONCLUSION

Based on the above report the meaning of tax principles have been made clear. The report

has highlighted the major functions of the governing body and how the taxes are used to create

the required means for the fulfilment of the sources. The report has outlined the differences

between the direct expenditures and the tax expenditures. Three different measures namely IP

companies to pay off their tax liabilities so that significant growth for citizen can become

possible. For this purpose meeting the tax liabilities in precise and fair manner is crucial

according to me so that greater government support for development can be received (Menekse,

2020). I have evaluated that there are set of strengths which has provided me assistance to

complete wok in effective work. This comprises having effective presentation & research tactic,

having higher level of concentration for paying attention on each detail and gaining significant

time management. These all has contributed me to develop highly valid study via referring each

crucial points so that significant knowledge can developed. From the analysis, I have analysed

that there are various aspects which severed as weaker areas that involves lack of communication

,organizing and creative problem solving. On the basis of this, it can be interpreted that these are

required to be modified in respect to make changes so that higher effective performance for

further activities can become possible.

It can be concluded that having effective understanding of taxation is important in

respect to meet the ethical conducting that government has taken different kinds of action for

avoiding irrelevant practices like tax evasion & avoidance for receiving personal benefits. In my

view there is need of taking reliable improvement actions so that higher level of performance to

coordinate with changing circumstances via gaining competitive advantages can become

possible. The action plan which I will implement to get improved communication skill having

reliable tutorials, indulging into communication based competition, etc. can provide assistance.

In addition to this, Organizing can be modified by having appropriate identification of prioritize

activity so that managing in appropriate formate exertion become possible. For improving the

creative problem solving approach in me, the major course of action which can be taken into

process involves having significant participation in case solving activities, getting relevant

pattern of knowledge of different method to resolve issues, etc. On the basis of this it can be

interpreted that these all improvement can help in gaining greater level of knowledge.

CONCLUSION

Based on the above report the meaning of tax principles have been made clear. The report

has highlighted the major functions of the governing body and how the taxes are used to create

the required means for the fulfilment of the sources. The report has outlined the differences

between the direct expenditures and the tax expenditures. Three different measures namely IP

structuring, thin capitalization and validity of schemes that are used by the multinationals for tax

avoidance of tax payment have been discussed based on this report. The report has drawn the

clear distinction between the tax evasion and tax avoidance. Two measures that are HMRC and

GAAR have been analysed in the report based on their utilization by the governments to combat

or to respond to the tax avoidance by the individuals and corporate. Further, in part B of the

report a reflected report has been made using Gibbs reflective model for demonstrating the

lessons captured with the preparation of the report.

avoidance of tax payment have been discussed based on this report. The report has drawn the

clear distinction between the tax evasion and tax avoidance. Two measures that are HMRC and

GAAR have been analysed in the report based on their utilization by the governments to combat

or to respond to the tax avoidance by the individuals and corporate. Further, in part B of the

report a reflected report has been made using Gibbs reflective model for demonstrating the

lessons captured with the preparation of the report.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.