TAX 101: Taxation Principles Assignment - Semester 1, University Name

VerifiedAdded on 2020/05/16

|14

|613

|48

Homework Assignment

AI Summary

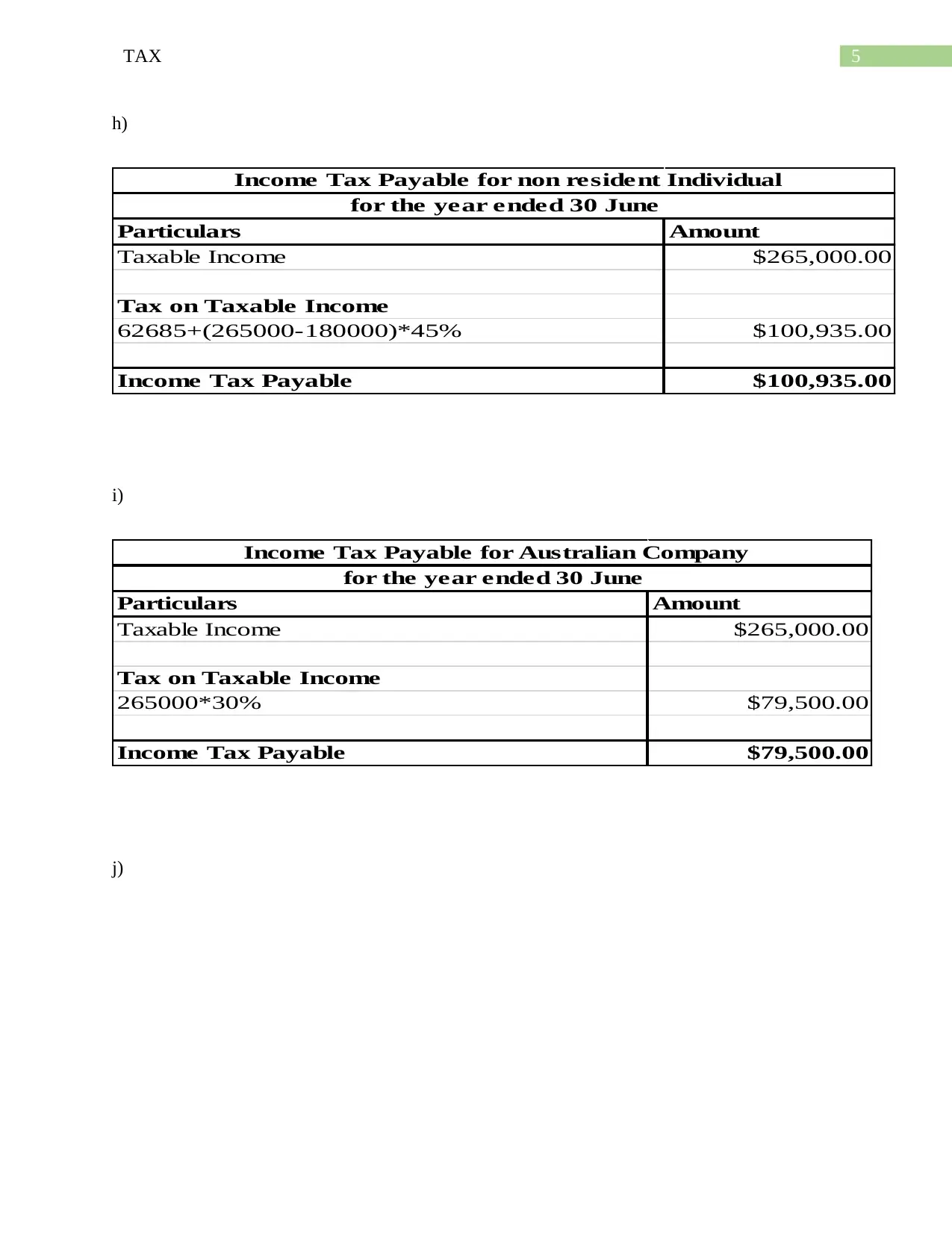

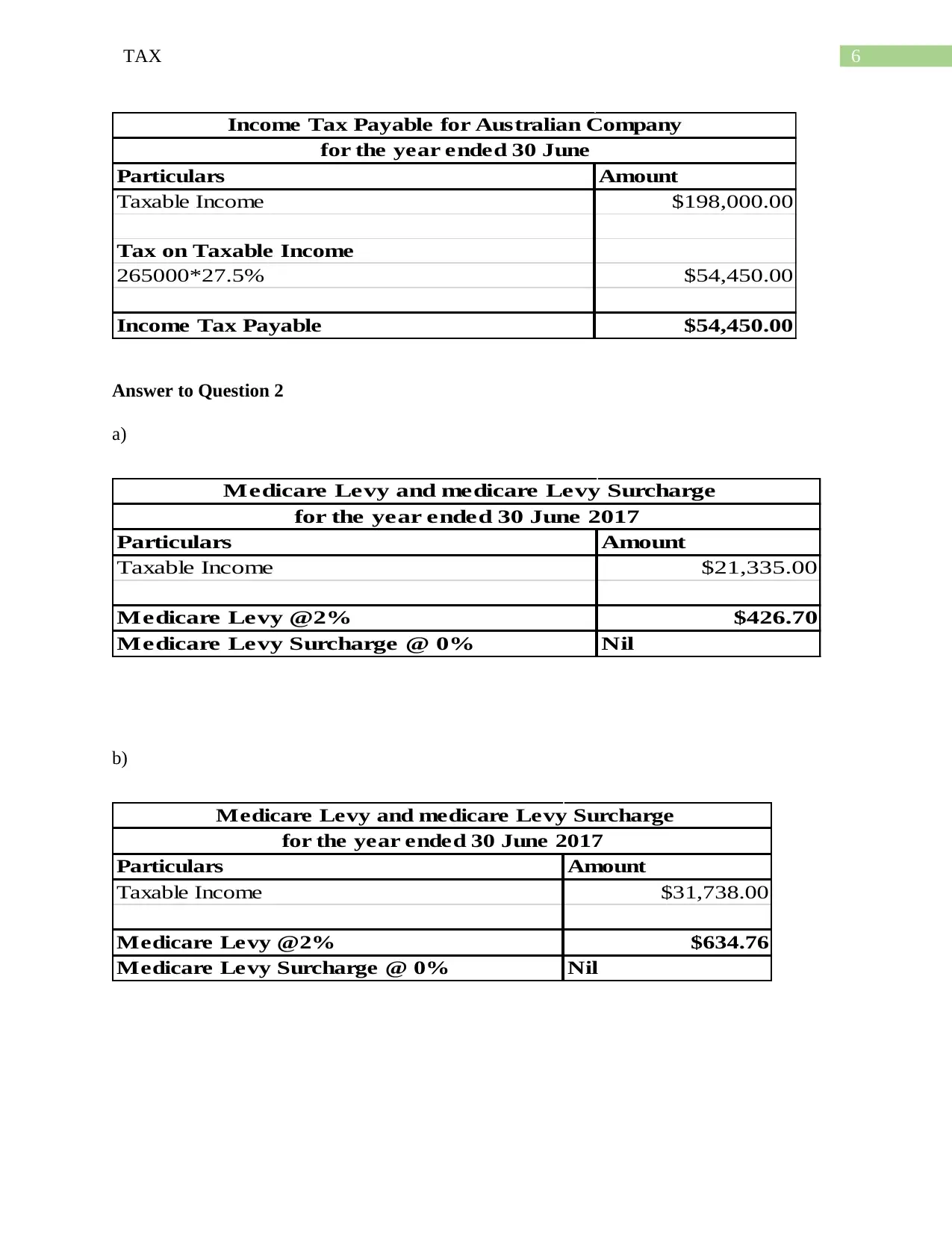

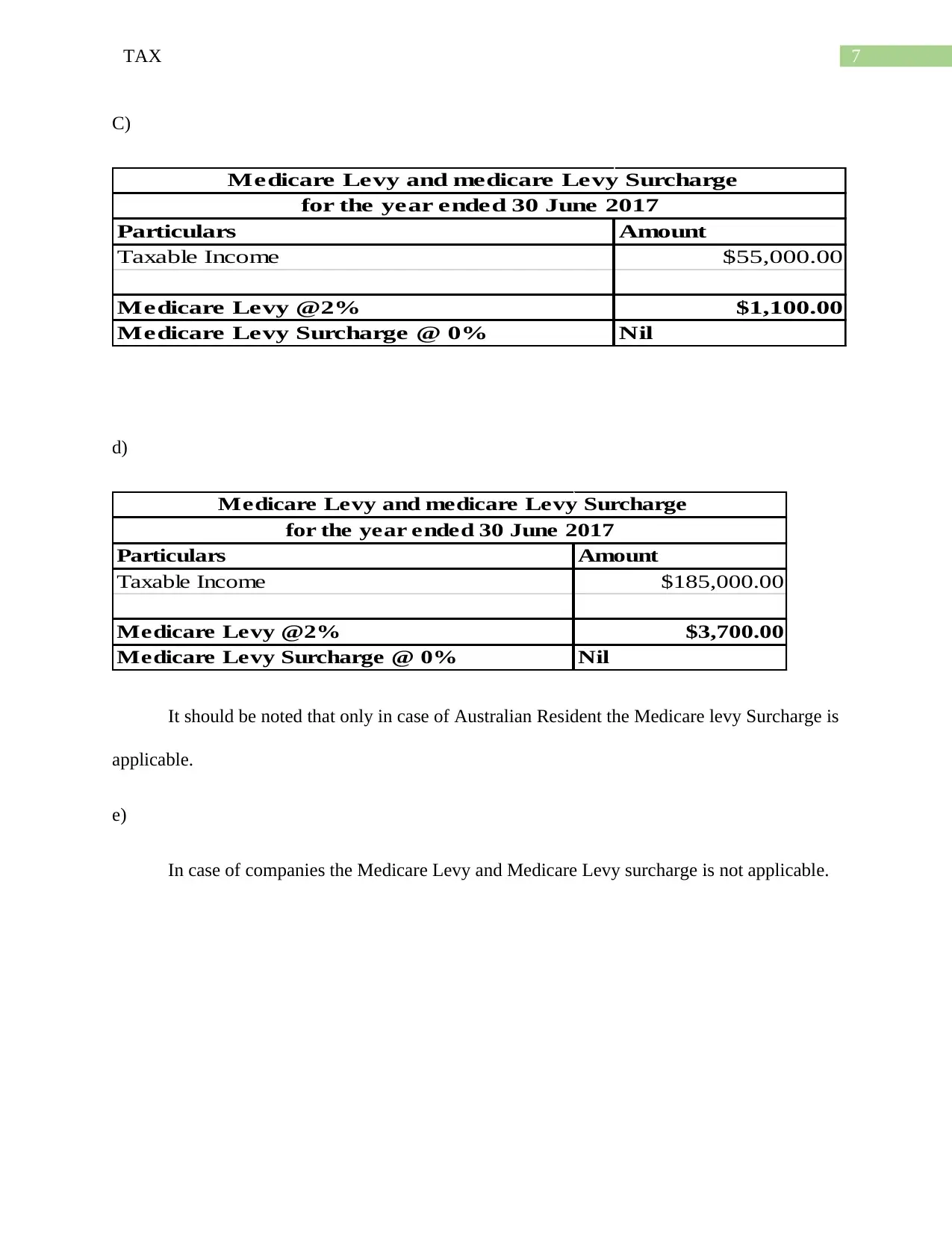

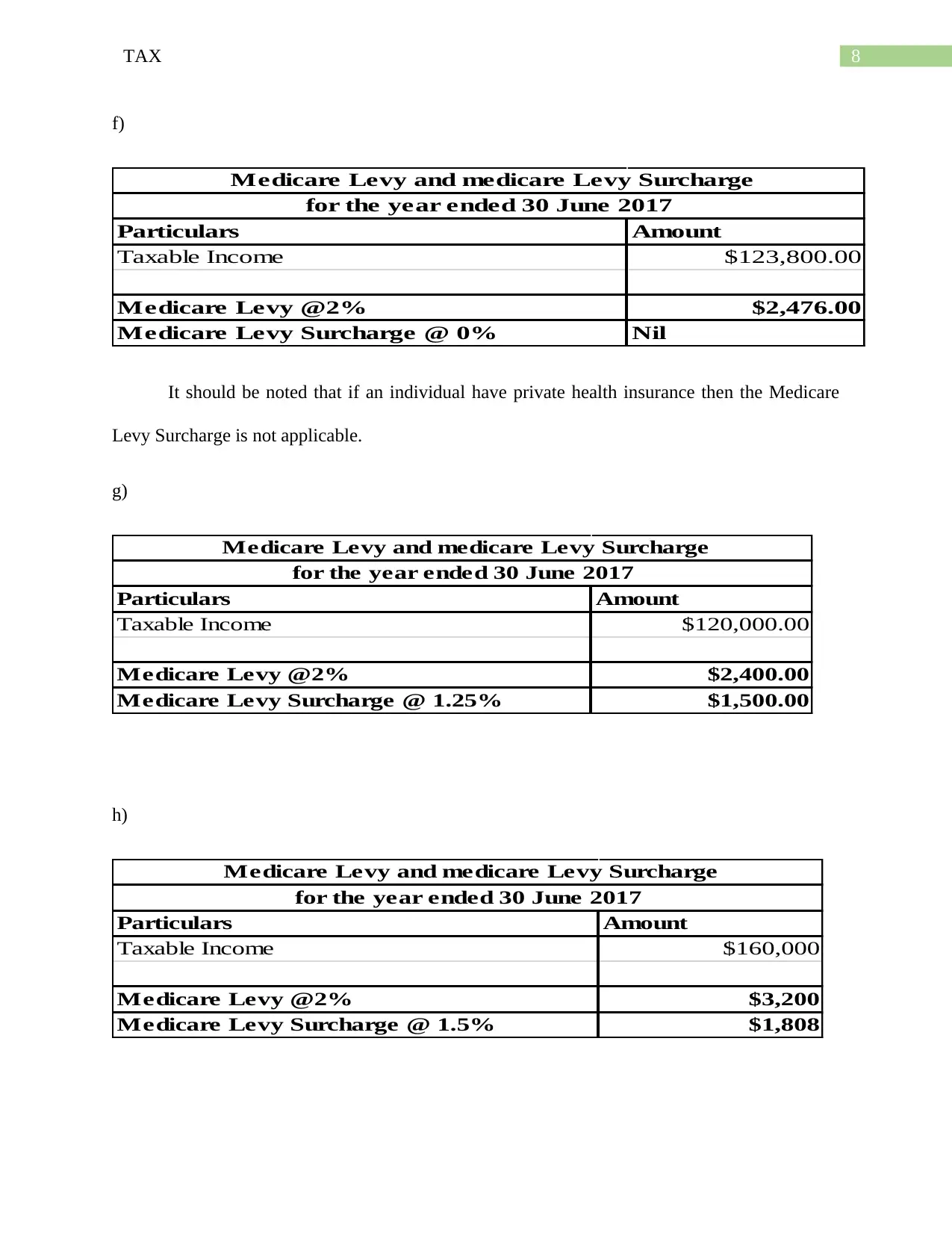

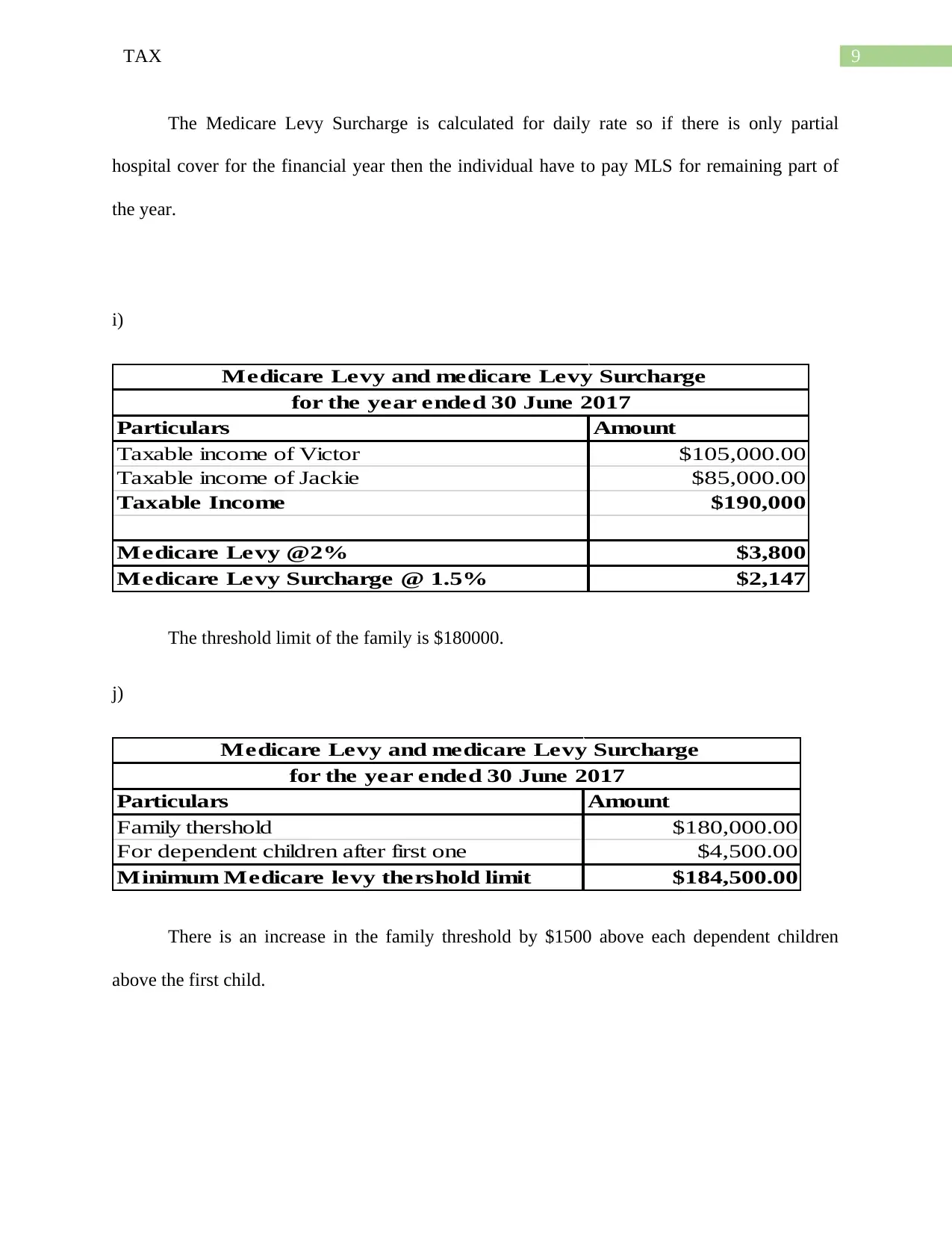

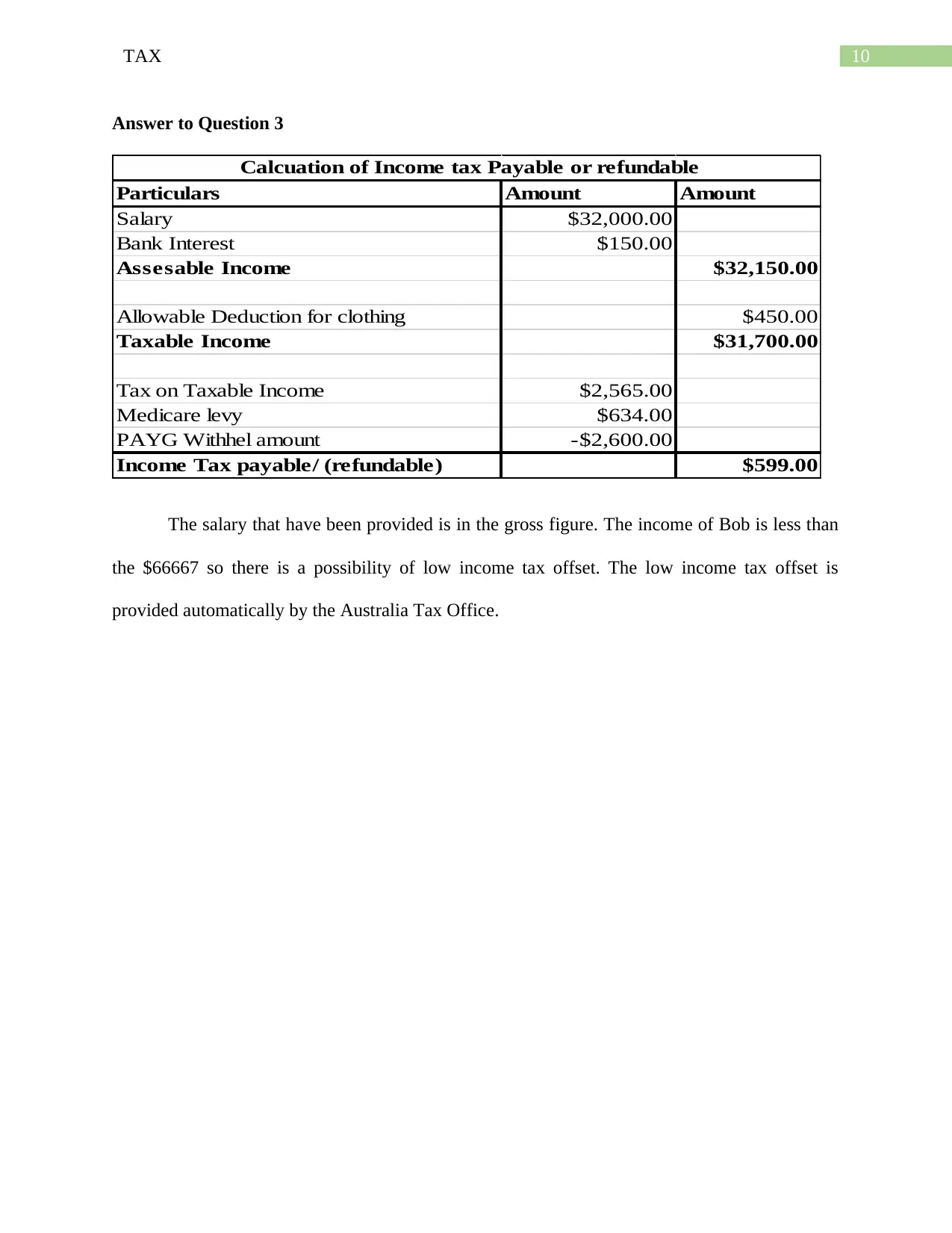

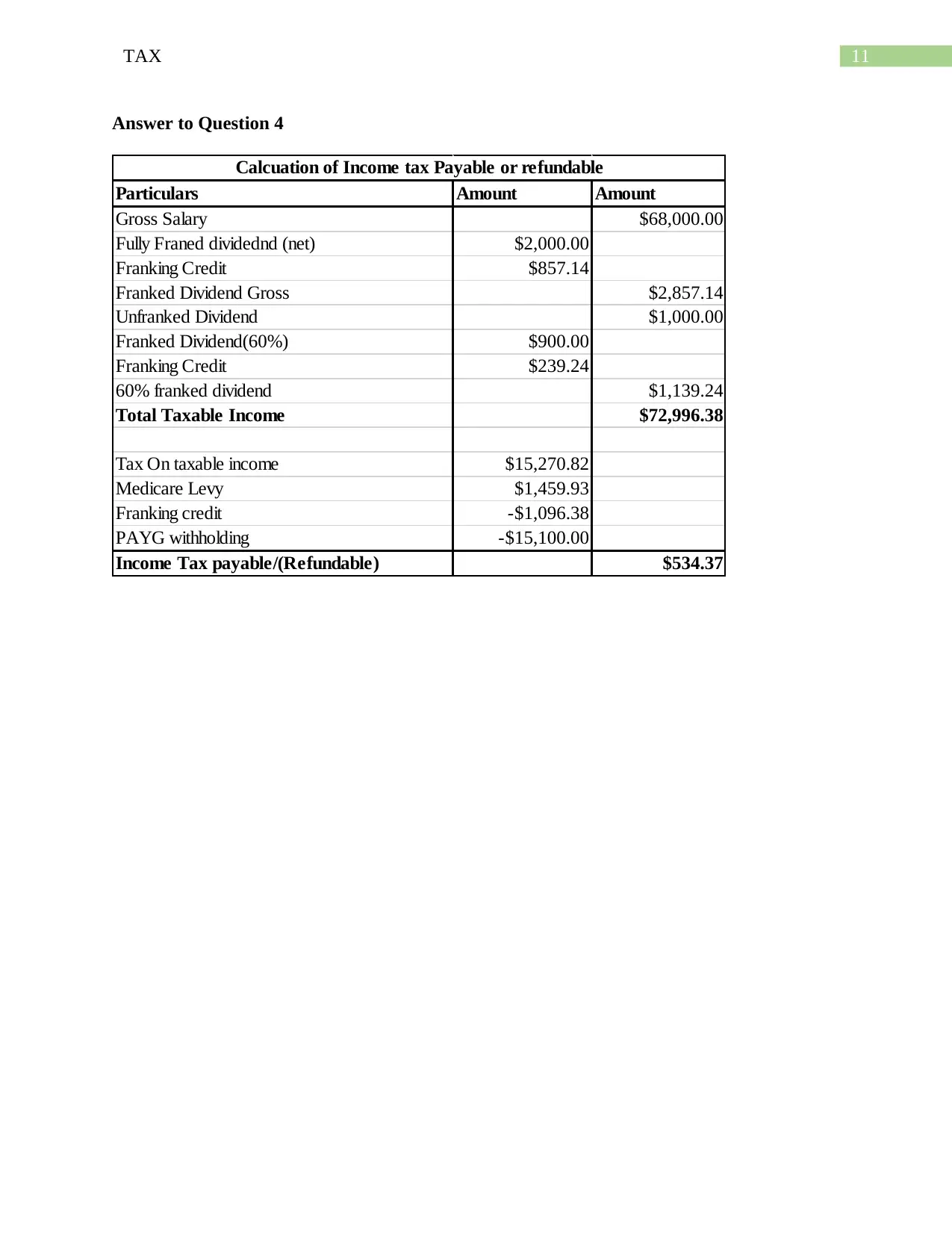

This document is a solution to a TAX assignment, focusing on Australian taxation principles. It addresses several questions related to tax calculations, including the Medicare Levy Surcharge (MLS), its applicability to residents, and the thresholds for family income. The assignment covers scenarios where MLS is not applicable, such as for companies and individuals with private health insurance. It also explores the calculation of the MLS based on a daily rate for partial hospital cover. Furthermore, the solution analyzes a case involving a gross salary and the potential for a low-income tax offset, which is automatically provided by the Australian Tax Office. The assignment concludes with a bibliography of relevant sources used in the solution.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.