Taxation Law Report: Taxation of Income and Capital Gains in Australia

VerifiedAdded on 2020/11/23

|10

|2642

|408

Report

AI Summary

This report provides an overview of Australian taxation law, addressing the treatment of annuity income from lottery winnings, the computation of taxable income for a pharmacy, and the relevance of the IRC v Duke of Westminster case regarding tax avoidance in the Australian context. It further examines the allocation of losses, expenses, and capital gains or losses arising from the sale of a rental property, considering relevant deductions and the treatment of losses. The report explores these topics through case studies and legal principles, offering a comprehensive analysis of taxation concepts and their practical application. The analysis includes the specifics of GST exemptions, the implications of tax avoidance, and the handling of capital losses and gains, providing a detailed insight into the complexities of Australian taxation law.

TAXATION LAW

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

QUESTION 1 ..................................................................................................................................1

Presenting treatment of annual payment of Annuity income......................................................1

QUESTION 2...................................................................................................................................2

Computation of taxable income of Corner Pharmacy.................................................................2

QUESTION 3...................................................................................................................................3

Principle laid down case of IRC v Duke of Westminster [1936] AC 1 and discussing its

relevancy IN Australia in present time........................................................................................3

QUESTION 4...................................................................................................................................5

Allocation of losses of expenses and capital gain/loss on sale of property................................5

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

QUESTION 1 ..................................................................................................................................1

Presenting treatment of annual payment of Annuity income......................................................1

QUESTION 2...................................................................................................................................2

Computation of taxable income of Corner Pharmacy.................................................................2

QUESTION 3...................................................................................................................................3

Principle laid down case of IRC v Duke of Westminster [1936] AC 1 and discussing its

relevancy IN Australia in present time........................................................................................3

QUESTION 4...................................................................................................................................5

Allocation of losses of expenses and capital gain/loss on sale of property................................5

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION

Taxation is one of most crucial part for an individual, business and government.

Individuals and organisation have to pay taxes on their income and GST(goods and sales tax)

on sale of goods and services, while for government it is a huge source of revenue. In present

report, treatment of income generated from various sources is presented along with capital

gain/loss and their taxation. along With this, discussion of principle established in case of IRC v

Duke of Westminster [1936] AC 1 is done with its relevancy in present time of Australia.

QUESTION 1

Presenting treatment of annual payment of Annuity income

Issue: An individual of Australia won a lottery and received an amount of $50000 per year for

20 years. Lottery was conducted by National Lottery Commission. For first year, $50000 was

paid immediately after informing him about the winning. For subsequent amount, annual

payments were paid on first anniversary of pyment. In case winner dies, remaining amount will

be transferred to estate of deceased by the commission.

Rule:

Australian taxation office: Income earned from lotterze is defined under subheading of

prize and award winning, of other income (Buchanan, J., 2018). As per this, income earned form

lottery, raffles and lottos are not taxable in Australia.

Section 160ZB: As per, Part 3 of Taxation Act, 1977 of Australia, winning from lottery

is treated as capital gains and Section 160ZB (2) defines that capital gain taxdo not arise on such

amount.

Capital gain taxes: In case a property is purchased ffrom amount that is earned from

winning lotteries and subsequently it is sold, capital loss/gain will arise. On profits, capital gain

tax will be charged and a 50 % deduction can be claimed from tax.

Amount transferred to Estate of deceased: In case a person is not nominated a as

legal heirs of the individual who ha won lottery, and in event of death of that person remaining

amount winning will be transferred to estate of deceased (Mnk, Nagle and Coss, 2017) . The

amount in this account, is latter on distributed among legal inheritors of that person.

Application: With application of ruling of ATO and Section 160ZB (2) -(3), it can be stated that

income from any winnings is an assets but it can not be charged to capital gain tax.

1

Taxation is one of most crucial part for an individual, business and government.

Individuals and organisation have to pay taxes on their income and GST(goods and sales tax)

on sale of goods and services, while for government it is a huge source of revenue. In present

report, treatment of income generated from various sources is presented along with capital

gain/loss and their taxation. along With this, discussion of principle established in case of IRC v

Duke of Westminster [1936] AC 1 is done with its relevancy in present time of Australia.

QUESTION 1

Presenting treatment of annual payment of Annuity income

Issue: An individual of Australia won a lottery and received an amount of $50000 per year for

20 years. Lottery was conducted by National Lottery Commission. For first year, $50000 was

paid immediately after informing him about the winning. For subsequent amount, annual

payments were paid on first anniversary of pyment. In case winner dies, remaining amount will

be transferred to estate of deceased by the commission.

Rule:

Australian taxation office: Income earned from lotterze is defined under subheading of

prize and award winning, of other income (Buchanan, J., 2018). As per this, income earned form

lottery, raffles and lottos are not taxable in Australia.

Section 160ZB: As per, Part 3 of Taxation Act, 1977 of Australia, winning from lottery

is treated as capital gains and Section 160ZB (2) defines that capital gain taxdo not arise on such

amount.

Capital gain taxes: In case a property is purchased ffrom amount that is earned from

winning lotteries and subsequently it is sold, capital loss/gain will arise. On profits, capital gain

tax will be charged and a 50 % deduction can be claimed from tax.

Amount transferred to Estate of deceased: In case a person is not nominated a as

legal heirs of the individual who ha won lottery, and in event of death of that person remaining

amount winning will be transferred to estate of deceased (Mnk, Nagle and Coss, 2017) . The

amount in this account, is latter on distributed among legal inheritors of that person.

Application: With application of ruling of ATO and Section 160ZB (2) -(3), it can be stated that

income from any winnings is an assets but it can not be charged to capital gain tax.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

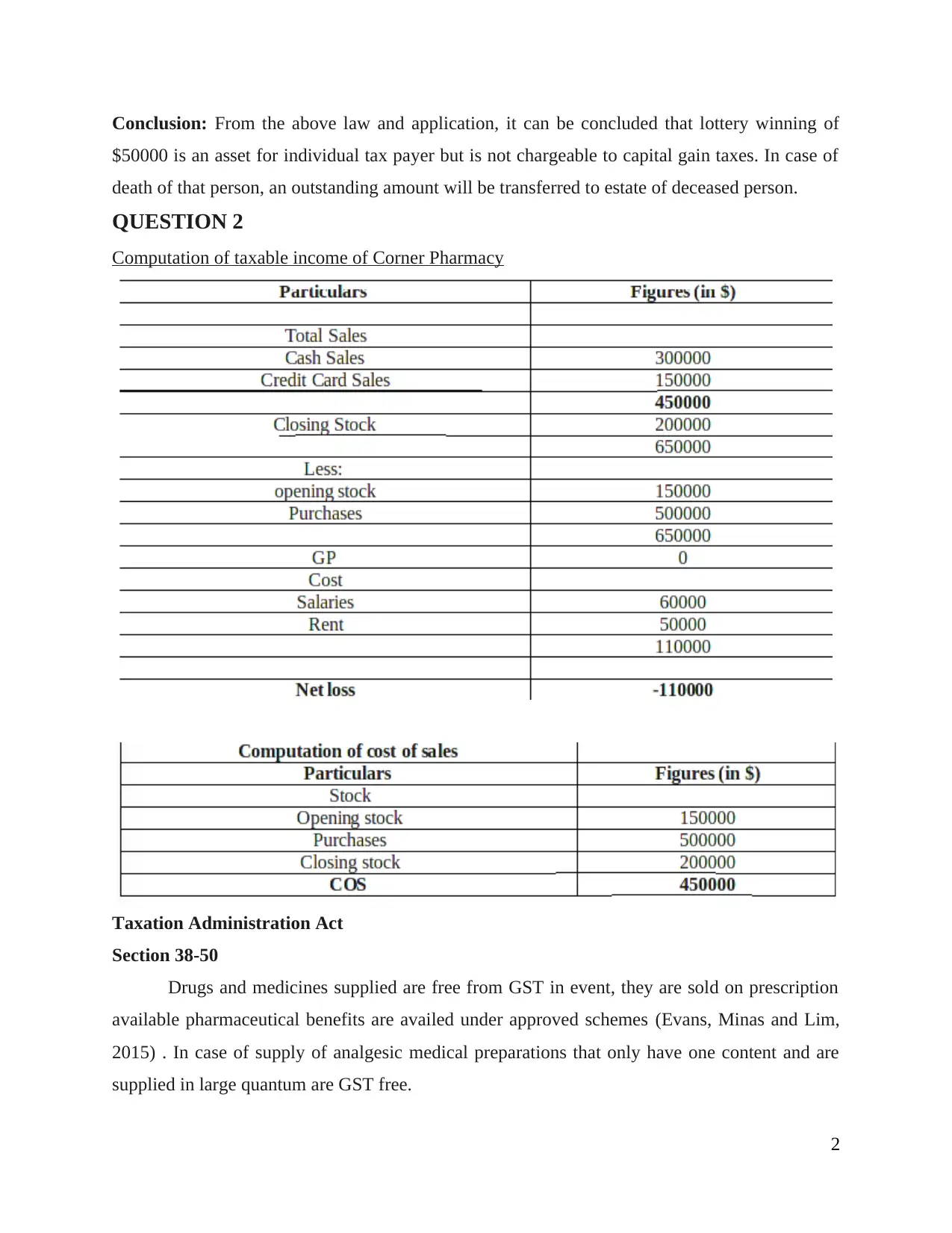

Conclusion: From the above law and application, it can be concluded that lottery winning of

$50000 is an asset for individual tax payer but is not chargeable to capital gain taxes. In case of

death of that person, an outstanding amount will be transferred to estate of deceased person.

QUESTION 2

Computation of taxable income of Corner Pharmacy

Taxation Administration Act

Section 38-50

Drugs and medicines supplied are free from GST in event, they are sold on prescription

available pharmaceutical benefits are availed under approved schemes (Evans, Minas and Lim,

2015) . In case of supply of analgesic medical preparations that only have one content and are

supplied in large quantum are GST free.

2

$50000 is an asset for individual tax payer but is not chargeable to capital gain taxes. In case of

death of that person, an outstanding amount will be transferred to estate of deceased person.

QUESTION 2

Computation of taxable income of Corner Pharmacy

Taxation Administration Act

Section 38-50

Drugs and medicines supplied are free from GST in event, they are sold on prescription

available pharmaceutical benefits are availed under approved schemes (Evans, Minas and Lim,

2015) . In case of supply of analgesic medical preparations that only have one content and are

supplied in large quantum are GST free.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 3

Principle laid down case of IRC v Duke of Westminster [1936] AC 1 and discussing its

relevancy in Australia in present time

IRC v Duke of Westminster [1936] AC 1

In this case, Duke, a tax payer used to pay 3 pounds to his gardener per week. He

executed a deed with his gardener and according to which duke will pay an equivalent amount to

the gardener and Duke stopped paying himwages (Burkhauser, Hahn and Wilkins, 2015). The

wages paid to gardner did not attract any tax deduction at that time but it reduced surtax liability

of Duke. According to Justin Tomlin who heard this case, stated it as the right act where the

wages were paid from his after tax income which reduced surtax liability of Duke. .

Principle was formed with conclusion of this case:

“This Principle states that a Person is Entitled for Making any Unlawful Arrangement of his/her

Financial Affairs that he/she Sees Fit to Reduce Tax Liability.”

From the above statement, it can be indicated that principle established in Australia with

conclusion of this case was for “ TAX AVOIDANCE”.

Tax avoidance

Tax avoidance can be defied as use of legal methods to modify financial situations of

individual to lower the amount of income tax liability. The process is followed by claiming

deduction and credits. This is a practice which is different from tax evasion which is an illegal

method for reducing tax payable. This law was first built by Indian Revenue Code when it was

held in court that a person when legally plans his income tax liability cannot be compelled to pay

more tax.

Relevance of tax avoidance in Australia

With conclusion from case headed by Justice Tomlin, stated that no one can be forced to

pay extra tax on the income which had been reduced with proper planning and application of

legal laws. A term in taxation was formed in name of Tax Avoidance which islegal for a person

to use, for reducing tax liability (Australian Tax Avoidance, 2018). With time, many rules and

regulations were made and deleted for this principle. By passing time, it got relevance in taxation

law and for its legal application, legislations were made and stated out in Taxation Act of

3

Principle laid down case of IRC v Duke of Westminster [1936] AC 1 and discussing its

relevancy in Australia in present time

IRC v Duke of Westminster [1936] AC 1

In this case, Duke, a tax payer used to pay 3 pounds to his gardener per week. He

executed a deed with his gardener and according to which duke will pay an equivalent amount to

the gardener and Duke stopped paying himwages (Burkhauser, Hahn and Wilkins, 2015). The

wages paid to gardner did not attract any tax deduction at that time but it reduced surtax liability

of Duke. According to Justin Tomlin who heard this case, stated it as the right act where the

wages were paid from his after tax income which reduced surtax liability of Duke. .

Principle was formed with conclusion of this case:

“This Principle states that a Person is Entitled for Making any Unlawful Arrangement of his/her

Financial Affairs that he/she Sees Fit to Reduce Tax Liability.”

From the above statement, it can be indicated that principle established in Australia with

conclusion of this case was for “ TAX AVOIDANCE”.

Tax avoidance

Tax avoidance can be defied as use of legal methods to modify financial situations of

individual to lower the amount of income tax liability. The process is followed by claiming

deduction and credits. This is a practice which is different from tax evasion which is an illegal

method for reducing tax payable. This law was first built by Indian Revenue Code when it was

held in court that a person when legally plans his income tax liability cannot be compelled to pay

more tax.

Relevance of tax avoidance in Australia

With conclusion from case headed by Justice Tomlin, stated that no one can be forced to

pay extra tax on the income which had been reduced with proper planning and application of

legal laws. A term in taxation was formed in name of Tax Avoidance which islegal for a person

to use, for reducing tax liability (Australian Tax Avoidance, 2018). With time, many rules and

regulations were made and deleted for this principle. By passing time, it got relevance in taxation

law and for its legal application, legislations were made and stated out in Taxation Act of

3

Australia. As far as legality is concerned, it was made through providing certain deductions and

credits to taxpayer in country.

As per Australian taxation office, there is a big difference between tax avoidance and tax

evasion. One is legal and is carried out with compliance of legislation and another is illegal

done, by breaking the law.

Tax avoidance in Australia

According to ATO, tax planning is organisation of income and tax affairs of a person in

most effective way and within prescribed limits of taxation law. Tax avoidance on the other

hand is exploitation of tax system (Tax planning vs tax avoidance, 2018). To make it more legal

with law, the government of Australia have developed different schemes that a taxpayer must

abide with.

A focus on tax avoidance arrangements over past ten years were given and this resulted in

development and identification of themes or behaviour that involved high risk.

They are as follows:

Aggressive marketing of tac services

Aggressive marking of tax products

Incorrect implication of product ruling arrangements

Misuse of advice given by Australian taxation office

Misuse of ruling that have significant reason to trigger arguments

Use of ineffective disclaimers by promoters in their marketing

These are certain schemes and examples where people try to avoid tax and refer those

schemes as tax planning but it was made clear by formations of ruling form the above case, so a

person who is planning his income to reduce tax liability under any of the above head shall

carry it out with adherence with ruling and Australian taxation law.

This can be clearly expressed that tax avoidance in Australia is considered as

exploitation of tax law but is not considered as irrelevance. It has gained significance over past

years and strict rules and laws are made which must be mandatoril followed while commutation

of taxable income and claiming deductions; in case, it is not done it will be considered as tax

evasion which is an offense under Taxation Act of Australia and hence punishable.

4

credits to taxpayer in country.

As per Australian taxation office, there is a big difference between tax avoidance and tax

evasion. One is legal and is carried out with compliance of legislation and another is illegal

done, by breaking the law.

Tax avoidance in Australia

According to ATO, tax planning is organisation of income and tax affairs of a person in

most effective way and within prescribed limits of taxation law. Tax avoidance on the other

hand is exploitation of tax system (Tax planning vs tax avoidance, 2018). To make it more legal

with law, the government of Australia have developed different schemes that a taxpayer must

abide with.

A focus on tax avoidance arrangements over past ten years were given and this resulted in

development and identification of themes or behaviour that involved high risk.

They are as follows:

Aggressive marketing of tac services

Aggressive marking of tax products

Incorrect implication of product ruling arrangements

Misuse of advice given by Australian taxation office

Misuse of ruling that have significant reason to trigger arguments

Use of ineffective disclaimers by promoters in their marketing

These are certain schemes and examples where people try to avoid tax and refer those

schemes as tax planning but it was made clear by formations of ruling form the above case, so a

person who is planning his income to reduce tax liability under any of the above head shall

carry it out with adherence with ruling and Australian taxation law.

This can be clearly expressed that tax avoidance in Australia is considered as

exploitation of tax law but is not considered as irrelevance. It has gained significance over past

years and strict rules and laws are made which must be mandatoril followed while commutation

of taxable income and claiming deductions; in case, it is not done it will be considered as tax

evasion which is an offense under Taxation Act of Australia and hence punishable.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUESTION 4

Allocation of losses of expenses and capital gain/loss on sale of property

Issue: As per case study, Joseph was an accountant and his wife, Jane who was a

housewife borrowed some money for purchasing rental property as joint tenants. In the

agreement, it was written that any profit from this property will be shared in ratio of 80:20 and

loss will by fully born by husband only. For previous year, the rental property incurred losses of

$40000.

Rules

Residential Rental Property: In case of owing a rental property, a person can claim certain

expenses as deductions from rental income must be declared in individual tax return. Income

from rental property will be reflected in personal income of taxpayer under ordinary-income.

Deduction allowed

1. Management fee of real estate

2. Advertisement expenses for rental property

3. Insurance premiums

4. Interest on loan/mortgagor for such rental house

5. Depreciation charged on such asset.

Items not allowed as deduction

1. Personal usage expenses for such rental property

2. Bill expenses paid for utilities on such asset

3. Expenditure incurred for purchase and sale of rental house; and

4. Loan/mortgage amount.

5

Allocation of losses of expenses and capital gain/loss on sale of property

Issue: As per case study, Joseph was an accountant and his wife, Jane who was a

housewife borrowed some money for purchasing rental property as joint tenants. In the

agreement, it was written that any profit from this property will be shared in ratio of 80:20 and

loss will by fully born by husband only. For previous year, the rental property incurred losses of

$40000.

Rules

Residential Rental Property: In case of owing a rental property, a person can claim certain

expenses as deductions from rental income must be declared in individual tax return. Income

from rental property will be reflected in personal income of taxpayer under ordinary-income.

Deduction allowed

1. Management fee of real estate

2. Advertisement expenses for rental property

3. Insurance premiums

4. Interest on loan/mortgagor for such rental house

5. Depreciation charged on such asset.

Items not allowed as deduction

1. Personal usage expenses for such rental property

2. Bill expenses paid for utilities on such asset

3. Expenditure incurred for purchase and sale of rental house; and

4. Loan/mortgage amount.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Allocation of loss for taxation purpose

Expenses incurred on rental property on interest and other maintenance expenditure are

deducted from gross rental income (AbdulRazaq and Adam, 2015). In case rental property is not

rented out and expenses are incurred on it, same will be treated as loss of expenses. Loss of

expenses can be treated as capital losses and will be charged against capital gains from property

and in case, there is no capital gain as it will be carried forward to next year.

Capital gain and loss for sale of rental property

Capital gain/loss arises on a property when it is disposed of, which means it is sold out.

The difference between cost base and sales proceeds of the house is considered as capital

gain/loss. Cost base is total of purchase price of the house, expenses incurred on developments of

property. The amounts which can be claimed as deduction are not added in cost base. The

expenditure which are included in cost base are related with expenses on search of title,

conveyance charged incurred to travel from and to property, valuation fees, and stamp duty

(Johnston, 2017). This adding up of expenses in cost base of property reduced the amount of

capital gain, thus reduces tax liability on such gains on sale of rental asset. They are added in

ordinary income of individual and capital losses are adjusted against profits and if left are carry

forward to the next financial year.

Deduction: 50 % of capital gain can be claimed as deduction on sale of rental property

Assumption

In present case, there is no specific information about sources of loss $40000. Expenses

are deducted from Gross Rental Income so $40000 are considered as expenses incurred on such

property related with maintenance and interest paid on rental asset . Here, it is assumed that there

was no rental income from house from previous financing year as it was vacant for whole year.

The reason for this is that, in, second part of question it is clearly given that 'if property is sold',

so loss of $40000 is not considered as capital loss on sale of property.

Gross income= 0

Expenses= $40000

Loss of expenses= 0-40000 = -$40000

Another assumption is that property was purchase after 19th September 1985.

1

Expenses incurred on rental property on interest and other maintenance expenditure are

deducted from gross rental income (AbdulRazaq and Adam, 2015). In case rental property is not

rented out and expenses are incurred on it, same will be treated as loss of expenses. Loss of

expenses can be treated as capital losses and will be charged against capital gains from property

and in case, there is no capital gain as it will be carried forward to next year.

Capital gain and loss for sale of rental property

Capital gain/loss arises on a property when it is disposed of, which means it is sold out.

The difference between cost base and sales proceeds of the house is considered as capital

gain/loss. Cost base is total of purchase price of the house, expenses incurred on developments of

property. The amounts which can be claimed as deduction are not added in cost base. The

expenditure which are included in cost base are related with expenses on search of title,

conveyance charged incurred to travel from and to property, valuation fees, and stamp duty

(Johnston, 2017). This adding up of expenses in cost base of property reduced the amount of

capital gain, thus reduces tax liability on such gains on sale of rental asset. They are added in

ordinary income of individual and capital losses are adjusted against profits and if left are carry

forward to the next financial year.

Deduction: 50 % of capital gain can be claimed as deduction on sale of rental property

Assumption

In present case, there is no specific information about sources of loss $40000. Expenses

are deducted from Gross Rental Income so $40000 are considered as expenses incurred on such

property related with maintenance and interest paid on rental asset . Here, it is assumed that there

was no rental income from house from previous financing year as it was vacant for whole year.

The reason for this is that, in, second part of question it is clearly given that 'if property is sold',

so loss of $40000 is not considered as capital loss on sale of property.

Gross income= 0

Expenses= $40000

Loss of expenses= 0-40000 = -$40000

Another assumption is that property was purchase after 19th September 1985.

1

Application

With application of rule and above assumption for part one of the question, losses of

$40000 are' loss of expenses' and will be treated as capital losses. The treatment of capital losses

is done as, deduction from capital gain for the current year and in case, there in no capital gain,

they will be carried forwarded to next year. Capital gain on sale of property are included in

ordinary income of an individual taxpayer.

Conclusion

Loss of expenses of $40000: They will be charged against capital gain for the same

financial year and in case, there is no such profit , it will be carried subsequent financial year.

Profit on sale of property: If profits arise on sale of rental asses, it will be capital gain

and will be added in ordinary income of Joseph and Jane in the ratio 80:20 as mentioned in the

rental property purchase agreement. In such case 50% deduction can be claimed on such gain

after adjusting/deducting any capital losses of previous and current financial year.

Loss on sale of property: If property sold at a price lower than cost base, there is a case

of capital loss. This loss along with loss of $40000, will be forwarded to coming financial year.

Both losses will cumulatively carried forward to next year.

CONCLUSION

From the above report, it can be concluded lottery winning are considered as an asset in

Australia but are free from capital gain taxes. This income does not become part of ordinary

income of a person. Further, is can be stated that taxable income of Corner Pharmacy calculated

on accrual basis and is tax free. The principle stated in IRC v Duke of Westminster [1936] AC 1

case was of tax avoidance and it can be articulated that in present time it has relevance in

Australia with application of rules and legislations.

1

With application of rule and above assumption for part one of the question, losses of

$40000 are' loss of expenses' and will be treated as capital losses. The treatment of capital losses

is done as, deduction from capital gain for the current year and in case, there in no capital gain,

they will be carried forwarded to next year. Capital gain on sale of property are included in

ordinary income of an individual taxpayer.

Conclusion

Loss of expenses of $40000: They will be charged against capital gain for the same

financial year and in case, there is no such profit , it will be carried subsequent financial year.

Profit on sale of property: If profits arise on sale of rental asses, it will be capital gain

and will be added in ordinary income of Joseph and Jane in the ratio 80:20 as mentioned in the

rental property purchase agreement. In such case 50% deduction can be claimed on such gain

after adjusting/deducting any capital losses of previous and current financial year.

Loss on sale of property: If property sold at a price lower than cost base, there is a case

of capital loss. This loss along with loss of $40000, will be forwarded to coming financial year.

Both losses will cumulatively carried forward to next year.

CONCLUSION

From the above report, it can be concluded lottery winning are considered as an asset in

Australia but are free from capital gain taxes. This income does not become part of ordinary

income of a person. Further, is can be stated that taxable income of Corner Pharmacy calculated

on accrual basis and is tax free. The principle stated in IRC v Duke of Westminster [1936] AC 1

case was of tax avoidance and it can be articulated that in present time it has relevance in

Australia with application of rules and legislations.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Book and Journals

Buchanan, J., 2018. Money laundering through gambling devices. Society and Business

Review.13(2), pp.217-237.

Menk, K.B., Nagle, B. and Coss, D.L., 2017. The disconnect between tax laws, public opinion

and taxpayer compliance: a study of the taxation of gambling winnings. International

Journal of Critical Accounting. 9(3). pp.206-227.

Evans, C., Minas, J. and Lim, Y., 2015. Taxing personal capital gains in Australia: an alternative

way forward. Austl. Tax F. 30. p.735.

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax record

data: A cautionary tale from Australia. The Journal of Economic Inequality. 13(2).

pp.181-205.

AbdulRazaq, M.T. and Adam, K.I., 2015. Anti-Avoidance Legislations: Issues & Doubts in the

Application of Tax Rules in Nigeria. AGORA Int'l J. Jurid. Sci., p.1.

Johnston, S., 2017. Multilateral Tax Convention to Prevent Base Erosion and Profit

Shifting. Auckland UL Rev. 23. p.384.

Online

Tax planning vs tax avoidance. 2018. [Online]. Available through

:<https://www.ato.gov.au/General/Tax-planning/Tax-planning-vs-tax-avoidance/>.

Australian Tax Avoidance. 2018. [Online]. Available through

:<http://www.fedcourt.gov.au/digital-law-library/judges-speeches/speeches-former-

judges/justice-pagone/201706>.

2

Book and Journals

Buchanan, J., 2018. Money laundering through gambling devices. Society and Business

Review.13(2), pp.217-237.

Menk, K.B., Nagle, B. and Coss, D.L., 2017. The disconnect between tax laws, public opinion

and taxpayer compliance: a study of the taxation of gambling winnings. International

Journal of Critical Accounting. 9(3). pp.206-227.

Evans, C., Minas, J. and Lim, Y., 2015. Taxing personal capital gains in Australia: an alternative

way forward. Austl. Tax F. 30. p.735.

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax record

data: A cautionary tale from Australia. The Journal of Economic Inequality. 13(2).

pp.181-205.

AbdulRazaq, M.T. and Adam, K.I., 2015. Anti-Avoidance Legislations: Issues & Doubts in the

Application of Tax Rules in Nigeria. AGORA Int'l J. Jurid. Sci., p.1.

Johnston, S., 2017. Multilateral Tax Convention to Prevent Base Erosion and Profit

Shifting. Auckland UL Rev. 23. p.384.

Online

Tax planning vs tax avoidance. 2018. [Online]. Available through

:<https://www.ato.gov.au/General/Tax-planning/Tax-planning-vs-tax-avoidance/>.

Australian Tax Avoidance. 2018. [Online]. Available through

:<http://www.fedcourt.gov.au/digital-law-library/judges-speeches/speeches-former-

judges/justice-pagone/201706>.

2

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.