Taxation Report: Analyzing Mr. Desai's Trading and VAT Obligations

VerifiedAdded on 2023/06/03

|12

|2453

|233

Report

AI Summary

This report addresses the taxation issues of Mr. Desai, a client of a Chartered Accountant firm, analyzing his antique trading activities and VAT obligations. The report defines 'badges of trade' to determine if Mr. Desai's vocation constitutes trading and discusses the differences between tax avoidance and tax evasion. It details allowable and disallowable business expenses, including loan expenses, capital expenses, fines, and depreciation. The report also covers VAT registration, including when it is required and the deadlines. It further explains the VAT return process, payment schedules, and the ineligibility for the flat-rate scheme, and the possibility of claiming bad debt relief. The report provides a calculation of Mr. Desai's adjusted trading profit for the year ending December 31, 2017.

Taxation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Introduction......................................................................................................................................3

Question 1........................................................................................................................................3

Question 2........................................................................................................................................4

Question 3........................................................................................................................................5

Part A...........................................................................................................................................5

Part B...........................................................................................................................................6

Part C...........................................................................................................................................7

Question 4........................................................................................................................................8

Part A...........................................................................................................................................8

Part B...........................................................................................................................................8

Part C...........................................................................................................................................9

Part D...........................................................................................................................................9

References......................................................................................................................................11

Introduction......................................................................................................................................3

Question 1........................................................................................................................................3

Question 2........................................................................................................................................4

Question 3........................................................................................................................................5

Part A...........................................................................................................................................5

Part B...........................................................................................................................................6

Part C...........................................................................................................................................7

Question 4........................................................................................................................................8

Part A...........................................................................................................................................8

Part B...........................................................................................................................................8

Part C...........................................................................................................................................9

Part D...........................................................................................................................................9

References......................................................................................................................................11

INTRODUCTION

Tax is a levy on the profit derived by the trading and the professional activity (Hoynes, Miller,

and Simon, 2015). The income tax Act describes the activity which is regarded as trading, and it

is known as “Badges of Trade”. The present study is about the evaluation of the badges of trade

along with the taxability of the business profits by considering relevant tax provisions. In this

study description regarding the allowed and disallowed expenses from the profit of the business

is also stated. Further the registration requirement under the vat, return, and payment of vat

liability and the eligibility of the flat rate scheme for the businesses has been discussed.

QUESTION 1

The income tax is a levy on the profit which is earned by the person from a business activity or

by profession or vocation (Saad, 2014). In the income tax of the United Kingdom, for

determining whether the transaction is considered as trading or not, “Badges of Trade” test is

defined which are as follows-

When a person enters into a transaction with the objective to earn the profit from the

transaction, then it is regarded as a trade according to the income tax rules.

If the person regularly deals with the same activity, then the same is regarded as a

trade. In the case of “Pickford v Quirke”, the taxpayer buys the mill for the trading

purpose, but due to the worse condition, the taxpayer sale all the items with the

objective to earn profits. The taxpayer regularly sale the items of the mill (Elsevier

UK Ltd, 2010). Therefore this transaction is considered as profit from trading.

Tax is a levy on the profit derived by the trading and the professional activity (Hoynes, Miller,

and Simon, 2015). The income tax Act describes the activity which is regarded as trading, and it

is known as “Badges of Trade”. The present study is about the evaluation of the badges of trade

along with the taxability of the business profits by considering relevant tax provisions. In this

study description regarding the allowed and disallowed expenses from the profit of the business

is also stated. Further the registration requirement under the vat, return, and payment of vat

liability and the eligibility of the flat rate scheme for the businesses has been discussed.

QUESTION 1

The income tax is a levy on the profit which is earned by the person from a business activity or

by profession or vocation (Saad, 2014). In the income tax of the United Kingdom, for

determining whether the transaction is considered as trading or not, “Badges of Trade” test is

defined which are as follows-

When a person enters into a transaction with the objective to earn the profit from the

transaction, then it is regarded as a trade according to the income tax rules.

If the person regularly deals with the same activity, then the same is regarded as a

trade. In the case of “Pickford v Quirke”, the taxpayer buys the mill for the trading

purpose, but due to the worse condition, the taxpayer sale all the items with the

objective to earn profits. The taxpayer regularly sale the items of the mill (Elsevier

UK Ltd, 2010). Therefore this transaction is considered as profit from trading.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

If the person, after purchasing any asset, modifies it with the objective for enhancing

the sale. Then it is a trading activity.

Nature of transaction is such that, even the single transaction also be regarded as

trading. In other words, the person is not required to carry out day to day activity of

the sale and purchase, but the single transaction of the sale and purchase also leads to

the trading activity (Elsevier UK Ltd, 2010).

If there is a direct link between the existing business and selling of any item by the

person, then it constitutes the profit from trading activity.

Financing arrangement such as obtains the loan for purchasing the asset and only

when the asset is sold, and then the loan is repaid. It is also regarded as trading

activity. In the case of “Wisdom v Chamberlain” the taxpayer obtained the loan for

buying the mould of silver bullion. Due to the non-repayment of interest from the

money, the taxpayer sold the mould. The profit is regarded as a trading profit.

In the present study, Desai enters into a buying and selling activity of the antiques and restoring

on a regular basis and making the profit (Elsevier UK Ltd, 2010). After considering all the above

aspect, Mr Desai vocation is termed as trading.

QUESTION 2

Part A

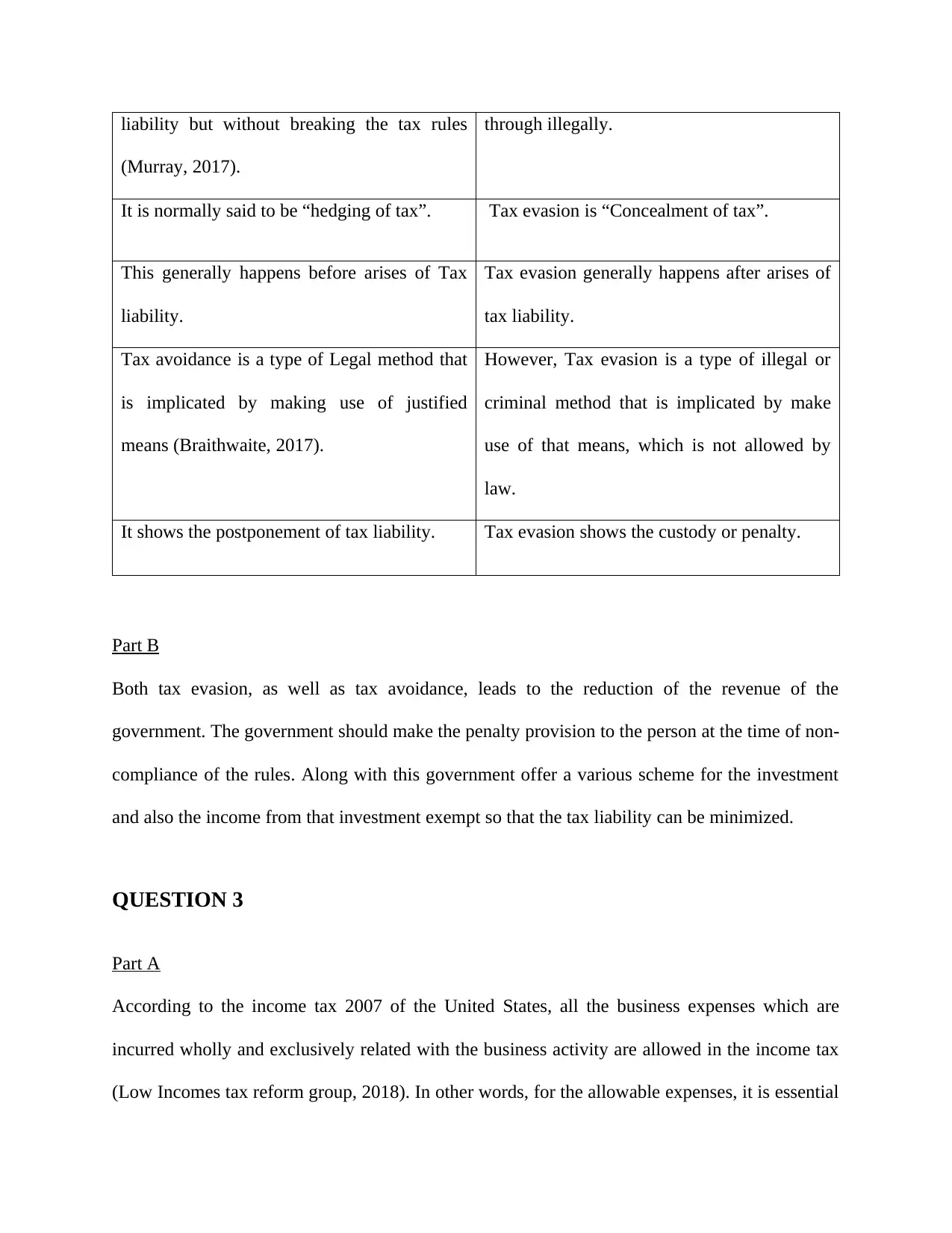

Difference between Tax Avoidance and Tax Evasion

Tax Avoidance Tax Evasion

Tax Avoidance refers to Reducing tax Tax Evasion refers to Reducing tax liability

the sale. Then it is a trading activity.

Nature of transaction is such that, even the single transaction also be regarded as

trading. In other words, the person is not required to carry out day to day activity of

the sale and purchase, but the single transaction of the sale and purchase also leads to

the trading activity (Elsevier UK Ltd, 2010).

If there is a direct link between the existing business and selling of any item by the

person, then it constitutes the profit from trading activity.

Financing arrangement such as obtains the loan for purchasing the asset and only

when the asset is sold, and then the loan is repaid. It is also regarded as trading

activity. In the case of “Wisdom v Chamberlain” the taxpayer obtained the loan for

buying the mould of silver bullion. Due to the non-repayment of interest from the

money, the taxpayer sold the mould. The profit is regarded as a trading profit.

In the present study, Desai enters into a buying and selling activity of the antiques and restoring

on a regular basis and making the profit (Elsevier UK Ltd, 2010). After considering all the above

aspect, Mr Desai vocation is termed as trading.

QUESTION 2

Part A

Difference between Tax Avoidance and Tax Evasion

Tax Avoidance Tax Evasion

Tax Avoidance refers to Reducing tax Tax Evasion refers to Reducing tax liability

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

liability but without breaking the tax rules

(Murray, 2017).

through illegally.

It is normally said to be “hedging of tax”. Tax evasion is “Concealment of tax”.

This generally happens before arises of Tax

liability.

Tax evasion generally happens after arises of

tax liability.

Tax avoidance is a type of Legal method that

is implicated by making use of justified

means (Braithwaite, 2017).

However, Tax evasion is a type of illegal or

criminal method that is implicated by make

use of that means, which is not allowed by

law.

It shows the postponement of tax liability. Tax evasion shows the custody or penalty.

Part B

Both tax evasion, as well as tax avoidance, leads to the reduction of the revenue of the

government. The government should make the penalty provision to the person at the time of non-

compliance of the rules. Along with this government offer a various scheme for the investment

and also the income from that investment exempt so that the tax liability can be minimized.

QUESTION 3

Part A

According to the income tax 2007 of the United States, all the business expenses which are

incurred wholly and exclusively related with the business activity are allowed in the income tax

(Low Incomes tax reform group, 2018). In other words, for the allowable expenses, it is essential

(Murray, 2017).

through illegally.

It is normally said to be “hedging of tax”. Tax evasion is “Concealment of tax”.

This generally happens before arises of Tax

liability.

Tax evasion generally happens after arises of

tax liability.

Tax avoidance is a type of Legal method that

is implicated by making use of justified

means (Braithwaite, 2017).

However, Tax evasion is a type of illegal or

criminal method that is implicated by make

use of that means, which is not allowed by

law.

It shows the postponement of tax liability. Tax evasion shows the custody or penalty.

Part B

Both tax evasion, as well as tax avoidance, leads to the reduction of the revenue of the

government. The government should make the penalty provision to the person at the time of non-

compliance of the rules. Along with this government offer a various scheme for the investment

and also the income from that investment exempt so that the tax liability can be minimized.

QUESTION 3

Part A

According to the income tax 2007 of the United States, all the business expenses which are

incurred wholly and exclusively related with the business activity are allowed in the income tax

(Low Incomes tax reform group, 2018). In other words, for the allowable expenses, it is essential

that the cost must be incurred for running the business activity (DeBacker, Heim, and Tran,

2015). Further, the capital expenses are not allowed, which is generally incurred for buying the

assets with a significant amount. Moreover, the income tax also disallowed some revenue nature

expenses such as personal expenses, which cannot be claimed by the person from the assessable

income (Cooper, & et al. 2016).

Part B

Expenses of £ 1500 are incurred for acquiring the loan is the allowed expenses. It is

because the loan is acquired for business purpose and amount incurred is the revenue

expense. Since allowed business expenses should be deducted from the profit and in the

income and expenditure account, this expense is already deducted. Therefore no further

treatment is required.

£ 4200, was spent on installing the new window in the factory, this expense is regarded as

the capital expense. Therefore it cannot be deducted from the profit. Since this expense is

already deducted from the profit; therefore it should be added again.

£ 250, related with the fine is not allowed in the income tax.

Depreciation amount £ 3500 is included in the income and expenditure account. Since

depreciation is considered as a capital allowance in the income tax and it can be deducted

from the trading income. Therefore, no more treatment is required.

Legal fees of £ 286, is related to the business activity. Therefore, it is allowed as a

business expense and can be deducted from business profits. Therefore no more treatment

is required.

2015). Further, the capital expenses are not allowed, which is generally incurred for buying the

assets with a significant amount. Moreover, the income tax also disallowed some revenue nature

expenses such as personal expenses, which cannot be claimed by the person from the assessable

income (Cooper, & et al. 2016).

Part B

Expenses of £ 1500 are incurred for acquiring the loan is the allowed expenses. It is

because the loan is acquired for business purpose and amount incurred is the revenue

expense. Since allowed business expenses should be deducted from the profit and in the

income and expenditure account, this expense is already deducted. Therefore no further

treatment is required.

£ 4200, was spent on installing the new window in the factory, this expense is regarded as

the capital expense. Therefore it cannot be deducted from the profit. Since this expense is

already deducted from the profit; therefore it should be added again.

£ 250, related with the fine is not allowed in the income tax.

Depreciation amount £ 3500 is included in the income and expenditure account. Since

depreciation is considered as a capital allowance in the income tax and it can be deducted

from the trading income. Therefore, no more treatment is required.

Legal fees of £ 286, is related to the business activity. Therefore, it is allowed as a

business expense and can be deducted from business profits. Therefore no more treatment

is required.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

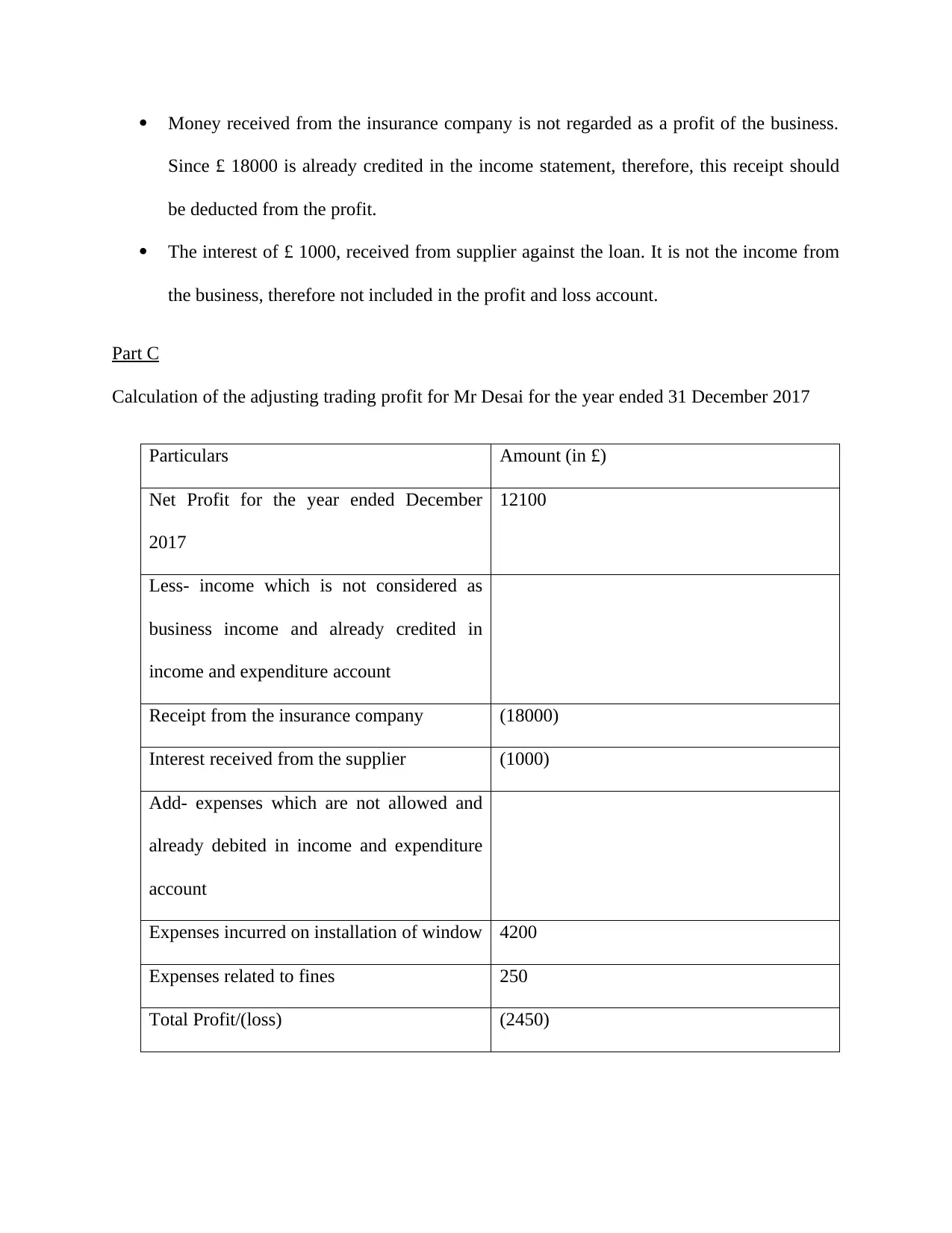

Money received from the insurance company is not regarded as a profit of the business.

Since £ 18000 is already credited in the income statement, therefore, this receipt should

be deducted from the profit.

The interest of £ 1000, received from supplier against the loan. It is not the income from

the business, therefore not included in the profit and loss account.

Part C

Calculation of the adjusting trading profit for Mr Desai for the year ended 31 December 2017

Particulars Amount (in £)

Net Profit for the year ended December

2017

12100

Less- income which is not considered as

business income and already credited in

income and expenditure account

Receipt from the insurance company (18000)

Interest received from the supplier (1000)

Add- expenses which are not allowed and

already debited in income and expenditure

account

Expenses incurred on installation of window 4200

Expenses related to fines 250

Total Profit/(loss) (2450)

Since £ 18000 is already credited in the income statement, therefore, this receipt should

be deducted from the profit.

The interest of £ 1000, received from supplier against the loan. It is not the income from

the business, therefore not included in the profit and loss account.

Part C

Calculation of the adjusting trading profit for Mr Desai for the year ended 31 December 2017

Particulars Amount (in £)

Net Profit for the year ended December

2017

12100

Less- income which is not considered as

business income and already credited in

income and expenditure account

Receipt from the insurance company (18000)

Interest received from the supplier (1000)

Add- expenses which are not allowed and

already debited in income and expenditure

account

Expenses incurred on installation of window 4200

Expenses related to fines 250

Total Profit/(loss) (2450)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 4

Part A

The registration under the VAT is required if the taxable turnover of the business get exceeded

from the prescribed limit under the act. In the United Kingdom, the person must get registered

the business under the VAT if in a twelve month of the period the taxable turnover of the

business gets exceeded from £85000 or if the person expected that the within a period of thirty

days, the taxable turnover will get exceeded from the prescribed limit, then it is compulsory to

take the registration under the VAT (UK VAT returns, 2018).

The time limit to get the registration is within the thirty days from the date when the turnover

crossed the prescribed limit.

In the present study, it is assumed that the turnover of Mr Desai is fully taxable. Since the Desai

on 1st November won the contract, by which the turnover of the business gets exceeded from the

£85000. Therefore it is compulsory for Desai to get the registration under the vat within a period

of thirty days from the date on which turnover crossed the prescribed limit.

Part B

Generally, in the United Kingdom, all the VAT returns filed on a quarterly basis. However, the

quarter does not mean to comply with the calendar quarter. At the time of registration of the

VAT, a business can choose their quarterly period. If the annual VAT liability of the business is

greater than £ 2.3 Million, then it is compulsory to make the payment on the last day of the

second or third month of each quarter. In any other case, the return for the VAT liability is due

on the 7th day of the next month in which the quarter in the end. The person is making the

payment of VAT liability electronically and submits the return through the electronically.

Part A

The registration under the VAT is required if the taxable turnover of the business get exceeded

from the prescribed limit under the act. In the United Kingdom, the person must get registered

the business under the VAT if in a twelve month of the period the taxable turnover of the

business gets exceeded from £85000 or if the person expected that the within a period of thirty

days, the taxable turnover will get exceeded from the prescribed limit, then it is compulsory to

take the registration under the VAT (UK VAT returns, 2018).

The time limit to get the registration is within the thirty days from the date when the turnover

crossed the prescribed limit.

In the present study, it is assumed that the turnover of Mr Desai is fully taxable. Since the Desai

on 1st November won the contract, by which the turnover of the business gets exceeded from the

£85000. Therefore it is compulsory for Desai to get the registration under the vat within a period

of thirty days from the date on which turnover crossed the prescribed limit.

Part B

Generally, in the United Kingdom, all the VAT returns filed on a quarterly basis. However, the

quarter does not mean to comply with the calendar quarter. At the time of registration of the

VAT, a business can choose their quarterly period. If the annual VAT liability of the business is

greater than £ 2.3 Million, then it is compulsory to make the payment on the last day of the

second or third month of each quarter. In any other case, the return for the VAT liability is due

on the 7th day of the next month in which the quarter in the end. The person is making the

payment of VAT liability electronically and submits the return through the electronically.

In this case, Mr Desai has to submit VAT liability electronically and up to the 7th day of the next

month of the quarter end.

Part C

Under the flat rate scheme, the person can charge the VAT from the customer in a normal

manner but make the payment of the liability on the turnover to the government at the fixed rate.

For obtaining the benefit of the flat rate scheme the turnover the business must be less than or

equal to £150000 (UK VAT returns, 2018).

In the flat rate scheme, the person has to make the payment of the fixed rate of the VAT; there

are different rates is described as per the type of business. Further, the person has to maintain the

different accounts related with what the amount is charged from the customer and what is the

amount payable to the government. Along with this, the person who availss the flat rate scheme

cannot claim the vat paid on the purchase.

In the present study, the turnover of Mr Desai is exceeded from the £150000. Therefore Desai

cannot avail the benefit of the flat rate scheme.

Part D

Generally, VAT liability is paid by the businessman at the time when the transaction incurred not

when the payment is received from the customers. Sometimes, this may lead to the difficulty in

the businessman (UK VAT returns, 2018). Since if the businessman paid the tax to the

government at the time of incurrence of the transaction, however, later customer makes the

default in the payment to the businessman and then they are unable to realize the payment from

the customer in such case businessman can claim the bad debt relief. For claiming the bad debt

month of the quarter end.

Part C

Under the flat rate scheme, the person can charge the VAT from the customer in a normal

manner but make the payment of the liability on the turnover to the government at the fixed rate.

For obtaining the benefit of the flat rate scheme the turnover the business must be less than or

equal to £150000 (UK VAT returns, 2018).

In the flat rate scheme, the person has to make the payment of the fixed rate of the VAT; there

are different rates is described as per the type of business. Further, the person has to maintain the

different accounts related with what the amount is charged from the customer and what is the

amount payable to the government. Along with this, the person who availss the flat rate scheme

cannot claim the vat paid on the purchase.

In the present study, the turnover of Mr Desai is exceeded from the £150000. Therefore Desai

cannot avail the benefit of the flat rate scheme.

Part D

Generally, VAT liability is paid by the businessman at the time when the transaction incurred not

when the payment is received from the customers. Sometimes, this may lead to the difficulty in

the businessman (UK VAT returns, 2018). Since if the businessman paid the tax to the

government at the time of incurrence of the transaction, however, later customer makes the

default in the payment to the businessman and then they are unable to realize the payment from

the customer in such case businessman can claim the bad debt relief. For claiming the bad debt

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

relief, the overdue should be more than six months from the date of invoice. Along with this, it is

compulsory to write-off in a particular bad debt account.

In the present study, the customer of Mr Desai makes the default in the payment. Therefore if the

overdue amount is more than the six months from the invoice, then Mr Desai can claim the bad

debt relief and must be a write-off in a particular bad debt account.

compulsory to write-off in a particular bad debt account.

In the present study, the customer of Mr Desai makes the default in the payment. Therefore if the

overdue amount is more than the six months from the invoice, then Mr Desai can claim the bad

debt relief and must be a write-off in a particular bad debt account.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Braithwaite, V., 2017. Taxing democracy: Understanding tax avoidance and evasion. Routledge.

Cooper, M., McClelland, J., Pearce, J., Prisinzano, R., Sullivan, J., Yagan, D., Zidar, O. and

Zwick, E., 2016. Business: Who Owns It, and How Much Tax Do They Pay?. Tax Policy and

the Economy, 30(1), pp.91-128.

DeBacker, J., Heim, B.T. and Tran, A., 2015. Importing corruption culture from overseas:

Evidence from corporate tax evasion in the United States. Journal of Financial

Economics, 117(1), pp.122-138.

Dharmapala, D., 2017. The Economics of Tax Avoidance and Evasion. Edward Elgar Publishing.

Elsevier UK Ltd, 2010. TRADING INCOME AND BADGES OF TRADE. [Pdf]. Available

through < http://www1.lexisnexis.co.uk/taxtutor/public/business/2a_business_tax/2a10-

01(F).pdf>. [Accessed on 6th November 2018].

Hoynes, H., Miller, D. and Simon, D., 2015. Income, the earned income tax credit, and infant

health. American Economic Journal: Economic Policy, 7(1), pp.172-211.

Low Incomes tax reform group, 2018. What business expenses are allowable?. [Online].

Available through < https://www.litrg.org.uk/tax-guides/self-employment/working-out-profits-

losses-and-capital-allowance/what-business-expenses#diff>. [Accessed on 6th November 2018].

Murray, J., 2017. What Is the Difference Between Tax Avoidance and Tax Evasion?. [Online].

Available through <The Balance, www. the balance. com/tax-avoidance-vs-evasion-397671>.

[Accessed on 6th November 2018].

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’ view. Procedia-

Social and Behavioral Sciences, 109, pp.1069-1075.

UK VAT returns, 2018. [Online]. Available through <

https://www.avalara.com/vatlive/en/country-guides/europe/uk/uk-vat-returns.html>. [Accessed

on 6th November 2018].

Braithwaite, V., 2017. Taxing democracy: Understanding tax avoidance and evasion. Routledge.

Cooper, M., McClelland, J., Pearce, J., Prisinzano, R., Sullivan, J., Yagan, D., Zidar, O. and

Zwick, E., 2016. Business: Who Owns It, and How Much Tax Do They Pay?. Tax Policy and

the Economy, 30(1), pp.91-128.

DeBacker, J., Heim, B.T. and Tran, A., 2015. Importing corruption culture from overseas:

Evidence from corporate tax evasion in the United States. Journal of Financial

Economics, 117(1), pp.122-138.

Dharmapala, D., 2017. The Economics of Tax Avoidance and Evasion. Edward Elgar Publishing.

Elsevier UK Ltd, 2010. TRADING INCOME AND BADGES OF TRADE. [Pdf]. Available

through < http://www1.lexisnexis.co.uk/taxtutor/public/business/2a_business_tax/2a10-

01(F).pdf>. [Accessed on 6th November 2018].

Hoynes, H., Miller, D. and Simon, D., 2015. Income, the earned income tax credit, and infant

health. American Economic Journal: Economic Policy, 7(1), pp.172-211.

Low Incomes tax reform group, 2018. What business expenses are allowable?. [Online].

Available through < https://www.litrg.org.uk/tax-guides/self-employment/working-out-profits-

losses-and-capital-allowance/what-business-expenses#diff>. [Accessed on 6th November 2018].

Murray, J., 2017. What Is the Difference Between Tax Avoidance and Tax Evasion?. [Online].

Available through <The Balance, www. the balance. com/tax-avoidance-vs-evasion-397671>.

[Accessed on 6th November 2018].

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’ view. Procedia-

Social and Behavioral Sciences, 109, pp.1069-1075.

UK VAT returns, 2018. [Online]. Available through <

https://www.avalara.com/vatlive/en/country-guides/europe/uk/uk-vat-returns.html>. [Accessed

on 6th November 2018].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.