Taxation Law: Application of Residency Tests and Income Assessment

VerifiedAdded on 2023/06/04

|13

|3198

|491

Homework Assignment

AI Summary

This assignment delves into various aspects of Australian taxation law, focusing on residency rules and income assessment. It analyzes scenarios involving individuals like Fred and Jenny to determine their residency status based on factors such as length of stay, intention, and connections to Australia. The assignment also examines different types of income, including salary, compensation, gifts, and proceeds from sales, to determine whether they are considered assessable income under the Income Tax Assessment Act (ITAA) 1997 and ITAA 1936. Furthermore, it covers allowable deductions for expenses such as electricity bills, home office expenses, and self-education costs, referencing relevant case laws to support the analysis. The computation of taxable income and net tax payable for an individual, Mick Viduka, is also demonstrated. The assignment concludes by discussing various scenarios related to deductions.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................2

Answer to question 3:.................................................................................................................3

Answer to question 4:.................................................................................................................5

Answer to question 5:.................................................................................................................6

Answer to question 6:.................................................................................................................7

Answer to question 7:.................................................................................................................8

Answer to question 8:...............................................................................................................10

References:...............................................................................................................................12

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................2

Answer to question 3:.................................................................................................................3

Answer to question 4:.................................................................................................................5

Answer to question 5:.................................................................................................................6

Answer to question 6:.................................................................................................................7

Answer to question 7:.................................................................................................................8

Answer to question 8:...............................................................................................................10

References:...............................................................................................................................12

2TAXATION LAW

Answer to question 1:

The Australian resident is referred as the person who is the resident of Australia for

the taxation purpose under “section 995-1 of the ITAA 1936”. The court in “Reid v The

Commissioners of Inland Revenue (1926)” considered the meaning of the word “reside”

(Kenny 2014). The commissioner expressed that the presence and time are to be taken into

account while determining whether the person reside in the place where they spend a portion

of their life.

Majority of the individuals work in numerous nations during their careers. They

regularly maintain a house in their domicile nation. Nevertheless, for the phase of assignment

in Australia, these individuals live and work in Australia (Jover-Ledesma 2014). Their family

often accompany them and they become involved in the social activity in Australia.

As understood Fred a British Executive came Australia to set up a branch for his

company. Even though his time of stay was not certain he leased his Melbourne residence for

12 months. He even rented out the family home and derived interest from France, however

due to ill health Fred returned to UK after 11 months from arriving in Australia.

Referring to “section 995-1 of the ITAA 1936” Fred, is an Australian resident

because all the factors reflect Fred is resident in Australia. While ascertaining tax liability in

Australia Jim must refer to the necessary provision of double taxation convention where he

will discover that his interest from France would not be held assessable in Australia due to

the duel resident tie-breaker tests in the convention operating to entirely treat Fred resident in

UK within the meaning of the convention.

Answer to question 2:

According to the “taxation ruling of TR 98/17” the period of physical presence in

Australia demonstrate that the behaviour of the individual possess the necessary continuity,

Answer to question 1:

The Australian resident is referred as the person who is the resident of Australia for

the taxation purpose under “section 995-1 of the ITAA 1936”. The court in “Reid v The

Commissioners of Inland Revenue (1926)” considered the meaning of the word “reside”

(Kenny 2014). The commissioner expressed that the presence and time are to be taken into

account while determining whether the person reside in the place where they spend a portion

of their life.

Majority of the individuals work in numerous nations during their careers. They

regularly maintain a house in their domicile nation. Nevertheless, for the phase of assignment

in Australia, these individuals live and work in Australia (Jover-Ledesma 2014). Their family

often accompany them and they become involved in the social activity in Australia.

As understood Fred a British Executive came Australia to set up a branch for his

company. Even though his time of stay was not certain he leased his Melbourne residence for

12 months. He even rented out the family home and derived interest from France, however

due to ill health Fred returned to UK after 11 months from arriving in Australia.

Referring to “section 995-1 of the ITAA 1936” Fred, is an Australian resident

because all the factors reflect Fred is resident in Australia. While ascertaining tax liability in

Australia Jim must refer to the necessary provision of double taxation convention where he

will discover that his interest from France would not be held assessable in Australia due to

the duel resident tie-breaker tests in the convention operating to entirely treat Fred resident in

UK within the meaning of the convention.

Answer to question 2:

According to the “taxation ruling of TR 98/17” the period of physical presence in

Australia demonstrate that the behaviour of the individual possess the necessary continuity,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

routine or habit as the question of fact, depending upon the situation of each case (James

2016). On entering Australia, a person may reflect that they do not intend to live in Australia.

However, when there is a change in the behaviour reflecting an intention to live in Australia,

a person may be treated as the Australian resident from time when such behaviour begins that

is consistent with living here in Australia begins. The intention should be ascertained

objectively, with regard to all the necessary facts and situations.

As understood in the current situation of Jenny who is a working accountant in Hong

Kong enters Australia to spend only three months for travelling and staying three cities. On

being offered to take up the position in Australia for nine months Jenny accepted the offer

and leased a service executive apartment in Sydney.

As Jenny is on the working trip, the time and nature of her stay in Australia in

temporary accommodation during April 2017. Jenny’s stay during the income year does not

establishes a pattern of continuous behaviour and she should be treated as non-resident for the

year ended 30 June 2018.

Later, from the early July the behaviour of Jenny alters. The leasing of a permanent

accommodation along with Jenny’s position in Sydney establishes a more settled purpose for

being in Australia in comparison to her initial three months in Australia. Jenny should be

treated as resident from the time when there is a change in her behaviour and is an Australian

resident for the income year of 2018.

Answer to question 3:

A: Salary received by the employee would be treated as ordinary income under “section 6-5

of the ITAA 1997” because the salary received constitute an income an income from the

personal exertion under “section 6-1 of the ITAA 1936”.

routine or habit as the question of fact, depending upon the situation of each case (James

2016). On entering Australia, a person may reflect that they do not intend to live in Australia.

However, when there is a change in the behaviour reflecting an intention to live in Australia,

a person may be treated as the Australian resident from time when such behaviour begins that

is consistent with living here in Australia begins. The intention should be ascertained

objectively, with regard to all the necessary facts and situations.

As understood in the current situation of Jenny who is a working accountant in Hong

Kong enters Australia to spend only three months for travelling and staying three cities. On

being offered to take up the position in Australia for nine months Jenny accepted the offer

and leased a service executive apartment in Sydney.

As Jenny is on the working trip, the time and nature of her stay in Australia in

temporary accommodation during April 2017. Jenny’s stay during the income year does not

establishes a pattern of continuous behaviour and she should be treated as non-resident for the

year ended 30 June 2018.

Later, from the early July the behaviour of Jenny alters. The leasing of a permanent

accommodation along with Jenny’s position in Sydney establishes a more settled purpose for

being in Australia in comparison to her initial three months in Australia. Jenny should be

treated as resident from the time when there is a change in her behaviour and is an Australian

resident for the income year of 2018.

Answer to question 3:

A: Salary received by the employee would be treated as ordinary income under “section 6-5

of the ITAA 1997” because the salary received constitute an income an income from the

personal exertion under “section 6-1 of the ITAA 1936”.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

B: Compensation received by the injured worker for the loss of salary because he was not

able to work for four weeks would be included in the assessable income of the taxpayer under

“section 15-2 of the ITAA 1997” as the ordinary income (Grange, Jover-Ledesma and

Maydew 2015). This is because the compensation received is in respect of the employment to

the worker.

C: Christmas gift received by the daughter from her mother cannot be treated as ordinary

income. The court in “Scott v FCT (1966)” held that personal gifts are not treated as income.

D: Proceeds from the sale of copyright to a book will be treated as assessable ordinary

income under “section 6-5 of the ITAA 1997” because the payment is received by the

recipient for the transfer of all the rights associated to the copyright in the books.

E: Proceeds from selling the copyright of book where the recipient is carrying on the

business of writing books and selling the copyright would be included for assessment as

ordinary income under “section 8-1 of the ITAA 1997” (Douglas et al. 2014). The proceeds

of such sale constitute assessable income in the hands of the recipient in agreement with the

“subsection 25 (1)”.

F: Profit on sale of shares which were held for number of years would be included into the

assessable income of the taxpayer under the ordinary meaning of “section 8-1 of the ITAA

1997”.

G: Unemployment benefits that is received by the unemployed person from the government

would not be included into the assessable income within ordinary meaning of “section 6-5”.

H: Award receive by the freelance photographer for his photography would be treated as

ordinary income under “section 8-1 of the ITAA 1997” because the amount of $4,000 is

related to the taxpayer income generating activities.

B: Compensation received by the injured worker for the loss of salary because he was not

able to work for four weeks would be included in the assessable income of the taxpayer under

“section 15-2 of the ITAA 1997” as the ordinary income (Grange, Jover-Ledesma and

Maydew 2015). This is because the compensation received is in respect of the employment to

the worker.

C: Christmas gift received by the daughter from her mother cannot be treated as ordinary

income. The court in “Scott v FCT (1966)” held that personal gifts are not treated as income.

D: Proceeds from the sale of copyright to a book will be treated as assessable ordinary

income under “section 6-5 of the ITAA 1997” because the payment is received by the

recipient for the transfer of all the rights associated to the copyright in the books.

E: Proceeds from selling the copyright of book where the recipient is carrying on the

business of writing books and selling the copyright would be included for assessment as

ordinary income under “section 8-1 of the ITAA 1997” (Douglas et al. 2014). The proceeds

of such sale constitute assessable income in the hands of the recipient in agreement with the

“subsection 25 (1)”.

F: Profit on sale of shares which were held for number of years would be included into the

assessable income of the taxpayer under the ordinary meaning of “section 8-1 of the ITAA

1997”.

G: Unemployment benefits that is received by the unemployed person from the government

would not be included into the assessable income within ordinary meaning of “section 6-5”.

H: Award receive by the freelance photographer for his photography would be treated as

ordinary income under “section 8-1 of the ITAA 1997” because the amount of $4,000 is

related to the taxpayer income generating activities.

5TAXATION LAW

I: Payment received from the sales of pottery as the part of hobby would not be considered as

ordinary income since the amount derived is from the hobby and hence non-assessable.

J: The sum of $200 received for the best painting by the local art exhibition would be held as

ordinary income because the amount received holds sufficient relation with the income

producing activities of the taxpayer.

Answer to question 4:

A: The receipt of gross salary by Frida will be treated as the assessable income within the

ordinary meaning of “section 8-1 of the ITAA 1997”.

B: The unused annual leave for the year 2017/18 constitutes a non-assessable income under

“section 15-2 of the ITAA 1997” (Barkoczy 2018). The annual leave received by Fried

would not be included for taxation purpose.

C: The winnings from the Powerball syndicate by Fried would not be held as assessable

income because it is a mere windfall gain and does not has the character of income.

D: Receipt of cash prize by Frieda for employee would be included for assessment. Referring

to “Kelly v FCT” receipt of award that is incidental to work and employment is an assessable

income (Kenny, Blissenden and Villios 2018). The cash receipt of cash prize by Frieda is

incidental to her work and employment.

E: Receipt of holiday to Fraser Island would not be included in the assessable income. The

holiday received constitute a non-cash benefit having nexus with the personal services which

is non-convertible to cash and hence not an ordinary income.

F: Frieda received a wedding gift from her work colleague that valued $750. Citing “Scott v

FCT (1966)” personal gifts are not treated as income and not included for assessment

purpose. The wedding gift received by Frieda is a non-assessable income.

I: Payment received from the sales of pottery as the part of hobby would not be considered as

ordinary income since the amount derived is from the hobby and hence non-assessable.

J: The sum of $200 received for the best painting by the local art exhibition would be held as

ordinary income because the amount received holds sufficient relation with the income

producing activities of the taxpayer.

Answer to question 4:

A: The receipt of gross salary by Frida will be treated as the assessable income within the

ordinary meaning of “section 8-1 of the ITAA 1997”.

B: The unused annual leave for the year 2017/18 constitutes a non-assessable income under

“section 15-2 of the ITAA 1997” (Barkoczy 2018). The annual leave received by Fried

would not be included for taxation purpose.

C: The winnings from the Powerball syndicate by Fried would not be held as assessable

income because it is a mere windfall gain and does not has the character of income.

D: Receipt of cash prize by Frieda for employee would be included for assessment. Referring

to “Kelly v FCT” receipt of award that is incidental to work and employment is an assessable

income (Kenny, Blissenden and Villios 2018). The cash receipt of cash prize by Frieda is

incidental to her work and employment.

E: Receipt of holiday to Fraser Island would not be included in the assessable income. The

holiday received constitute a non-cash benefit having nexus with the personal services which

is non-convertible to cash and hence not an ordinary income.

F: Frieda received a wedding gift from her work colleague that valued $750. Citing “Scott v

FCT (1966)” personal gifts are not treated as income and not included for assessment

purpose. The wedding gift received by Frieda is a non-assessable income.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

G: Frieda received a reimbursement of the self-education costs that is incurred for the

logistics course. The amount received by her employer would be treated as assessable income

for assessment purpose.

H: The rental income received from the rental apartment by Samantha Storey would be

treated as assessable income within the ordinary meaning of the “section 6-5 of the ITAA

1997” (Sadiq et al. 2018). The rental income constitutes periodic receipts for Samantha.

I: Samantha reported the receipt of $700 as the reimbursement by tenants for cleaning

carpets. The amount received by Samantha would be held taxable and would be included in

the assessable income.

J: Insurance pay-outs that is received for the items that is used by the taxpayer to generate

income should be included for assessment purpose. The receipt of insurance pay-out by

Samantha would be treated as assessable income for assessment purpose.

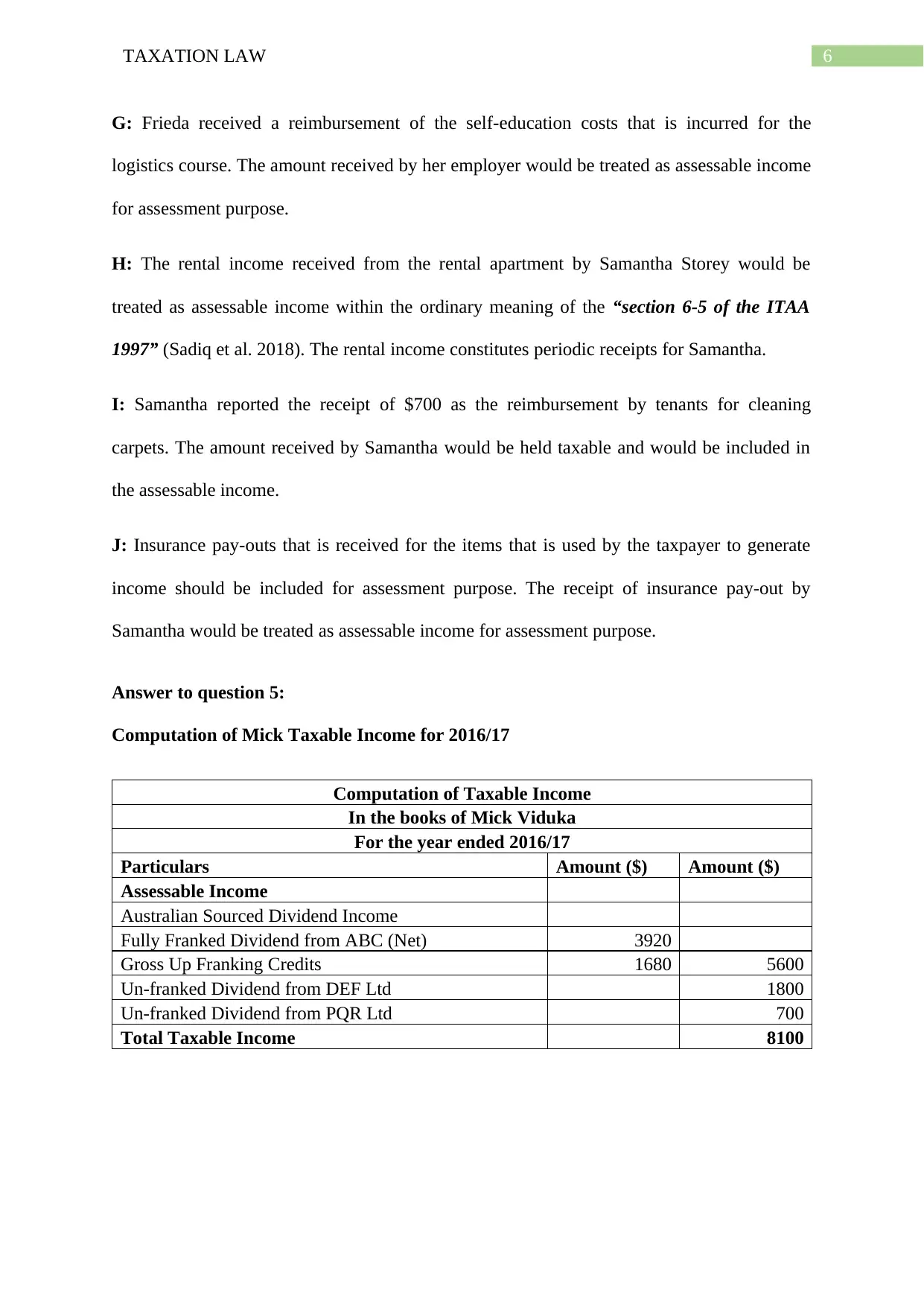

Answer to question 5:

Computation of Mick Taxable Income for 2016/17

Computation of Taxable Income

In the books of Mick Viduka

For the year ended 2016/17

Particulars Amount ($) Amount ($)

Assessable Income

Australian Sourced Dividend Income

Fully Franked Dividend from ABC (Net) 3920

Gross Up Franking Credits 1680 5600

Un-franked Dividend from DEF Ltd 1800

Un-franked Dividend from PQR Ltd 700

Total Taxable Income 8100

G: Frieda received a reimbursement of the self-education costs that is incurred for the

logistics course. The amount received by her employer would be treated as assessable income

for assessment purpose.

H: The rental income received from the rental apartment by Samantha Storey would be

treated as assessable income within the ordinary meaning of the “section 6-5 of the ITAA

1997” (Sadiq et al. 2018). The rental income constitutes periodic receipts for Samantha.

I: Samantha reported the receipt of $700 as the reimbursement by tenants for cleaning

carpets. The amount received by Samantha would be held taxable and would be included in

the assessable income.

J: Insurance pay-outs that is received for the items that is used by the taxpayer to generate

income should be included for assessment purpose. The receipt of insurance pay-out by

Samantha would be treated as assessable income for assessment purpose.

Answer to question 5:

Computation of Mick Taxable Income for 2016/17

Computation of Taxable Income

In the books of Mick Viduka

For the year ended 2016/17

Particulars Amount ($) Amount ($)

Assessable Income

Australian Sourced Dividend Income

Fully Franked Dividend from ABC (Net) 3920

Gross Up Franking Credits 1680 5600

Un-franked Dividend from DEF Ltd 1800

Un-franked Dividend from PQR Ltd 700

Total Taxable Income 8100

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

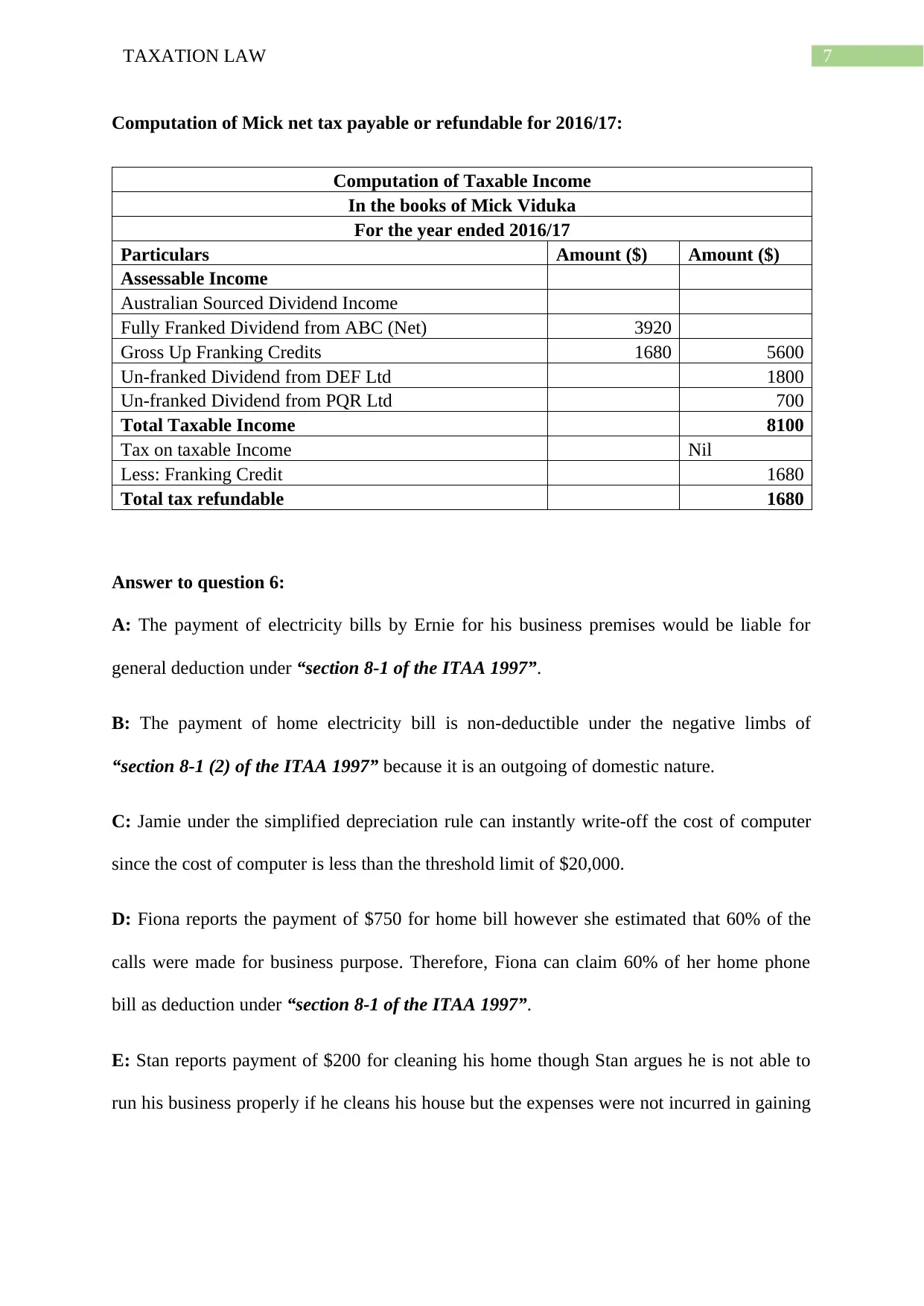

Computation of Mick net tax payable or refundable for 2016/17:

Computation of Taxable Income

In the books of Mick Viduka

For the year ended 2016/17

Particulars Amount ($) Amount ($)

Assessable Income

Australian Sourced Dividend Income

Fully Franked Dividend from ABC (Net) 3920

Gross Up Franking Credits 1680 5600

Un-franked Dividend from DEF Ltd 1800

Un-franked Dividend from PQR Ltd 700

Total Taxable Income 8100

Tax on taxable Income Nil

Less: Franking Credit 1680

Total tax refundable 1680

Answer to question 6:

A: The payment of electricity bills by Ernie for his business premises would be liable for

general deduction under “section 8-1 of the ITAA 1997”.

B: The payment of home electricity bill is non-deductible under the negative limbs of

“section 8-1 (2) of the ITAA 1997” because it is an outgoing of domestic nature.

C: Jamie under the simplified depreciation rule can instantly write-off the cost of computer

since the cost of computer is less than the threshold limit of $20,000.

D: Fiona reports the payment of $750 for home bill however she estimated that 60% of the

calls were made for business purpose. Therefore, Fiona can claim 60% of her home phone

bill as deduction under “section 8-1 of the ITAA 1997”.

E: Stan reports payment of $200 for cleaning his home though Stan argues he is not able to

run his business properly if he cleans his house but the expenses were not incurred in gaining

Computation of Mick net tax payable or refundable for 2016/17:

Computation of Taxable Income

In the books of Mick Viduka

For the year ended 2016/17

Particulars Amount ($) Amount ($)

Assessable Income

Australian Sourced Dividend Income

Fully Franked Dividend from ABC (Net) 3920

Gross Up Franking Credits 1680 5600

Un-franked Dividend from DEF Ltd 1800

Un-franked Dividend from PQR Ltd 700

Total Taxable Income 8100

Tax on taxable Income Nil

Less: Franking Credit 1680

Total tax refundable 1680

Answer to question 6:

A: The payment of electricity bills by Ernie for his business premises would be liable for

general deduction under “section 8-1 of the ITAA 1997”.

B: The payment of home electricity bill is non-deductible under the negative limbs of

“section 8-1 (2) of the ITAA 1997” because it is an outgoing of domestic nature.

C: Jamie under the simplified depreciation rule can instantly write-off the cost of computer

since the cost of computer is less than the threshold limit of $20,000.

D: Fiona reports the payment of $750 for home bill however she estimated that 60% of the

calls were made for business purpose. Therefore, Fiona can claim 60% of her home phone

bill as deduction under “section 8-1 of the ITAA 1997”.

E: Stan reports payment of $200 for cleaning his home though Stan argues he is not able to

run his business properly if he cleans his house but the expenses were not incurred in gaining

8TAXATION LAW

assessable income. Therefore, under “section 8-1 of the ITAA 1997” Stan would not be

allowed to claim deduction.

F: Rita pays a sum of $12,000 as child care fees to enable her to carry her full time job.

Referring “Lodge v FCT (1972)” the child care fees will not be allowed for deduction since it

is not incurred in the derivation of assessable income (Morgan, Mortimer and Pinto 2017).

G: Tara incurs a traveling expenses by train to travel from her home to work. Referring to

“Lunney v FCT (1958)” travel between home and the place of work by Tara is not allowed

for deductions.

H: Nicole reports a payment of $6,000 to her payments. The expenses will not be considered

as allowable deduction under “section 8-1 of the ITAA 1997” since it is a private or personal

expense.

I: Citing the case of “FCT v Finn”, Stu employed as the legal assistant would be allowed to

claim deduction for self-education expenses under “section 8-1” because the expenses

incurred were to maintain or increase his occupation skills (McCouat 2018).

J: Ron will not be allowed to claim deduction for the self-education expense under “section

8-1” because the expenses incurred not related to his occupation or skills.

Answer to question 7:

A: Referring to “Swinford v FCT” Stefan will be allowed to claim deduction for rent under

“section 8-1” as the home office expenses up to 20% of floor area that has the character of

“place of business” because the expenses were incurred in derivation of assessable income

(Taylor et al. 2018).

assessable income. Therefore, under “section 8-1 of the ITAA 1997” Stan would not be

allowed to claim deduction.

F: Rita pays a sum of $12,000 as child care fees to enable her to carry her full time job.

Referring “Lodge v FCT (1972)” the child care fees will not be allowed for deduction since it

is not incurred in the derivation of assessable income (Morgan, Mortimer and Pinto 2017).

G: Tara incurs a traveling expenses by train to travel from her home to work. Referring to

“Lunney v FCT (1958)” travel between home and the place of work by Tara is not allowed

for deductions.

H: Nicole reports a payment of $6,000 to her payments. The expenses will not be considered

as allowable deduction under “section 8-1 of the ITAA 1997” since it is a private or personal

expense.

I: Citing the case of “FCT v Finn”, Stu employed as the legal assistant would be allowed to

claim deduction for self-education expenses under “section 8-1” because the expenses

incurred were to maintain or increase his occupation skills (McCouat 2018).

J: Ron will not be allowed to claim deduction for the self-education expense under “section

8-1” because the expenses incurred not related to his occupation or skills.

Answer to question 7:

A: Referring to “Swinford v FCT” Stefan will be allowed to claim deduction for rent under

“section 8-1” as the home office expenses up to 20% of floor area that has the character of

“place of business” because the expenses were incurred in derivation of assessable income

(Taylor et al. 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

B: Jo will be denied deduction under “section 8-1 of the ITAA 1997”. Referring to

“Handley v FCT” Jo being a barrister also maintained his own chamber or office in town and

hence no deduction will be allowed.

C: Annice will be denied for the expenses that were incurred from her home related to her

employment. Annice took the work to home for convenience purpose and not because of

compulsion. Referring to “FCT v Forsyth” the expenses incurred by Annice were not

relevant or incidental in derivation of assessable income.

D: Don will be denied deduction under “section 8-1” for mortgage and rates because worked

from home for convenience purpose. Citing “FCT v Forsyth” the expenses were not relevant

or incidental in derivation of assessable income (Woellner et al. 2014).

E: Russell will be denied deduction under “section 8-1” for purchasing and establishing a

shelf company. Referring to “FCT v Softwood Pulp & Paper” the expenses incurred by

Russell were preliminary to the commencement of income earning activities and hence non-

deductible (McCouat 2018).

F: Cherene will be denied deduction under “section 8-1” for purchasing and establishing a

shelf company of retail clothing. Referring to “Goodman Fielder Wattie v FCT” the

expenses incurred by Cherene were preliminary to the commencement of income earning

activities and hence non-deductible.

G: Mack will be allowed to claim deduction for the legal expenses incurred for the cessation

of the business under “section 8-1 of the ITAA 1997”. Citing “AGC Ltd v FCT (1975)” the

expenses incurred for business that were formerly carried on by Mack and hence it is tax

deductible.

H: Wilf will be denied deduction for the cost of preliminary expenses under “section 8-1 of

the ITAA 1997”. Referring to “FCT v Softwood Pulp & Paper” the expenses incurred by

B: Jo will be denied deduction under “section 8-1 of the ITAA 1997”. Referring to

“Handley v FCT” Jo being a barrister also maintained his own chamber or office in town and

hence no deduction will be allowed.

C: Annice will be denied for the expenses that were incurred from her home related to her

employment. Annice took the work to home for convenience purpose and not because of

compulsion. Referring to “FCT v Forsyth” the expenses incurred by Annice were not

relevant or incidental in derivation of assessable income.

D: Don will be denied deduction under “section 8-1” for mortgage and rates because worked

from home for convenience purpose. Citing “FCT v Forsyth” the expenses were not relevant

or incidental in derivation of assessable income (Woellner et al. 2014).

E: Russell will be denied deduction under “section 8-1” for purchasing and establishing a

shelf company. Referring to “FCT v Softwood Pulp & Paper” the expenses incurred by

Russell were preliminary to the commencement of income earning activities and hence non-

deductible (McCouat 2018).

F: Cherene will be denied deduction under “section 8-1” for purchasing and establishing a

shelf company of retail clothing. Referring to “Goodman Fielder Wattie v FCT” the

expenses incurred by Cherene were preliminary to the commencement of income earning

activities and hence non-deductible.

G: Mack will be allowed to claim deduction for the legal expenses incurred for the cessation

of the business under “section 8-1 of the ITAA 1997”. Citing “AGC Ltd v FCT (1975)” the

expenses incurred for business that were formerly carried on by Mack and hence it is tax

deductible.

H: Wilf will be denied deduction for the cost of preliminary expenses under “section 8-1 of

the ITAA 1997”. Referring to “FCT v Softwood Pulp & Paper” the expenses incurred by

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Wilf were preliminary to the commencement of income earning activities and hence non-

deductible (Morgan, Mortimer and Pinto 2017).

I: Janelle will be allowed to claim deduction under “section 8-1 of the ITAA 1997” for the

travel purpose because the expenses were incurred in derivation of assessable income.

J: Shaun will not be allowed to claim deduction for the sum of $1000 that was spend on

accommodation because the amount was entirely paid by his employer. As he did not

maintained any record, no deduction will be allowed to Shaun under “section 8-1 of the

ITAA 1997”.

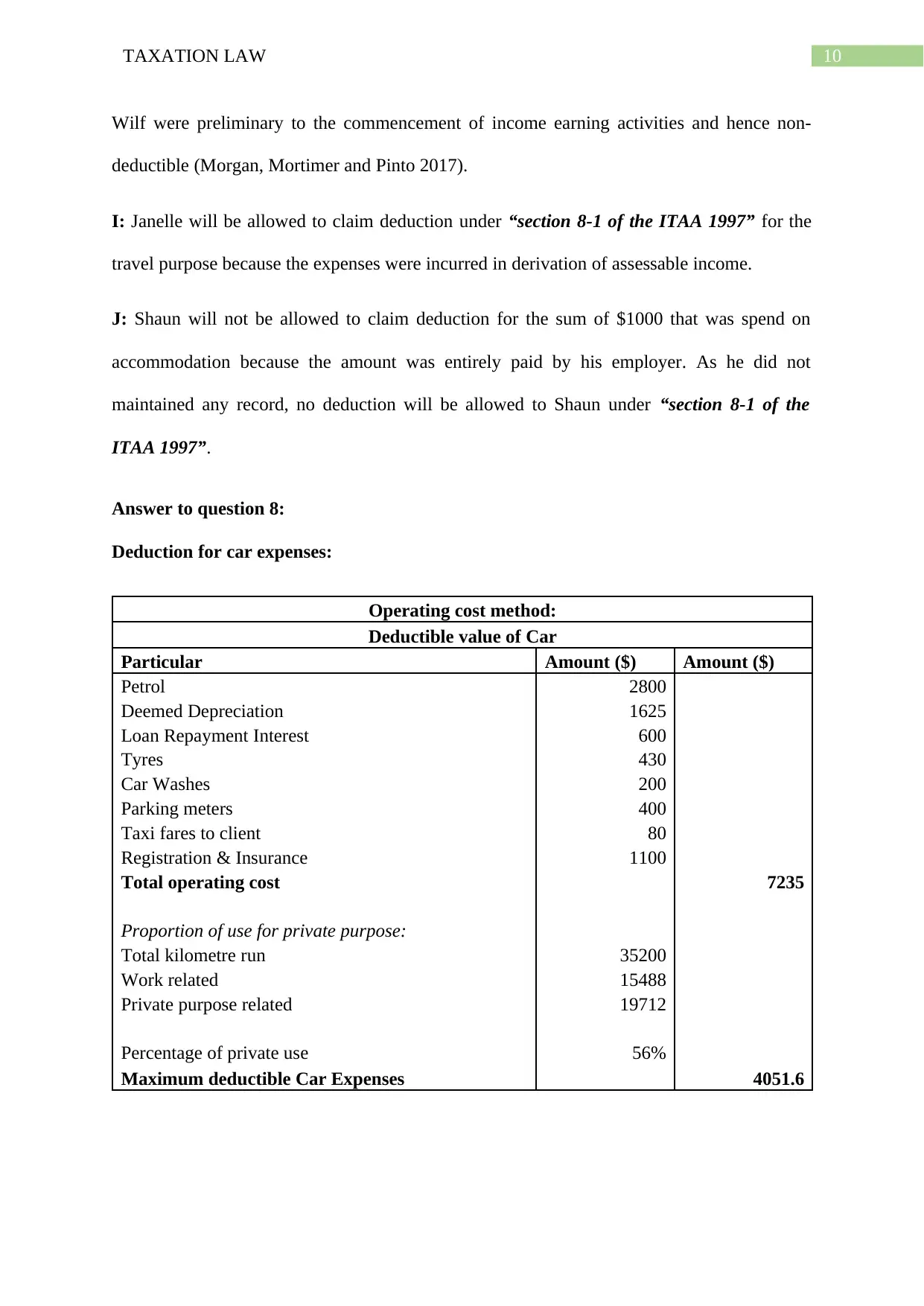

Answer to question 8:

Deduction for car expenses:

Operating cost method:

Deductible value of Car

Particular Amount ($) Amount ($)

Petrol 2800

Deemed Depreciation 1625

Loan Repayment Interest 600

Tyres 430

Car Washes 200

Parking meters 400

Taxi fares to client 80

Registration & Insurance 1100

Total operating cost 7235

Proportion of use for private purpose:

Total kilometre run 35200

Work related 15488

Private purpose related 19712

Percentage of private use 56%

Maximum deductible Car Expenses 4051.6

Wilf were preliminary to the commencement of income earning activities and hence non-

deductible (Morgan, Mortimer and Pinto 2017).

I: Janelle will be allowed to claim deduction under “section 8-1 of the ITAA 1997” for the

travel purpose because the expenses were incurred in derivation of assessable income.

J: Shaun will not be allowed to claim deduction for the sum of $1000 that was spend on

accommodation because the amount was entirely paid by his employer. As he did not

maintained any record, no deduction will be allowed to Shaun under “section 8-1 of the

ITAA 1997”.

Answer to question 8:

Deduction for car expenses:

Operating cost method:

Deductible value of Car

Particular Amount ($) Amount ($)

Petrol 2800

Deemed Depreciation 1625

Loan Repayment Interest 600

Tyres 430

Car Washes 200

Parking meters 400

Taxi fares to client 80

Registration & Insurance 1100

Total operating cost 7235

Proportion of use for private purpose:

Total kilometre run 35200

Work related 15488

Private purpose related 19712

Percentage of private use 56%

Maximum deductible Car Expenses 4051.6

11TAXATION LAW

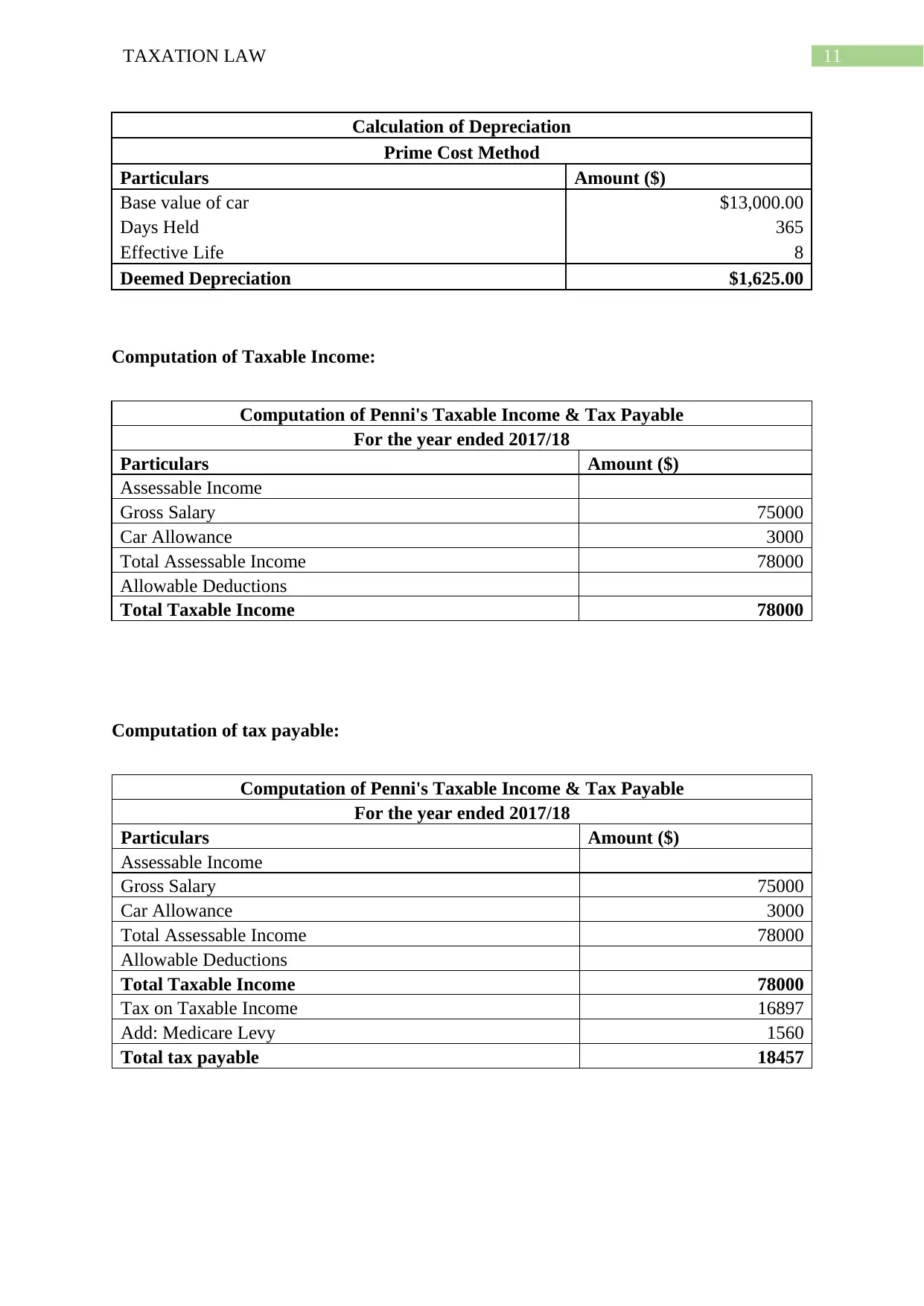

Calculation of Depreciation

Prime Cost Method

Particulars Amount ($)

Base value of car $13,000.00

Days Held 365

Effective Life 8

Deemed Depreciation $1,625.00

Computation of Taxable Income:

Computation of Penni's Taxable Income & Tax Payable

For the year ended 2017/18

Particulars Amount ($)

Assessable Income

Gross Salary 75000

Car Allowance 3000

Total Assessable Income 78000

Allowable Deductions

Total Taxable Income 78000

Computation of tax payable:

Computation of Penni's Taxable Income & Tax Payable

For the year ended 2017/18

Particulars Amount ($)

Assessable Income

Gross Salary 75000

Car Allowance 3000

Total Assessable Income 78000

Allowable Deductions

Total Taxable Income 78000

Tax on Taxable Income 16897

Add: Medicare Levy 1560

Total tax payable 18457

Calculation of Depreciation

Prime Cost Method

Particulars Amount ($)

Base value of car $13,000.00

Days Held 365

Effective Life 8

Deemed Depreciation $1,625.00

Computation of Taxable Income:

Computation of Penni's Taxable Income & Tax Payable

For the year ended 2017/18

Particulars Amount ($)

Assessable Income

Gross Salary 75000

Car Allowance 3000

Total Assessable Income 78000

Allowable Deductions

Total Taxable Income 78000

Computation of tax payable:

Computation of Penni's Taxable Income & Tax Payable

For the year ended 2017/18

Particulars Amount ($)

Assessable Income

Gross Salary 75000

Car Allowance 3000

Total Assessable Income 78000

Allowable Deductions

Total Taxable Income 78000

Tax on Taxable Income 16897

Add: Medicare Levy 1560

Total tax payable 18457

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.