Taxation Law Report: Case Studies on Taxation Issues and Rulings

VerifiedAdded on 2020/04/07

|12

|2240

|33

Report

AI Summary

This report provides a comprehensive analysis of various taxation law cases, addressing issues related to capital gains, fringe benefits tax (FBT), rental properties, tax avoidance, and the sale of timber. The report delves into specific scenarios, such as the acquisition of an antique vase, the implications of interest refunds from a banking corporation, the allocation of losses in co-owned rental properties, and the legal principles of tax avoidance. Each case is examined in detail, referencing relevant taxation rulings and legislation, including the Income Tax Assessment Act 1936 and associated regulations. The report offers concluding remarks for each case, summarizing the key findings and their implications for tax liability and compliance, providing a clear understanding of complex tax scenarios.

Running head: TAXATION LAW

Taxation Law

University Name

Student Name

Authors’ Note

Taxation Law

University Name

Student Name

Authors’ Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

TAXATION LAW

Table of Contents

Task 1:........................................................................................................................................2

Task 2:........................................................................................................................................4

Task 3:........................................................................................................................................6

Task 4:........................................................................................................................................8

Task 5:........................................................................................................................................8

References................................................................................................................................11

TAXATION LAW

Table of Contents

Task 1:........................................................................................................................................2

Task 2:........................................................................................................................................4

Task 3:........................................................................................................................................6

Task 4:........................................................................................................................................8

Task 5:........................................................................................................................................8

References................................................................................................................................11

3

TAXATION LAW

Task 1:

Issues that can be detected from the given case:

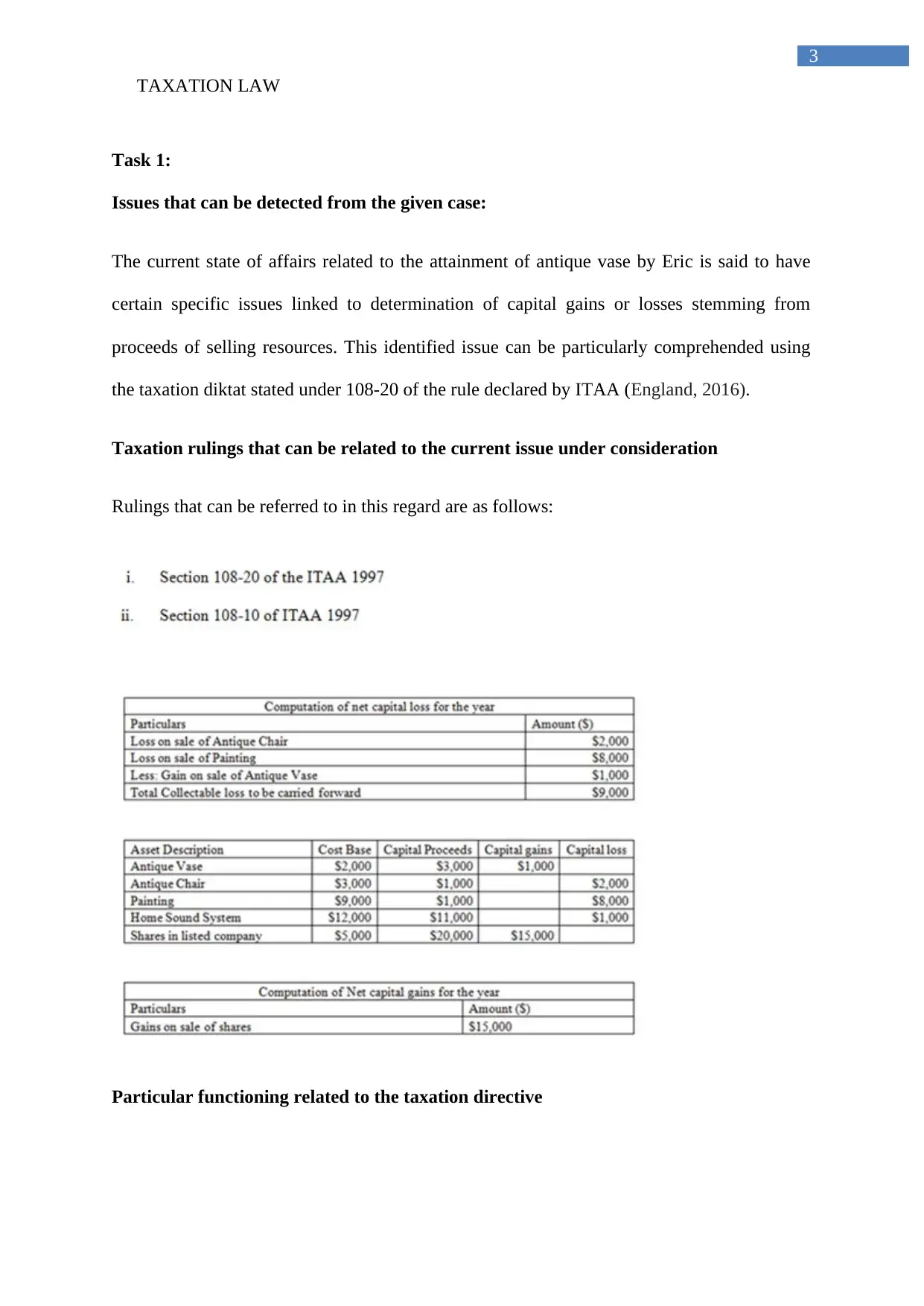

The current state of affairs related to the attainment of antique vase by Eric is said to have

certain specific issues linked to determination of capital gains or losses stemming from

proceeds of selling resources. This identified issue can be particularly comprehended using

the taxation diktat stated under 108-20 of the rule declared by ITAA (England, 2016).

Taxation rulings that can be related to the current issue under consideration

Rulings that can be referred to in this regard are as follows:

Particular functioning related to the taxation directive

TAXATION LAW

Task 1:

Issues that can be detected from the given case:

The current state of affairs related to the attainment of antique vase by Eric is said to have

certain specific issues linked to determination of capital gains or losses stemming from

proceeds of selling resources. This identified issue can be particularly comprehended using

the taxation diktat stated under 108-20 of the rule declared by ITAA (England, 2016).

Taxation rulings that can be related to the current issue under consideration

Rulings that can be referred to in this regard are as follows:

Particular functioning related to the taxation directive

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

TAXATION LAW

Founded on the taxation decree stated under the guideline mentioned under section 108-20

pronounced by ITAA, it can be hereby said that there is a total amount of loss of $1000 that

essentially stems from the marketing different home sound gadget. However, as per

mentioned regulation it can be said that this expenditure cannot be considered for the purpose

of subtraction from the assessable income. However, the tactic used for the purpose of

balancing the entire amount of losses can follow from the diktats stipulated under the 108 to

that of 110 sub sections of the law pronounced by ITAA -1997 (Braithwaite, 2016). In this

particular case, as Eric has achieved the profit from releasing of firm’s usual resources,

therefore no amount of capital can be considered for deduction in the current year. However,

the total gain obtained from investment of capital of Eric necessarily amounts to $15000.

Concluding Remark

As a result, it can be said that Eric cannot reimburse the loss suffered from various

collectables as he has acquired gains from the releasing of normal reserve.

Task 2:

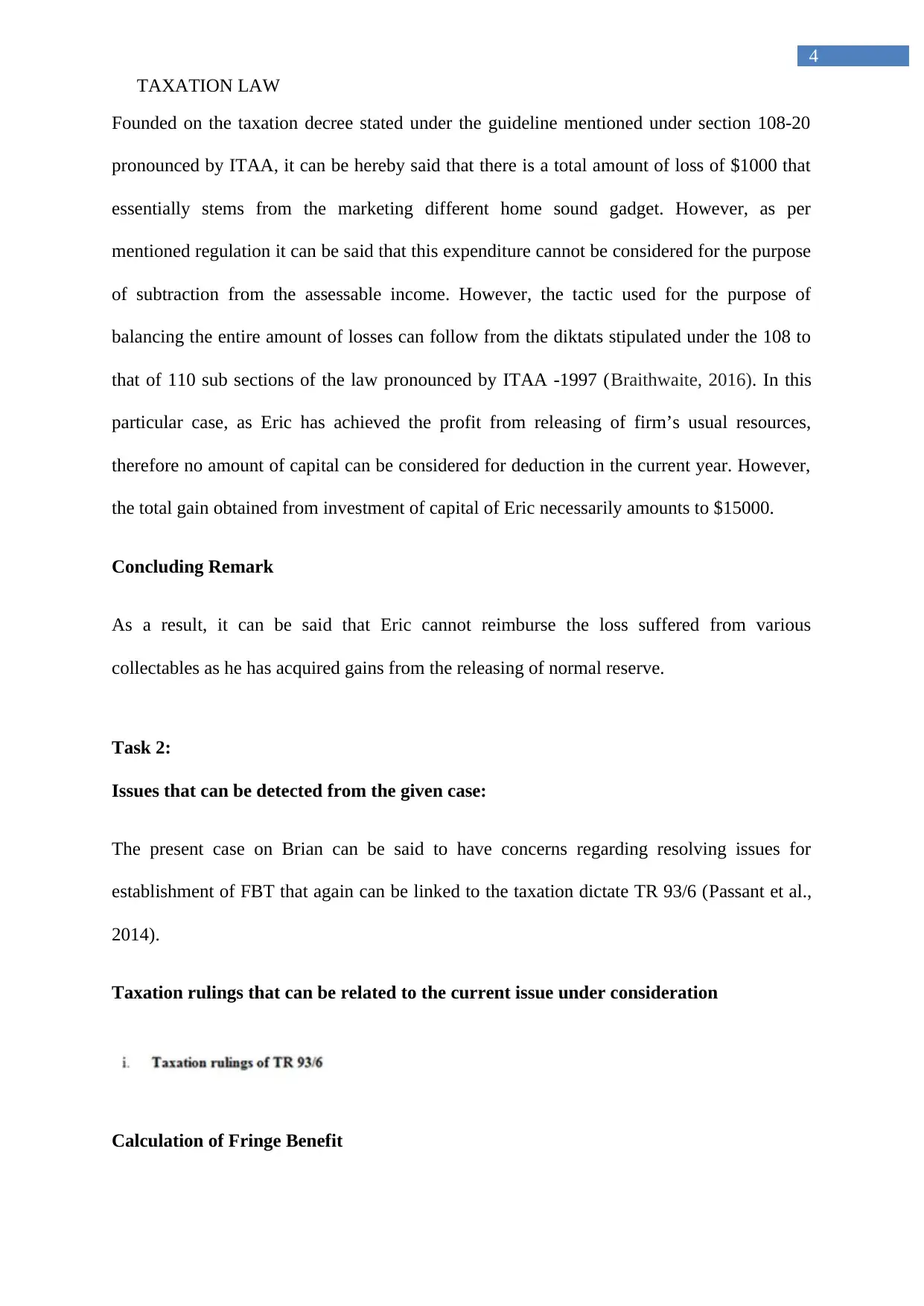

Issues that can be detected from the given case:

The present case on Brian can be said to have concerns regarding resolving issues for

establishment of FBT that again can be linked to the taxation dictate TR 93/6 (Passant et al.,

2014).

Taxation rulings that can be related to the current issue under consideration

Calculation of Fringe Benefit

TAXATION LAW

Founded on the taxation decree stated under the guideline mentioned under section 108-20

pronounced by ITAA, it can be hereby said that there is a total amount of loss of $1000 that

essentially stems from the marketing different home sound gadget. However, as per

mentioned regulation it can be said that this expenditure cannot be considered for the purpose

of subtraction from the assessable income. However, the tactic used for the purpose of

balancing the entire amount of losses can follow from the diktats stipulated under the 108 to

that of 110 sub sections of the law pronounced by ITAA -1997 (Braithwaite, 2016). In this

particular case, as Eric has achieved the profit from releasing of firm’s usual resources,

therefore no amount of capital can be considered for deduction in the current year. However,

the total gain obtained from investment of capital of Eric necessarily amounts to $15000.

Concluding Remark

As a result, it can be said that Eric cannot reimburse the loss suffered from various

collectables as he has acquired gains from the releasing of normal reserve.

Task 2:

Issues that can be detected from the given case:

The present case on Brian can be said to have concerns regarding resolving issues for

establishment of FBT that again can be linked to the taxation dictate TR 93/6 (Passant et al.,

2014).

Taxation rulings that can be related to the current issue under consideration

Calculation of Fringe Benefit

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

TAXATION LAW

Appropriate Functionalities:

Analysis of the taxation regulation helps in comprehending the fact in case if the banking

corporation necessarily liberates from the compulsion of refunding an interest, then in that

case Brian cannot be considered to be held responsible for paying back the tax amount

(Novikov et al., 2014)

Concluding Remarks:

Founded on specific taxation law, it can thus be stated that it is not obligatory to pay out a

specific amount for resolving the tax compulsion since Brian is released by the lending bank

for the payment of specific amount of interest.

TAXATION LAW

Appropriate Functionalities:

Analysis of the taxation regulation helps in comprehending the fact in case if the banking

corporation necessarily liberates from the compulsion of refunding an interest, then in that

case Brian cannot be considered to be held responsible for paying back the tax amount

(Novikov et al., 2014)

Concluding Remarks:

Founded on specific taxation law, it can thus be stated that it is not obligatory to pay out a

specific amount for resolving the tax compulsion since Brian is released by the lending bank

for the payment of specific amount of interest.

6

TAXATION LAW

Task 3:

Issues that can be detected from the given case:

The issues that can hereby be recognized from the given business scenario on Jill as well as

his wife can be related to subtraction of loss from a specific rental possessions since there is

co-control.

Taxation rulings that can be related to the current issue under consideration

Rulings that can be linked to the present issue under reflection are as follows:

Particular functioning related to the taxation directive

Taxation decree quoted under the directive TR 93/32 spells out that the entire amount of

earnings/ loss stemming from the rental possession between two diverse holders (Weller et

al., 2013). Essentially, the given set-up turns to appraisal of the tax of different co-holders of

properties that are in put on rent. Basically, Jack is particularly liable for nearly 10% of the

rental possession whilst Jill is liable for approximately 90% of the overall value of the co-

belongings. Thorough analysis of taxation law associated to the rental properties helps in

gaining deep insight regarding the fact that there subsists co-possession of different rental

resources that can be taken into account as partnership of rental reserve for assessable tax

(Tran-Nam, 2016). Again, earnings gathered from different rental properties can be deduced

from different rented assets. Pertinent decree states that contract of partnership might

TAXATION LAW

Task 3:

Issues that can be detected from the given case:

The issues that can hereby be recognized from the given business scenario on Jill as well as

his wife can be related to subtraction of loss from a specific rental possessions since there is

co-control.

Taxation rulings that can be related to the current issue under consideration

Rulings that can be linked to the present issue under reflection are as follows:

Particular functioning related to the taxation directive

Taxation decree quoted under the directive TR 93/32 spells out that the entire amount of

earnings/ loss stemming from the rental possession between two diverse holders (Weller et

al., 2013). Essentially, the given set-up turns to appraisal of the tax of different co-holders of

properties that are in put on rent. Basically, Jack is particularly liable for nearly 10% of the

rental possession whilst Jill is liable for approximately 90% of the overall value of the co-

belongings. Thorough analysis of taxation law associated to the rental properties helps in

gaining deep insight regarding the fact that there subsists co-possession of different rental

resources that can be taken into account as partnership of rental reserve for assessable tax

(Tran-Nam, 2016). Again, earnings gathered from different rental properties can be deduced

from different rented assets. Pertinent decree states that contract of partnership might

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

TAXATION LAW

possibly have the effect on allotment of earnings acquired from a rented property (Tran-Nam,

2016).

Again, taxation diktat mentioned that the co-holder of a rented resource/property under

reflection can never be taken into account as associates under normal verdict (Riaz et al.

2015). As such, in case of joint venture contract whether it be oral or else written does not

necessarily exert pressure on shared gain or else loss derived from a specific assets (Riaz et

al., 2015). Thus, co-possessors is Jill as well as his wife of different rental assets of both can

obtain the said assets on the entire amount since joint renters can be recognized to be very

usual in nature/features.

As is mentioned in the legal case on the “F.C. of T. v McDonald (1987) 18 ATR 957”, it can

thus be hereby stated that the spouse of payer of tax possessed two different layer title

fragments as a sort of joint endeavour (AO, 2015). Essentially, the contract verified between

the two possessors mention that the entire income obtained from the rental possessions can

once more be doled out in particular proportion. For example, the same can be distributed in

the fraction (25% to Mr. Donald and 75% to his wife). Even so, the entire loss incurred can

now be acquired by Mr. Mc Donald.

Concluding Remark:

As per the taxation diktat mentioned under the law stipulated under the TR 93/32 loss

stemming from c-holding of rental property need to be fairly doled out among different joint

owners (in this case Jack and his wife) (Lewis et al., 2014). Nevertheless, the joint possession

of the rental property cannot be taken into account as partnership business dealing.

TAXATION LAW

possibly have the effect on allotment of earnings acquired from a rented property (Tran-Nam,

2016).

Again, taxation diktat mentioned that the co-holder of a rented resource/property under

reflection can never be taken into account as associates under normal verdict (Riaz et al.

2015). As such, in case of joint venture contract whether it be oral or else written does not

necessarily exert pressure on shared gain or else loss derived from a specific assets (Riaz et

al., 2015). Thus, co-possessors is Jill as well as his wife of different rental assets of both can

obtain the said assets on the entire amount since joint renters can be recognized to be very

usual in nature/features.

As is mentioned in the legal case on the “F.C. of T. v McDonald (1987) 18 ATR 957”, it can

thus be hereby stated that the spouse of payer of tax possessed two different layer title

fragments as a sort of joint endeavour (AO, 2015). Essentially, the contract verified between

the two possessors mention that the entire income obtained from the rental possessions can

once more be doled out in particular proportion. For example, the same can be distributed in

the fraction (25% to Mr. Donald and 75% to his wife). Even so, the entire loss incurred can

now be acquired by Mr. Mc Donald.

Concluding Remark:

As per the taxation diktat mentioned under the law stipulated under the TR 93/32 loss

stemming from c-holding of rental property need to be fairly doled out among different joint

owners (in this case Jack and his wife) (Lewis et al., 2014). Nevertheless, the joint possession

of the rental property cannot be taken into account as partnership business dealing.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

TAXATION LAW

Task 4:

The ruling as mentioned herein the case on “IRC v Duke of Westminster [1936] AC 1” helps

in understanding facts about skirting of tax. However, in the current case study, a specific

principle was initiated stating about the assurance as regards a particular principle. This

helped in authentication of the fact that each and every individual can be approved to order

particular state of affairs that can allow taxation. As rightly indicated by Van Akkeren and

Tarr (2014), this regulation can be considered as an effective rule for different individuals

asking for avoidance of tax, when considering intricacy of legal structure. Basically, these

can be weakened by the specific cases in which courts have spoken about the authority on the

whole. In this case, by referring to the verdicts of the legal cases in the “WT Ramsay v. IRC

principle”, it can be better understood (Pearce & Pinto, 2015). Necessarily, in the current day

circumstances, the applicable standard with the purview of Australia states that in case if a

specific individual achieves success by reaching out to the conclusion, then for that case,

inland earnings from the acquired revenue might possibly be used for the particular

arrangement.

Task 5:

Issues that can be detected from the given case

The identified matter of concern points out towards the fact that intricacies in the process of

estimation of earnings from sale proceeds of felled timber. Nevertheless, this business case

can be evaluated by pointing out towards regulations announced under sub division 6(1) of

the taxation regulation of Income Tax Assessment Act publicized during 1936 (Barkoczy,

2017).

Taxation rulings that can be related to the current issue under consideration

TAXATION LAW

Task 4:

The ruling as mentioned herein the case on “IRC v Duke of Westminster [1936] AC 1” helps

in understanding facts about skirting of tax. However, in the current case study, a specific

principle was initiated stating about the assurance as regards a particular principle. This

helped in authentication of the fact that each and every individual can be approved to order

particular state of affairs that can allow taxation. As rightly indicated by Van Akkeren and

Tarr (2014), this regulation can be considered as an effective rule for different individuals

asking for avoidance of tax, when considering intricacy of legal structure. Basically, these

can be weakened by the specific cases in which courts have spoken about the authority on the

whole. In this case, by referring to the verdicts of the legal cases in the “WT Ramsay v. IRC

principle”, it can be better understood (Pearce & Pinto, 2015). Necessarily, in the current day

circumstances, the applicable standard with the purview of Australia states that in case if a

specific individual achieves success by reaching out to the conclusion, then for that case,

inland earnings from the acquired revenue might possibly be used for the particular

arrangement.

Task 5:

Issues that can be detected from the given case

The identified matter of concern points out towards the fact that intricacies in the process of

estimation of earnings from sale proceeds of felled timber. Nevertheless, this business case

can be evaluated by pointing out towards regulations announced under sub division 6(1) of

the taxation regulation of Income Tax Assessment Act publicized during 1936 (Barkoczy,

2017).

Taxation rulings that can be related to the current issue under consideration

9

TAXATION LAW

Particular functioning related to the taxation directive

Taxation ruling TR 95/6 mentioned in detail outcomes of tax occurring from activities of both

production plus forestry (England, 2016). In addition to this, this ruling also talks about

restriction to acceptance of proceeds obtained from selling of timber, evaluation of

quantifiable earning from forestry activities. Again, sub-regulation pronounced under Income

Tax Assessment Act -1936, main production is mainly linked to programs of plantation of

tree considered under plantation work.

Taking into consideration the present case study, it can thus be stated that Bill owns a defined

piece of land that necessarily cultivates trees. Essentially, Bill thought of using the piece of

land for grazing of sheep and wanted to get it cleaned. However, the logging business can

obtain right of utilizing the land. Being the holder of the land, Bill necessarily did not

undertake works of plantation and the entire amount accepted from cutting trees reflected the

entire amount that can be appraised for the purpose of taxation. Principally, in case if the

payers of tax were essentially paid a lump sum amount of approximately $50000 by agreeing

the concerned authority for removal of timber. In this specific case, the entire sum assumed

can be regarded as royalty. According to the taxation ruling/dictate stated under 26 (f),

royalties can be accepted from approval of the concerned authority to sell their product that is

in this case necessarily timber. Then again, under this specific situation, Bill cannot assume

business dealings linked to forestry. The current case explicates that expenses undertaken by

diverse individual grant can be necessarily taken into account under the particular influence.

Specifically, explicit amount accepted as royalty by Bill join the overall calculable earnings

and can be referred to as taxation ruling under section 26 (f) (Braithwaite, 2016).

TAXATION LAW

Particular functioning related to the taxation directive

Taxation ruling TR 95/6 mentioned in detail outcomes of tax occurring from activities of both

production plus forestry (England, 2016). In addition to this, this ruling also talks about

restriction to acceptance of proceeds obtained from selling of timber, evaluation of

quantifiable earning from forestry activities. Again, sub-regulation pronounced under Income

Tax Assessment Act -1936, main production is mainly linked to programs of plantation of

tree considered under plantation work.

Taking into consideration the present case study, it can thus be stated that Bill owns a defined

piece of land that necessarily cultivates trees. Essentially, Bill thought of using the piece of

land for grazing of sheep and wanted to get it cleaned. However, the logging business can

obtain right of utilizing the land. Being the holder of the land, Bill necessarily did not

undertake works of plantation and the entire amount accepted from cutting trees reflected the

entire amount that can be appraised for the purpose of taxation. Principally, in case if the

payers of tax were essentially paid a lump sum amount of approximately $50000 by agreeing

the concerned authority for removal of timber. In this specific case, the entire sum assumed

can be regarded as royalty. According to the taxation ruling/dictate stated under 26 (f),

royalties can be accepted from approval of the concerned authority to sell their product that is

in this case necessarily timber. Then again, under this specific situation, Bill cannot assume

business dealings linked to forestry. The current case explicates that expenses undertaken by

diverse individual grant can be necessarily taken into account under the particular influence.

Specifically, explicit amount accepted as royalty by Bill join the overall calculable earnings

and can be referred to as taxation ruling under section 26 (f) (Braithwaite, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

TAXATION LAW

Concluding Remark

In conclusion it can be hereby stated that recognizing receipt as earnings from marketing

felled trees can be taken into account as taxable earning. This can be particularly considered

under ruling sub-division 6(1) of tax decree of ITAA pronounced in 1997.

TAXATION LAW

Concluding Remark

In conclusion it can be hereby stated that recognizing receipt as earnings from marketing

felled trees can be taken into account as taxable earning. This can be particularly considered

under ruling sub-division 6(1) of tax decree of ITAA pronounced in 1997.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

TAXATION LAW

References

AO, M.D.A., (2015). Modernising the Australian Taxation Office: Vision, people, systems

and values. eJournal of Tax Research, 13(1), p.1.

Barkoczy, S., (2017). Core Tax Legislation and Study Guide. OUP Catalogue.

Braithwaite, J.B., (2016). Restorative Justice and Responsive Regulation: The Question of

Evidence.

England, P., (2016). Between Regulation and Markets: Ironies and Anomalies in the

Regulatory Governance of Biodiversity Conservation in Australia. 1 Australian

Journal of Environmental Law, p.44.

Gray, E., Oss-Emer, M. & Sheng, Y., (2014). Australian agricultural productivity

growth. Research by the Australian Bureau of Agricultural and Resource Economics

and Sciences, p.56.

Lewis, P., Richard, A. & Corliss, M., (2014). Compliance Costs of Regulation for Small

Business. Journal of Business Systems, Governance & Ethics, 9(2).

Novikov, A.A., Ling, T.G. & Kordzakhia, N., (2014). Pricing of volume-weighted average

options: Analytical approximations and numerical results. In Inspired by Finance (pp.

461-474). Springer International Publishing.

Passant, J., McLaren, J.A. & Silaen, P., (2014). Are returns received by householders from

electricity generated by solar panels assessable income?.

Pearce, P. & Pinto, D., (2015). An evaluation of the case for a congestion tax in

Australia. The Tax Specialist, 18(4), pp.146-153.

TAXATION LAW

References

AO, M.D.A., (2015). Modernising the Australian Taxation Office: Vision, people, systems

and values. eJournal of Tax Research, 13(1), p.1.

Barkoczy, S., (2017). Core Tax Legislation and Study Guide. OUP Catalogue.

Braithwaite, J.B., (2016). Restorative Justice and Responsive Regulation: The Question of

Evidence.

England, P., (2016). Between Regulation and Markets: Ironies and Anomalies in the

Regulatory Governance of Biodiversity Conservation in Australia. 1 Australian

Journal of Environmental Law, p.44.

Gray, E., Oss-Emer, M. & Sheng, Y., (2014). Australian agricultural productivity

growth. Research by the Australian Bureau of Agricultural and Resource Economics

and Sciences, p.56.

Lewis, P., Richard, A. & Corliss, M., (2014). Compliance Costs of Regulation for Small

Business. Journal of Business Systems, Governance & Ethics, 9(2).

Novikov, A.A., Ling, T.G. & Kordzakhia, N., (2014). Pricing of volume-weighted average

options: Analytical approximations and numerical results. In Inspired by Finance (pp.

461-474). Springer International Publishing.

Passant, J., McLaren, J.A. & Silaen, P., (2014). Are returns received by householders from

electricity generated by solar panels assessable income?.

Pearce, P. & Pinto, D., (2015). An evaluation of the case for a congestion tax in

Australia. The Tax Specialist, 18(4), pp.146-153.

12

TAXATION LAW

Riaz, Z., Ray, S. & Ray, P., (2015). The Synergistic Effect of State Regulation and Self-

Regulation on Disclosure Level of Director and Executive Remuneration in

Australia. Administration & Society, 47(6), pp.623-655.

Tran-Nam, B., (2016). Tax Reform and Tax Simplification: Conceptual and Measurement

Issues and Australian Experiences. In The Complexity of Tax Simplification (pp. 11-

44). Palgrave Macmillan UK.

Van Akkeren, J. & Tarr, J.A., (2014). Regulation, compliance and the Australian forensic

accounting profession. Journal of Forensic and Investigative Accounting, 6(3), pp.1-

26.

Weller, S., Smith, E.F. & Pritchard, B., (2013). Family or Enterprise? What shapes the

business structures of Australian farming?. Australian Geographer, 44(2), pp.129-

142.

TAXATION LAW

Riaz, Z., Ray, S. & Ray, P., (2015). The Synergistic Effect of State Regulation and Self-

Regulation on Disclosure Level of Director and Executive Remuneration in

Australia. Administration & Society, 47(6), pp.623-655.

Tran-Nam, B., (2016). Tax Reform and Tax Simplification: Conceptual and Measurement

Issues and Australian Experiences. In The Complexity of Tax Simplification (pp. 11-

44). Palgrave Macmillan UK.

Van Akkeren, J. & Tarr, J.A., (2014). Regulation, compliance and the Australian forensic

accounting profession. Journal of Forensic and Investigative Accounting, 6(3), pp.1-

26.

Weller, S., Smith, E.F. & Pritchard, B., (2013). Family or Enterprise? What shapes the

business structures of Australian farming?. Australian Geographer, 44(2), pp.129-

142.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.