Case Study: Taxation and Statutory Requirements for Sports Businesses

VerifiedAdded on 2020/12/09

|7

|1600

|249

Case Study

AI Summary

This case study analyzes various aspects of taxation within the Australian sports business context. It examines the tax implications for a golf club, including turnover and applicable tax rates for not-for-profit entities. The study also delves into the deductibility of legal expenses incurred by a sports company, specifically addressing whether expenses related to protecting exclusive rights are of capital nature. Furthermore, it explores the concept of special professional income averaging for a rugby player, differentiating between professional and other income sources for tax purposes. Finally, the case study assesses capital expenditure for a gym, determining the tax treatment of building upgrades and repairs, clarifying what constitutes capital expenditure and its implications for tax deductions. The report concludes with a summary of key statutory requirements and the importance of staying updated with tax legislation for efficient business operations.

Case study

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

TASK 2............................................................................................................................................2

TASK 3............................................................................................................................................2

TASK 4............................................................................................................................................3

CONCLUSION................................................................................................................................4

REFERENCES................................................................................................................................5

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

TASK 2............................................................................................................................................2

TASK 3............................................................................................................................................2

TASK 4............................................................................................................................................3

CONCLUSION................................................................................................................................4

REFERENCES................................................................................................................................5

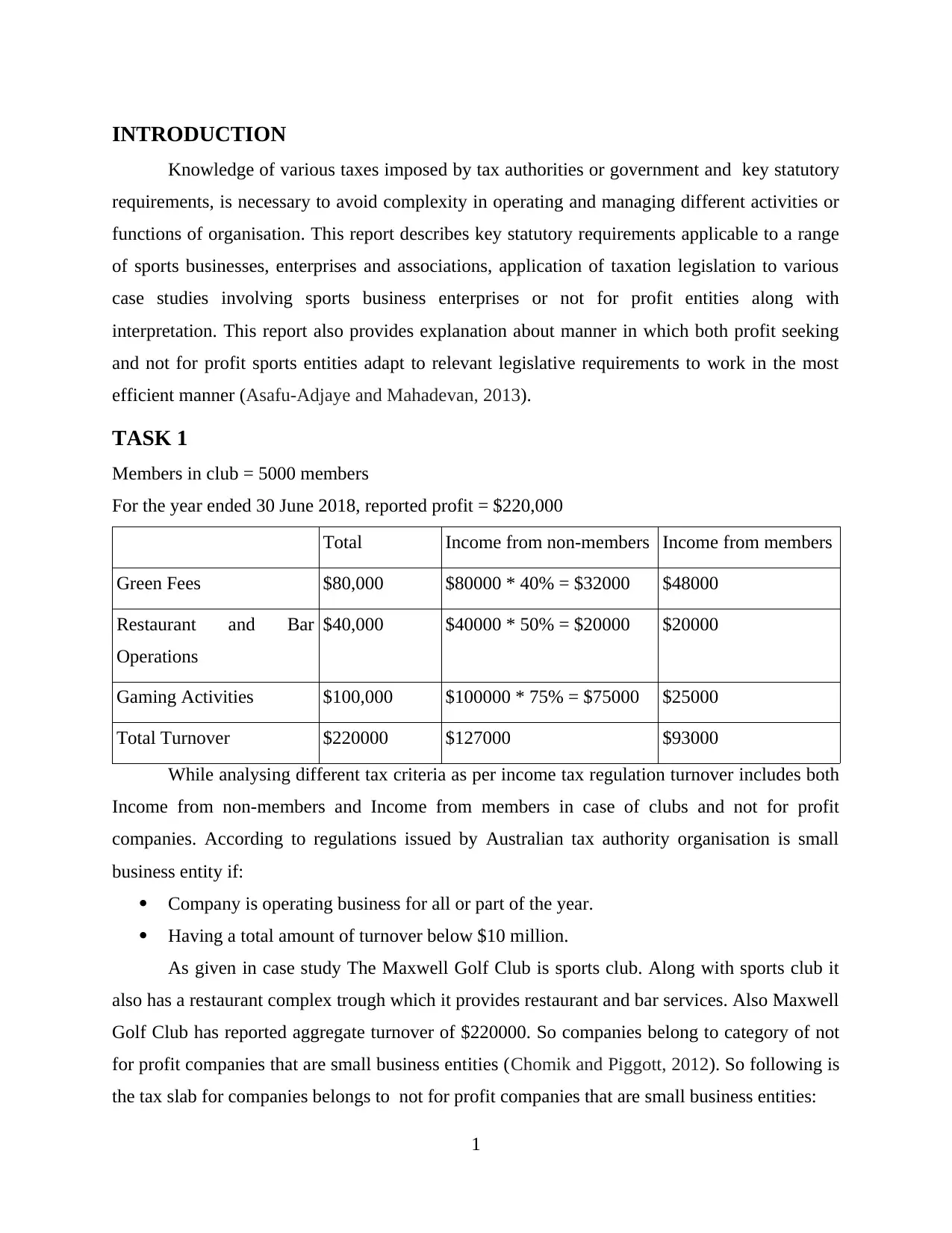

INTRODUCTION

Knowledge of various taxes imposed by tax authorities or government and key statutory

requirements, is necessary to avoid complexity in operating and managing different activities or

functions of organisation. This report describes key statutory requirements applicable to a range

of sports businesses, enterprises and associations, application of taxation legislation to various

case studies involving sports business enterprises or not for profit entities along with

interpretation. This report also provides explanation about manner in which both profit seeking

and not for profit sports entities adapt to relevant legislative requirements to work in the most

efficient manner (Asafu-Adjaye and Mahadevan, 2013).

TASK 1

Members in club = 5000 members

For the year ended 30 June 2018, reported profit = $220,000

Total Income from non-members Income from members

Green Fees $80,000 $80000 * 40% = $32000 $48000

Restaurant and Bar

Operations

$40,000 $40000 * 50% = $20000 $20000

Gaming Activities $100,000 $100000 * 75% = $75000 $25000

Total Turnover $220000 $127000 $93000

While analysing different tax criteria as per income tax regulation turnover includes both

Income from non-members and Income from members in case of clubs and not for profit

companies. According to regulations issued by Australian tax authority organisation is small

business entity if:

Company is operating business for all or part of the year.

Having a total amount of turnover below $10 million.

As given in case study The Maxwell Golf Club is sports club. Along with sports club it

also has a restaurant complex trough which it provides restaurant and bar services. Also Maxwell

Golf Club has reported aggregate turnover of $220000. So companies belong to category of not

for profit companies that are small business entities (Chomik and Piggott, 2012). So following is

the tax slab for companies belongs to not for profit companies that are small business entities:

1

Knowledge of various taxes imposed by tax authorities or government and key statutory

requirements, is necessary to avoid complexity in operating and managing different activities or

functions of organisation. This report describes key statutory requirements applicable to a range

of sports businesses, enterprises and associations, application of taxation legislation to various

case studies involving sports business enterprises or not for profit entities along with

interpretation. This report also provides explanation about manner in which both profit seeking

and not for profit sports entities adapt to relevant legislative requirements to work in the most

efficient manner (Asafu-Adjaye and Mahadevan, 2013).

TASK 1

Members in club = 5000 members

For the year ended 30 June 2018, reported profit = $220,000

Total Income from non-members Income from members

Green Fees $80,000 $80000 * 40% = $32000 $48000

Restaurant and Bar

Operations

$40,000 $40000 * 50% = $20000 $20000

Gaming Activities $100,000 $100000 * 75% = $75000 $25000

Total Turnover $220000 $127000 $93000

While analysing different tax criteria as per income tax regulation turnover includes both

Income from non-members and Income from members in case of clubs and not for profit

companies. According to regulations issued by Australian tax authority organisation is small

business entity if:

Company is operating business for all or part of the year.

Having a total amount of turnover below $10 million.

As given in case study The Maxwell Golf Club is sports club. Along with sports club it

also has a restaurant complex trough which it provides restaurant and bar services. Also Maxwell

Golf Club has reported aggregate turnover of $220000. So companies belong to category of not

for profit companies that are small business entities (Chomik and Piggott, 2012). So following is

the tax slab for companies belongs to not for profit companies that are small business entities:

1

Case : For Not-for-profit companies that

are small business entities Case : Other not-for-profit companies

If Taxable income

is :

Tax Rates would

be:

If Taxable

income is : Tax Rates would be:

0 – $ 416 Nil 0 – $ 416 Nil

$ 417 – $ 832

55% for every dollar

over $416 $ 417 – $ 915

55% for every dollar over

$416

$ 833 and above

27.5% for every

dollar

$ 916 and

above 30% for every dollar

Note: In case taxable income equals to $

833 or more then whole amount would be

taxable.

Note: In case taxable income equal to $ 916

or more then whole amount would be

taxable.

Therefore taxable amount for The Maxwell Golf Club would be:

$ 220,000 * 27.5% = $ 60500

TASK 2

According to rulings of income tax regularity of Australia, Expenses of capital nature are

not deductible. Generally legal expenses are of capital natures, following legal expenses are not

deductible, as follows:

1. Legal expenses related to acquisition or selling of property

2. Legal expenses for Resisting land resumption

3. Legal expense incurred to defend title property.

Here in given case Sydney Sports Ltd incurred legal expenses of $500,000 in October 2018 in

protecting its exclusive rights agreement with the Sydney Rugby Union to televise all major club

rugby fixtures in Sydney (Fletcher and Guttmann, 2013). The agreement is the sole asset of

Sydney Sports Ltd which indicates that such legal expenses are of capital nature therefore no

deduction is available for legal expenses of $500,000.

2

are small business entities Case : Other not-for-profit companies

If Taxable income

is :

Tax Rates would

be:

If Taxable

income is : Tax Rates would be:

0 – $ 416 Nil 0 – $ 416 Nil

$ 417 – $ 832

55% for every dollar

over $416 $ 417 – $ 915

55% for every dollar over

$416

$ 833 and above

27.5% for every

dollar

$ 916 and

above 30% for every dollar

Note: In case taxable income equals to $

833 or more then whole amount would be

taxable.

Note: In case taxable income equal to $ 916

or more then whole amount would be

taxable.

Therefore taxable amount for The Maxwell Golf Club would be:

$ 220,000 * 27.5% = $ 60500

TASK 2

According to rulings of income tax regularity of Australia, Expenses of capital nature are

not deductible. Generally legal expenses are of capital natures, following legal expenses are not

deductible, as follows:

1. Legal expenses related to acquisition or selling of property

2. Legal expenses for Resisting land resumption

3. Legal expense incurred to defend title property.

Here in given case Sydney Sports Ltd incurred legal expenses of $500,000 in October 2018 in

protecting its exclusive rights agreement with the Sydney Rugby Union to televise all major club

rugby fixtures in Sydney (Fletcher and Guttmann, 2013). The agreement is the sole asset of

Sydney Sports Ltd which indicates that such legal expenses are of capital nature therefore no

deduction is available for legal expenses of $500,000.

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TASK 3

When a individual uses physical skills in performing any activity then will be termed as

special professional. When a person fall in the group of special professional then eligibility for

special professional income averaging is applicable. This is a concessional tax treatment which

leads to application of tax at a rate lower then amount paid in general sense. Taxable professional

income is the amount remaining after taking away from the professional income the total of the

deductions that is reasonably related with the professional income. The deductions such as gifts

to charity will be taken into account for calculating the taxable professional income (Veall,

2012). The assessable professional income will include-

rewards and prices

income from endorsements, advertisements, interviews, commentating and any similar

services.

Royalty from copyright of a literary, dramatic, musical or artistic work.

Income from a patent for an invention.

In the given case Jamiles Elias a Rugby player is offered a three year contract in which an

amount of $2000 per game w3ill be paid. Together with this $10000 bonus will be paid if the

team makes the top at the end of the season and a lump sum of $150000 will be paid for entering

into the contract. As the person is special professional and tax will be charged at special rate. The

amount of payment received per match and bonus both will be termed as professional income of

the game. When amount of $150000 is received for playing only rugby and giving up on cricket

then it will not be termed as professional income and considered as other income. Rate of tax

charged on the professional income will be concessional but other income will be taxed at the

normal rate.

TASK 4

In the given situation on 1st July 2017, Max fit Gym acquired an abandoned warehouse in

order to convert into Gym. After this $750000 has been spent by the company on upgrading the

building to reasonable working condition. An asset that have a longer life are termed as capital

assets. Such as building, motor vehicles, furniture, machinery and equipment. A capital asset is

either the cost of an asset that has longer life(more then one year). An expense associated with

establishing, replacing, enlarging or improving the structure of business (Capital assets and

expenses, 2018). Capital expenditure is done in an small amount then it can be claimed as

3

When a individual uses physical skills in performing any activity then will be termed as

special professional. When a person fall in the group of special professional then eligibility for

special professional income averaging is applicable. This is a concessional tax treatment which

leads to application of tax at a rate lower then amount paid in general sense. Taxable professional

income is the amount remaining after taking away from the professional income the total of the

deductions that is reasonably related with the professional income. The deductions such as gifts

to charity will be taken into account for calculating the taxable professional income (Veall,

2012). The assessable professional income will include-

rewards and prices

income from endorsements, advertisements, interviews, commentating and any similar

services.

Royalty from copyright of a literary, dramatic, musical or artistic work.

Income from a patent for an invention.

In the given case Jamiles Elias a Rugby player is offered a three year contract in which an

amount of $2000 per game w3ill be paid. Together with this $10000 bonus will be paid if the

team makes the top at the end of the season and a lump sum of $150000 will be paid for entering

into the contract. As the person is special professional and tax will be charged at special rate. The

amount of payment received per match and bonus both will be termed as professional income of

the game. When amount of $150000 is received for playing only rugby and giving up on cricket

then it will not be termed as professional income and considered as other income. Rate of tax

charged on the professional income will be concessional but other income will be taxed at the

normal rate.

TASK 4

In the given situation on 1st July 2017, Max fit Gym acquired an abandoned warehouse in

order to convert into Gym. After this $750000 has been spent by the company on upgrading the

building to reasonable working condition. An asset that have a longer life are termed as capital

assets. Such as building, motor vehicles, furniture, machinery and equipment. A capital asset is

either the cost of an asset that has longer life(more then one year). An expense associated with

establishing, replacing, enlarging or improving the structure of business (Capital assets and

expenses, 2018). Capital expenditure is done in an small amount then it can be claimed as

3

expense in the same year. When amount of capital expenditure is huge then expense can be

claimed for an amount in decline value of the asset each year over the number of years. Amount

that is spend to make repair in building to bring it in working condition. Some capital

expenditure can not be claimed such as substantial improvement to an item or property. Repairs

made to machinery, tools or property immediately after purchase or acquire them then also

capital expenditure can not be claimed.

In the given case Max organisation also acquired an abandoned warehouse and after that

make expenditure to bring it in working condition. This expenditure of the company can not be

claimed as capital expenditure because price paid for the repairs reflects the items condition.

Amount that is spend on building will be included in the cost of acquisition of warehouse and

can not be deducted for the company in the tax year 2017 and 2018 (Worthington, 2012).

CONCLUSION

From this report it has been articulated that for organisation whether their motive is to

earn profit or not, adaption of key statutory requirements is essential to operate its functions in

smoothly manner. Some changes in tax legislation have major effects on organisation workings

so organisation should keep updated with current changes in tax legislation in order to prepare

themselves for such changes. Their is difference in the applicability of taxation policy of an

individual that is based on their profession and various taxation benefits in form of deductions

are provided to businesses and individuals to support them.

4

claimed for an amount in decline value of the asset each year over the number of years. Amount

that is spend to make repair in building to bring it in working condition. Some capital

expenditure can not be claimed such as substantial improvement to an item or property. Repairs

made to machinery, tools or property immediately after purchase or acquire them then also

capital expenditure can not be claimed.

In the given case Max organisation also acquired an abandoned warehouse and after that

make expenditure to bring it in working condition. This expenditure of the company can not be

claimed as capital expenditure because price paid for the repairs reflects the items condition.

Amount that is spend on building will be included in the cost of acquisition of warehouse and

can not be deducted for the company in the tax year 2017 and 2018 (Worthington, 2012).

CONCLUSION

From this report it has been articulated that for organisation whether their motive is to

earn profit or not, adaption of key statutory requirements is essential to operate its functions in

smoothly manner. Some changes in tax legislation have major effects on organisation workings

so organisation should keep updated with current changes in tax legislation in order to prepare

themselves for such changes. Their is difference in the applicability of taxation policy of an

individual that is based on their profession and various taxation benefits in form of deductions

are provided to businesses and individuals to support them.

4

REFERENCES

Books and Journals

Asafu-Adjaye, J. and Mahadevan, R., 2013. Implications of CO2 reduction policies for a high

carbon emitting economy. Energy economics. 38. pp.32-41.

Chomik, R. and Piggott, J., 2012. Pensions, Ageing and Retirement in Australia: Long‐Term

Projections and Policies. Australian Economic Review. 45(3). pp.350-361.

Fletcher, M. and Guttmann, B., 2013. Income inequality in Australia. Economic Round-up. (2).

p.35.

Veall, M. R., 2012. Top income shares in Canada: recent trends and policy implications.

Canadian Journal of Economics/Revue canadienne d'économique. 45(4). pp.1247-1272.

Worthington, A. C., 2012. The quarter century record on housing affordability, affordability

drivers, and government policy responses in Australia. International Journal of Housing

Markets and Analysis. 5(3). pp.235-252.

Online

Capital assets and expenses. 2018. [Online]. Available through:

<https://www.ato.gov.au/Business/Income-and-deductions-for-business/Deductions/

Capital-assets-and-expenses/>

5

Books and Journals

Asafu-Adjaye, J. and Mahadevan, R., 2013. Implications of CO2 reduction policies for a high

carbon emitting economy. Energy economics. 38. pp.32-41.

Chomik, R. and Piggott, J., 2012. Pensions, Ageing and Retirement in Australia: Long‐Term

Projections and Policies. Australian Economic Review. 45(3). pp.350-361.

Fletcher, M. and Guttmann, B., 2013. Income inequality in Australia. Economic Round-up. (2).

p.35.

Veall, M. R., 2012. Top income shares in Canada: recent trends and policy implications.

Canadian Journal of Economics/Revue canadienne d'économique. 45(4). pp.1247-1272.

Worthington, A. C., 2012. The quarter century record on housing affordability, affordability

drivers, and government policy responses in Australia. International Journal of Housing

Markets and Analysis. 5(3). pp.235-252.

Online

Capital assets and expenses. 2018. [Online]. Available through:

<https://www.ato.gov.au/Business/Income-and-deductions-for-business/Deductions/

Capital-assets-and-expenses/>

5

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.