Taxation Major Assignment Case Study of Stefan for 2017

VerifiedAdded on 2020/03/23

|5

|1253

|62

Case Study

AI Summary

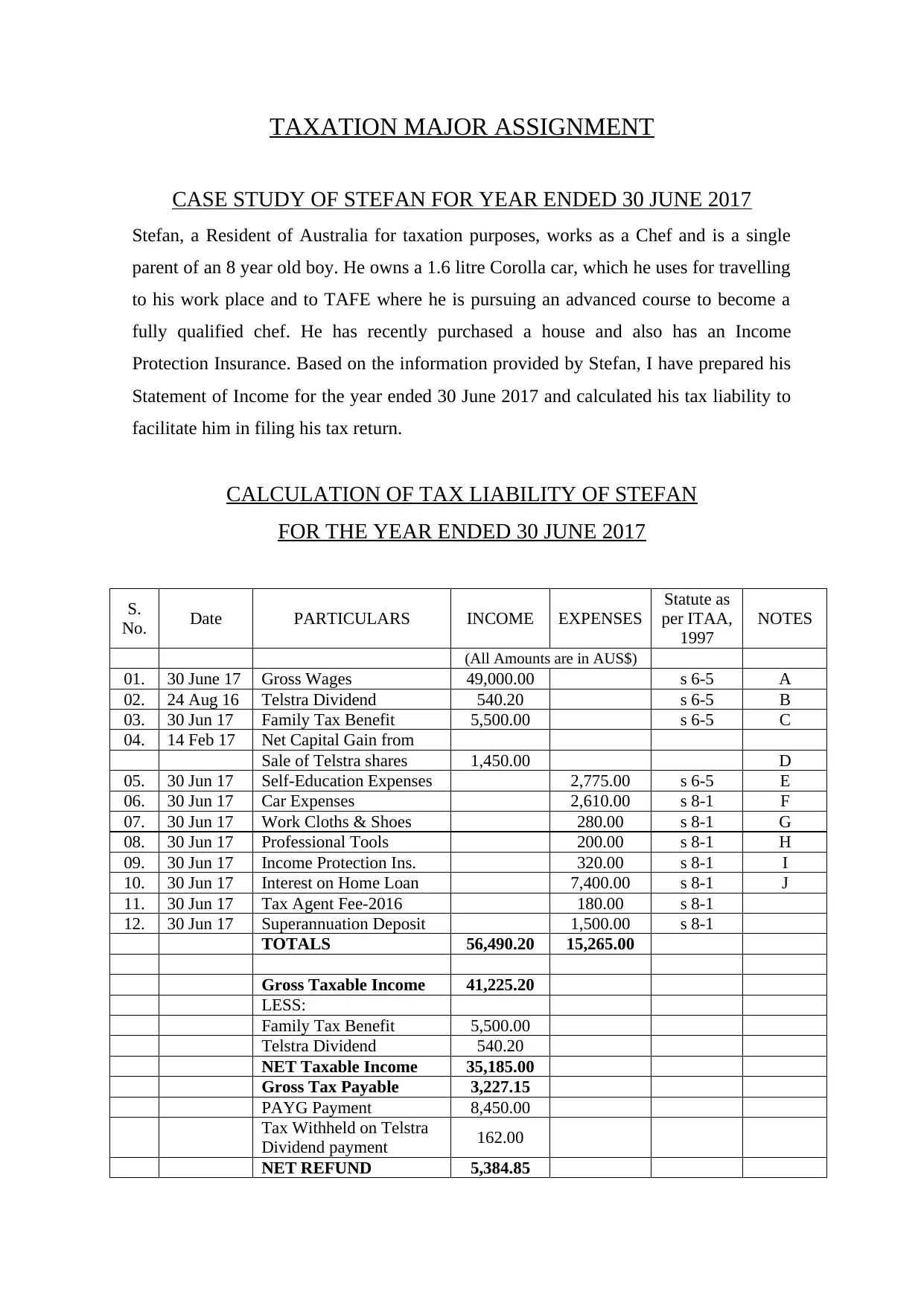

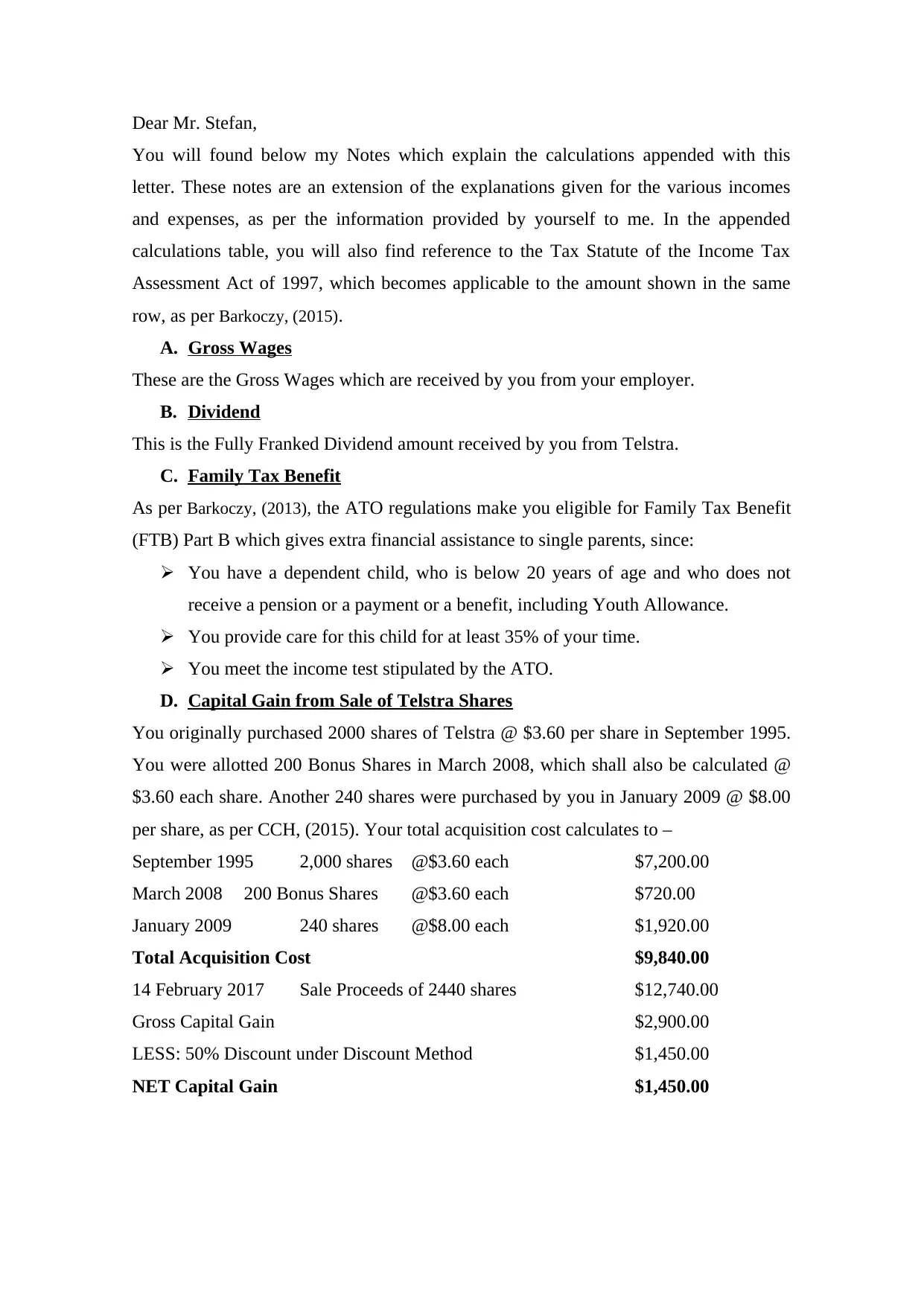

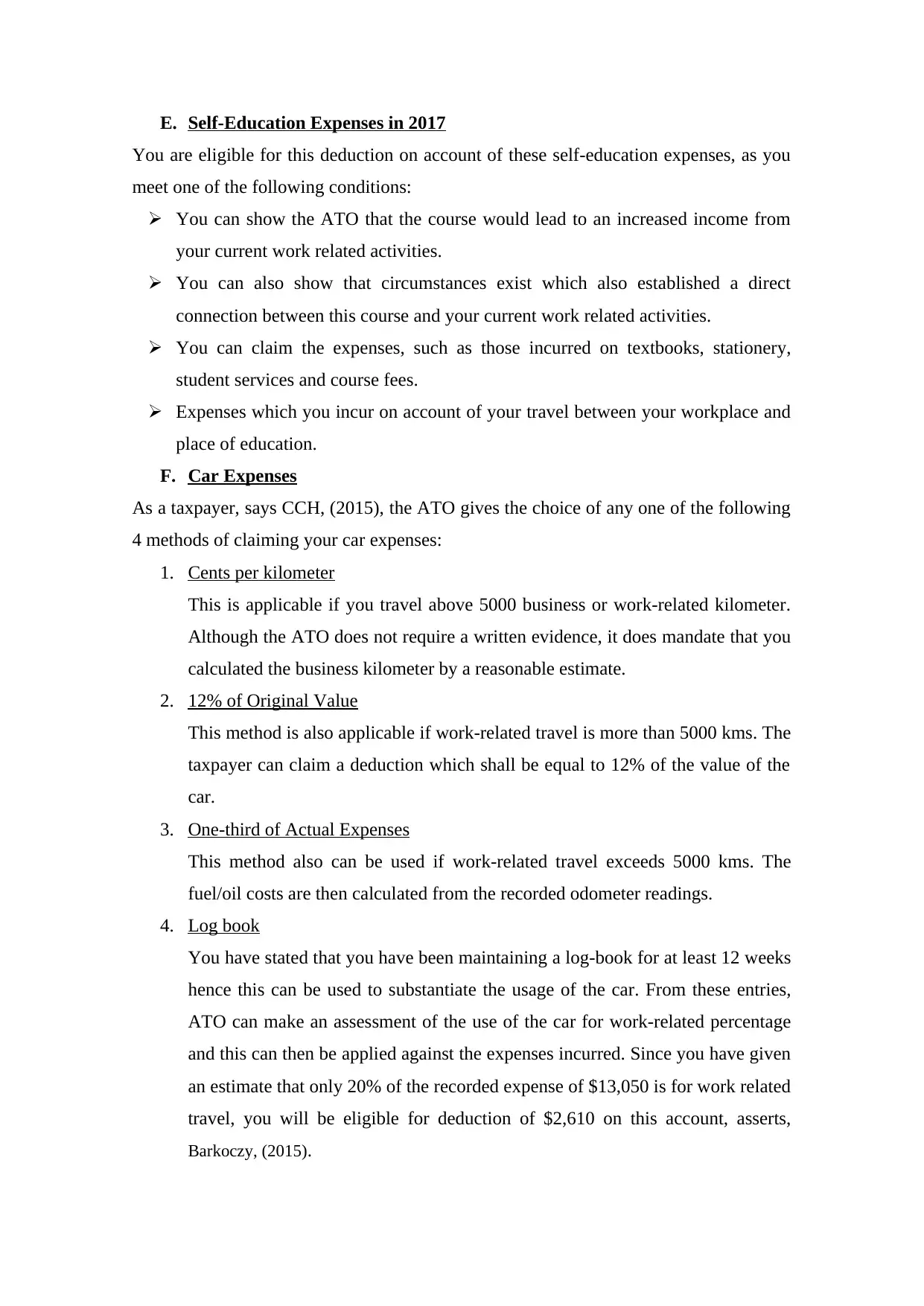

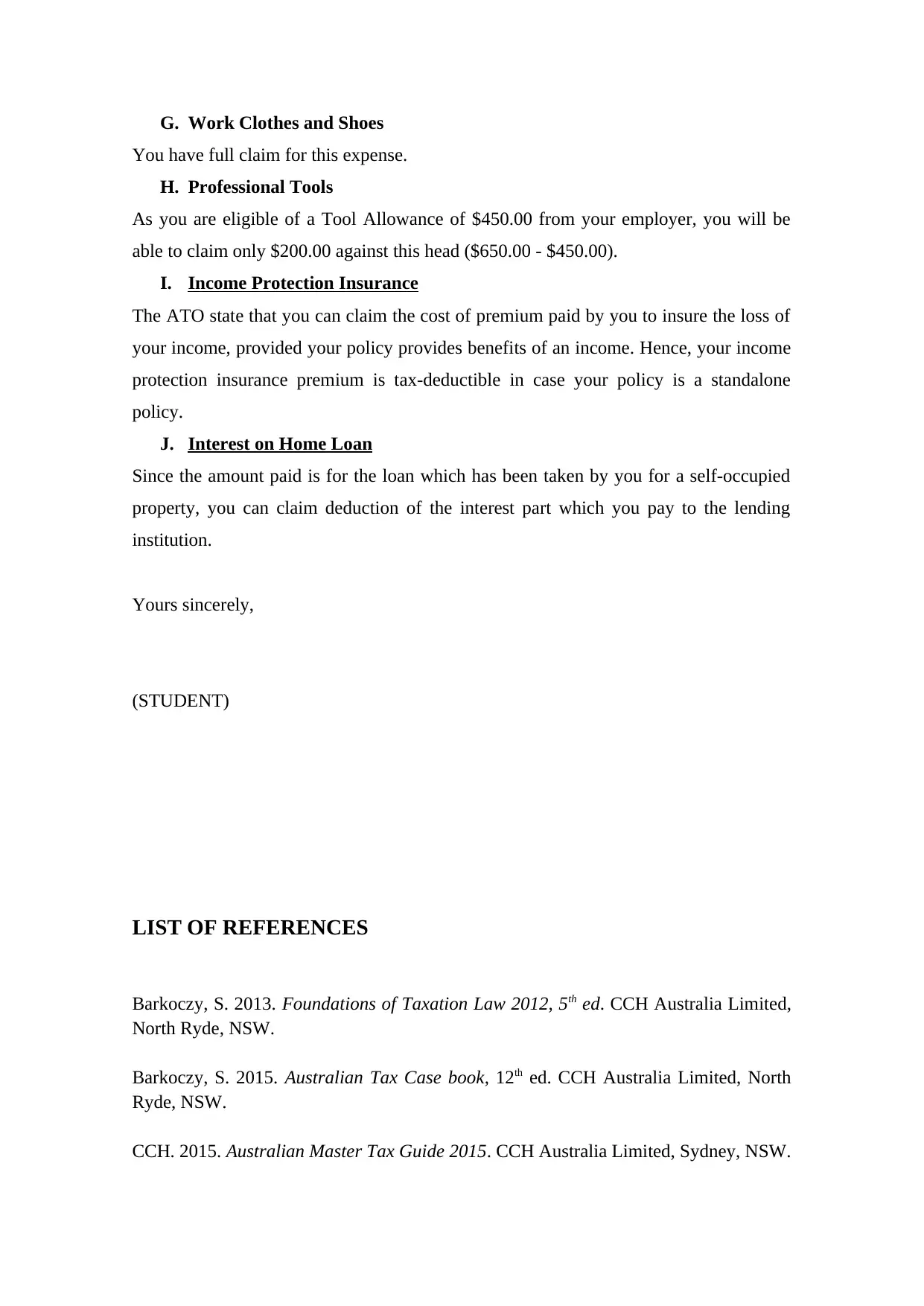

This assignment is a case study analyzing the tax situation of Stefan, an Australian resident chef and single parent, for the year ended June 30, 2017. It details his income sources, including gross wages, dividends, and family tax benefits, alongside his expenses, such as self-education, car, work clothes, professional tools, income protection insurance, and home loan interest. The document presents a comprehensive calculation of his taxable income, tax payable, and net refund, referencing the Income Tax Assessment Act 1997 and relevant tax regulations, including capital gains tax, deductions for self-education, car expenses, and other eligible claims. The analysis includes the calculation of capital gains from the sale of shares, detailing the acquisition cost and sale proceeds. The case study provides a detailed breakdown of each income and expense item, citing relevant tax laws and providing justifications for deductions, offering a practical application of taxation principles.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.