HI6028 Taxation Theory, Practice & Law T3 2018 Individual Assignment

VerifiedAdded on 2023/04/23

|11

|2515

|409

Homework Assignment

AI Summary

This document presents a detailed solution to the HI6028 Taxation Theory, Practice & Law assignment from T3 2018. The assignment addresses two key questions. Question 1 focuses on determining the net income for a partner, including provisions related to assessable income, repair and maintenance, trading stock, borrowing expenses, depreciation, and drawings. It includes detailed working papers with calculations for credit sales, credit purchases, stock changes, and depreciation. Question 2 explores fringe benefits tax (FBT) in the Australian tax system, defining fringe benefits, the assessment procedure, and providing a calculation example for an employee, John, considering housing and educational aid benefits. The solution references relevant sections of the Income Tax Assessment Act 1997 and provides citations for supporting legal cases and academic literature.

HI6028 Taxation Theory, Practice &

Law

T3 2018 Individual Assignment

Law

T3 2018 Individual Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Question 1..................................................................................................................................3

Provisions...............................................................................................................................3

Net income for the partner for the year ended 30 June 2017.................................................3

Working papers......................................................................................................................3

Question 2..................................................................................................................................3

Provisions...............................................................................................................................3

Calculations............................................................................................................................3

References..................................................................................................................................4

Question 1..................................................................................................................................3

Provisions...............................................................................................................................3

Net income for the partner for the year ended 30 June 2017.................................................3

Working papers......................................................................................................................3

Question 2..................................................................................................................................3

Provisions...............................................................................................................................3

Calculations............................................................................................................................3

References..................................................................................................................................4

QUESTION 1

Provisions

The provision related with the determination of the assessable income of the partnership firm

is contained in the Pt III of Division 5 of the Income Tax Assessment Act 1997. Tax is

chargeable on the all income which is derived by the firm from the ordinary course of the

business activity (Butler, and Giles, 2018). Along with this, normally all the expenses which

are incurred for carrying the business activity are allowed as deduction while calculating the

assessable income (Datt, and Keating, 2018). The provision related to the partnership firm is

described as below –

Repair and maintenance

As per the Income Tax Assessment Act 1997, section 25-5, the person can avail the

deduction of the expenses to the extent they are related with managing the tax affairs of the

business. Section 25-10 of the ITAA is related with the deduction of expenses related with

the repairs; it states that person can deduct expenses incurred for repairing the premises or

depreciating assets which are solely used for producing the assessable income (Wilkins,

2015). If the property is used party for the business purpose then only so much of expenses

are allowed for the deduction. Further, the deduction of the capital expenditure is not

allowed. Generally, the repair and maintenance related to the initial installation of the asset

are not deductible (Burkhauser, Hahn, and Wilkins, 2015). As per the legal case law FCT v

Western Suburbs Cinema, the court held that deduction is not allowed as the taxpayer chose

to make the capital expenditure by replacing the ceiling, therefore, it is notional repair which

is not deductible. Therefore if the item is considered as the improvement, then no deduction

is allowed. If the repair results in substantially replacing the asset, it is the capital expenditure

as per the decision was given under Lindsay v FCT. Further functional improvement in the

quality of the asset is not considered as the repair of the asset (Bloch, and Bhattacharya,

2016).

Trading stock

Trading stock is considered as the revenue assets, therefore, it is dealt as per the normal

income tax provisions (Chardon, Freudenberg, and Brimble, 2016). Receipt from sale of

trading stock is considered as the ordinary income which is assessable under section 6-5.

Provisions

The provision related with the determination of the assessable income of the partnership firm

is contained in the Pt III of Division 5 of the Income Tax Assessment Act 1997. Tax is

chargeable on the all income which is derived by the firm from the ordinary course of the

business activity (Butler, and Giles, 2018). Along with this, normally all the expenses which

are incurred for carrying the business activity are allowed as deduction while calculating the

assessable income (Datt, and Keating, 2018). The provision related to the partnership firm is

described as below –

Repair and maintenance

As per the Income Tax Assessment Act 1997, section 25-5, the person can avail the

deduction of the expenses to the extent they are related with managing the tax affairs of the

business. Section 25-10 of the ITAA is related with the deduction of expenses related with

the repairs; it states that person can deduct expenses incurred for repairing the premises or

depreciating assets which are solely used for producing the assessable income (Wilkins,

2015). If the property is used party for the business purpose then only so much of expenses

are allowed for the deduction. Further, the deduction of the capital expenditure is not

allowed. Generally, the repair and maintenance related to the initial installation of the asset

are not deductible (Burkhauser, Hahn, and Wilkins, 2015). As per the legal case law FCT v

Western Suburbs Cinema, the court held that deduction is not allowed as the taxpayer chose

to make the capital expenditure by replacing the ceiling, therefore, it is notional repair which

is not deductible. Therefore if the item is considered as the improvement, then no deduction

is allowed. If the repair results in substantially replacing the asset, it is the capital expenditure

as per the decision was given under Lindsay v FCT. Further functional improvement in the

quality of the asset is not considered as the repair of the asset (Bloch, and Bhattacharya,

2016).

Trading stock

Trading stock is considered as the revenue assets, therefore, it is dealt as per the normal

income tax provisions (Chardon, Freudenberg, and Brimble, 2016). Receipt from sale of

trading stock is considered as the ordinary income which is assessable under section 6-5.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Borrowing and interest expenses

Section 25-25 of the ITAA 1997 is related to the deduction of the borrowing expenses. This

section states that the deduction is allowed for the expenditure incurred for borrowing the

money used in generating the assessable income. These expenses are normally deducted over

the term of the loan amount. Interest on money loaned to the partnership is deductible

expenses to the partnership firm (Barth, 2017).

Depreciation

Depreciation can be calculated by two methods which are prime cost method and the

diminishing value method. In the prime cost, method depreciation is charged over the useful

life of asset uniformly (Richardson Taylor, and Lanis, 2015). In the case of the diminishing

method,

If the assets are hold before 10 May, 2006 then formula of depreciation =

Base vale * (days held/365)*150% / effective life of assets)

If the assets are hold after 10 May 2006 then the formula of depreciation =

Base vale * (days held/365)*200% / effective life of assets)

Drawings

Drawings of the partners are not deductible expenses from the assessable income (Cumming,

and Johan, 2016).

Union fee

Payment of the fee is allowed as deduction if the partner is the member of the union. In this

study, it is assumed that the partner is the member of the union, therefore, the deduction is

allowed.

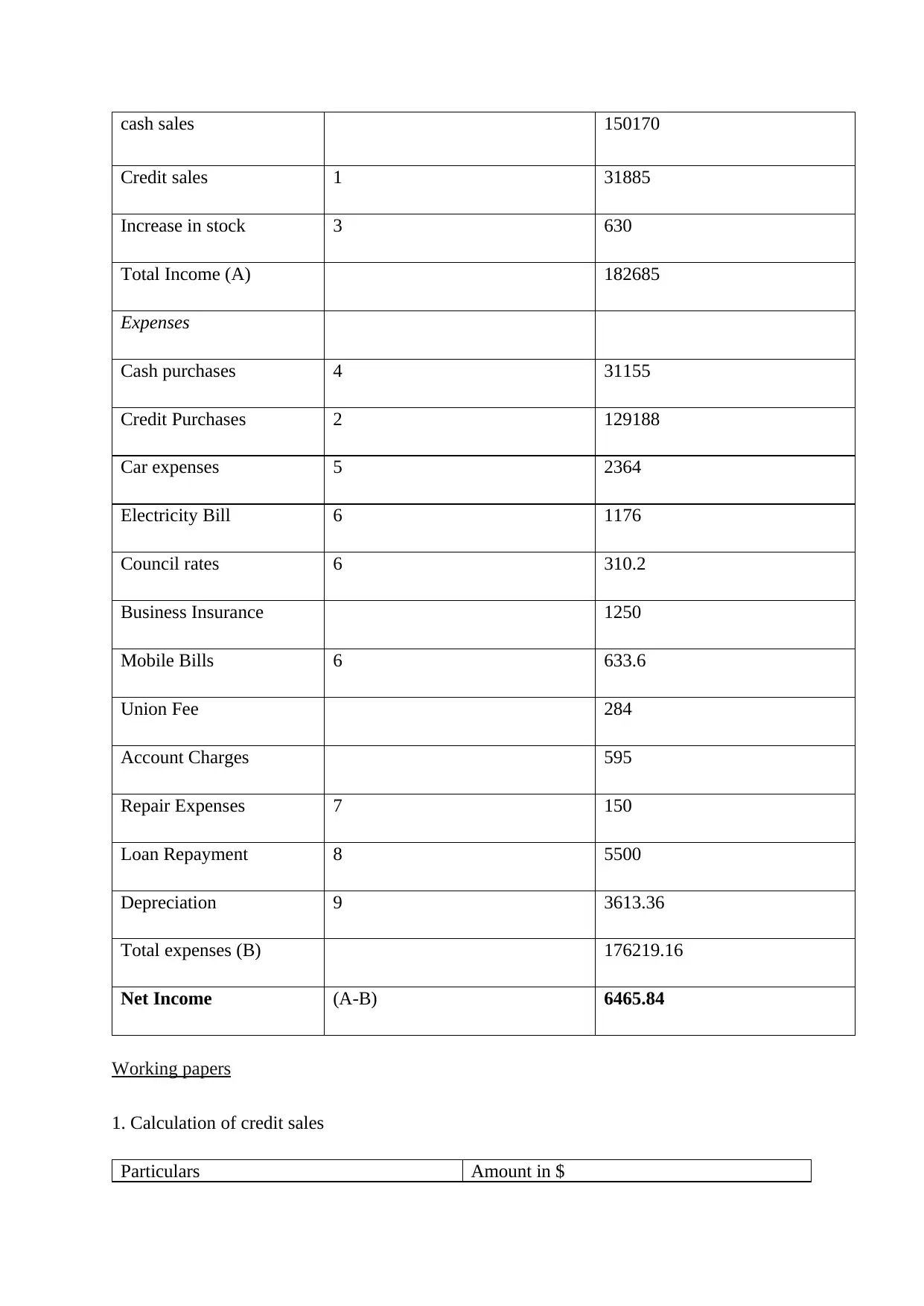

Net income for the partner for the year ended 30 June 2017

Particulars Working notes The amount in ($)

Income

Section 25-25 of the ITAA 1997 is related to the deduction of the borrowing expenses. This

section states that the deduction is allowed for the expenditure incurred for borrowing the

money used in generating the assessable income. These expenses are normally deducted over

the term of the loan amount. Interest on money loaned to the partnership is deductible

expenses to the partnership firm (Barth, 2017).

Depreciation

Depreciation can be calculated by two methods which are prime cost method and the

diminishing value method. In the prime cost, method depreciation is charged over the useful

life of asset uniformly (Richardson Taylor, and Lanis, 2015). In the case of the diminishing

method,

If the assets are hold before 10 May, 2006 then formula of depreciation =

Base vale * (days held/365)*150% / effective life of assets)

If the assets are hold after 10 May 2006 then the formula of depreciation =

Base vale * (days held/365)*200% / effective life of assets)

Drawings

Drawings of the partners are not deductible expenses from the assessable income (Cumming,

and Johan, 2016).

Union fee

Payment of the fee is allowed as deduction if the partner is the member of the union. In this

study, it is assumed that the partner is the member of the union, therefore, the deduction is

allowed.

Net income for the partner for the year ended 30 June 2017

Particulars Working notes The amount in ($)

Income

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

cash sales 150170

Credit sales 1 31885

Increase in stock 3 630

Total Income (A) 182685

Expenses

Cash purchases 4 31155

Credit Purchases 2 129188

Car expenses 5 2364

Electricity Bill 6 1176

Council rates 6 310.2

Business Insurance 1250

Mobile Bills 6 633.6

Union Fee 284

Account Charges 595

Repair Expenses 7 150

Loan Repayment 8 5500

Depreciation 9 3613.36

Total expenses (B) 176219.16

Net Income (A-B) 6465.84

Working papers

1. Calculation of credit sales

Particulars Amount in $

Credit sales 1 31885

Increase in stock 3 630

Total Income (A) 182685

Expenses

Cash purchases 4 31155

Credit Purchases 2 129188

Car expenses 5 2364

Electricity Bill 6 1176

Council rates 6 310.2

Business Insurance 1250

Mobile Bills 6 633.6

Union Fee 284

Account Charges 595

Repair Expenses 7 150

Loan Repayment 8 5500

Depreciation 9 3613.36

Total expenses (B) 176219.16

Net Income (A-B) 6465.84

Working papers

1. Calculation of credit sales

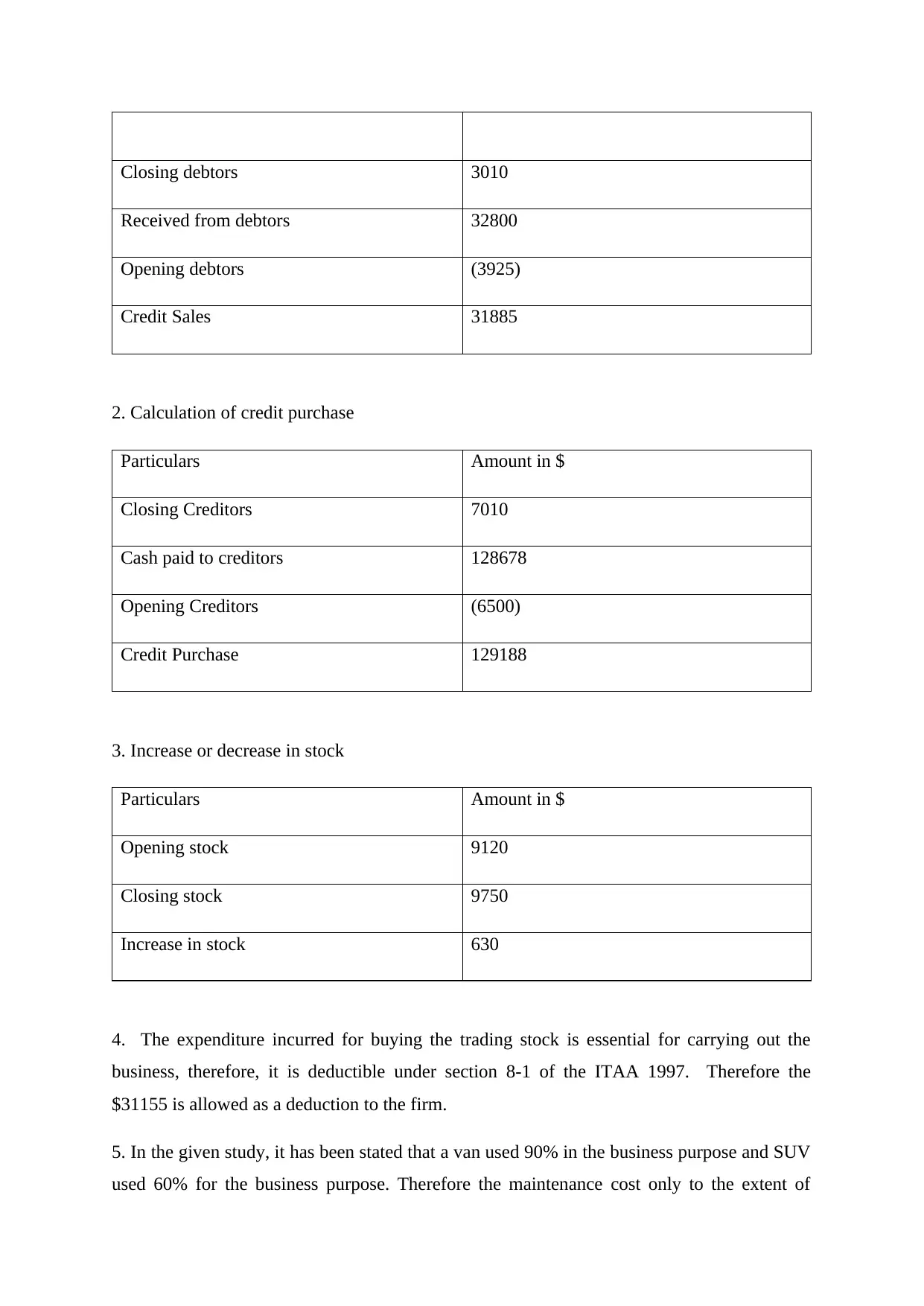

Particulars Amount in $

Closing debtors 3010

Received from debtors 32800

Opening debtors (3925)

Credit Sales 31885

2. Calculation of credit purchase

Particulars Amount in $

Closing Creditors 7010

Cash paid to creditors 128678

Opening Creditors (6500)

Credit Purchase 129188

3. Increase or decrease in stock

Particulars Amount in $

Opening stock 9120

Closing stock 9750

Increase in stock 630

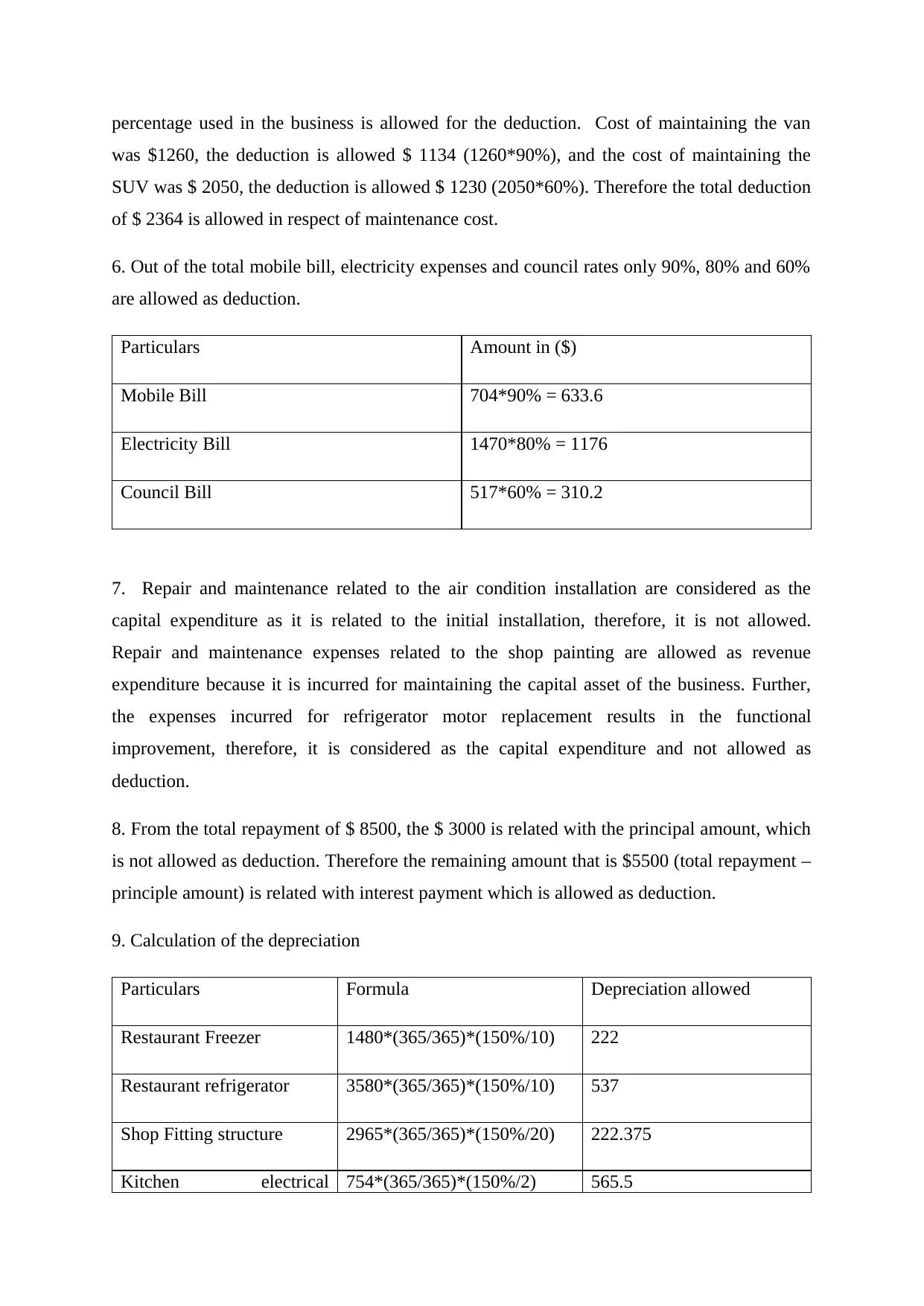

4. The expenditure incurred for buying the trading stock is essential for carrying out the

business, therefore, it is deductible under section 8-1 of the ITAA 1997. Therefore the

$31155 is allowed as a deduction to the firm.

5. In the given study, it has been stated that a van used 90% in the business purpose and SUV

used 60% for the business purpose. Therefore the maintenance cost only to the extent of

Received from debtors 32800

Opening debtors (3925)

Credit Sales 31885

2. Calculation of credit purchase

Particulars Amount in $

Closing Creditors 7010

Cash paid to creditors 128678

Opening Creditors (6500)

Credit Purchase 129188

3. Increase or decrease in stock

Particulars Amount in $

Opening stock 9120

Closing stock 9750

Increase in stock 630

4. The expenditure incurred for buying the trading stock is essential for carrying out the

business, therefore, it is deductible under section 8-1 of the ITAA 1997. Therefore the

$31155 is allowed as a deduction to the firm.

5. In the given study, it has been stated that a van used 90% in the business purpose and SUV

used 60% for the business purpose. Therefore the maintenance cost only to the extent of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

percentage used in the business is allowed for the deduction. Cost of maintaining the van

was $1260, the deduction is allowed $ 1134 (1260*90%), and the cost of maintaining the

SUV was $ 2050, the deduction is allowed $ 1230 (2050*60%). Therefore the total deduction

of $ 2364 is allowed in respect of maintenance cost.

6. Out of the total mobile bill, electricity expenses and council rates only 90%, 80% and 60%

are allowed as deduction.

Particulars Amount in ($)

Mobile Bill 704*90% = 633.6

Electricity Bill 1470*80% = 1176

Council Bill 517*60% = 310.2

7. Repair and maintenance related to the air condition installation are considered as the

capital expenditure as it is related to the initial installation, therefore, it is not allowed.

Repair and maintenance expenses related to the shop painting are allowed as revenue

expenditure because it is incurred for maintaining the capital asset of the business. Further,

the expenses incurred for refrigerator motor replacement results in the functional

improvement, therefore, it is considered as the capital expenditure and not allowed as

deduction.

8. From the total repayment of $ 8500, the $ 3000 is related with the principal amount, which

is not allowed as deduction. Therefore the remaining amount that is $5500 (total repayment –

principle amount) is related with interest payment which is allowed as deduction.

9. Calculation of the depreciation

Particulars Formula Depreciation allowed

Restaurant Freezer 1480*(365/365)*(150%/10) 222

Restaurant refrigerator 3580*(365/365)*(150%/10) 537

Shop Fitting structure 2965*(365/365)*(150%/20) 222.375

Kitchen electrical 754*(365/365)*(150%/2) 565.5

was $1260, the deduction is allowed $ 1134 (1260*90%), and the cost of maintaining the

SUV was $ 2050, the deduction is allowed $ 1230 (2050*60%). Therefore the total deduction

of $ 2364 is allowed in respect of maintenance cost.

6. Out of the total mobile bill, electricity expenses and council rates only 90%, 80% and 60%

are allowed as deduction.

Particulars Amount in ($)

Mobile Bill 704*90% = 633.6

Electricity Bill 1470*80% = 1176

Council Bill 517*60% = 310.2

7. Repair and maintenance related to the air condition installation are considered as the

capital expenditure as it is related to the initial installation, therefore, it is not allowed.

Repair and maintenance expenses related to the shop painting are allowed as revenue

expenditure because it is incurred for maintaining the capital asset of the business. Further,

the expenses incurred for refrigerator motor replacement results in the functional

improvement, therefore, it is considered as the capital expenditure and not allowed as

deduction.

8. From the total repayment of $ 8500, the $ 3000 is related with the principal amount, which

is not allowed as deduction. Therefore the remaining amount that is $5500 (total repayment –

principle amount) is related with interest payment which is allowed as deduction.

9. Calculation of the depreciation

Particulars Formula Depreciation allowed

Restaurant Freezer 1480*(365/365)*(150%/10) 222

Restaurant refrigerator 3580*(365/365)*(150%/10) 537

Shop Fitting structure 2965*(365/365)*(150%/20) 222.375

Kitchen electrical 754*(365/365)*(150%/2) 565.5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

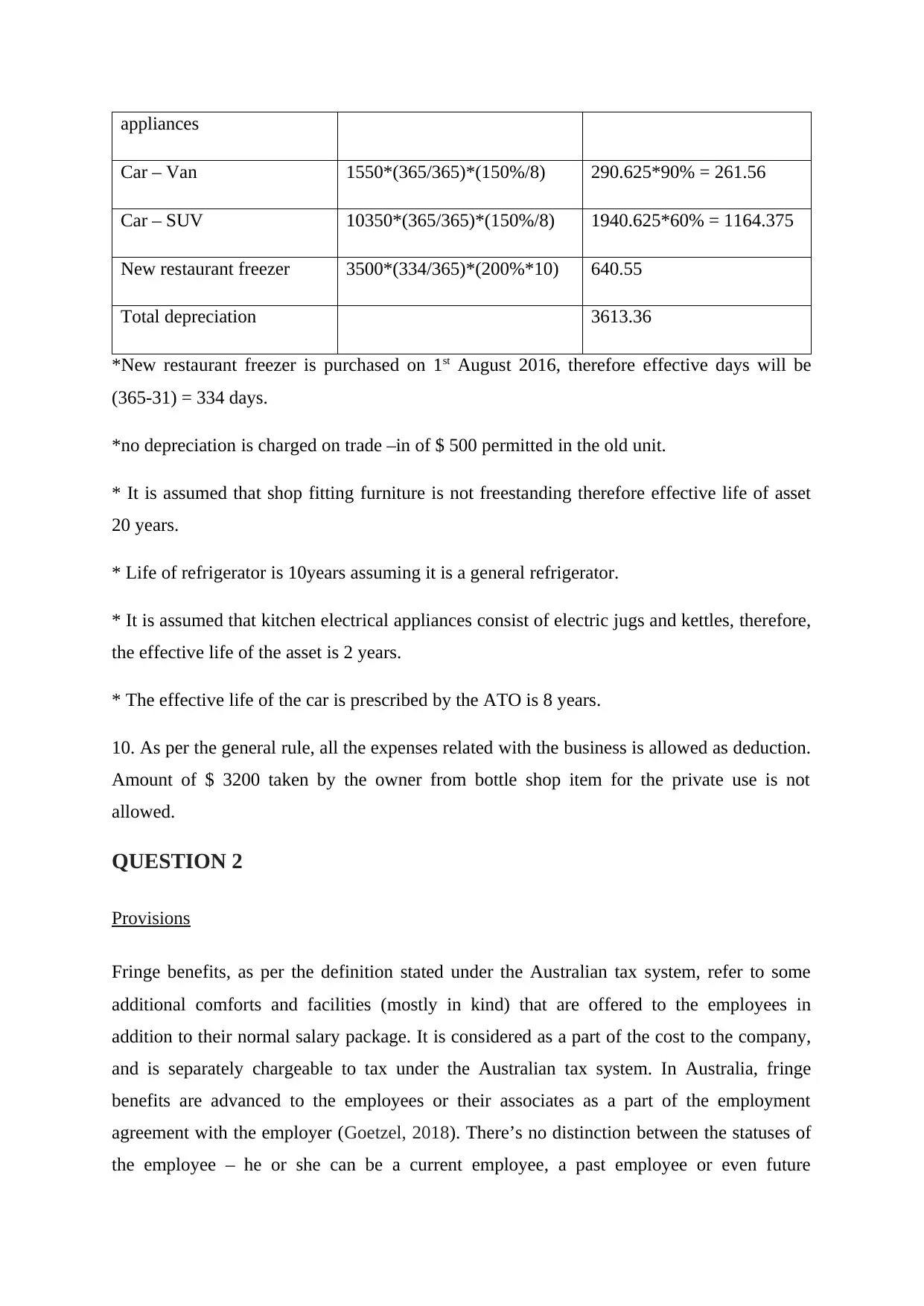

appliances

Car – Van 1550*(365/365)*(150%/8) 290.625*90% = 261.56

Car – SUV 10350*(365/365)*(150%/8) 1940.625*60% = 1164.375

New restaurant freezer 3500*(334/365)*(200%*10) 640.55

Total depreciation 3613.36

*New restaurant freezer is purchased on 1st August 2016, therefore effective days will be

(365-31) = 334 days.

*no depreciation is charged on trade –in of $ 500 permitted in the old unit.

* It is assumed that shop fitting furniture is not freestanding therefore effective life of asset

20 years.

* Life of refrigerator is 10years assuming it is a general refrigerator.

* It is assumed that kitchen electrical appliances consist of electric jugs and kettles, therefore,

the effective life of the asset is 2 years.

* The effective life of the car is prescribed by the ATO is 8 years.

10. As per the general rule, all the expenses related with the business is allowed as deduction.

Amount of $ 3200 taken by the owner from bottle shop item for the private use is not

allowed.

QUESTION 2

Provisions

Fringe benefits, as per the definition stated under the Australian tax system, refer to some

additional comforts and facilities (mostly in kind) that are offered to the employees in

addition to their normal salary package. It is considered as a part of the cost to the company,

and is separately chargeable to tax under the Australian tax system. In Australia, fringe

benefits are advanced to the employees or their associates as a part of the employment

agreement with the employer (Goetzel, 2018). There’s no distinction between the statuses of

the employee – he or she can be a current employee, a past employee or even future

Car – Van 1550*(365/365)*(150%/8) 290.625*90% = 261.56

Car – SUV 10350*(365/365)*(150%/8) 1940.625*60% = 1164.375

New restaurant freezer 3500*(334/365)*(200%*10) 640.55

Total depreciation 3613.36

*New restaurant freezer is purchased on 1st August 2016, therefore effective days will be

(365-31) = 334 days.

*no depreciation is charged on trade –in of $ 500 permitted in the old unit.

* It is assumed that shop fitting furniture is not freestanding therefore effective life of asset

20 years.

* Life of refrigerator is 10years assuming it is a general refrigerator.

* It is assumed that kitchen electrical appliances consist of electric jugs and kettles, therefore,

the effective life of the asset is 2 years.

* The effective life of the car is prescribed by the ATO is 8 years.

10. As per the general rule, all the expenses related with the business is allowed as deduction.

Amount of $ 3200 taken by the owner from bottle shop item for the private use is not

allowed.

QUESTION 2

Provisions

Fringe benefits, as per the definition stated under the Australian tax system, refer to some

additional comforts and facilities (mostly in kind) that are offered to the employees in

addition to their normal salary package. It is considered as a part of the cost to the company,

and is separately chargeable to tax under the Australian tax system. In Australia, fringe

benefits are advanced to the employees or their associates as a part of the employment

agreement with the employer (Goetzel, 2018). There’s no distinction between the statuses of

the employee – he or she can be a current employee, a past employee or even future

recruitment. Further, as per the proviso contained in the law, it has been stated that the

contractors are not included in the definition of employees; they are a separate entity and

shall not be treated at par with the employees.

The Australian tax system has assigned the fringe benefits into various categories, depending

upon their value and frequency of availing. This is followed by laying down of rules for the

taxation of these benefits, which may differ from case to case. Following are some of the

categories according to which the final liability may be calculated: -

Car Fringe Benefits

Parking Fringe Benefits

Lodging and Housing Fringe Benefits

Loan Granting Fringe Benefits

The Assessment Procedure

Once the assessee (the taxpayer) gets acquainted of the category in which the benefits paid by

him fall, he can then proceed to chalk out the final liability imposed on him (Freebairn,

2018). The FBT can then be calculated easily by following some simple steps as enumerated

below: -

Calculate the gross value of the taxable fringe benefits

Deduct any amount which has been recovered, either in part or full, from the

employee

Multiply the amount so calculated with the FBT rate followed by a boost with gross-

up rate

The resulting amount will be the total liability payable by the employer in regards to

fringe benefits tax

Calculations

John, who is working with a printing company, has been provided with two different types of

fringe benefits, namely housing and education aid. Hence, in the light of the above laws and

as per the latest provisions made in regards to FBT, the final liability in case of John’s perks

can be calculated as follows: -

[(Housing Allowance + Educational Aid) x FBT Rate for the Assessment Year

Ending March 2019 x Type – 2 Gross-Up Rate] – Recovery Made from John

contractors are not included in the definition of employees; they are a separate entity and

shall not be treated at par with the employees.

The Australian tax system has assigned the fringe benefits into various categories, depending

upon their value and frequency of availing. This is followed by laying down of rules for the

taxation of these benefits, which may differ from case to case. Following are some of the

categories according to which the final liability may be calculated: -

Car Fringe Benefits

Parking Fringe Benefits

Lodging and Housing Fringe Benefits

Loan Granting Fringe Benefits

The Assessment Procedure

Once the assessee (the taxpayer) gets acquainted of the category in which the benefits paid by

him fall, he can then proceed to chalk out the final liability imposed on him (Freebairn,

2018). The FBT can then be calculated easily by following some simple steps as enumerated

below: -

Calculate the gross value of the taxable fringe benefits

Deduct any amount which has been recovered, either in part or full, from the

employee

Multiply the amount so calculated with the FBT rate followed by a boost with gross-

up rate

The resulting amount will be the total liability payable by the employer in regards to

fringe benefits tax

Calculations

John, who is working with a printing company, has been provided with two different types of

fringe benefits, namely housing and education aid. Hence, in the light of the above laws and

as per the latest provisions made in regards to FBT, the final liability in case of John’s perks

can be calculated as follows: -

[(Housing Allowance + Educational Aid) x FBT Rate for the Assessment Year

Ending March 2019 x Type – 2 Gross-Up Rate] – Recovery Made from John

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

[($800 x 52 weeks – $100 x 52 weeks) + $15000) x 47% x 1.8868] [($41, 600 – $5200 + $15000) x 47% x 1.8868] $45, 581.3144

Hence, the final tax liability conferred upon the employer regarding the fringe benefits paid

to John amounts to $45, 581.3144. However, the fringe benefits enjoyed by John shall also be

reported by the employer on John’s PAYG payment summary (erstwhile group certificate),

since the quantum of benefits paid exceeds $2000.

Hence, the final tax liability conferred upon the employer regarding the fringe benefits paid

to John amounts to $45, 581.3144. However, the fringe benefits enjoyed by John shall also be

reported by the employer on John’s PAYG payment summary (erstwhile group certificate),

since the quantum of benefits paid exceeds $2000.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Barth, J., (2016). Agenda for Australia: Reality of family unit must underlie the tax

system. News Weekly, Issue 3007 (21 Oct 2017) p.7.

Bloch, H. and Bhattacharya, M., (2016). Promotion of innovation and job growth in small‐

and medium‐sized enterprises in Australia: Evidence and policy issues. Australian Economic

Review, 49(2), pp.192-199.

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., (2015). Measuring top incomes using tax

record data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2),

pp.181-205.

Butler, T. and Giles, A., 2018. Tax and inequality. Australian Options, (88), p.10.

Chardon, T., Freudenberg, B. and Brimble, M., (2016).Tax literacy in Australia: not knowing

your deduction from your offset. Austl. Tax F., 31, p.321.

Cumming, D. and Johan, S., (2016).Venture’s economic impact in Australia. The Journal of

Technology Transfer, 41(1), pp.25-59.

Datt, K.H. and Keating, M., (2018). April. The Commissioner’s obligation to make

compensating adjustments for income tax and GST in Australia and New Zealand.

In Australian Tax Forum (Vol. 33, No. 3).

Freebairn, J., (2018). Federalism and Tax Reform. Australian Economic Review, 51(2),

pp.262-268.

Goetzel, R.Z., (2018). Review of Promoting Worker Health: A New Approach to Employee

Benefits in the Twenty-First Century. Journal of Occupational and Environmental

Medicine, 60(12), p.e681.

Richardson, G., Taylor, G. and Lanis, R., (2015). The impact of financial distress on

corporate tax avoidance spanning the global financial crisis: Evidence from

Australia. Economic Modelling, 44, pp.44-53.

Wilkins, R., (2015). Measuring income inequality in Australia. Australian Economic

Review, 48(1), pp.93-102.

Barth, J., (2016). Agenda for Australia: Reality of family unit must underlie the tax

system. News Weekly, Issue 3007 (21 Oct 2017) p.7.

Bloch, H. and Bhattacharya, M., (2016). Promotion of innovation and job growth in small‐

and medium‐sized enterprises in Australia: Evidence and policy issues. Australian Economic

Review, 49(2), pp.192-199.

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., (2015). Measuring top incomes using tax

record data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2),

pp.181-205.

Butler, T. and Giles, A., 2018. Tax and inequality. Australian Options, (88), p.10.

Chardon, T., Freudenberg, B. and Brimble, M., (2016).Tax literacy in Australia: not knowing

your deduction from your offset. Austl. Tax F., 31, p.321.

Cumming, D. and Johan, S., (2016).Venture’s economic impact in Australia. The Journal of

Technology Transfer, 41(1), pp.25-59.

Datt, K.H. and Keating, M., (2018). April. The Commissioner’s obligation to make

compensating adjustments for income tax and GST in Australia and New Zealand.

In Australian Tax Forum (Vol. 33, No. 3).

Freebairn, J., (2018). Federalism and Tax Reform. Australian Economic Review, 51(2),

pp.262-268.

Goetzel, R.Z., (2018). Review of Promoting Worker Health: A New Approach to Employee

Benefits in the Twenty-First Century. Journal of Occupational and Environmental

Medicine, 60(12), p.e681.

Richardson, G., Taylor, G. and Lanis, R., (2015). The impact of financial distress on

corporate tax avoidance spanning the global financial crisis: Evidence from

Australia. Economic Modelling, 44, pp.44-53.

Wilkins, R., (2015). Measuring income inequality in Australia. Australian Economic

Review, 48(1), pp.93-102.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.