Taxation Theory, Practice & Law Assignment - Finance Module

VerifiedAdded on 2021/02/19

|10

|2642

|26

Homework Assignment

AI Summary

This taxation assignment analyzes two scenarios. The first case examines City Sky Co., a property developer, and its entitlement to GST input tax credits for legal services related to land purchase for apartment construction. The analysis focuses on the application of GST rules, including taxable, GST-free, and input-taxed supplies, and the conditions for claiming input tax credits. The second case involves Emma, who sold land and shares, and the calculation of capital gains tax. The assignment applies the Income Tax Assessment Act 1997 to determine the cost base, capital gains, and the tax implications of various expenses and transactions, including stamp duty and the sale of a piano. The assignment concludes by summarizing the GST implications for City Sky Co. and the capital gains tax liabilities for Emma, highlighting the relevant tax provisions and calculations.

Taxation Theory, Practice &

Law

Law

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

QUESTION 1...................................................................................................................................1

Rule..............................................................................................................................................1

Application...................................................................................................................................2

Conclusion...................................................................................................................................3

QUESTION 2...................................................................................................................................1

Rule..............................................................................................................................................1

Application...................................................................................................................................2

Conclusions..................................................................................................................................3

REFERENCES................................................................................................................................5

QUESTION 1...................................................................................................................................1

Rule..............................................................................................................................................1

Application...................................................................................................................................2

Conclusion...................................................................................................................................3

QUESTION 2...................................................................................................................................1

Rule..............................................................................................................................................1

Application...................................................................................................................................2

Conclusions..................................................................................................................................3

REFERENCES................................................................................................................................5

QUESTION 1

City sky Co a property investor & development company purchased a vacant piece in south

Brisbane with a motive of building 15 apartments for sale. Company has entailed the services of

Maurice Blackburn a local lawyer for providing legal guidance on development for $ 33000. A

well established proprietary business is being run by lawyer Maurice Blackburn having turnover

of $ 300000 for the year. The tax credits entitlements for the City Sky are to be found out

assuming it to be registered GST company.

Rule

GST - It is a general principle related to tax on supply. GST is payable by person who

has made the taxable supply. GST is paid by purchaser only when contract with seller requires

the GST to be paid by purchaser or to be reimbursed to seller which he is required to pay.

Generally it is seller who have to pay GST to ATO which is ultimately paid by consumer. GST

is applicable on purchase and sale of land. One has to be clear whether GST rates are applicable

on it or not.

As per guidelines of ATO, GST credit can be claimed if the prices is paid for the

purchase of goods or services which are bought for the business purpose. This is also known as

input tax credit. Credit for prices inclusive of taxes for business inputs (Claiming GST

credits,2019)

GST credit can be claimed if following conditions are satisfied

The purchase or service was undertaken partly or solely for business and it is not related

to making of input taxed supplies.

Purchase price is inclusive of GST.

Tax invoice for the goods or service is available from supplier.

Circumstances where GST credit cannot be claimed

If the company is not GST registered.

Purchases that are not having GST inclusive in their prices,

◦ Sale is GST free.

◦ Where the purchase is input taxed.

◦ Purchases from unregistered supplier or that has applied for registration.

For wages

If tax invoice is not available for purchases costing above $ 82.50

1

City sky Co a property investor & development company purchased a vacant piece in south

Brisbane with a motive of building 15 apartments for sale. Company has entailed the services of

Maurice Blackburn a local lawyer for providing legal guidance on development for $ 33000. A

well established proprietary business is being run by lawyer Maurice Blackburn having turnover

of $ 300000 for the year. The tax credits entitlements for the City Sky are to be found out

assuming it to be registered GST company.

Rule

GST - It is a general principle related to tax on supply. GST is payable by person who

has made the taxable supply. GST is paid by purchaser only when contract with seller requires

the GST to be paid by purchaser or to be reimbursed to seller which he is required to pay.

Generally it is seller who have to pay GST to ATO which is ultimately paid by consumer. GST

is applicable on purchase and sale of land. One has to be clear whether GST rates are applicable

on it or not.

As per guidelines of ATO, GST credit can be claimed if the prices is paid for the

purchase of goods or services which are bought for the business purpose. This is also known as

input tax credit. Credit for prices inclusive of taxes for business inputs (Claiming GST

credits,2019)

GST credit can be claimed if following conditions are satisfied

The purchase or service was undertaken partly or solely for business and it is not related

to making of input taxed supplies.

Purchase price is inclusive of GST.

Tax invoice for the goods or service is available from supplier.

Circumstances where GST credit cannot be claimed

If the company is not GST registered.

Purchases that are not having GST inclusive in their prices,

◦ Sale is GST free.

◦ Where the purchase is input taxed.

◦ Purchases from unregistered supplier or that has applied for registration.

For wages

If tax invoice is not available for purchases costing above $ 82.50

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Purchased Real state property under marginal scheme.

Application

As City Sky Company is the development firm and makes investment in the property so

the main GST consequences that applies to this company involves if the company supplies the

property and is been registered in respect of the GST purposes, its sale might be :

Taxable- City sky would been liable for the GST on sale and could claim credits on the

GST for the land purchased by the company or importing for the purpose of sale.

GST- Free- City sky would not be liable for paying GST on sale of its apartments, but

could claim for input tax credit for buying a vacant land.

Input taxed- Under this, the company is not liable for the goods and services tax as well

as cannot claim credits relating to purchase and import of land for making sale.

In accordance with Australian taxation law, a company can claim for the ITC in case if it

is purchasing a property or the land for an enterprise under the standard land contract, provided

that the amount of GST is been included in sales price. Such credit can be claimed on the activity

statement for the period of tax at the time when the settlement occurs but there are some

exception where an entity cannot claim for the GST credits such as:

the company is not registered for the GST at times of purchasing the property or the land

an entity had only paid for deposit under the contract of standard land

Purchasing existing residence

purchased the property for the purpose of private sale

constructing or purchasing the new residential property for the rental purposes

buying property as a part of free- GST supply of the going concern or the free-farmland

GST

Purchasing the land under a margin scheme

Have purchase a residential premises like room, apartment or the unit is been leased to

business and then supplied as the hotel accommodation in addition with all the other

facilities.

As per the relevant laws and guidelines provided by Australian Taxation Office as regards the

GST City Sky can claim input tax credit for the professional services that are undertaken by it

related to the purchase of vacant land. The land has been purchased by company for building

2

Application

As City Sky Company is the development firm and makes investment in the property so

the main GST consequences that applies to this company involves if the company supplies the

property and is been registered in respect of the GST purposes, its sale might be :

Taxable- City sky would been liable for the GST on sale and could claim credits on the

GST for the land purchased by the company or importing for the purpose of sale.

GST- Free- City sky would not be liable for paying GST on sale of its apartments, but

could claim for input tax credit for buying a vacant land.

Input taxed- Under this, the company is not liable for the goods and services tax as well

as cannot claim credits relating to purchase and import of land for making sale.

In accordance with Australian taxation law, a company can claim for the ITC in case if it

is purchasing a property or the land for an enterprise under the standard land contract, provided

that the amount of GST is been included in sales price. Such credit can be claimed on the activity

statement for the period of tax at the time when the settlement occurs but there are some

exception where an entity cannot claim for the GST credits such as:

the company is not registered for the GST at times of purchasing the property or the land

an entity had only paid for deposit under the contract of standard land

Purchasing existing residence

purchased the property for the purpose of private sale

constructing or purchasing the new residential property for the rental purposes

buying property as a part of free- GST supply of the going concern or the free-farmland

GST

Purchasing the land under a margin scheme

Have purchase a residential premises like room, apartment or the unit is been leased to

business and then supplied as the hotel accommodation in addition with all the other

facilities.

As per the relevant laws and guidelines provided by Australian Taxation Office as regards the

GST City Sky can claim input tax credit for the professional services that are undertaken by it

related to the purchase of vacant land. The land has been purchased by company for building

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

apartments for resale as it is their business to develop and sell apartments. Services of lawyer

relates to professional service amounting to $ 33000 for providing guidance for development.

Therefore, as City Sky Co. is registered entity so it will regarded as eligible in respect of

availing input tax credit as it is purchasing the land for building apartments and then selling the

apartments for earning profit.

Conclusion

After carrying out the research regarding the GST and the input tax credit that can be

claimed by company it is concluded that input tax credit is available for purchase of goods

related to business. In the present case company has purchased vacant land in Brisbane that will

be used by it for constructing apartments for sale. The company is a real state investor and

developer therefore the cost that are related to the construction of apartments are allowed for

GST input tax credits. Since the services of lawyer were undertaken by company for the

development related purpose of the apartments it will included in the sale price of apartments.

Company has paid $ 33000 for the service and the lawyer is having annual turnover of $ 300000

which means he is falling under the GST regime and must have registered itself under the GST

laws. It is assumed that Lawyer is registered GST service provider and has provided invoice

inclusive of GST charges. Company will only be able to claim input tax credit for the

professional service if the supplier has provided invoice inclusive of GST. The company will

avail the GST credit on the fees of $ 33000 at the time of payments for GST. Building of

apartments for resale is the business of City Sky and the service was incurred by company for

the development work related to its business therefore input credit will be availed.

3

relates to professional service amounting to $ 33000 for providing guidance for development.

Therefore, as City Sky Co. is registered entity so it will regarded as eligible in respect of

availing input tax credit as it is purchasing the land for building apartments and then selling the

apartments for earning profit.

Conclusion

After carrying out the research regarding the GST and the input tax credit that can be

claimed by company it is concluded that input tax credit is available for purchase of goods

related to business. In the present case company has purchased vacant land in Brisbane that will

be used by it for constructing apartments for sale. The company is a real state investor and

developer therefore the cost that are related to the construction of apartments are allowed for

GST input tax credits. Since the services of lawyer were undertaken by company for the

development related purpose of the apartments it will included in the sale price of apartments.

Company has paid $ 33000 for the service and the lawyer is having annual turnover of $ 300000

which means he is falling under the GST regime and must have registered itself under the GST

laws. It is assumed that Lawyer is registered GST service provider and has provided invoice

inclusive of GST charges. Company will only be able to claim input tax credit for the

professional service if the supplier has provided invoice inclusive of GST. The company will

avail the GST credit on the fees of $ 33000 at the time of payments for GST. Building of

apartments for resale is the business of City Sky and the service was incurred by company for

the development work related to its business therefore input credit will be availed.

3

QUESTION 2

In the above question the case is about purchase of land. The land is sold by Emma for $

1000000. Land was purchased by her in year 1991 for $ 250000 including stamp duty of $5000

and legal fees of $ 10000. Loan was also taken by her for purchase on which interest amounted

to $32000. During the ownership period amount totalling $22000 was paid for council, water

rates & insurance. Legal fees amounting $ 5000 was incurred for resolving dispute with

neighbour over use of land. $ 27500 were spent by her for removing the large number of pine

trees from the land. Advertisement expense of $ 25000 was incurred for promoting the sale o f

land

Rule

Income Tax Assessment Act, 1997

Act covers the treatment and effect on sale and purchase of land. Income tax act gives the rules

and instructions regarding sale and purchase of land (Tran, 2015). The act lays down all the

provisions to deal with the different cases. Income tax return of individuals are prepared on the

basis of this law (Richardson, Taylor and Lanis, 2015).Sale of land is subject to capital gain tax

if it is considered as capital asset at time of sale.

On sale of capital asset there is generally capital loss or gain (O'Connor and Strauch, 2018).

Capital gain tax is difference between the cost of acquisition and the proceeds received on sale of

asset. Capital gains are to be reported in income tax returns and is not separately taxed. Capital

gain on sale of asset is charged at rates (Brandon, 2019). Capital loss cannot be claimed against

other income but can be used against capital gain. Assets acquired after September 20, 1985 are

subjected to capital gain tax unless excluded specifically.

Incidental cost for acquiring the CGT asset includes company the other cost incurred on

CGT asset includes remuneration for services rendered by valuer, surveyor, broker, consultant or

legal advisor , transferring costs, stamp duty, advertising or marketing cost for finding buyer/

seller, valuation cost and borrowing expenses (Freebairn, 2016). These costs cannot be

included for assets acquired before August 21, 1991. Costs related to ownership include land

taxes, rates, repairs and insurance premiums.

Provisions are provided for the sale of shares are same as that applies to real estate. The

sale of shares are covered under capital gain tax (Trezise, 2018). Shares held for long will

attract capital gain tax.

In the above question the case is about purchase of land. The land is sold by Emma for $

1000000. Land was purchased by her in year 1991 for $ 250000 including stamp duty of $5000

and legal fees of $ 10000. Loan was also taken by her for purchase on which interest amounted

to $32000. During the ownership period amount totalling $22000 was paid for council, water

rates & insurance. Legal fees amounting $ 5000 was incurred for resolving dispute with

neighbour over use of land. $ 27500 were spent by her for removing the large number of pine

trees from the land. Advertisement expense of $ 25000 was incurred for promoting the sale o f

land

Rule

Income Tax Assessment Act, 1997

Act covers the treatment and effect on sale and purchase of land. Income tax act gives the rules

and instructions regarding sale and purchase of land (Tran, 2015). The act lays down all the

provisions to deal with the different cases. Income tax return of individuals are prepared on the

basis of this law (Richardson, Taylor and Lanis, 2015).Sale of land is subject to capital gain tax

if it is considered as capital asset at time of sale.

On sale of capital asset there is generally capital loss or gain (O'Connor and Strauch, 2018).

Capital gain tax is difference between the cost of acquisition and the proceeds received on sale of

asset. Capital gains are to be reported in income tax returns and is not separately taxed. Capital

gain on sale of asset is charged at rates (Brandon, 2019). Capital loss cannot be claimed against

other income but can be used against capital gain. Assets acquired after September 20, 1985 are

subjected to capital gain tax unless excluded specifically.

Incidental cost for acquiring the CGT asset includes company the other cost incurred on

CGT asset includes remuneration for services rendered by valuer, surveyor, broker, consultant or

legal advisor , transferring costs, stamp duty, advertising or marketing cost for finding buyer/

seller, valuation cost and borrowing expenses (Freebairn, 2016). These costs cannot be

included for assets acquired before August 21, 1991. Costs related to ownership include land

taxes, rates, repairs and insurance premiums.

Provisions are provided for the sale of shares are same as that applies to real estate. The

sale of shares are covered under capital gain tax (Trezise, 2018). Shares held for long will

attract capital gain tax.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Stamp duty collection is collection of tax on transactions and written documents. They

are imposed on by territory and state governments. Stamp duties are generally collected on

transactions including motor vehicles, leases and mortgages, insurance companies, hire purchase

agreements and property transfers (Blunden, 2016). Sale of stamp collection will attract tax

provisions as if they were purchased with the motive of resale.

The tax provisions provide for the treatment of different transactions incurred by

individuals. Tax return is prepared on the basis of Income Tax Assessment Act, 1997.

Deductions are available for different transactions incurred by the individual during the year.

Interest paid on loan for purchasing the home are allowed for deductions (Roy, 2018). Law has

given criteria for claiming deductions and for identifying which transactions are deductible and

which are not .

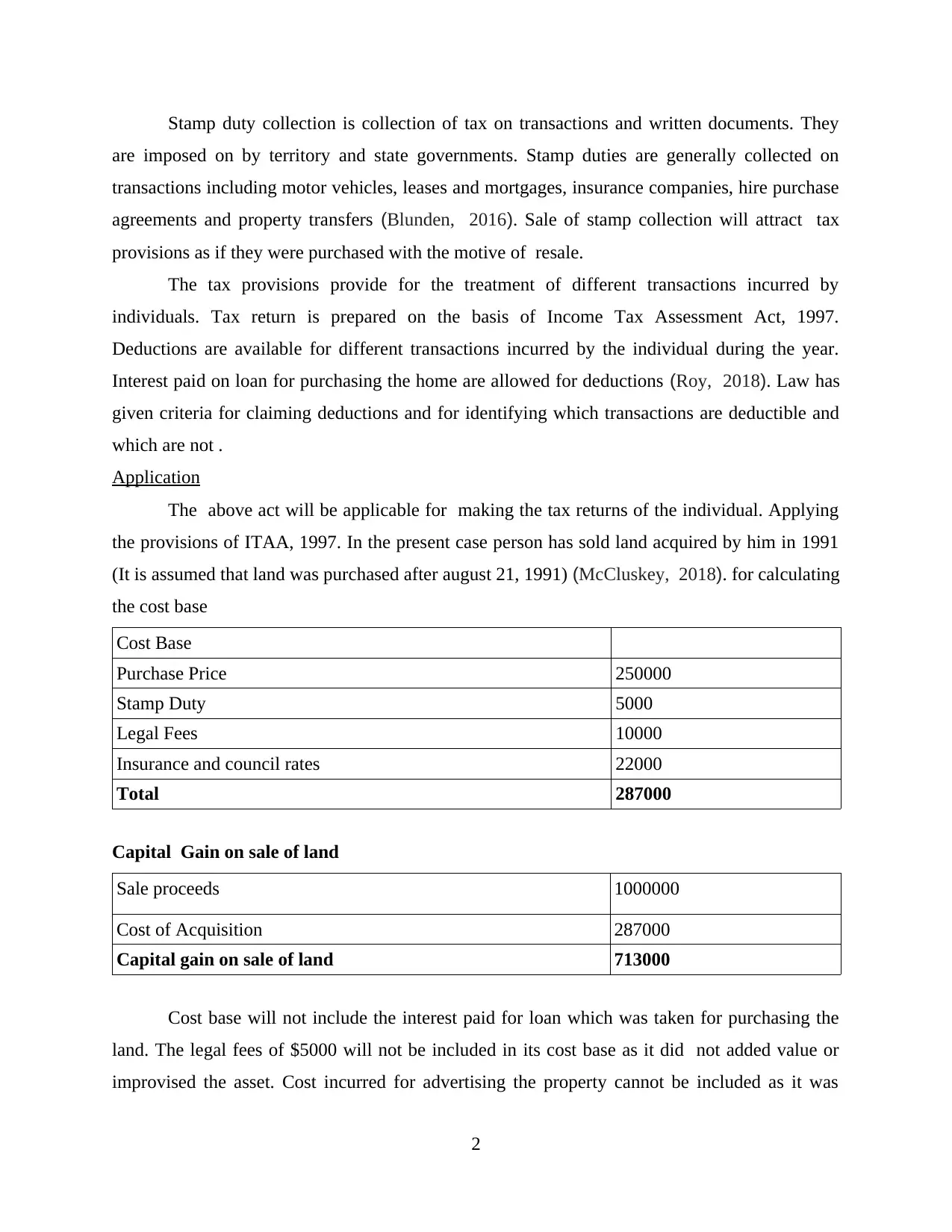

Application

The above act will be applicable for making the tax returns of the individual. Applying

the provisions of ITAA, 1997. In the present case person has sold land acquired by him in 1991

(It is assumed that land was purchased after august 21, 1991) (McCluskey, 2018). for calculating

the cost base

Cost Base

Purchase Price 250000

Stamp Duty 5000

Legal Fees 10000

Insurance and council rates 22000

Total 287000

Capital Gain on sale of land

Sale proceeds 1000000

Cost of Acquisition 287000

Capital gain on sale of land 713000

Cost base will not include the interest paid for loan which was taken for purchasing the

land. The legal fees of $5000 will not be included in its cost base as it did not added value or

improvised the asset. Cost incurred for advertising the property cannot be included as it was

2

are imposed on by territory and state governments. Stamp duties are generally collected on

transactions including motor vehicles, leases and mortgages, insurance companies, hire purchase

agreements and property transfers (Blunden, 2016). Sale of stamp collection will attract tax

provisions as if they were purchased with the motive of resale.

The tax provisions provide for the treatment of different transactions incurred by

individuals. Tax return is prepared on the basis of Income Tax Assessment Act, 1997.

Deductions are available for different transactions incurred by the individual during the year.

Interest paid on loan for purchasing the home are allowed for deductions (Roy, 2018). Law has

given criteria for claiming deductions and for identifying which transactions are deductible and

which are not .

Application

The above act will be applicable for making the tax returns of the individual. Applying

the provisions of ITAA, 1997. In the present case person has sold land acquired by him in 1991

(It is assumed that land was purchased after august 21, 1991) (McCluskey, 2018). for calculating

the cost base

Cost Base

Purchase Price 250000

Stamp Duty 5000

Legal Fees 10000

Insurance and council rates 22000

Total 287000

Capital Gain on sale of land

Sale proceeds 1000000

Cost of Acquisition 287000

Capital gain on sale of land 713000

Cost base will not include the interest paid for loan which was taken for purchasing the

land. The legal fees of $5000 will not be included in its cost base as it did not added value or

improvised the asset. Cost incurred for advertising the property cannot be included as it was

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

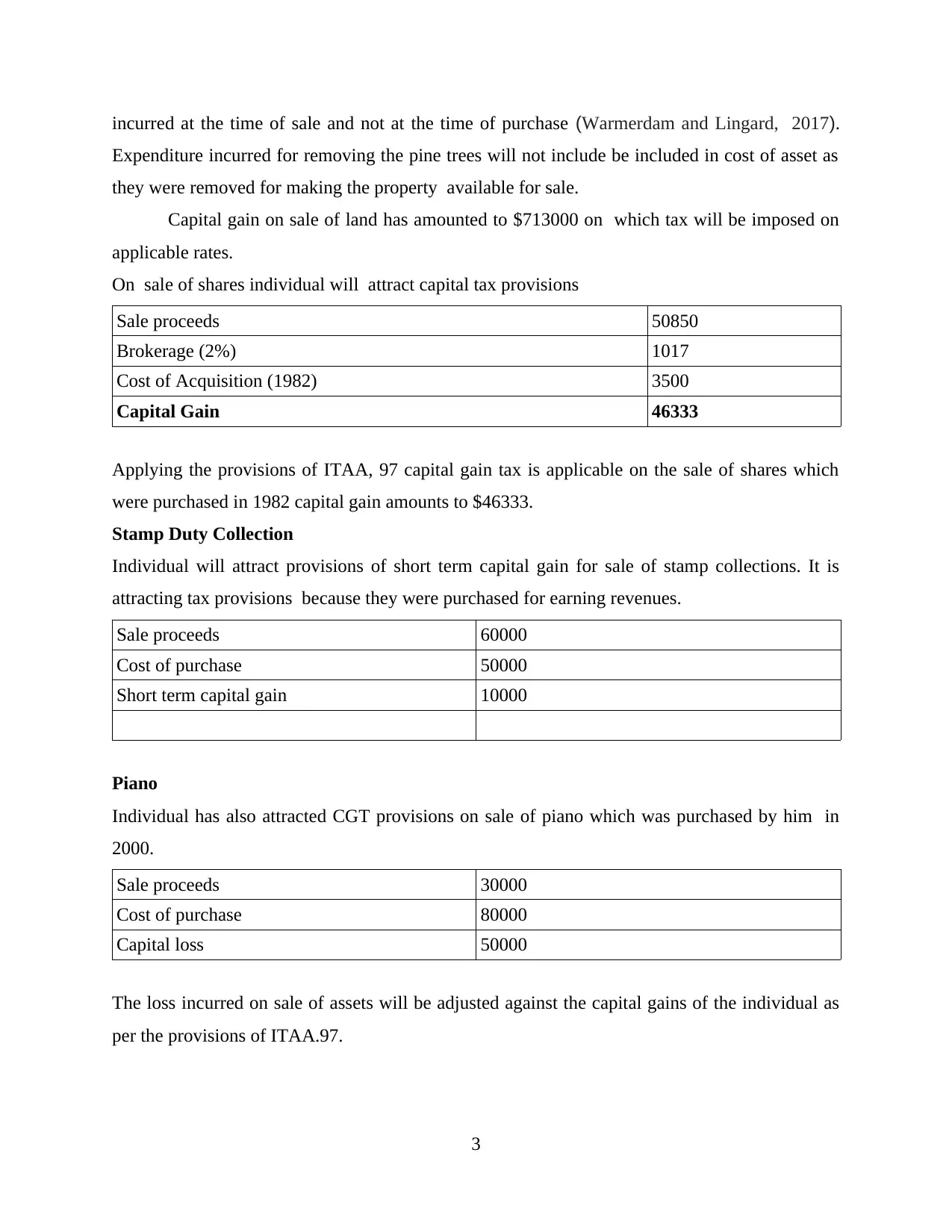

incurred at the time of sale and not at the time of purchase (Warmerdam and Lingard, 2017).

Expenditure incurred for removing the pine trees will not include be included in cost of asset as

they were removed for making the property available for sale.

Capital gain on sale of land has amounted to $713000 on which tax will be imposed on

applicable rates.

On sale of shares individual will attract capital tax provisions

Sale proceeds 50850

Brokerage (2%) 1017

Cost of Acquisition (1982) 3500

Capital Gain 46333

Applying the provisions of ITAA, 97 capital gain tax is applicable on the sale of shares which

were purchased in 1982 capital gain amounts to $46333.

Stamp Duty Collection

Individual will attract provisions of short term capital gain for sale of stamp collections. It is

attracting tax provisions because they were purchased for earning revenues.

Sale proceeds 60000

Cost of purchase 50000

Short term capital gain 10000

Piano

Individual has also attracted CGT provisions on sale of piano which was purchased by him in

2000.

Sale proceeds 30000

Cost of purchase 80000

Capital loss 50000

The loss incurred on sale of assets will be adjusted against the capital gains of the individual as

per the provisions of ITAA.97.

3

Expenditure incurred for removing the pine trees will not include be included in cost of asset as

they were removed for making the property available for sale.

Capital gain on sale of land has amounted to $713000 on which tax will be imposed on

applicable rates.

On sale of shares individual will attract capital tax provisions

Sale proceeds 50850

Brokerage (2%) 1017

Cost of Acquisition (1982) 3500

Capital Gain 46333

Applying the provisions of ITAA, 97 capital gain tax is applicable on the sale of shares which

were purchased in 1982 capital gain amounts to $46333.

Stamp Duty Collection

Individual will attract provisions of short term capital gain for sale of stamp collections. It is

attracting tax provisions because they were purchased for earning revenues.

Sale proceeds 60000

Cost of purchase 50000

Short term capital gain 10000

Piano

Individual has also attracted CGT provisions on sale of piano which was purchased by him in

2000.

Sale proceeds 30000

Cost of purchase 80000

Capital loss 50000

The loss incurred on sale of assets will be adjusted against the capital gains of the individual as

per the provisions of ITAA.97.

3

Conclusions

From the above study it is concluded that for capital gains there are tax provisions given

in Income Tax Assessment Act, 1997. As per the provisions capital gain tax will be charged by

government on all the assets that have been sold by company and have generated significant

revenues for the individual (Richardson, Taylor and Lanis, 2015). The capital gains will be

included in the tax returns and will become part of assessable income. Individual has to pay tax

as per the applicable rates provided by the Act.

4

From the above study it is concluded that for capital gains there are tax provisions given

in Income Tax Assessment Act, 1997. As per the provisions capital gain tax will be charged by

government on all the assets that have been sold by company and have generated significant

revenues for the individual (Richardson, Taylor and Lanis, 2015). The capital gains will be

included in the tax returns and will become part of assessable income. Individual has to pay tax

as per the applicable rates provided by the Act.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

O'Connor, A. and Strauch, M., 2018. New GST payment obligations for residential property

transactions. Taxation in Australia. 52(9). p.507.

Brandon, G., 2019. Who has a liability to pay GST?. Taxation in Australia. 53(7). p.357.

Trezise, J., 2018. It's broken, so let's fix it: Seeking a new generation of laws. Habitat

Australia. 46(1). p.16.

Roy, S., 2018. Transition to goods and services tax (GST) regime: rationale and impasse.

Warmerdam, A. and Lingard, H., 2017, June. EXAMINING THE DEFINITION OF A

CONSTRUCTION PROJECT IN AUSTRALIA. In Joint CIB W099 & TG59 International

Safety, Health, and People in Construction Conference. (p. 242).

McGregor-Lowndes, M., 2018. Country Report 2018: Australia.

McCluskey, W., 2018. Property tax: An international comparative review. Routledge.

Blunden, H., 2016. Discourses around negative gearing of investment properties in

Australia. Housing Studies. 31(3). pp.340-357.

Freebairn, J., 2016. Taxation of housing. Australian Economic Review.49(3). pp.307-316.

Tran, A., 2015. Can taxable income be estimated from financial reports of listed companies in

Australia. Austl. Tax F.. 30. p.569.

Richardson, G., Taylor, G. and Lanis, R., 2015. The impact of financial distress on corporate tax

avoidance spanning the global financial crisis: Evidence from Australia. Economic

Modelling. 44. pp.44-53.

Devos, K. and Zackrisson, M., 2015. Tax compliance and the public disclosure of tax

information: An Australia/Norway comparison. EJTR. 13. p.108.

Castelyn, D., Hodgson, H. and Marriott, L., 2019, May. Income equalisation: is all fair in

primary production and tax law?. In Australian Tax Forum. (Vol. 34, No. 2).

Online

Claiming GST credits. 2019.[Online]. Available through :

<https://www.ato.gov.au/Business/GST/Claiming-GST-credits/>.

5

Books and Journals

O'Connor, A. and Strauch, M., 2018. New GST payment obligations for residential property

transactions. Taxation in Australia. 52(9). p.507.

Brandon, G., 2019. Who has a liability to pay GST?. Taxation in Australia. 53(7). p.357.

Trezise, J., 2018. It's broken, so let's fix it: Seeking a new generation of laws. Habitat

Australia. 46(1). p.16.

Roy, S., 2018. Transition to goods and services tax (GST) regime: rationale and impasse.

Warmerdam, A. and Lingard, H., 2017, June. EXAMINING THE DEFINITION OF A

CONSTRUCTION PROJECT IN AUSTRALIA. In Joint CIB W099 & TG59 International

Safety, Health, and People in Construction Conference. (p. 242).

McGregor-Lowndes, M., 2018. Country Report 2018: Australia.

McCluskey, W., 2018. Property tax: An international comparative review. Routledge.

Blunden, H., 2016. Discourses around negative gearing of investment properties in

Australia. Housing Studies. 31(3). pp.340-357.

Freebairn, J., 2016. Taxation of housing. Australian Economic Review.49(3). pp.307-316.

Tran, A., 2015. Can taxable income be estimated from financial reports of listed companies in

Australia. Austl. Tax F.. 30. p.569.

Richardson, G., Taylor, G. and Lanis, R., 2015. The impact of financial distress on corporate tax

avoidance spanning the global financial crisis: Evidence from Australia. Economic

Modelling. 44. pp.44-53.

Devos, K. and Zackrisson, M., 2015. Tax compliance and the public disclosure of tax

information: An Australia/Norway comparison. EJTR. 13. p.108.

Castelyn, D., Hodgson, H. and Marriott, L., 2019, May. Income equalisation: is all fair in

primary production and tax law?. In Australian Tax Forum. (Vol. 34, No. 2).

Online

Claiming GST credits. 2019.[Online]. Available through :

<https://www.ato.gov.au/Business/GST/Claiming-GST-credits/>.

5

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.