HI6028 Taxation Theory, Practice and Law: Tutorial Questions Analysis

VerifiedAdded on 2023/01/10

|8

|2028

|75

Homework Assignment

AI Summary

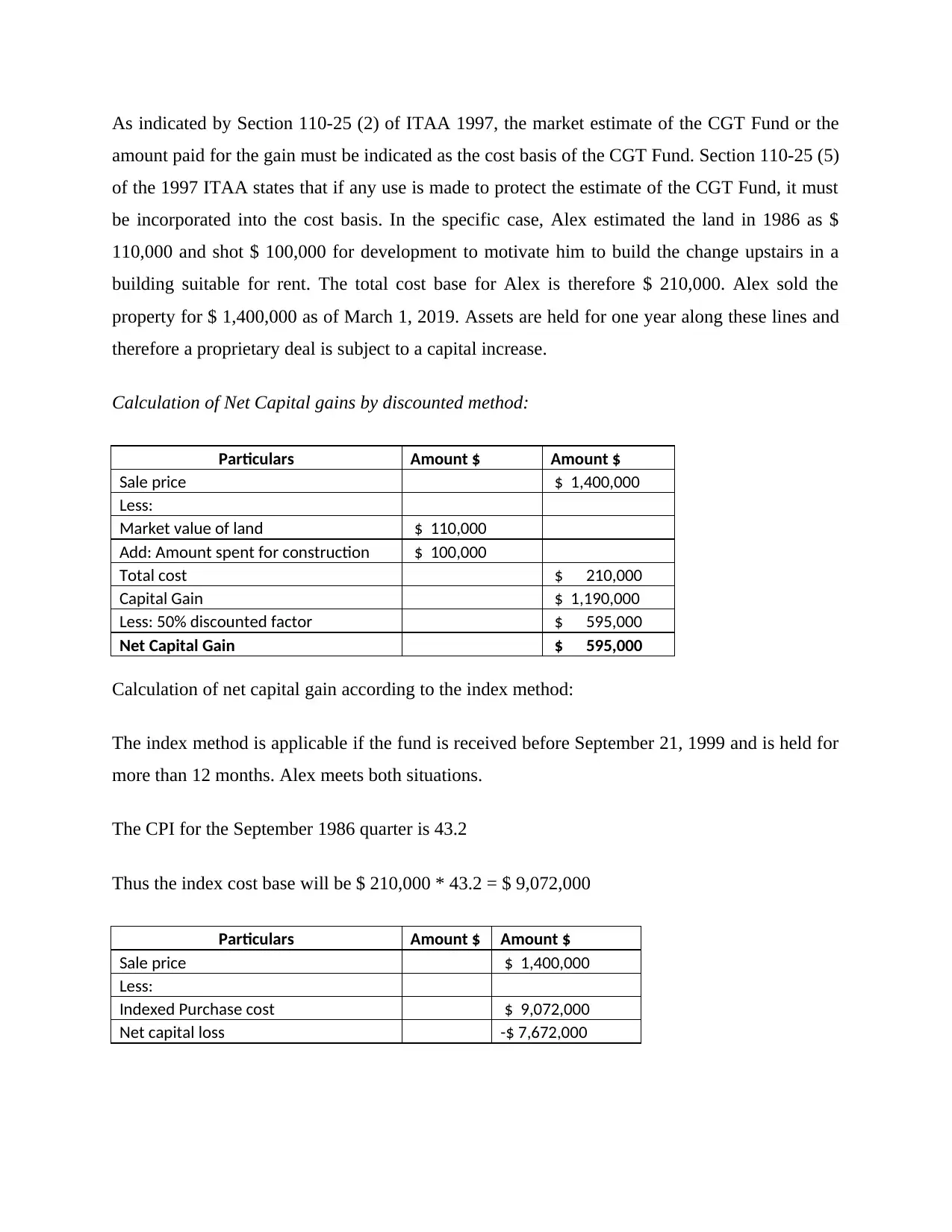

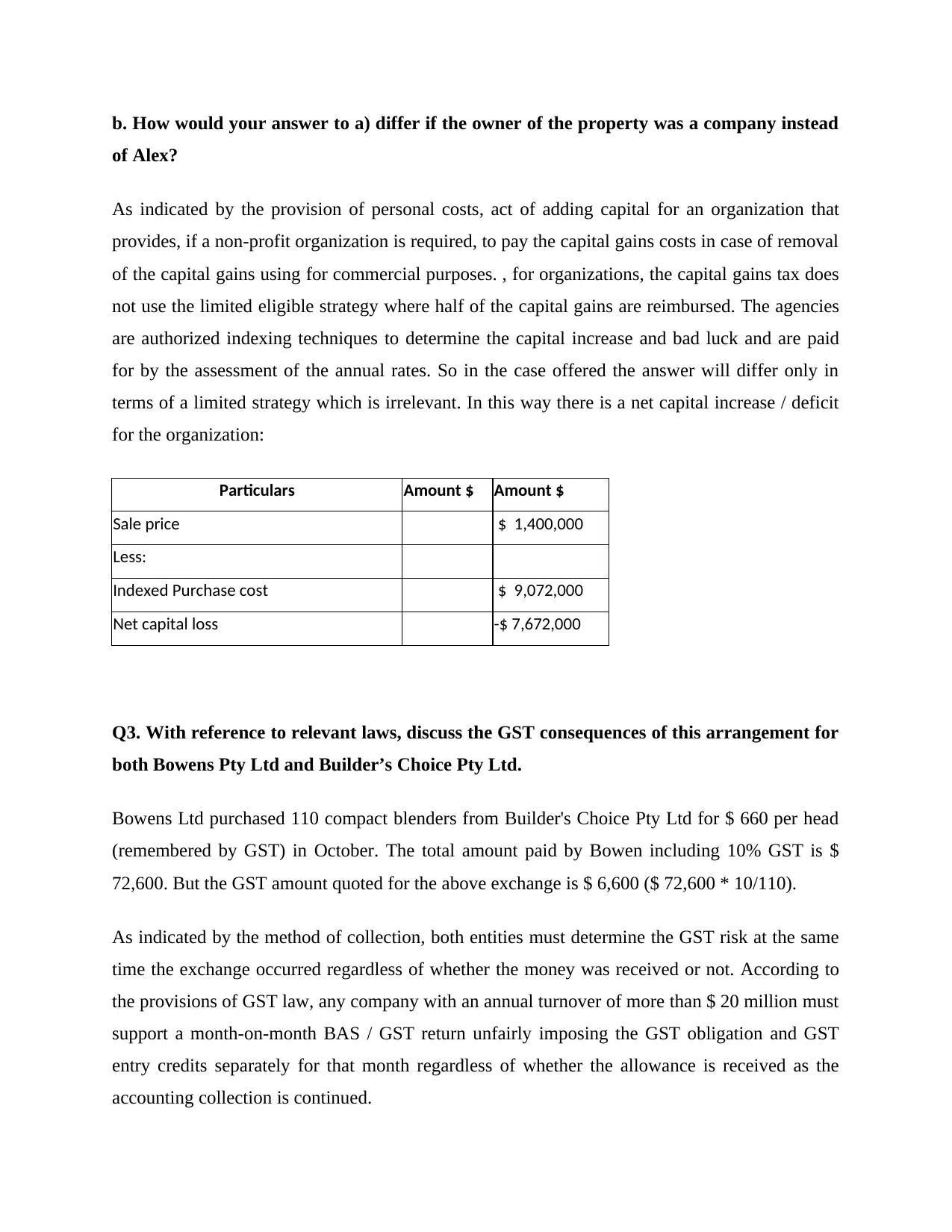

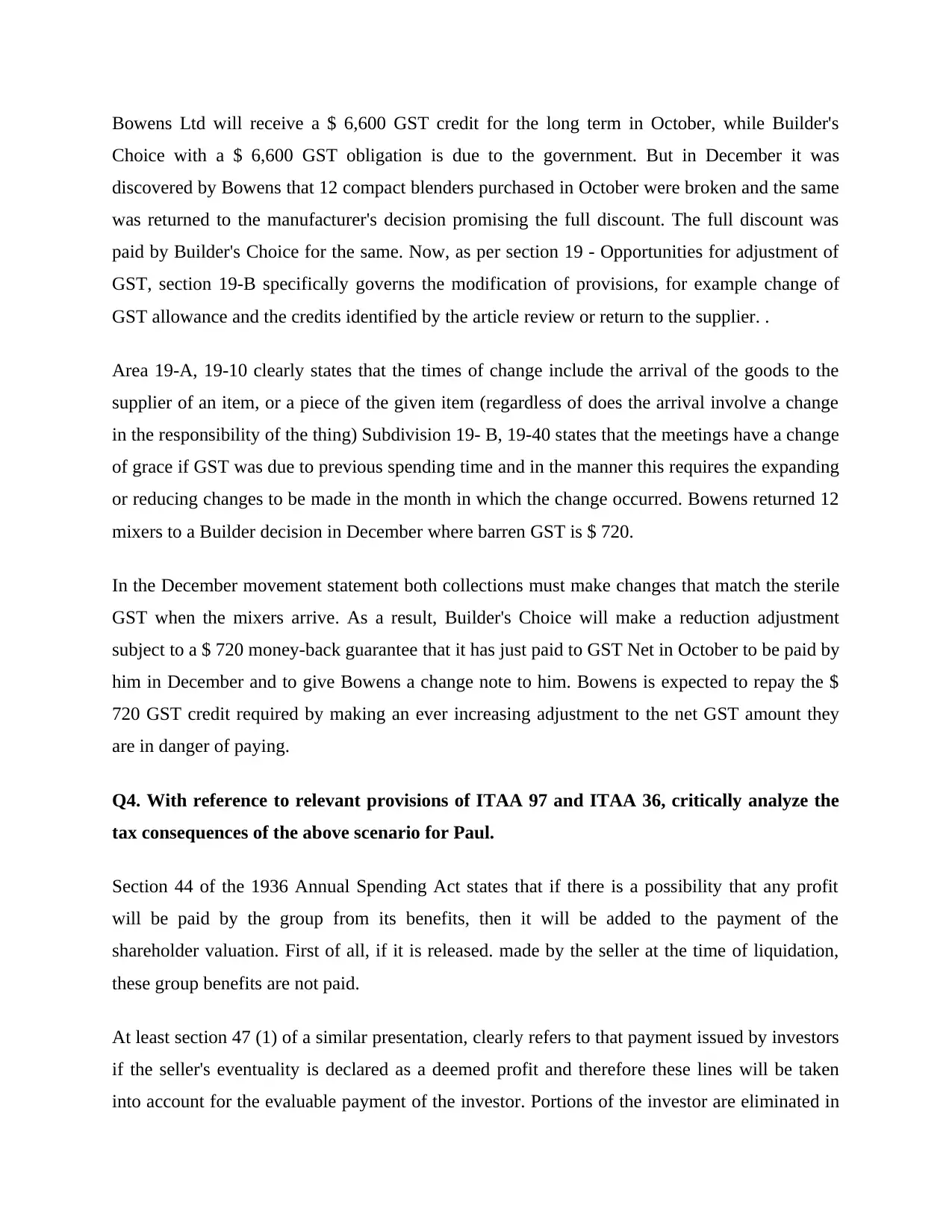

This assignment addresses several key areas of Australian taxation law. It begins by analyzing the Fringe Benefits Tax (FBT) consequences of an employee's remuneration package, including the calculation of FBT payable and strategies to minimize it. The assignment then delves into Capital Gains Tax (CGT), calculating net capital gains using both the discounted and indexation methods, and comparing the outcomes for an individual versus a company. The Goods and Services Tax (GST) implications of a transaction between two companies are examined, focusing on adjustments for returned goods. Finally, the assignment analyzes the tax consequences for a shareholder receiving distributions from a company, referencing relevant provisions of the Income Tax Assessment Acts (ITAA) 1997 and 1936, and discusses the taxation of partnership income, considering the tax obligations of both resident and non-resident partners.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.