Taxation Theory, Practice & Law Report - Finance Module, University X

VerifiedAdded on 2023/01/07

|9

|2540

|75

Report

AI Summary

This report provides a comprehensive analysis of taxation theory, practice, and law, focusing on fringe benefits tax (FBT) and capital gains tax (CGT) within the Australian context. It begins with an introduction to taxation and the Goods and Services Tax (GST), then delves into the calculation of FBT, including the valuation of a company car. The report then explores the legal framework of taxation in Australia, referencing key legislation such as the Income Tax Assessment Act (ITAA) and the Fringe Benefits Tax Act. The second part of the report addresses CGT, explaining its application to various asset sales, including an antique painting, a car, a Harry Potter collection, a gold necklace, and a sculpture. The report calculates the capital gains for each asset and provides an overview of CGT regulations, including long-term capital gains, indexation, and tax deductions. The conclusion summarizes the key aspects of FBT and CGT, highlighting their implications for taxpayers.

Taxation Theory,

Practice & Law

Practice & Law

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question 1...............................................................................................................................3

QUESTION 2...................................................................................................................................5

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question 1...............................................................................................................................3

QUESTION 2...................................................................................................................................5

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Taxation seems to be the process through which the governing body or legislature

implements or surcharges a tax over its residents and corporate organisations. Tax avoidance

includes every aspect, from payroll taxes to value added tax and also GST (Tang, 2016). The

legislation of the centre and states plays an important part in deciding the taxation in every

country. During the last few decades, the centre and local governments have implemented

numerous new policies to simplify the taxation system and enhance accountability within the

country. One such reform was the Goods and Services Tax (GST) which loosened the

government's tax framework on the selling and distribution of goods. In this report, Fringe

Benefits Tax Liability and Capital Gain Tax Consequences are calculated for the respected

parties.

MAIN BODY

Question 1

Fringe benefit tax shall be levied by the contractor in view of the extra compensation that

perhaps the employer must offer to the worker. This fee, regardless of income fee responsibility,

is a duty owed by the company. (FBT) is, in effect, a fee levied by an employer in lieu of the

wages offered to its workers. This was an effort to impose the tax on certain assets in full, which

managed to evade the tax authorities. The list of advantages included a huge spectrum of

advantages, services, facilities or conveniences that a company gave intentionally or

unintentionally to former employees, whether through things straightforward like mobile phone

payments, unlimited or concessional bookings and even pension payments to a pension fund.

There have been explicitly written out some rules on what fell into the fringe benefits umbrella.

For example, spending on drinks and snacks made by an organization to its workers, fees

charged for employee attendance at conventions or any expense paid by the firm in meeting the

government's duty to workers was exempt from this framework.

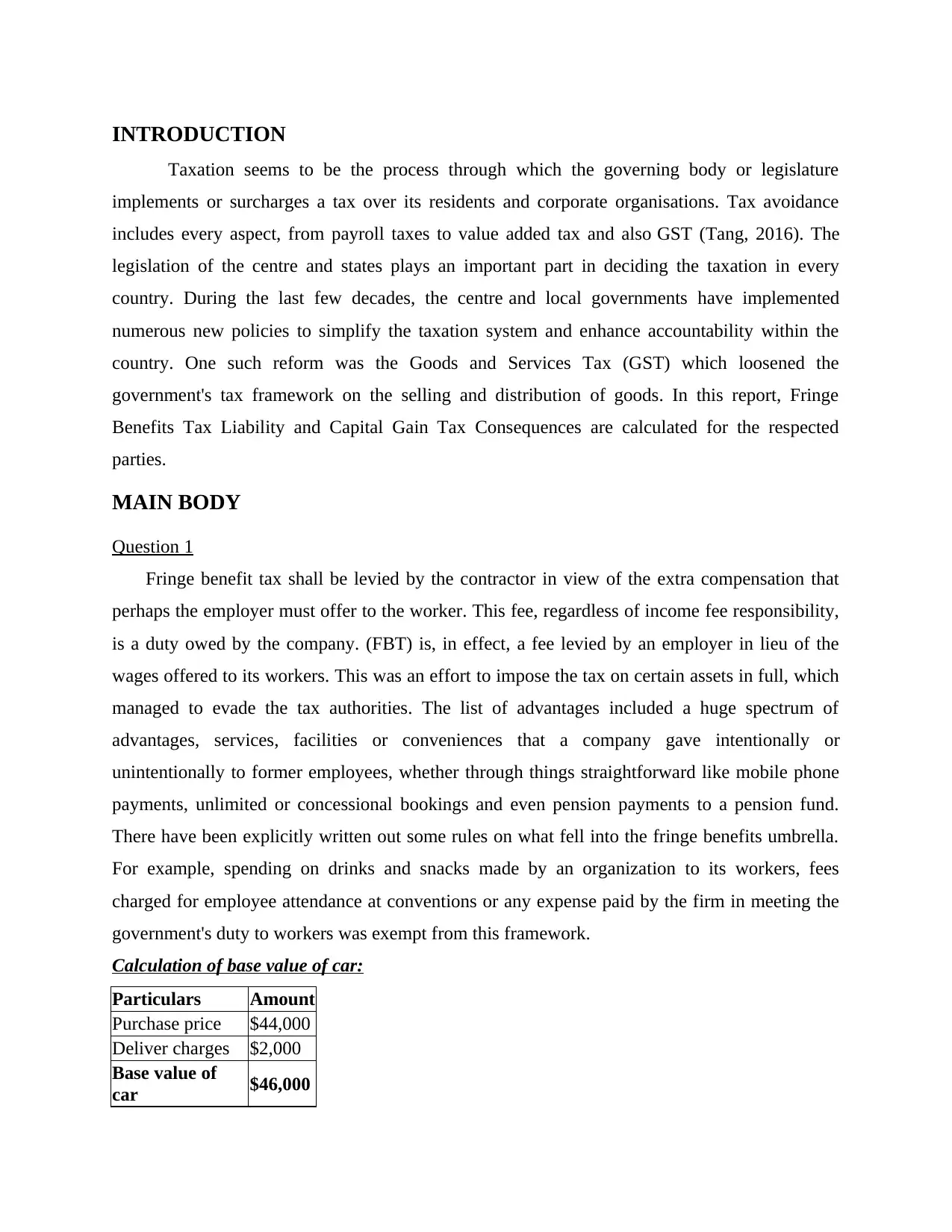

Calculation of base value of car:

Particulars Amount

Purchase price $44,000

Deliver charges $2,000

Base value of

car $46,000

Taxation seems to be the process through which the governing body or legislature

implements or surcharges a tax over its residents and corporate organisations. Tax avoidance

includes every aspect, from payroll taxes to value added tax and also GST (Tang, 2016). The

legislation of the centre and states plays an important part in deciding the taxation in every

country. During the last few decades, the centre and local governments have implemented

numerous new policies to simplify the taxation system and enhance accountability within the

country. One such reform was the Goods and Services Tax (GST) which loosened the

government's tax framework on the selling and distribution of goods. In this report, Fringe

Benefits Tax Liability and Capital Gain Tax Consequences are calculated for the respected

parties.

MAIN BODY

Question 1

Fringe benefit tax shall be levied by the contractor in view of the extra compensation that

perhaps the employer must offer to the worker. This fee, regardless of income fee responsibility,

is a duty owed by the company. (FBT) is, in effect, a fee levied by an employer in lieu of the

wages offered to its workers. This was an effort to impose the tax on certain assets in full, which

managed to evade the tax authorities. The list of advantages included a huge spectrum of

advantages, services, facilities or conveniences that a company gave intentionally or

unintentionally to former employees, whether through things straightforward like mobile phone

payments, unlimited or concessional bookings and even pension payments to a pension fund.

There have been explicitly written out some rules on what fell into the fringe benefits umbrella.

For example, spending on drinks and snacks made by an organization to its workers, fees

charged for employee attendance at conventions or any expense paid by the firm in meeting the

government's duty to workers was exempt from this framework.

Calculation of base value of car:

Particulars Amount

Purchase price $44,000

Deliver charges $2,000

Base value of

car $46,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Amount of days on which the company provides compensation from 1May 2019 to 31March

2020= 304 days

Fringe profits are valued at 30% @

Measurement of the maximum payable for the fringe benefits:

Taxable amount: 20% * Base value of car * Number of days of benefit / 365 days – Expenses

incurred

= 20% * $ 46000 * 304 / 365 -$ 770

= $ 6, 892.46

Information relating to 55 including its Australian Constitution, the union government shall

guarantee that tax rules always deal with taxation and deals through one issue only (O’Connell,

2017). As a consequence, several laws exist at the regional level, each implementing and

controlling one type of tax-e.g. income tax , excise duty, import taxes, service tax, fringe benefits

tax, luxury vehicle tax, liquor redistribution tax as well as other payroll taxes. Within each tax

issue, there is generally an obligation law (which determines the tax liability), a rate law (which

defines the tax rate) and an evaluation law (which includes the guidelines for deciding what is

taxable and estimating the tax payable). The high renaissance Actions (the references below will

direct access to the executive authority Registry of Laws website open access law) are concerned

with:

Collection of income tax for persons and corporations: The income tax act 1936 (ITAA

1936) as well as the assessment Act 1997 (ITAA 1997) as well as the Fringe Benefits yearly tax

Act 1986 are the principal laws. The ITAA of 1997 was initially designed to supplement the

ITAA of 1936 but both Actions are now functioning simultaneously at present. The 1997 ITAA

contains the tax regulations on capital gains, as losses are obtainable revenue. The constitutional

definition of tax rules in Australia is driven by a number of statutory and doctrinal

considerations. While a limited view of the yield benefits, a local economy not accessible under

the Law to individual states, has considerably restricted the ability for states to impose excise

taxes, the statutory taxing authority of the central government has been understood very narrowly

with, in particular, only constitutional restrictions on its use. Through trust law theories and

assumptions resulting in a limited view of the income tax burden and a strange differentiation

among capital and sales spending that also only slightly aligned with the standard income tax

concepts. Assessment of the goods and services tax (GST) as a company tax instead of a tax on

2020= 304 days

Fringe profits are valued at 30% @

Measurement of the maximum payable for the fringe benefits:

Taxable amount: 20% * Base value of car * Number of days of benefit / 365 days – Expenses

incurred

= 20% * $ 46000 * 304 / 365 -$ 770

= $ 6, 892.46

Information relating to 55 including its Australian Constitution, the union government shall

guarantee that tax rules always deal with taxation and deals through one issue only (O’Connell,

2017). As a consequence, several laws exist at the regional level, each implementing and

controlling one type of tax-e.g. income tax , excise duty, import taxes, service tax, fringe benefits

tax, luxury vehicle tax, liquor redistribution tax as well as other payroll taxes. Within each tax

issue, there is generally an obligation law (which determines the tax liability), a rate law (which

defines the tax rate) and an evaluation law (which includes the guidelines for deciding what is

taxable and estimating the tax payable). The high renaissance Actions (the references below will

direct access to the executive authority Registry of Laws website open access law) are concerned

with:

Collection of income tax for persons and corporations: The income tax act 1936 (ITAA

1936) as well as the assessment Act 1997 (ITAA 1997) as well as the Fringe Benefits yearly tax

Act 1986 are the principal laws. The ITAA of 1997 was initially designed to supplement the

ITAA of 1936 but both Actions are now functioning simultaneously at present. The 1997 ITAA

contains the tax regulations on capital gains, as losses are obtainable revenue. The constitutional

definition of tax rules in Australia is driven by a number of statutory and doctrinal

considerations. While a limited view of the yield benefits, a local economy not accessible under

the Law to individual states, has considerably restricted the ability for states to impose excise

taxes, the statutory taxing authority of the central government has been understood very narrowly

with, in particular, only constitutional restrictions on its use. Through trust law theories and

assumptions resulting in a limited view of the income tax burden and a strange differentiation

among capital and sales spending that also only slightly aligned with the standard income tax

concepts. Assessment of the goods and services tax (GST) as a company tax instead of a tax on

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

sales has limited the scope of the GST foundation. A purposeful method, therefore, has been

extended to understanding agreements, restricting misuse or accidental manipulation of certain

measures. Treaties were viewed quite narrowly, as is the case with domestic legislation which

overlaps against treaties (Kraal and Kasipillai, 2016). In such cases, judicial rulings favouring

investors have caused legislative initiatives to overturn judiciary definitions of treaty laws

relating to firms interposed among shareholders and real estate and national law dealing

regarding tax avoidance. The right of an individual or dependent to collect pension payments

from a program shall be considered to have expired at a certain time (either during the enactment

of this segment) if, according to the contract terms relevant to the system at a certain time, the

privilege (such as a conditional right) of the individual or dependent on the beneficiary, because

as situation may well be, to an is denied. By moving the sum to some other account wherein the

individual acquires, or state benefits of the individual obtain, as the situation may well be, a

completely-secured right (such as a conditional right) to earn pension scheme benefits on top of

the transition, a benefit which is no less important than the last right listed.

QUESTION 2

Capital Gains Tax could be described as both the taxes that can then be levied mostly on

realizing of benefit by the national government when selling certain types of assets. Typically a

capital gain is represented as the variance between the purchase and disposition costs paid by a

person or an organisation. It is important to remember that CGT is the component of the income

tax laws set out from the Income Tax Assessment Act (ITAA), 1997, like Goods and Service

Tax. Especially, when a capital liability is sustained when some capital asset is disposed of, the

average taxpayer will not assert a CGT on those cases. Capital costs may be removed towards

capital gains in order to derive the net income for each year, if any (Boadway and Tremblay,

2016). However, the equations get more complicated if you have sustained capital gains or losses

through both short-term as well as long-term portfolios. Firstly, all like-kind benefits and losses

need to be linked together. Both short-term losses have to be equated to achieve a cumulative

return in the medium term. Then the gains in the short-term are zero. Lastly, benefits and defeats

over the medium haul are recorded. Of necessity, the capital gains tax essentially decreases the

net return produced also by investment. Yet some owners have a legal means of reducing or even

minimising their net capital gains income for the year (Jones, 2016). The easiest of tactics is to

extended to understanding agreements, restricting misuse or accidental manipulation of certain

measures. Treaties were viewed quite narrowly, as is the case with domestic legislation which

overlaps against treaties (Kraal and Kasipillai, 2016). In such cases, judicial rulings favouring

investors have caused legislative initiatives to overturn judiciary definitions of treaty laws

relating to firms interposed among shareholders and real estate and national law dealing

regarding tax avoidance. The right of an individual or dependent to collect pension payments

from a program shall be considered to have expired at a certain time (either during the enactment

of this segment) if, according to the contract terms relevant to the system at a certain time, the

privilege (such as a conditional right) of the individual or dependent on the beneficiary, because

as situation may well be, to an is denied. By moving the sum to some other account wherein the

individual acquires, or state benefits of the individual obtain, as the situation may well be, a

completely-secured right (such as a conditional right) to earn pension scheme benefits on top of

the transition, a benefit which is no less important than the last right listed.

QUESTION 2

Capital Gains Tax could be described as both the taxes that can then be levied mostly on

realizing of benefit by the national government when selling certain types of assets. Typically a

capital gain is represented as the variance between the purchase and disposition costs paid by a

person or an organisation. It is important to remember that CGT is the component of the income

tax laws set out from the Income Tax Assessment Act (ITAA), 1997, like Goods and Service

Tax. Especially, when a capital liability is sustained when some capital asset is disposed of, the

average taxpayer will not assert a CGT on those cases. Capital costs may be removed towards

capital gains in order to derive the net income for each year, if any (Boadway and Tremblay,

2016). However, the equations get more complicated if you have sustained capital gains or losses

through both short-term as well as long-term portfolios. Firstly, all like-kind benefits and losses

need to be linked together. Both short-term losses have to be equated to achieve a cumulative

return in the medium term. Then the gains in the short-term are zero. Lastly, benefits and defeats

over the medium haul are recorded. Of necessity, the capital gains tax essentially decreases the

net return produced also by investment. Yet some owners have a legal means of reducing or even

minimising their net capital gains income for the year (Jones, 2016). The easiest of tactics is to

get investments kept for longer than it was a year until they are sold. That is smart, since the

long-term capital gains rate users will pay is usually smaller versus short-term gains.

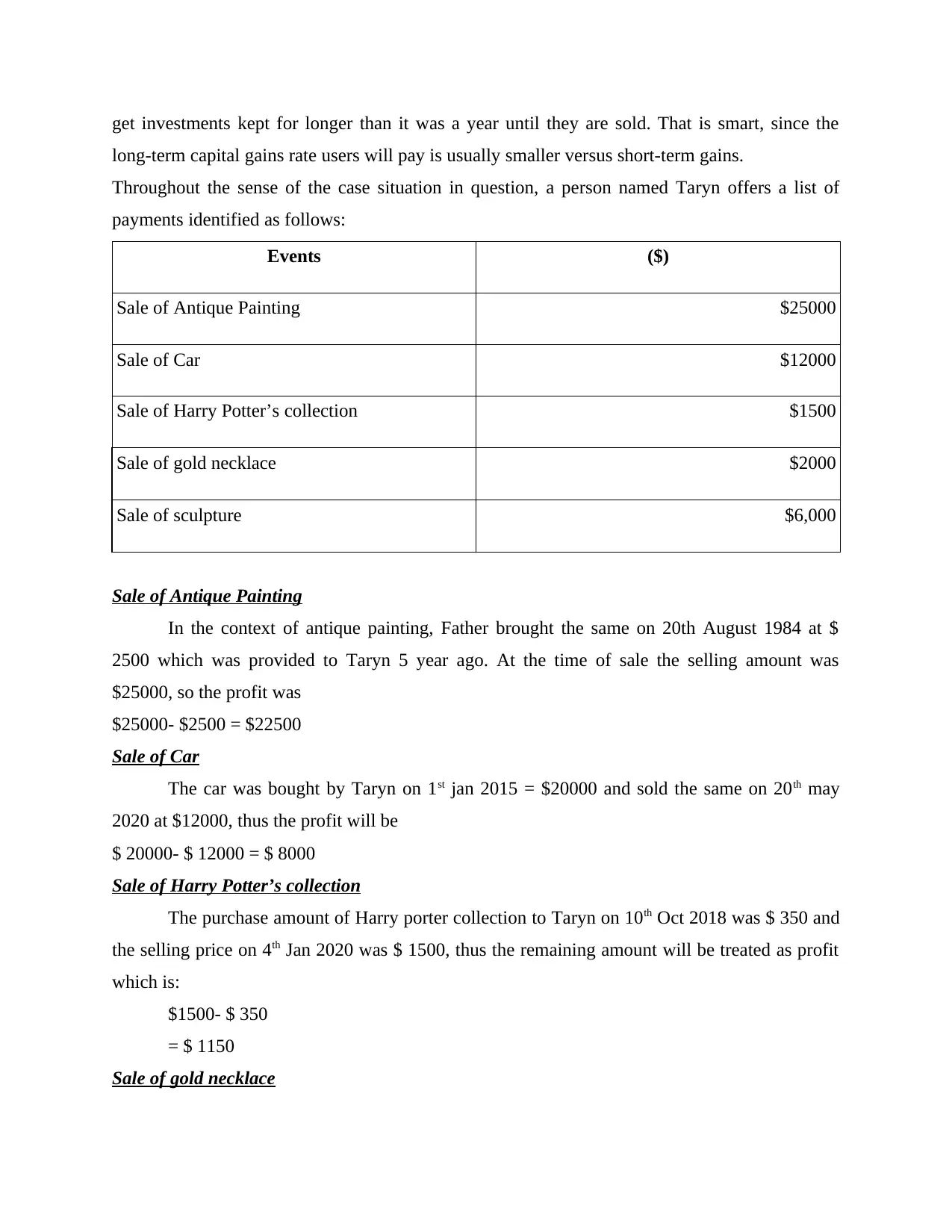

Throughout the sense of the case situation in question, a person named Taryn offers a list of

payments identified as follows:

Events ($)

Sale of Antique Painting $25000

Sale of Car $12000

Sale of Harry Potter’s collection $1500

Sale of gold necklace $2000

Sale of sculpture $6,000

Sale of Antique Painting

In the context of antique painting, Father brought the same on 20th August 1984 at $

2500 which was provided to Taryn 5 year ago. At the time of sale the selling amount was

$25000, so the profit was

$25000- $2500 = $22500

Sale of Car

The car was bought by Taryn on 1st jan 2015 = $20000 and sold the same on 20th may

2020 at $12000, thus the profit will be

$ 20000- $ 12000 = $ 8000

Sale of Harry Potter’s collection

The purchase amount of Harry porter collection to Taryn on 10th Oct 2018 was $ 350 and

the selling price on 4th Jan 2020 was $ 1500, thus the remaining amount will be treated as profit

which is:

$1500- $ 350

= $ 1150

Sale of gold necklace

long-term capital gains rate users will pay is usually smaller versus short-term gains.

Throughout the sense of the case situation in question, a person named Taryn offers a list of

payments identified as follows:

Events ($)

Sale of Antique Painting $25000

Sale of Car $12000

Sale of Harry Potter’s collection $1500

Sale of gold necklace $2000

Sale of sculpture $6,000

Sale of Antique Painting

In the context of antique painting, Father brought the same on 20th August 1984 at $

2500 which was provided to Taryn 5 year ago. At the time of sale the selling amount was

$25000, so the profit was

$25000- $2500 = $22500

Sale of Car

The car was bought by Taryn on 1st jan 2015 = $20000 and sold the same on 20th may

2020 at $12000, thus the profit will be

$ 20000- $ 12000 = $ 8000

Sale of Harry Potter’s collection

The purchase amount of Harry porter collection to Taryn on 10th Oct 2018 was $ 350 and

the selling price on 4th Jan 2020 was $ 1500, thus the remaining amount will be treated as profit

which is:

$1500- $ 350

= $ 1150

Sale of gold necklace

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

As gold prices are increasing day by day all over the world, thus selling of gold necklace

by Taryn also makes a decent profit to her. Such as the purchase price of necklace was $ 1200 on

8th Aug 2018 which she sold for $ 2000 on 20th Mar 2020 (Datt and Keating, 2018). The profit

amount will be

= $ 2000- $ 1200 = $ 800

Sale of sculpture

On 1st Jan 2020, Taryn traded a $6,000 sculpture, which she acquired on December 1994

Calculation of CBT

$ 22500 + $ 8000+ $1150 + $ 800 + $ 6000

= $ 38450 * 20.6/100

= $ 7920.7

In this, the major question about how Taryn must handle all these activities in the context

including its Capital Gains Tax laws to adjust for all CGT events and their associated

implications for their transfers as defined in the tax rate Act 1999 (Capital Gain Tax Act, 2019).

When Taryn sell an item for much more than they charged for it, a capital gain happens. They

keep an asset before trading for even more than two years; the benefit is called a long-term profit

but is paid at a reduced amount. By saving for the longer term, utilizing tax-advantaged pension

plans then replacing investment income with investment losses, they can reduce or eliminate

capital gains income. Gains on collectibles such as sets of artworks and coins are charged at a

rate of 28 per cent. That very same limit represents the portion of profit on the selling of eligible

small company inventory that is not tax-excluded (Section 1202 stock) (Evans, Minas and Lim,

2015). To a specific exception, investment income from the selling of a principal property is

treated so differently from any real assets. Essentially, as soon as the purchaser has purchased

and moved into the house for 2 years about every, the first $250,000 of a person's earnings from

selling a home is exempt from their taxes during the year. Long-term capital gains are charged

with deductibility at a cost of 20.8 per cent (scale includes cessation of health and education).

Indexation is essentially a method for calculating asset prices as per the inflation index. This will

raise total expenses and therefore will taxable income and tax liabilities as a result. Thus, under

long-term capital assets, the gain of indexing and the individual who drops underneath the 30 per

cent income range also gets the bonus of charging the 20 per cent lower tax rate. Long-term

capital profit are measured in the same manner as short-term capital profit except the purchasing

by Taryn also makes a decent profit to her. Such as the purchase price of necklace was $ 1200 on

8th Aug 2018 which she sold for $ 2000 on 20th Mar 2020 (Datt and Keating, 2018). The profit

amount will be

= $ 2000- $ 1200 = $ 800

Sale of sculpture

On 1st Jan 2020, Taryn traded a $6,000 sculpture, which she acquired on December 1994

Calculation of CBT

$ 22500 + $ 8000+ $1150 + $ 800 + $ 6000

= $ 38450 * 20.6/100

= $ 7920.7

In this, the major question about how Taryn must handle all these activities in the context

including its Capital Gains Tax laws to adjust for all CGT events and their associated

implications for their transfers as defined in the tax rate Act 1999 (Capital Gain Tax Act, 2019).

When Taryn sell an item for much more than they charged for it, a capital gain happens. They

keep an asset before trading for even more than two years; the benefit is called a long-term profit

but is paid at a reduced amount. By saving for the longer term, utilizing tax-advantaged pension

plans then replacing investment income with investment losses, they can reduce or eliminate

capital gains income. Gains on collectibles such as sets of artworks and coins are charged at a

rate of 28 per cent. That very same limit represents the portion of profit on the selling of eligible

small company inventory that is not tax-excluded (Section 1202 stock) (Evans, Minas and Lim,

2015). To a specific exception, investment income from the selling of a principal property is

treated so differently from any real assets. Essentially, as soon as the purchaser has purchased

and moved into the house for 2 years about every, the first $250,000 of a person's earnings from

selling a home is exempt from their taxes during the year. Long-term capital gains are charged

with deductibility at a cost of 20.8 per cent (scale includes cessation of health and education).

Indexation is essentially a method for calculating asset prices as per the inflation index. This will

raise total expenses and therefore will taxable income and tax liabilities as a result. Thus, under

long-term capital assets, the gain of indexing and the individual who drops underneath the 30 per

cent income range also gets the bonus of charging the 20 per cent lower tax rate. Long-term

capital profit are measured in the same manner as short-term capital profit except the purchasing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

costs and development costs are offset by the weighted transaction costs and enhancement costs.

Capital benefit investment scheme helps an individual to obtain tax deductions when owning a

home. The Government of Australia only permits the removal of funding from this account to

buy houses and plots, and if extracted for any other reason, the funds must be used within three

years of withdrawals. Otherwise the gross benefit figure would be paid according to the standard

long-term capital gain tax thresholds (Deb, 2018).

CONCLUSION

In this report, it has been concluded that the allowance that the purchaser obtained or is to

obtain as a consequences of the sale of his financial assets. In the year of transition, capital gains

are payable except though no payment has been earned. Capital gains tax is levied mostly on

gains recorded because after asset has been sold regulation of capital gains refers only to

"financial properties" such as securities, shares, jewellery, coin holdings and property

development. The IRS regulates all capital gains and has various attitudes to taxation long-term

gains vs. short-term gains taxpayers may use schemes to balance capital gains against investment

losses and reduce the capital gains taxes.

Capital benefit investment scheme helps an individual to obtain tax deductions when owning a

home. The Government of Australia only permits the removal of funding from this account to

buy houses and plots, and if extracted for any other reason, the funds must be used within three

years of withdrawals. Otherwise the gross benefit figure would be paid according to the standard

long-term capital gain tax thresholds (Deb, 2018).

CONCLUSION

In this report, it has been concluded that the allowance that the purchaser obtained or is to

obtain as a consequences of the sale of his financial assets. In the year of transition, capital gains

are payable except though no payment has been earned. Capital gains tax is levied mostly on

gains recorded because after asset has been sold regulation of capital gains refers only to

"financial properties" such as securities, shares, jewellery, coin holdings and property

development. The IRS regulates all capital gains and has various attitudes to taxation long-term

gains vs. short-term gains taxpayers may use schemes to balance capital gains against investment

losses and reduce the capital gains taxes.

REFERENCES

Books and Journals

Boadway, R. and Tremblay, J. F., 2016. Modernizing Business Taxation. CD Howe Institute

Commentary. 452.

Datt, K. H. and Keating, M., 2018, April. The Commissioner’s obligation to make compensating

adjustments for income tax and GST in Australia and New Zealand. In Australian Tax

Forum (Vol. 33, No. 3).

Deb, R., 2018. Tax Reforms and GST: A Systematic Literature Review. Journal of Commerce

and Accounting Research. 7(1). p.40.

Evans, C., Minas, J. and Lim, Y., 2015. Taxing personal capital gains in Australia: An alternative

way forward. Austl. Tax F.. 30. p.735.

Jones, D., 2016. Capital gains tax: The rise of market value?. Taxation in Australia. 51(2). p.67.

Kraal, D. and Kasipillai, J., 2016. Finally, a goods and services tax for Malaysia: A comparison

to Australia's GST experience. Austl. Tax F.. 31. p.257.

O’Connell, A., 2017. Australia. In Capital Gains Taxation. Edward Elgar Publishing.

Tang, C., 2016. Australian GST update—2015. World Journal of VAT/GST Law. 5(1). pp.32-41.

Books and Journals

Boadway, R. and Tremblay, J. F., 2016. Modernizing Business Taxation. CD Howe Institute

Commentary. 452.

Datt, K. H. and Keating, M., 2018, April. The Commissioner’s obligation to make compensating

adjustments for income tax and GST in Australia and New Zealand. In Australian Tax

Forum (Vol. 33, No. 3).

Deb, R., 2018. Tax Reforms and GST: A Systematic Literature Review. Journal of Commerce

and Accounting Research. 7(1). p.40.

Evans, C., Minas, J. and Lim, Y., 2015. Taxing personal capital gains in Australia: An alternative

way forward. Austl. Tax F.. 30. p.735.

Jones, D., 2016. Capital gains tax: The rise of market value?. Taxation in Australia. 51(2). p.67.

Kraal, D. and Kasipillai, J., 2016. Finally, a goods and services tax for Malaysia: A comparison

to Australia's GST experience. Austl. Tax F.. 31. p.257.

O’Connell, A., 2017. Australia. In Capital Gains Taxation. Edward Elgar Publishing.

Tang, C., 2016. Australian GST update—2015. World Journal of VAT/GST Law. 5(1). pp.32-41.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.