Taxation Theory, Practice and Law - Tutorial Questions Solution

VerifiedAdded on 2023/01/10

|8

|1968

|70

Homework Assignment

AI Summary

This document provides a comprehensive solution to tutorial questions from a Taxation Theory, Practice and Law unit. It covers various aspects of Australian taxation law, including the functions of taxation, residential status and income tax liability, tax treatment of payments, assessability and deductibility of events, and the calculation of depreciation using both prime cost and diminishing value methods. The solution incorporates relevant legislation, case law, and practical examples to illustrate the application of tax principles. Specific topics include the Income Tax Assessment Act 1997, residency tests, capital versus revenue receipts, and work-related expenses. The document aims to provide a clear and concise understanding of the complex tax concepts through detailed explanations and calculations.

TAXATION, THEORY

PRACTICE AND LAW

PRACTICE AND LAW

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

WEEK 1...........................................................................................................................................1

Functions of Taxation..................................................................................................................1

WEEK 2...........................................................................................................................................2

Residential status and income tax liability of Amandeep............................................................2

WEEK 3...........................................................................................................................................2

Tax treatment of payment for Gary.............................................................................................2

WEEK 4...........................................................................................................................................3

Assessability or Deductibility of the events................................................................................3

WEEK 5...........................................................................................................................................4

Deduction for decline in value using prime cost and diminishing value method........................4

REFERENCES................................................................................................................................6

TABLE OF CONTENTS................................................................................................................2

WEEK 1...........................................................................................................................................1

Functions of Taxation..................................................................................................................1

WEEK 2...........................................................................................................................................2

Residential status and income tax liability of Amandeep............................................................2

WEEK 3...........................................................................................................................................2

Tax treatment of payment for Gary.............................................................................................2

WEEK 4...........................................................................................................................................3

Assessability or Deductibility of the events................................................................................3

WEEK 5...........................................................................................................................................4

Deduction for decline in value using prime cost and diminishing value method........................4

REFERENCES................................................................................................................................6

WEEK 1

Functions of Taxation

Tax is defines as the charge over the organisations and individuals by statutory

authorities on the product, services or income. Taxation is governed by the Income Tax

Assessment Act, 1997 that requires the individuals to pay tax on their income above the

threshold limit. Tax in Australia is collected by the Australian taxation office that also guides

about the taxability of events and payments of tax. Tax is collected by the government for

running the economy of country. Government uses the tax collected for the development and

upliftment of the society. It undertakes various plans and projects for developing the

infrastructure and increasing the growth rate of economy. There are number of functions to be

performed by the taxation.

It functions as the body having charges of imposing tax over the individuals equitably on

the basis of their earnings and income. Earning capacity and assets of the individuals are

sued for measuring the earning ability. It ensures that taxes are charged from the people

on progressive basis.

Taxation has the function of ensuring that taxes are increased in manner that decreases

economic costs that is created by the bias or distortions from various tax implications.

These are evaluated on the basis of revenues generated as rise in overall taxes (Murphy,

2019).

Taxation performs the function of raising revenues from the incomes and services of

individuals for satisfying increasing needs of society. This is essential for public to earn

adequate level of incomes for taxation purposes.

It has established age neutrality between the age group of different generations. It ensures

that there is uniform taxation system for people belonging to same age group in the

country.

The taxation ensures community is consulted and engaged in the process of making

taxation reforms with diversity, interests and views. Big reforms brought immediately

don not get much acceptance as in the case where the problems are defined and solutions

are searched for getting more acceptance.

It functions as a body to make system of Australian taxation simple as well as

predictable. It pays attention towards framing structure of tax systems in ways that

1

Functions of Taxation

Tax is defines as the charge over the organisations and individuals by statutory

authorities on the product, services or income. Taxation is governed by the Income Tax

Assessment Act, 1997 that requires the individuals to pay tax on their income above the

threshold limit. Tax in Australia is collected by the Australian taxation office that also guides

about the taxability of events and payments of tax. Tax is collected by the government for

running the economy of country. Government uses the tax collected for the development and

upliftment of the society. It undertakes various plans and projects for developing the

infrastructure and increasing the growth rate of economy. There are number of functions to be

performed by the taxation.

It functions as the body having charges of imposing tax over the individuals equitably on

the basis of their earnings and income. Earning capacity and assets of the individuals are

sued for measuring the earning ability. It ensures that taxes are charged from the people

on progressive basis.

Taxation has the function of ensuring that taxes are increased in manner that decreases

economic costs that is created by the bias or distortions from various tax implications.

These are evaluated on the basis of revenues generated as rise in overall taxes (Murphy,

2019).

Taxation performs the function of raising revenues from the incomes and services of

individuals for satisfying increasing needs of society. This is essential for public to earn

adequate level of incomes for taxation purposes.

It has established age neutrality between the age group of different generations. It ensures

that there is uniform taxation system for people belonging to same age group in the

country.

The taxation ensures community is consulted and engaged in the process of making

taxation reforms with diversity, interests and views. Big reforms brought immediately

don not get much acceptance as in the case where the problems are defined and solutions

are searched for getting more acceptance.

It functions as a body to make system of Australian taxation simple as well as

predictable. It pays attention towards framing structure of tax systems in ways that

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

minimise the compliance costs. it also ensures that the possibilities of tax avoidance are

mitigated and reduced to minimum.

WEEK 2

Residential status and income tax liability of Amandeep.

In Australia taxability is dependent over the residential status of the tax payer. Before

charging tax residency tests are to be checked of the individuals coming from abroad in

Australia. There are three test given under the residency tests

Resides Test – In this test individual is regarded as Australian resident for the tax purposes in

person resides in Australia. Residency status of the person is determined on the basis of various

criteria like intention of purpose, physical and family presence, business or employment ties,

social & living arrangements.

Domicile Test – It is done if resides test is not satisfied. If the person is having domicile in

Australia it is considered as Australian resident except when on satisfaction that permanent place

of abode is out of Australia.

183 Day Test - It is applied over people visiting from outside in Australia. According to the test

if an individual is present in Australia above half of income year, is considered as Australian

resident. Person could be having constructive residence if the adobe place is outside Australia

and the intention is not to live in Australia (Hobson, 2019). Those individual that have taken

residence are considered as Australian citizen.

In this case Amandeep has satisfied the resides test as place of residence is already taken

in Australia Amandeep is living in the residence along with the family and has also opened

Australian bank account. From these actions it could be clearly identified that the Amandeep

intends to reside in Australia and also domicile test is satisfied as residence unit has been

purchased in Australia. Therefore from the above tests it could be identified that Amandeep is an

Australian resident for the tax purpose. Tax will be paid in Australia on Salary and not on

investment incomes.

WEEK 3

Tax treatment of payment for Gary

In the present case Gary has leased premises and commercial buildings for conducting

bakery business. John has received 3100 to recover the repair expenses. Compensation has been

2

mitigated and reduced to minimum.

WEEK 2

Residential status and income tax liability of Amandeep.

In Australia taxability is dependent over the residential status of the tax payer. Before

charging tax residency tests are to be checked of the individuals coming from abroad in

Australia. There are three test given under the residency tests

Resides Test – In this test individual is regarded as Australian resident for the tax purposes in

person resides in Australia. Residency status of the person is determined on the basis of various

criteria like intention of purpose, physical and family presence, business or employment ties,

social & living arrangements.

Domicile Test – It is done if resides test is not satisfied. If the person is having domicile in

Australia it is considered as Australian resident except when on satisfaction that permanent place

of abode is out of Australia.

183 Day Test - It is applied over people visiting from outside in Australia. According to the test

if an individual is present in Australia above half of income year, is considered as Australian

resident. Person could be having constructive residence if the adobe place is outside Australia

and the intention is not to live in Australia (Hobson, 2019). Those individual that have taken

residence are considered as Australian citizen.

In this case Amandeep has satisfied the resides test as place of residence is already taken

in Australia Amandeep is living in the residence along with the family and has also opened

Australian bank account. From these actions it could be clearly identified that the Amandeep

intends to reside in Australia and also domicile test is satisfied as residence unit has been

purchased in Australia. Therefore from the above tests it could be identified that Amandeep is an

Australian resident for the tax purpose. Tax will be paid in Australia on Salary and not on

investment incomes.

WEEK 3

Tax treatment of payment for Gary

In the present case Gary has leased premises and commercial buildings for conducting

bakery business. John has received 3100 to recover the repair expenses. Compensation has been

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

received by the Gary for because of the breach of the terms of lease. In this case contract is

breached by John for whom compensation has been paid by John of 3100.

As per rule TR 95/35 it is required to identify that the receipts whether are income or

capital. Damages had been made by John to the underlying asset of the property (Mackie and

et.al., 2019). The receipts are received due to the damage to capital assets therefore they are

considered as capital receipts. As per the taxation department compensation receipts are taxable,

revenues receipts are allowed as deduction in the year in which they are received and capital

receipts are amortised over 5 years or useful life whichever is shorter. Applying the provisions of

the above compensation it could be compensation received for the damages are charged as

capital receipt and is taxable in capital gain tax of the income tax returns.

WEEK 4

Assessability or Deductibility of the events

i) In the present case legal expenses are incurred for false advertising. Expenses incurred

for producing assessable income are allowed for deduction under ITAA, 1997. Fines or penalties

are not allowed to be claimed as deduction as per section 25.5 of ITAA, 97. Legal expenses for

fighting suit for false advertising and these are not related to the work for producing assessable

income. Therefore, deduction over legal expenses is not allowed as deduction.

ii) Under the taxation systems tax payers are not allowed for deduction on immediate basis

over capital expenditures or the capital assets. On the capital expenditures deduction is allowed

to the tax payers in form of depreciation (Braithwaite, ed., 2017). Constriction expenditure is

incurred by John after February 26, 1992 and they are allowed as deduction under section 43.210

of the ITAA, 97. John can claim deduction for capital expenditures of $22000 by adding it to

building cost as depreciation.

iii) Income tax provides for deduction for work related expenses to produce assessable

income. In present case John has incurred expenses on T shirts with logo of company to market

the business that means for producing assessable income. According to section 900 of he ITAA,

97 work related expenses could be claimed as deduction as they related with producing

assessable income. Expenditures incurred other than related to the work are not allowed for

deduction.

iv) Taxation department of Australia has specified that deduction could not be claimed for

the expenditures that are related with fines or penalties. In this case John is fined for putting the

3

breached by John for whom compensation has been paid by John of 3100.

As per rule TR 95/35 it is required to identify that the receipts whether are income or

capital. Damages had been made by John to the underlying asset of the property (Mackie and

et.al., 2019). The receipts are received due to the damage to capital assets therefore they are

considered as capital receipts. As per the taxation department compensation receipts are taxable,

revenues receipts are allowed as deduction in the year in which they are received and capital

receipts are amortised over 5 years or useful life whichever is shorter. Applying the provisions of

the above compensation it could be compensation received for the damages are charged as

capital receipt and is taxable in capital gain tax of the income tax returns.

WEEK 4

Assessability or Deductibility of the events

i) In the present case legal expenses are incurred for false advertising. Expenses incurred

for producing assessable income are allowed for deduction under ITAA, 1997. Fines or penalties

are not allowed to be claimed as deduction as per section 25.5 of ITAA, 97. Legal expenses for

fighting suit for false advertising and these are not related to the work for producing assessable

income. Therefore, deduction over legal expenses is not allowed as deduction.

ii) Under the taxation systems tax payers are not allowed for deduction on immediate basis

over capital expenditures or the capital assets. On the capital expenditures deduction is allowed

to the tax payers in form of depreciation (Braithwaite, ed., 2017). Constriction expenditure is

incurred by John after February 26, 1992 and they are allowed as deduction under section 43.210

of the ITAA, 97. John can claim deduction for capital expenditures of $22000 by adding it to

building cost as depreciation.

iii) Income tax provides for deduction for work related expenses to produce assessable

income. In present case John has incurred expenses on T shirts with logo of company to market

the business that means for producing assessable income. According to section 900 of he ITAA,

97 work related expenses could be claimed as deduction as they related with producing

assessable income. Expenditures incurred other than related to the work are not allowed for

deduction.

iv) Taxation department of Australia has specified that deduction could not be claimed for

the expenditures that are related with fines or penalties. In this case John is fined for putting the

3

items on display without receiving proper permit for the same (ITAA, 1997. 2019). John cannot

claim deduction for payment of fines in the tax return in accordance with the section 26 of ITAA,

1997.

WEEK 5

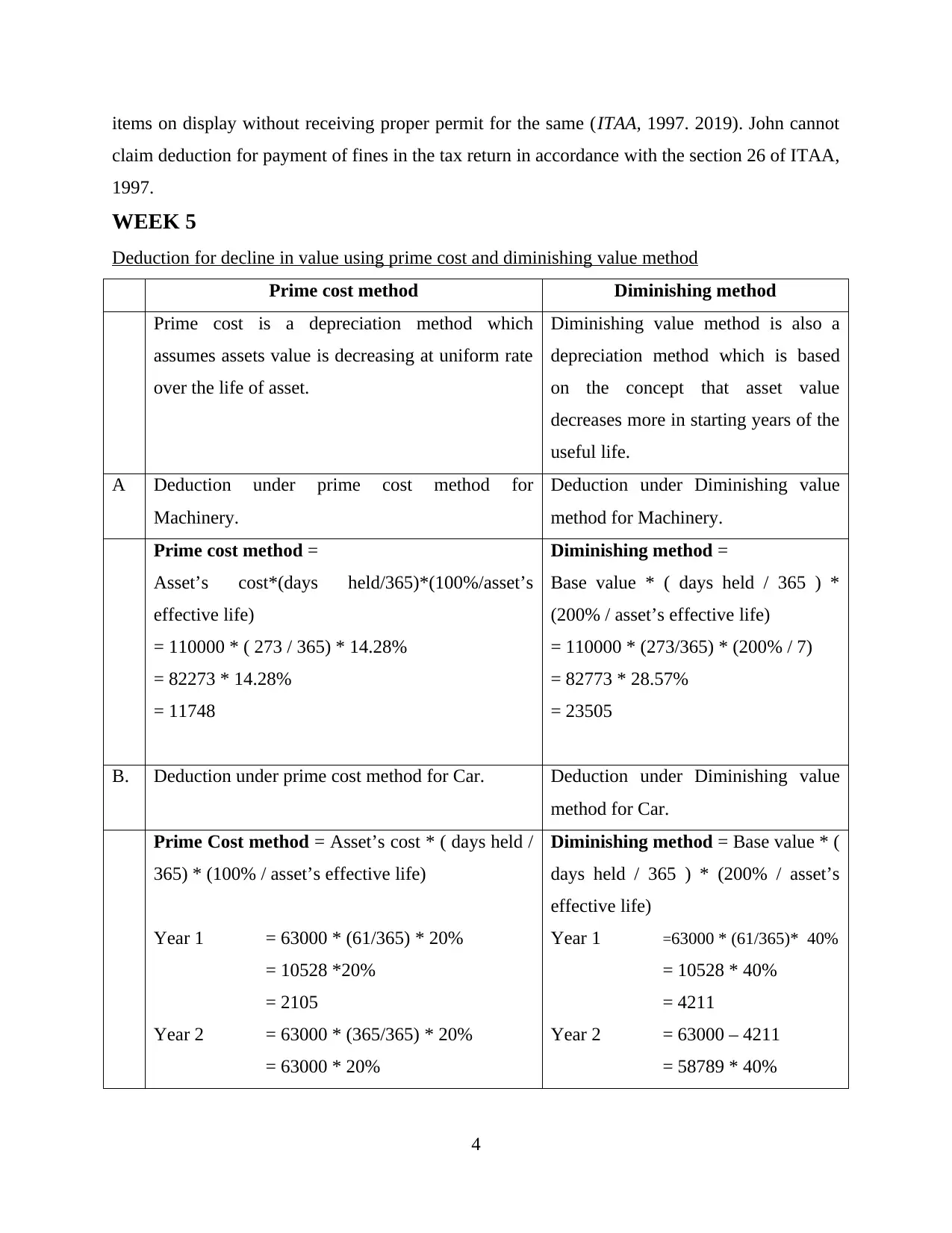

Deduction for decline in value using prime cost and diminishing value method

Prime cost method Diminishing method

Prime cost is a depreciation method which

assumes assets value is decreasing at uniform rate

over the life of asset.

Diminishing value method is also a

depreciation method which is based

on the concept that asset value

decreases more in starting years of the

useful life.

A Deduction under prime cost method for

Machinery.

Deduction under Diminishing value

method for Machinery.

Prime cost method =

Asset’s cost*(days held/365)*(100%/asset’s

effective life)

= 110000 * ( 273 / 365) * 14.28%

= 82273 * 14.28%

= 11748

Diminishing method =

Base value * ( days held / 365 ) *

(200% / asset’s effective life)

= 110000 * (273/365) * (200% / 7)

= 82773 * 28.57%

= 23505

B. Deduction under prime cost method for Car. Deduction under Diminishing value

method for Car.

Prime Cost method = Asset’s cost * ( days held /

365) * (100% / asset’s effective life)

Year 1 = 63000 * (61/365) * 20%

= 10528 *20%

= 2105

Year 2 = 63000 * (365/365) * 20%

= 63000 * 20%

Diminishing method = Base value * (

days held / 365 ) * (200% / asset’s

effective life)

Year 1 =63000 * (61/365)* 40%

= 10528 * 40%

= 4211

Year 2 = 63000 – 4211

= 58789 * 40%

4

claim deduction for payment of fines in the tax return in accordance with the section 26 of ITAA,

1997.

WEEK 5

Deduction for decline in value using prime cost and diminishing value method

Prime cost method Diminishing method

Prime cost is a depreciation method which

assumes assets value is decreasing at uniform rate

over the life of asset.

Diminishing value method is also a

depreciation method which is based

on the concept that asset value

decreases more in starting years of the

useful life.

A Deduction under prime cost method for

Machinery.

Deduction under Diminishing value

method for Machinery.

Prime cost method =

Asset’s cost*(days held/365)*(100%/asset’s

effective life)

= 110000 * ( 273 / 365) * 14.28%

= 82273 * 14.28%

= 11748

Diminishing method =

Base value * ( days held / 365 ) *

(200% / asset’s effective life)

= 110000 * (273/365) * (200% / 7)

= 82773 * 28.57%

= 23505

B. Deduction under prime cost method for Car. Deduction under Diminishing value

method for Car.

Prime Cost method = Asset’s cost * ( days held /

365) * (100% / asset’s effective life)

Year 1 = 63000 * (61/365) * 20%

= 10528 *20%

= 2105

Year 2 = 63000 * (365/365) * 20%

= 63000 * 20%

Diminishing method = Base value * (

days held / 365 ) * (200% / asset’s

effective life)

Year 1 =63000 * (61/365)* 40%

= 10528 * 40%

= 4211

Year 2 = 63000 – 4211

= 58789 * 40%

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= 12600 = 23516

According to section 40 of ITAA, 1997 deduction for capital expenditures allowed as

deduction in the form of depreciation over the useful life of asset. In the present case claims

could be made as deduction under the income tax return (Biddle, Fels and Sinning, 2017). In

the present case machine is purchased on October 1, 2019 and from this date it is held for 273

days in the income year. on the depreciation over car will be charged for full year as it was

purchased last year.

Asset Prime Cost Method Diminishing value Method

Machine 11748 23505

Car 12600 23516

5

According to section 40 of ITAA, 1997 deduction for capital expenditures allowed as

deduction in the form of depreciation over the useful life of asset. In the present case claims

could be made as deduction under the income tax return (Biddle, Fels and Sinning, 2017). In

the present case machine is purchased on October 1, 2019 and from this date it is held for 273

days in the income year. on the depreciation over car will be charged for full year as it was

purchased last year.

Asset Prime Cost Method Diminishing value Method

Machine 11748 23505

Car 12600 23516

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Murphy, K., 2019. Moving towards a more effective model of regulatory enforcement in the

Australian Taxation Office. Centre for Tax System Integrity (CTSI), Research School of

Social Sciences, The Australian National University.

Hobson, K., 2019. 'Say no to the ATO': The cultural politics of protest against the Australian Tax

Office. Centre for Tax System Integrity (CTSI), Research School of Social Sciences, The

Australian National University.

Mackie, R.S., and et.al., 2019. Trends in nicotine consumption between 2010 and 2017 in an

Australian city using the wastewater-based epidemiology approach. Environment

international. 125. pp.184-190.

Braithwaite, V. ed., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Biddle, N., Fels, K. and Sinning, M., 2017. Behavioural insights and business taxation: Evidence

from two randomized controlled trials. Tax and Transfer Policy Institute-Working

Paper, 2.

Online

ITAA, 1997. 2019. [Online]. Available through :

<http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/>.

6

Books and Journals

Murphy, K., 2019. Moving towards a more effective model of regulatory enforcement in the

Australian Taxation Office. Centre for Tax System Integrity (CTSI), Research School of

Social Sciences, The Australian National University.

Hobson, K., 2019. 'Say no to the ATO': The cultural politics of protest against the Australian Tax

Office. Centre for Tax System Integrity (CTSI), Research School of Social Sciences, The

Australian National University.

Mackie, R.S., and et.al., 2019. Trends in nicotine consumption between 2010 and 2017 in an

Australian city using the wastewater-based epidemiology approach. Environment

international. 125. pp.184-190.

Braithwaite, V. ed., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Biddle, N., Fels, K. and Sinning, M., 2017. Behavioural insights and business taxation: Evidence

from two randomized controlled trials. Tax and Transfer Policy Institute-Working

Paper, 2.

Online

ITAA, 1997. 2019. [Online]. Available through :

<http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/>.

6

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.