Taxation, Theory and Practice 1 Assignment - University Homework

VerifiedAdded on 2020/03/23

|10

|1242

|38

Homework Assignment

AI Summary

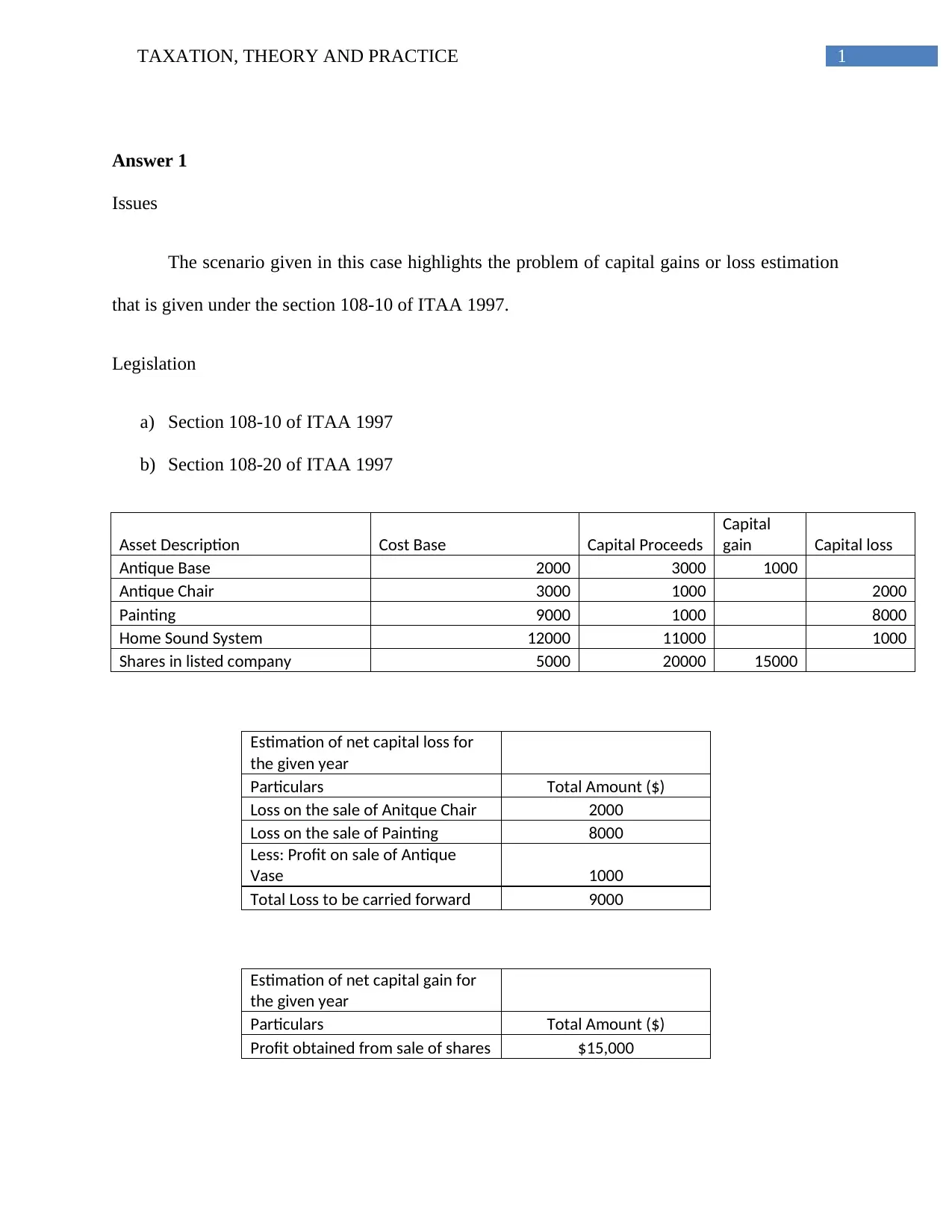

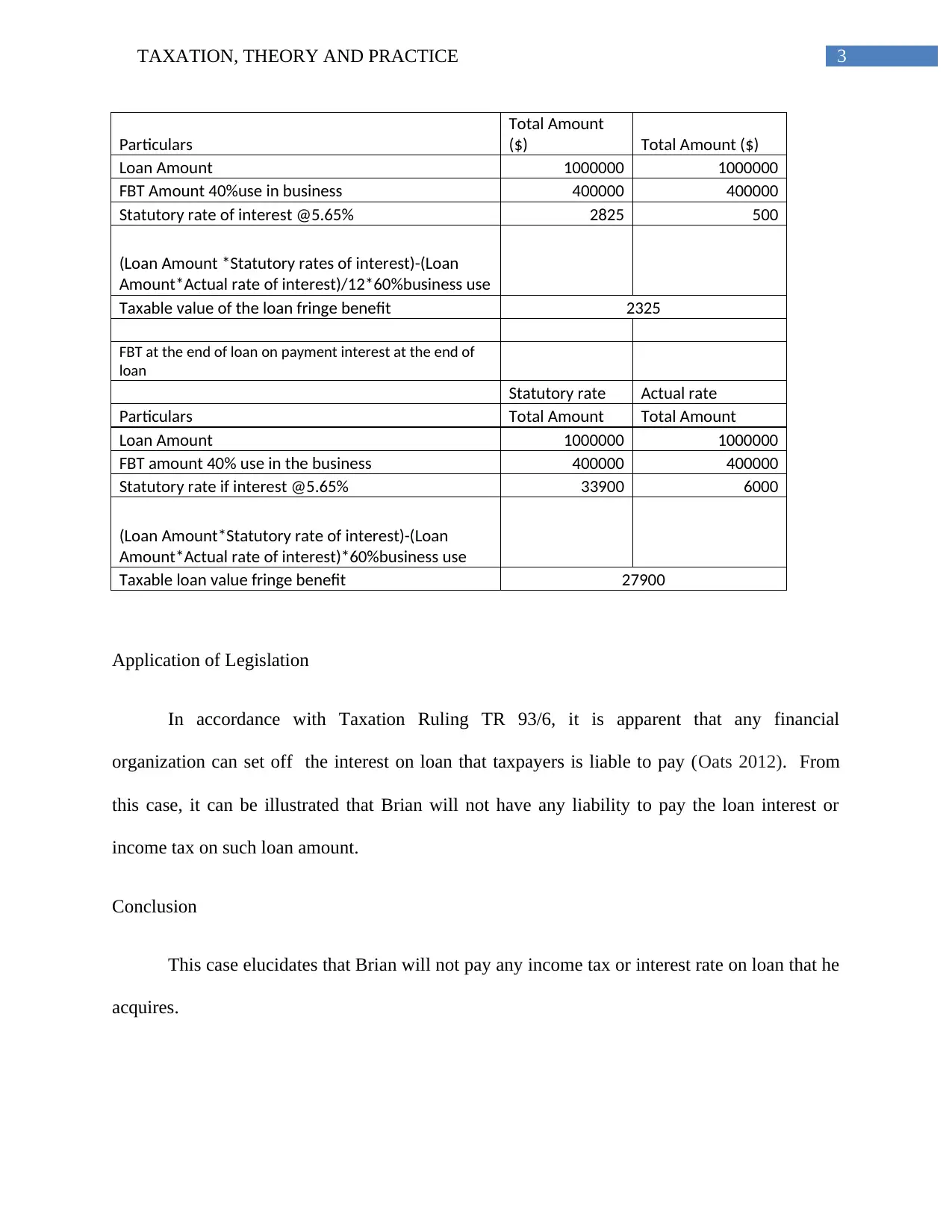

This assignment solution addresses various taxation issues, including capital gains and losses under ITAA 1997, the concept of Fringe Benefits Tax (FBT) and its calculation, and income computation from the sale of timber. The solution analyzes scenarios involving asset sales, loan fringe benefits, property rentals, and tax avoidance cases. The assignment covers relevant legislation, such as Section 108-10 and 108-20 of ITAA 1997, the FBT Act 1986, and various taxation rulings. The solution provides detailed calculations, applications of legislation, and conclusions for each issue, supported by relevant case laws and references. It explores topics like net capital gain/loss estimation, taxable value of loan fringe benefits, co-ownership of properties, and income from timber sales, offering a comprehensive analysis of complex taxation scenarios.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.