Taxation Assignment: HI6028, T2 2019 - GST and Capital Gains Tax

VerifiedAdded on 2022/10/09

|8

|2696

|226

Homework Assignment

AI Summary

This assignment, prepared for the HI6028 Taxation Theory, Practice & Law unit at Holmes Institute, focuses on the application of Australian taxation principles. It presents a detailed analysis of the Goods and Services Tax (GST), including eligibility for Input Tax Credit (ITC) for a company named City Sky Co. It also examines Capital Gains Tax (CGT) implications for Emma, analyzing gains from the sale of land, shares, and a stamp collection. The assignment meticulously calculates taxable capital gains, considering various costs and the 50% discount for shares held over 12 months. The analysis includes relevant legal issues, application of tax laws, and conclusions for each scenario, demonstrating an understanding of the Australian income tax system and its practical application.

TAXATION THEORY, PRACTICE & LAW

TRIMESTER: T2 2019

UNIT CODE: HI6028

1

TRIMESTER: T2 2019

UNIT CODE: HI6028

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION................................................................................................................................................3

QUESTION 1: THE GOODS AND SERVICES TAX (GST):...................................................................................3

ANALYSIS OF THE ELIGIBILITY OF ITC FOR CITY SKY GOODS:....................................................................3

QUESTION 2: CAPITAL GAINS TAX: ANALYSIS OF GAINS OF EMMA UNDER VARIOUS CASES:......................5

SALE OF A BLOCK OF LAND FOR $1,000,000 ON WHICH ADDITIONAL COSTS HAVE BEEN INCURRED:.....5

SALE OF 1000 SHARES BY EMMA:.............................................................................................................6

SALE OF STAMP COLLECTION:..................................................................................................................6

SALE OF GRAND PIANO FOR $30,000:......................................................................................................7

CONCLUSION:...................................................................................................................................................7

REFERENCES:....................................................................................................................................................8

2

INTRODUCTION................................................................................................................................................3

QUESTION 1: THE GOODS AND SERVICES TAX (GST):...................................................................................3

ANALYSIS OF THE ELIGIBILITY OF ITC FOR CITY SKY GOODS:....................................................................3

QUESTION 2: CAPITAL GAINS TAX: ANALYSIS OF GAINS OF EMMA UNDER VARIOUS CASES:......................5

SALE OF A BLOCK OF LAND FOR $1,000,000 ON WHICH ADDITIONAL COSTS HAVE BEEN INCURRED:.....5

SALE OF 1000 SHARES BY EMMA:.............................................................................................................6

SALE OF STAMP COLLECTION:..................................................................................................................6

SALE OF GRAND PIANO FOR $30,000:......................................................................................................7

CONCLUSION:...................................................................................................................................................7

REFERENCES:....................................................................................................................................................8

2

INTRODUCTION

The tax policies in any country is being framed by the regulators of that particular country.

It is to be noted that although the provisions with respect to taxation and their rates varies

from government to government but in case of the basic structure of law, it all remains

same across the world for a developing and a developed country. The basic motive behind

the formation of taxation policies is the improvement in economy and the society that

exists with the country. The tax policies being framed by the government are both on the

production process as well as the income of the individual and businesses. Like any other

developed country, the tax policies of Australia are being framed by its government. The

indirect tax being introduced by the government that abolished the entire existing indirect

taxes that were in effect and introduced one single tax called Goods and Services Tax in

the process of manufacturing and production which creates and generates values. The

basic motive behind the introduction of the Goods and Services Tax, popularly the GST

was to have uniformity in taxation and also for avoidance of imposition of tax on the

amount of tax. The government of Australia have fixed rate of GST which is of two different

types based on the industries and companies contributing towards the betterment of

economy. The basic rate is 10% which is applicable to all the major industries and

businesses. However, for companies that requires boosts from government, providing the

items of necessity, their tax rate are being charged at a subsidised rate which is 5.5%. In

addition to the two rates, there are certain businesses that have been kept outside the

purview of GST by the Australian Government since they are made exempt from taxation.

In addition to the indirect tax act, there are direct tax act namely Income Tax Assessment

Act, being applicable on the income earned by individual and businesses in different forms

so as to have provisions on the gains and their tax liability. The paper here will have

analysis of the GST and the provisions of Capital Gains Tax with respect to earnings

earned on sale of capital assets.

QUESTION 1: THE GOODS AND SERVICES TAX (GST):

ANALYSIS OF THE ELIGIBILITY OF ITC FOR CITY SKY GOODS:

The basic idea towards the introduction of Goods and Service Tax (GST) was the

introduction of one act governing the production process and abolishing all the existing

multiple taxes. As per the provisions of the law stated in GST, the businesses are provided

a threshold limit for registering themselves under GST. Businesses having revenue above

the threshold limit are mandatorily required to get them registered whereas for the

businesses having revenue less than the threshold limit does not have to require

themselves to be registered until they do it voluntarily. The limit of gross total revenue fixed

as threshold is $75,000(Aaron Henry, 1974). The rate of GST is 10% for the major group

of industries and companies. The government, however, have provided a concessional

rate of 5.5% on businesses that for expansion needs the support of the government. Going

forward, it can also be seen that certain group of industries and businesses are kept

outside the purview of GST and are exempt from it. Those industries are the one’s that

carries the business of dealing in items of necessity like specific food, items of household

and the healthcare industries. This was done by the government so as to have more

businesses in this line of business. The law of GST contains a provision wherein it has

been observed that in case there has been excess payment done on account of GST, the

3

The tax policies in any country is being framed by the regulators of that particular country.

It is to be noted that although the provisions with respect to taxation and their rates varies

from government to government but in case of the basic structure of law, it all remains

same across the world for a developing and a developed country. The basic motive behind

the formation of taxation policies is the improvement in economy and the society that

exists with the country. The tax policies being framed by the government are both on the

production process as well as the income of the individual and businesses. Like any other

developed country, the tax policies of Australia are being framed by its government. The

indirect tax being introduced by the government that abolished the entire existing indirect

taxes that were in effect and introduced one single tax called Goods and Services Tax in

the process of manufacturing and production which creates and generates values. The

basic motive behind the introduction of the Goods and Services Tax, popularly the GST

was to have uniformity in taxation and also for avoidance of imposition of tax on the

amount of tax. The government of Australia have fixed rate of GST which is of two different

types based on the industries and companies contributing towards the betterment of

economy. The basic rate is 10% which is applicable to all the major industries and

businesses. However, for companies that requires boosts from government, providing the

items of necessity, their tax rate are being charged at a subsidised rate which is 5.5%. In

addition to the two rates, there are certain businesses that have been kept outside the

purview of GST by the Australian Government since they are made exempt from taxation.

In addition to the indirect tax act, there are direct tax act namely Income Tax Assessment

Act, being applicable on the income earned by individual and businesses in different forms

so as to have provisions on the gains and their tax liability. The paper here will have

analysis of the GST and the provisions of Capital Gains Tax with respect to earnings

earned on sale of capital assets.

QUESTION 1: THE GOODS AND SERVICES TAX (GST):

ANALYSIS OF THE ELIGIBILITY OF ITC FOR CITY SKY GOODS:

The basic idea towards the introduction of Goods and Service Tax (GST) was the

introduction of one act governing the production process and abolishing all the existing

multiple taxes. As per the provisions of the law stated in GST, the businesses are provided

a threshold limit for registering themselves under GST. Businesses having revenue above

the threshold limit are mandatorily required to get them registered whereas for the

businesses having revenue less than the threshold limit does not have to require

themselves to be registered until they do it voluntarily. The limit of gross total revenue fixed

as threshold is $75,000(Aaron Henry, 1974). The rate of GST is 10% for the major group

of industries and companies. The government, however, have provided a concessional

rate of 5.5% on businesses that for expansion needs the support of the government. Going

forward, it can also be seen that certain group of industries and businesses are kept

outside the purview of GST and are exempt from it. Those industries are the one’s that

carries the business of dealing in items of necessity like specific food, items of household

and the healthcare industries. This was done by the government so as to have more

businesses in this line of business. The law of GST contains a provision wherein it has

been observed that in case there has been excess payment done on account of GST, the

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

same can be received by the business as refund and in case the businesses pays GST on

the purchases, consultancy and any other payments made by it during course of business

the same can be claimed by it in its Business Activity Statement (BAS) and the annual

return as Input Tax Credit. However, there is no entitlement of availing credit of GST paid

in the hands of the end consumers.

There are specified provisions of law in relation to the real estate properties, which are

required to be analysed before charging GST and claiming ITC on the same (Anderson

John E., 1993). The property which is complete in nature, which means, completion

certificate has been received by the government, no GST is applicable on it and the same

is exempt from taxation. The properties irrespective of them being commercial or

residential if is under construction then the same will come under the laws and the

provisions of GST.

There are certain criteria required to be met if a business wants to claim Input Tax Credit

(ITC) on the invoices received by it through suppliers. The same are discussed as below:

It is required that the business as well as the supplier should both be registered

under the laws of GST. In case of absence of GST in any case, no ITC can be

claimed.

The purchases or the services being received should be ones that are essential for

the smooth running of the businesses.

The amount of GST being paid to the supplier or payable to the supplier must have

been accounted for in the books of accounts.

The final amount i.e. the total amount appearing in the invoice must have GST

included in it.

The supplier must have issued “TAX INVOICE” in accordance to the provisions

contained within the law of GST.

The details of the Input Tax Credit is being submitted to the GST Department through filing

of forms online in the site of GST (Bradbury Katharine L., and Mayer Christopher J., and

Case Karl E., 2000).

MATERIAL FACTS OF THE COMPANY CITY SKY CO.:

The business of the company City Sky Co. is the investment in properties for the purpose

of construction of apartments on land being purchased. This company is registered under

the GST as mentioned in the question specifically. However, it is clear from the given

information in the question that Maurice Blackburn, the lawyer is also registered under

GST since his Gross Total Turnover exceeds the threshold limit i.e. $300,000 exceeds

$75,000. The analysis is pertaining of the bill being received Maurice Blackburn and to

analyse whether the GST amount payable on the same would be allowed as Input Tax

Credit.

ANALYSIS OF LEGAL ISSUES AND APPLICATION OF GOODS AND SERVICES TAX (GST)

LAW:

The law of GST states that the properties that are completed in nature are not subject to

GST. In this case, however, the company City Sky Co., is into the business of construction

of apartments and thus the land sold by him would be subject to GST. The bill received

from lawyer amounting to $33,000 is required to be analysed so as to claim the amount of

Input Tax Credit (ITC) by the company City Sky Co., on the same.

The analysis of eligibility of ITC on bill of Maurice Blackburn by City Sky Co., is as follows:

4

the purchases, consultancy and any other payments made by it during course of business

the same can be claimed by it in its Business Activity Statement (BAS) and the annual

return as Input Tax Credit. However, there is no entitlement of availing credit of GST paid

in the hands of the end consumers.

There are specified provisions of law in relation to the real estate properties, which are

required to be analysed before charging GST and claiming ITC on the same (Anderson

John E., 1993). The property which is complete in nature, which means, completion

certificate has been received by the government, no GST is applicable on it and the same

is exempt from taxation. The properties irrespective of them being commercial or

residential if is under construction then the same will come under the laws and the

provisions of GST.

There are certain criteria required to be met if a business wants to claim Input Tax Credit

(ITC) on the invoices received by it through suppliers. The same are discussed as below:

It is required that the business as well as the supplier should both be registered

under the laws of GST. In case of absence of GST in any case, no ITC can be

claimed.

The purchases or the services being received should be ones that are essential for

the smooth running of the businesses.

The amount of GST being paid to the supplier or payable to the supplier must have

been accounted for in the books of accounts.

The final amount i.e. the total amount appearing in the invoice must have GST

included in it.

The supplier must have issued “TAX INVOICE” in accordance to the provisions

contained within the law of GST.

The details of the Input Tax Credit is being submitted to the GST Department through filing

of forms online in the site of GST (Bradbury Katharine L., and Mayer Christopher J., and

Case Karl E., 2000).

MATERIAL FACTS OF THE COMPANY CITY SKY CO.:

The business of the company City Sky Co. is the investment in properties for the purpose

of construction of apartments on land being purchased. This company is registered under

the GST as mentioned in the question specifically. However, it is clear from the given

information in the question that Maurice Blackburn, the lawyer is also registered under

GST since his Gross Total Turnover exceeds the threshold limit i.e. $300,000 exceeds

$75,000. The analysis is pertaining of the bill being received Maurice Blackburn and to

analyse whether the GST amount payable on the same would be allowed as Input Tax

Credit.

ANALYSIS OF LEGAL ISSUES AND APPLICATION OF GOODS AND SERVICES TAX (GST)

LAW:

The law of GST states that the properties that are completed in nature are not subject to

GST. In this case, however, the company City Sky Co., is into the business of construction

of apartments and thus the land sold by him would be subject to GST. The bill received

from lawyer amounting to $33,000 is required to be analysed so as to claim the amount of

Input Tax Credit (ITC) by the company City Sky Co., on the same.

The analysis of eligibility of ITC on bill of Maurice Blackburn by City Sky Co., is as follows:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The company receiving and providing consultancy are both registered for the

purpose of taxation under the provisions of the Goods and Services Tax Act.

The company City Sky Co. used the legal opinion of Maurice Blackburn solely in

relation to the business of the company.

The company have accounted for the bill being issued by Maurice Blackburn.

The total fees of $33,000 includes the amount of GST being applicable on service

of legal fees which is 10% and thus $3,000 is included in the total invoice towards

GST.

Maurice Blackburn have issued TAX INVOICE which is in accordance to the rules

and provisions of GST.

CONCLUSION

It can thus be analysed that the company City Sky Co, is eligible to claim Input Tax Credit

on the amount paid towards GST to Maurice Blackburn by the company. This would be

done by the company in making adjustments to its output tax liability.

QUESTION 2: CAPITAL GAINS TAX: ANALYSIS OF GAINS OF EMMA UNDER

VARIOUS CASES:

Indexation on gains arising from sale of capital assets being held for long have been

ignored as mentioned in the question.

SALE OF A BLOCK OF LAND FOR $1,000,000 ON WHICH ADDITIONAL COSTS

HAVE BEEN INCURRED:

The Income Tax Assessment Act (ITAA) prevailing in Australia contains provisions with

respect to the gains arising from the sale of Capital Assets. As per the provisions

contained within the ITAA pertaining to the Capital Gains Tax it is held that the initial cost

of acquisition of capital asset is being increased by any cost or costs being incurred

towards its improvisation and towards making the asset in a saleable condition (CCH,

2011). The nature of the additional costs can be of various type but their ultimate goal is

creation and addition of value to the capital asset. The sale proceeds are thus reduced

from the adjusted cost to arrive at the Capital Gain or Loss.

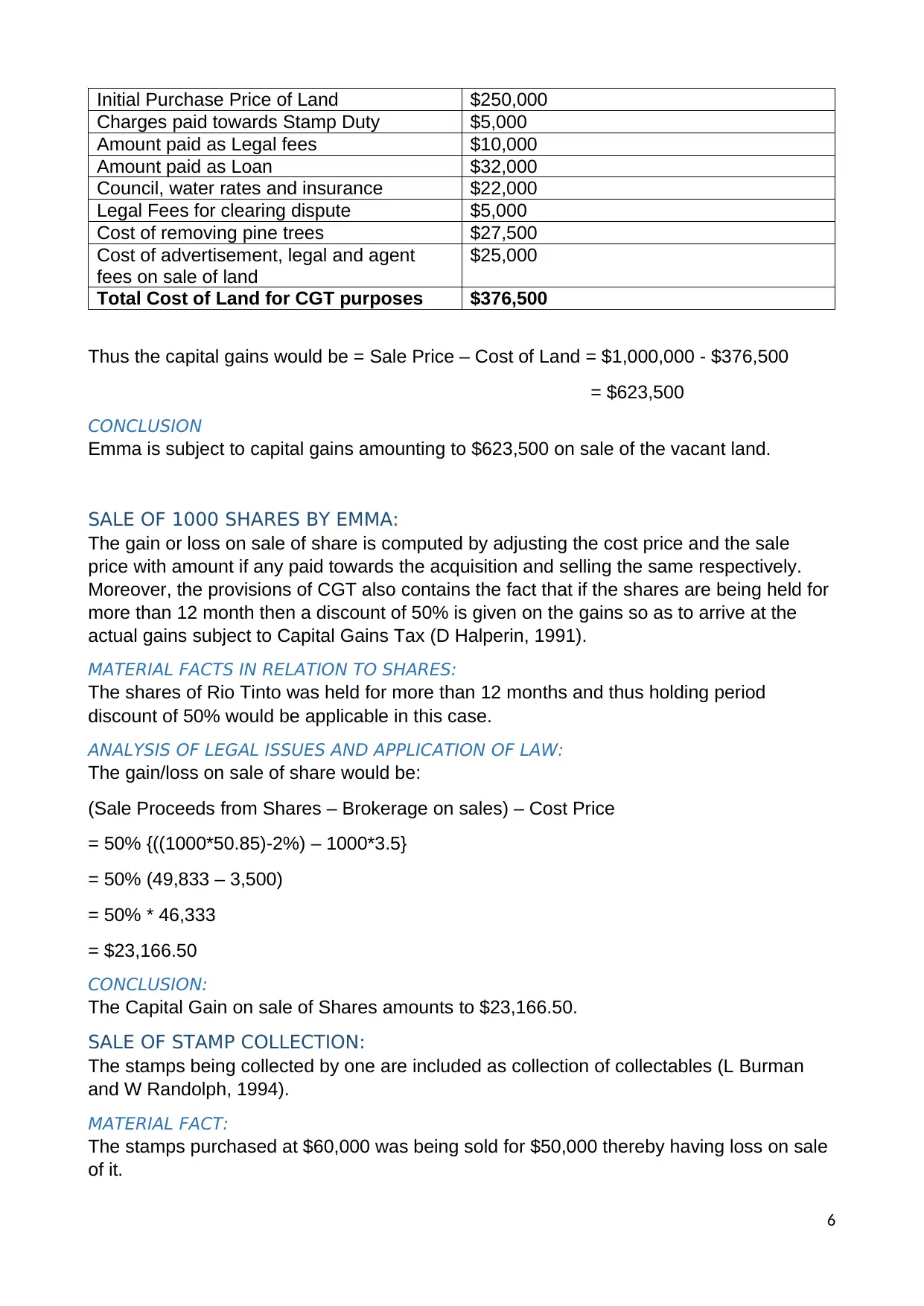

MATERIAL FACTS OF LAND OF EMMA:

The land is a Capital Asset for Emma since the same was held and purchased with an

intention of making investment. Thus, the gain or loss arising from the sale of the land will

be subject to Capital Gains Tax (A Auerbach, 1991). The adjusted costs are derived by

addition of initial cost of acquisition with the expenses incurred for its improvisation and for

its maintenance.

ANALYSIS OF LEGAL ISSUES AND APPLICATION OF LAW IN CASE OF SALE OF LAND BY

EMMA:

Emma sold the land after holding it for a long period of time and thus many costs were

incurred on the same which is required to be added in its initial costs to arrive at the capital

gain/loss from sale of land. The adjusted cost of land for the purpose of computation of

capital gains would be as follows:

5

purpose of taxation under the provisions of the Goods and Services Tax Act.

The company City Sky Co. used the legal opinion of Maurice Blackburn solely in

relation to the business of the company.

The company have accounted for the bill being issued by Maurice Blackburn.

The total fees of $33,000 includes the amount of GST being applicable on service

of legal fees which is 10% and thus $3,000 is included in the total invoice towards

GST.

Maurice Blackburn have issued TAX INVOICE which is in accordance to the rules

and provisions of GST.

CONCLUSION

It can thus be analysed that the company City Sky Co, is eligible to claim Input Tax Credit

on the amount paid towards GST to Maurice Blackburn by the company. This would be

done by the company in making adjustments to its output tax liability.

QUESTION 2: CAPITAL GAINS TAX: ANALYSIS OF GAINS OF EMMA UNDER

VARIOUS CASES:

Indexation on gains arising from sale of capital assets being held for long have been

ignored as mentioned in the question.

SALE OF A BLOCK OF LAND FOR $1,000,000 ON WHICH ADDITIONAL COSTS

HAVE BEEN INCURRED:

The Income Tax Assessment Act (ITAA) prevailing in Australia contains provisions with

respect to the gains arising from the sale of Capital Assets. As per the provisions

contained within the ITAA pertaining to the Capital Gains Tax it is held that the initial cost

of acquisition of capital asset is being increased by any cost or costs being incurred

towards its improvisation and towards making the asset in a saleable condition (CCH,

2011). The nature of the additional costs can be of various type but their ultimate goal is

creation and addition of value to the capital asset. The sale proceeds are thus reduced

from the adjusted cost to arrive at the Capital Gain or Loss.

MATERIAL FACTS OF LAND OF EMMA:

The land is a Capital Asset for Emma since the same was held and purchased with an

intention of making investment. Thus, the gain or loss arising from the sale of the land will

be subject to Capital Gains Tax (A Auerbach, 1991). The adjusted costs are derived by

addition of initial cost of acquisition with the expenses incurred for its improvisation and for

its maintenance.

ANALYSIS OF LEGAL ISSUES AND APPLICATION OF LAW IN CASE OF SALE OF LAND BY

EMMA:

Emma sold the land after holding it for a long period of time and thus many costs were

incurred on the same which is required to be added in its initial costs to arrive at the capital

gain/loss from sale of land. The adjusted cost of land for the purpose of computation of

capital gains would be as follows:

5

Initial Purchase Price of Land $250,000

Charges paid towards Stamp Duty $5,000

Amount paid as Legal fees $10,000

Amount paid as Loan $32,000

Council, water rates and insurance $22,000

Legal Fees for clearing dispute $5,000

Cost of removing pine trees $27,500

Cost of advertisement, legal and agent

fees on sale of land

$25,000

Total Cost of Land for CGT purposes $376,500

Thus the capital gains would be = Sale Price – Cost of Land = $1,000,000 - $376,500

= $623,500

CONCLUSION

Emma is subject to capital gains amounting to $623,500 on sale of the vacant land.

SALE OF 1000 SHARES BY EMMA:

The gain or loss on sale of share is computed by adjusting the cost price and the sale

price with amount if any paid towards the acquisition and selling the same respectively.

Moreover, the provisions of CGT also contains the fact that if the shares are being held for

more than 12 month then a discount of 50% is given on the gains so as to arrive at the

actual gains subject to Capital Gains Tax (D Halperin, 1991).

MATERIAL FACTS IN RELATION TO SHARES:

The shares of Rio Tinto was held for more than 12 months and thus holding period

discount of 50% would be applicable in this case.

ANALYSIS OF LEGAL ISSUES AND APPLICATION OF LAW:

The gain/loss on sale of share would be:

(Sale Proceeds from Shares – Brokerage on sales) – Cost Price

= 50% {((1000*50.85)-2%) – 1000*3.5}

= 50% (49,833 – 3,500)

= 50% * 46,333

= $23,166.50

CONCLUSION:

The Capital Gain on sale of Shares amounts to $23,166.50.

SALE OF STAMP COLLECTION:

The stamps being collected by one are included as collection of collectables (L Burman

and W Randolph, 1994).

MATERIAL FACT:

The stamps purchased at $60,000 was being sold for $50,000 thereby having loss on sale

of it.

6

Charges paid towards Stamp Duty $5,000

Amount paid as Legal fees $10,000

Amount paid as Loan $32,000

Council, water rates and insurance $22,000

Legal Fees for clearing dispute $5,000

Cost of removing pine trees $27,500

Cost of advertisement, legal and agent

fees on sale of land

$25,000

Total Cost of Land for CGT purposes $376,500

Thus the capital gains would be = Sale Price – Cost of Land = $1,000,000 - $376,500

= $623,500

CONCLUSION

Emma is subject to capital gains amounting to $623,500 on sale of the vacant land.

SALE OF 1000 SHARES BY EMMA:

The gain or loss on sale of share is computed by adjusting the cost price and the sale

price with amount if any paid towards the acquisition and selling the same respectively.

Moreover, the provisions of CGT also contains the fact that if the shares are being held for

more than 12 month then a discount of 50% is given on the gains so as to arrive at the

actual gains subject to Capital Gains Tax (D Halperin, 1991).

MATERIAL FACTS IN RELATION TO SHARES:

The shares of Rio Tinto was held for more than 12 months and thus holding period

discount of 50% would be applicable in this case.

ANALYSIS OF LEGAL ISSUES AND APPLICATION OF LAW:

The gain/loss on sale of share would be:

(Sale Proceeds from Shares – Brokerage on sales) – Cost Price

= 50% {((1000*50.85)-2%) – 1000*3.5}

= 50% (49,833 – 3,500)

= 50% * 46,333

= $23,166.50

CONCLUSION:

The Capital Gain on sale of Shares amounts to $23,166.50.

SALE OF STAMP COLLECTION:

The stamps being collected by one are included as collection of collectables (L Burman

and W Randolph, 1994).

MATERIAL FACT:

The stamps purchased at $60,000 was being sold for $50,000 thereby having loss on sale

of it.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ANALYSIS OF LEGAL ISSUES AND APPLICATION OF LAW:

As per the CGT law, the loss on sale of collectables can be set off from the gains from sale

of collectables only if two major conditions are satisfied which is that they have been

bought for less than $500 and are purchased before 16th December, 1995. In this case, no

condition is being satisfied and thus the loss would be not allowed to set off.

CONCLUSION:

The loss on sale of collectables will not be allowed to set off.

SALE OF GRAND PIANO FOR $30,000:

MATERIAL FACTS:

Loss on sale of Piano will not be allowed to set off assuming the fact that Emma is not a

professional piano player. (L Burman, K Clausing and J O’Hare, 1994).

ANALYSIS OF LEGAL ISSUES AND APPLICATION OF LAW:

The capital loss on sale of Piano would be $80,000 - $30,000 = $50,000

CONCLUSION:

Thus, the amount of $50,000 towards loss on sale of piano will be disregarded for CGT

purposes.

CONCLUSION:

The GST law has been analysed so as to analyse the entitlement of Input Tax Credit along

with the CGT provisions contained within the ITAA.

7

As per the CGT law, the loss on sale of collectables can be set off from the gains from sale

of collectables only if two major conditions are satisfied which is that they have been

bought for less than $500 and are purchased before 16th December, 1995. In this case, no

condition is being satisfied and thus the loss would be not allowed to set off.

CONCLUSION:

The loss on sale of collectables will not be allowed to set off.

SALE OF GRAND PIANO FOR $30,000:

MATERIAL FACTS:

Loss on sale of Piano will not be allowed to set off assuming the fact that Emma is not a

professional piano player. (L Burman, K Clausing and J O’Hare, 1994).

ANALYSIS OF LEGAL ISSUES AND APPLICATION OF LAW:

The capital loss on sale of Piano would be $80,000 - $30,000 = $50,000

CONCLUSION:

Thus, the amount of $50,000 towards loss on sale of piano will be disregarded for CGT

purposes.

CONCLUSION:

The GST law has been analysed so as to analyse the entitlement of Input Tax Credit along

with the CGT provisions contained within the ITAA.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES:

1. Aaron Henry, 1974.The property tax: progressive or regressive? A new view of

property tax incidence. American Economic Association Volume 64, Number 2, pp

212-221

2. Anderson John E., 1993. Use-Value Property Tax Assessment: Effects on Land

Development, Land Economics, Volume 69, Number 3, pp 263-269

3. Bradbury Katharine L., and Mayer Christopher J., and Case Karl E., 2000. Property

tax limits, local fiscal behaviour, and property values: evidence from Massachusetts

under proposition 2.5, Journal of Public Economics, Volume 80, pp 287-311

4. CCH, 2011. Australian Income Tax Legislation, Volumes 1 to 3, Sydney

5. A Auerbach, 1991. “Retrospective Capital Gains Taxation” ,81 American Economic

Review 167

6. D Halperin, 1991. “Saving the Income Tax: An Agenda for Research” above n 24.

7. L Burman and W Randolph, 1994. “Measuring Permanent Responses to Capital-

Gains Tax Changes in PanelData” 84 American Economic Review 794.

8. L Burman, K Clausing and J O’Hare, 1994. “Tax Reform and Realizations of Capital

Gains in 1986” 47 National Tax Journal 1.

8

1. Aaron Henry, 1974.The property tax: progressive or regressive? A new view of

property tax incidence. American Economic Association Volume 64, Number 2, pp

212-221

2. Anderson John E., 1993. Use-Value Property Tax Assessment: Effects on Land

Development, Land Economics, Volume 69, Number 3, pp 263-269

3. Bradbury Katharine L., and Mayer Christopher J., and Case Karl E., 2000. Property

tax limits, local fiscal behaviour, and property values: evidence from Massachusetts

under proposition 2.5, Journal of Public Economics, Volume 80, pp 287-311

4. CCH, 2011. Australian Income Tax Legislation, Volumes 1 to 3, Sydney

5. A Auerbach, 1991. “Retrospective Capital Gains Taxation” ,81 American Economic

Review 167

6. D Halperin, 1991. “Saving the Income Tax: An Agenda for Research” above n 24.

7. L Burman and W Randolph, 1994. “Measuring Permanent Responses to Capital-

Gains Tax Changes in PanelData” 84 American Economic Review 794.

8. L Burman, K Clausing and J O’Hare, 1994. “Tax Reform and Realizations of Capital

Gains in 1986” 47 National Tax Journal 1.

8

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.