Taxation Theory, Practice, and Law: Tutorial Questions Assignment

VerifiedAdded on 2022/12/27

|8

|1276

|86

Homework Assignment

AI Summary

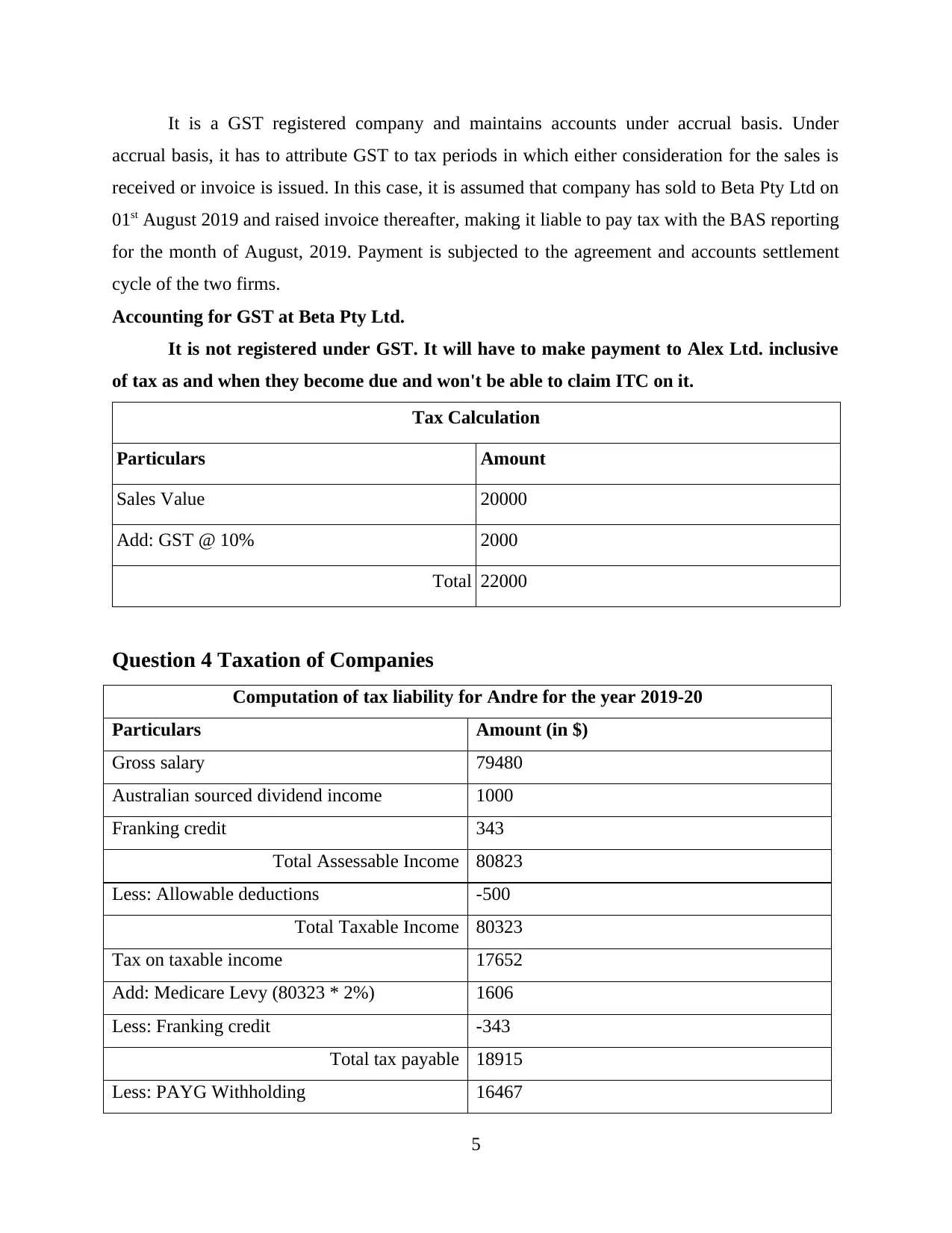

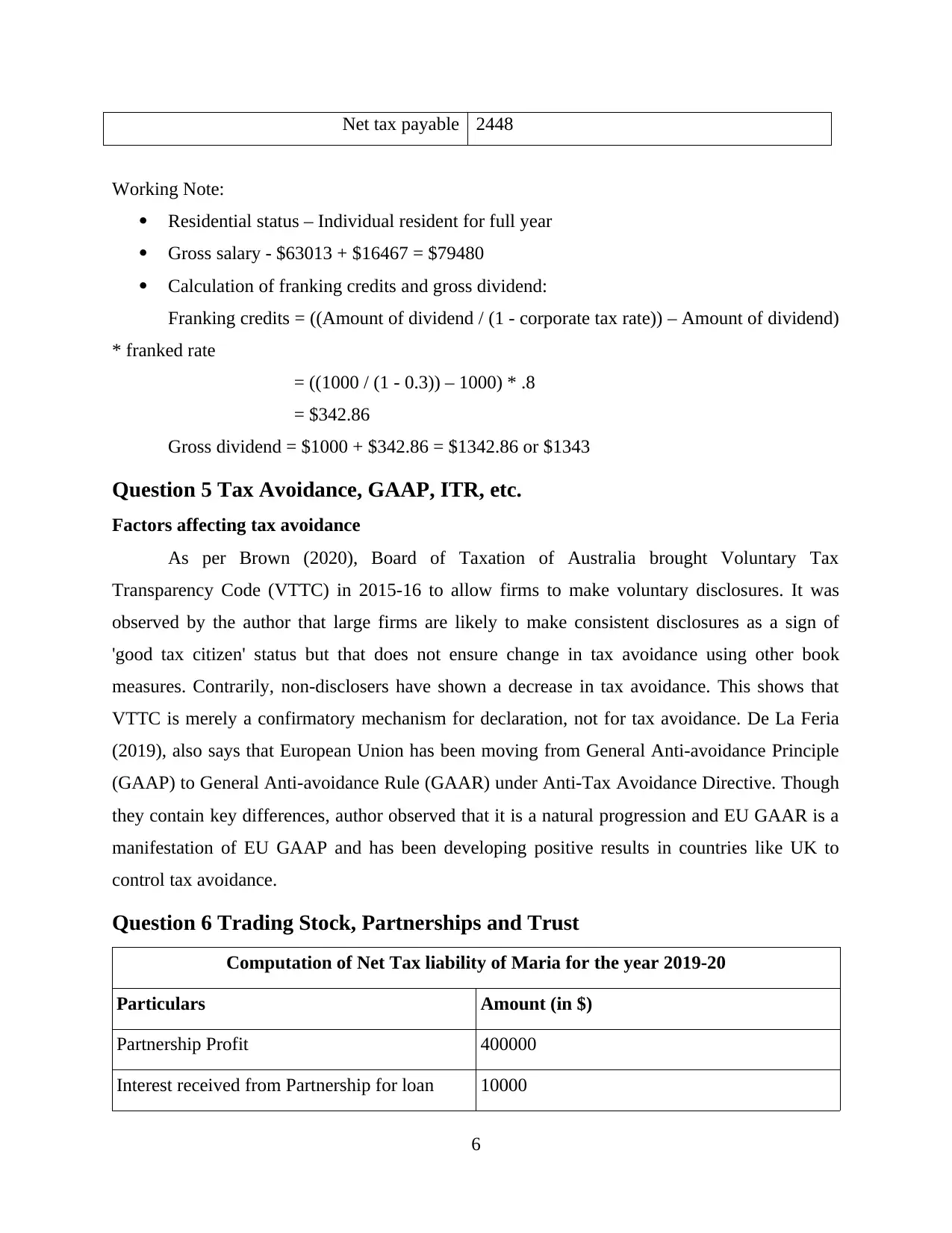

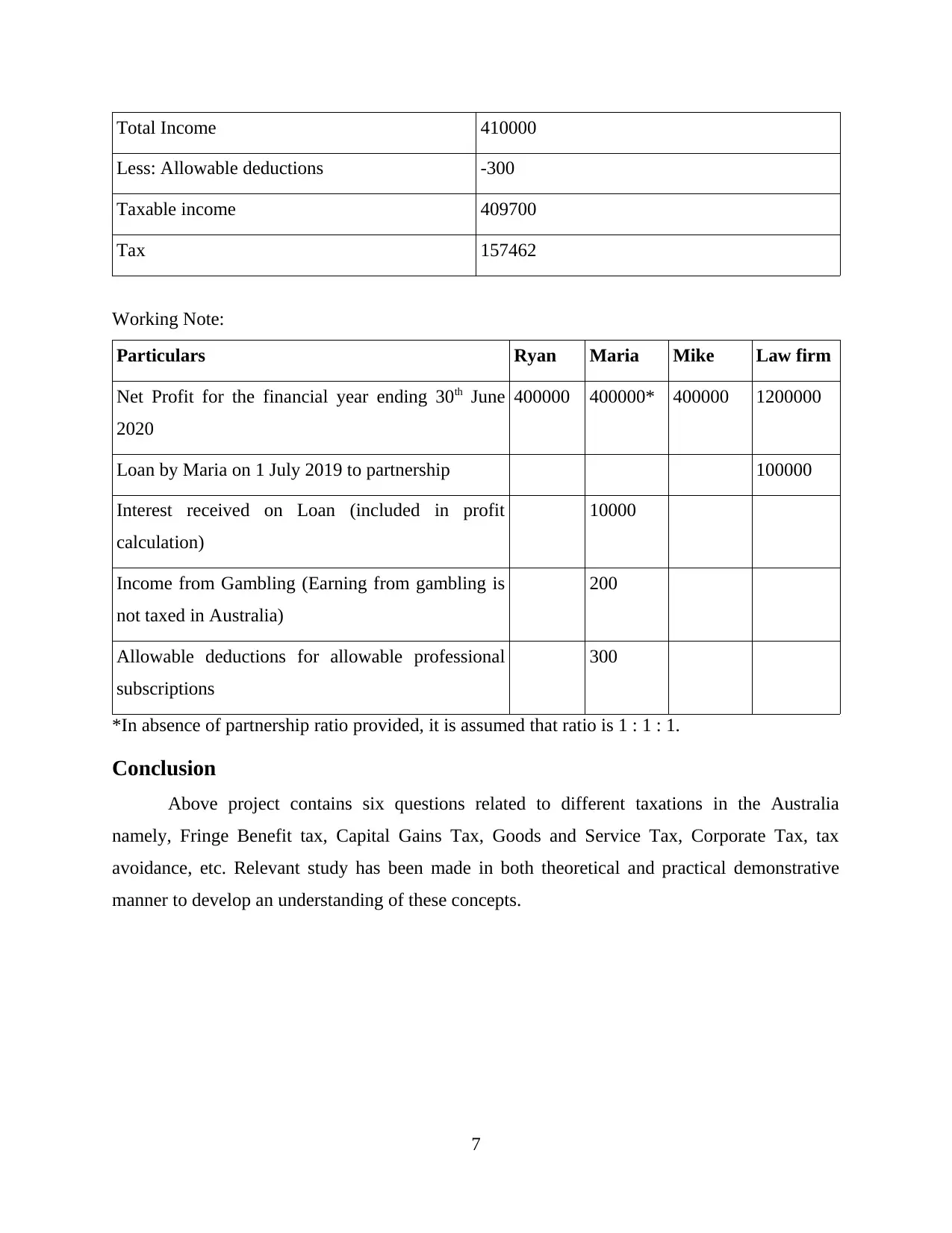

This document provides a comprehensive solution to a taxation assignment, addressing various aspects of the Australian tax system. The assignment covers six key questions, including fringe benefits tax (FBT), capital gains tax (CGT), goods and services tax (GST), taxation of companies, tax avoidance, and the taxation of trading stock, partnerships, and trusts. Each question is thoroughly analyzed, with relevant facts, rules, and calculations presented to support the conclusions. The solution includes practical examples and calculations to demonstrate the application of tax principles. Furthermore, the assignment explores the Voluntary Tax Transparency Code and the progression from GAAP to GAAR in the context of tax avoidance. The document concludes with a summary of the key concepts and a list of references used in the analysis.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.