Taxation Theory, Practice & Law: Fringe Benefits and Capital Gain

VerifiedAdded on 2023/01/06

|8

|2257

|71

Report

AI Summary

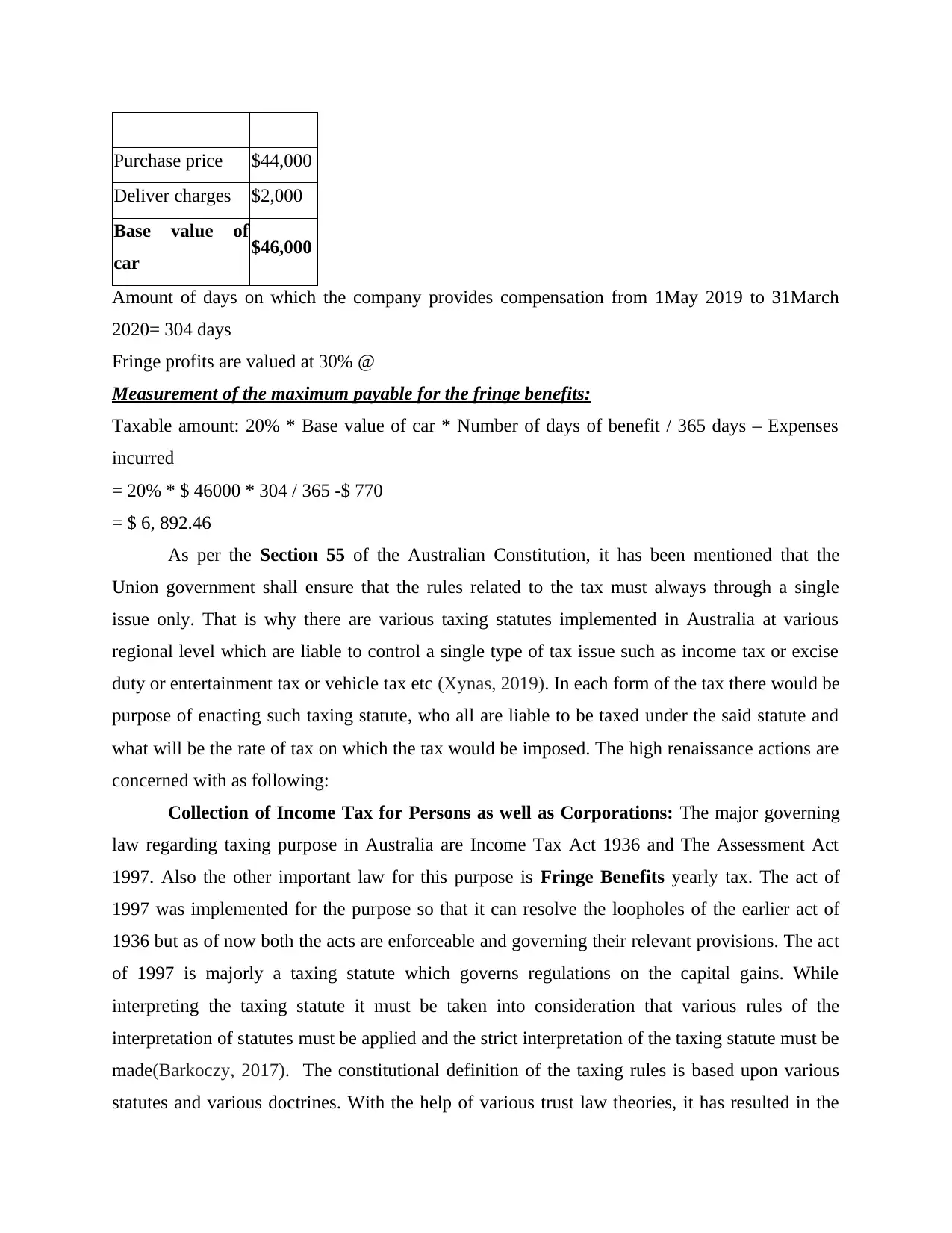

This report provides a comprehensive analysis of taxation principles, specifically focusing on Fringe Benefits Tax (FBT) and Capital Gain Tax (CGT) within the Australian context. It begins with an introduction to taxation, its importance, and the interpretation of taxing statutes. The main body of the report addresses two key questions. The first question calculates the fringe benefits tax liability for a car provided by a company, considering base value, usage days, and expenses. The second question delves into capital gains tax, detailing the calculation of capital gains from the sale of various assets, including an antique painting, car, Harry Potter collection, gold necklace, and sculpture. The report considers the relevant legislations and case law for the calculations and concludes with a summary of the findings and the significance of taxation in the financial system. The report also examines the application of relevant taxation legislations and principles to real-world scenarios, offering a practical understanding of tax implications for individuals and organizations.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.