Taxation Theory, Practice, and Law

VerifiedAdded on 2019/10/31

|13

|2561

|155

Homework Assignment

AI Summary

This homework assignment addresses several taxation questions based on Australian tax law. The assignment tackles issues such as capital gains tax set-off, fringe benefit tax calculation, loss distribution in joint ownership of rental property, tax evasion strategies, and the assessment of tax from timber sales. Each question involves identifying relevant laws (sections of the ITAA 1997, relevant rulings, and case law), applying those laws to the facts, and reaching a conclusion. The assignment demonstrates a strong understanding of Australian taxation principles and their practical application. The website provides this solved assignment as a resource for students.

Running head: TAXATION THEORY, PRACTICE AND LAW

Taxation Theory, Practice and Law

Name of the Student

Name of the University

Author’s Note

Taxation Theory, Practice and Law

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION THEORY, PRACTICE AND LAW

Table of Contents

Answer to Question 1......................................................................................................................2

Answer to Question 2......................................................................................................................3

Answer to Question 3......................................................................................................................5

Answer to Question 4......................................................................................................................6

Answer to Question 5......................................................................................................................7

References......................................................................................................................................10

Table of Contents

Answer to Question 1......................................................................................................................2

Answer to Question 2......................................................................................................................3

Answer to Question 3......................................................................................................................5

Answer to Question 4......................................................................................................................6

Answer to Question 5......................................................................................................................7

References......................................................................................................................................10

2TAXATION THEORY, PRACTICE AND LAW

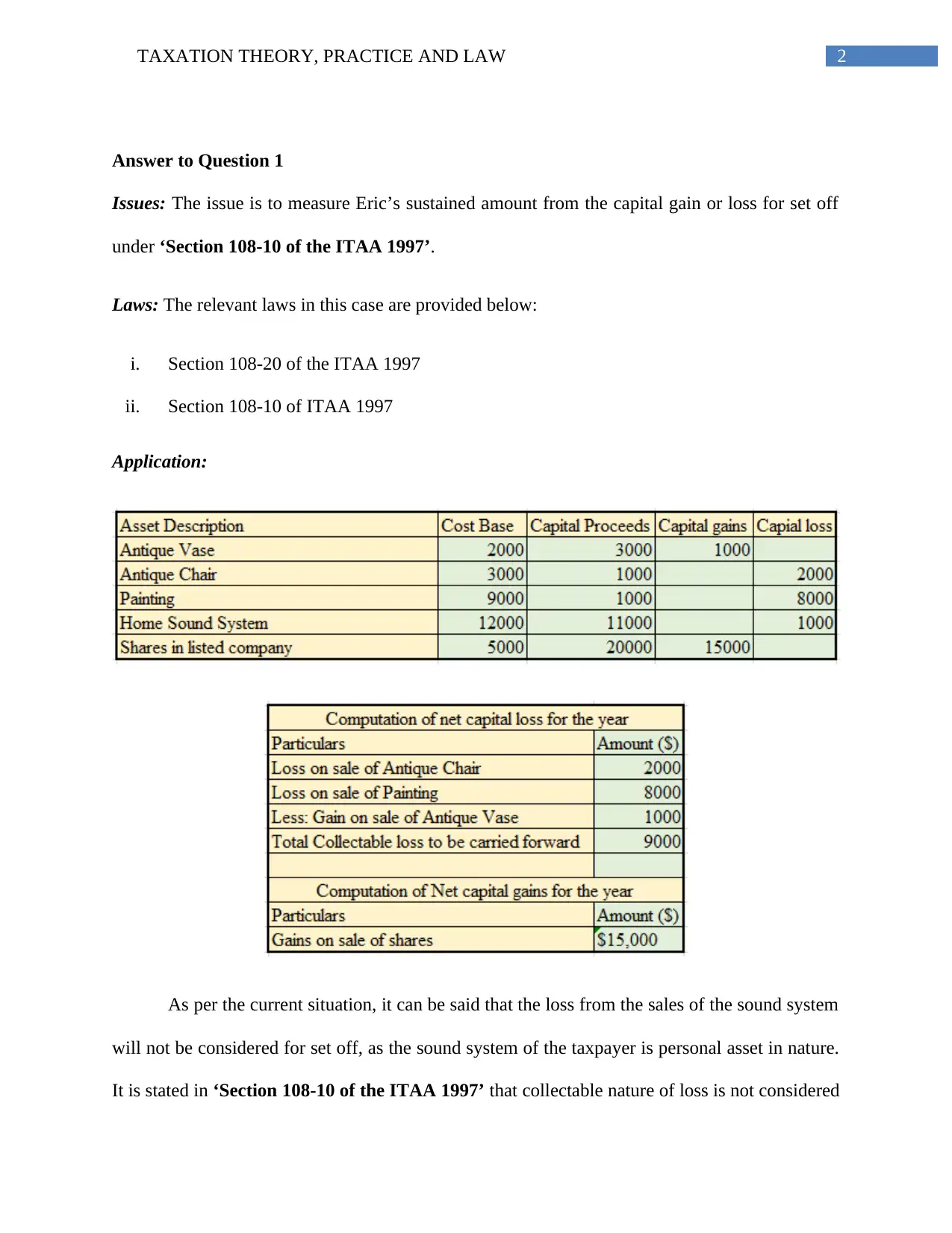

Answer to Question 1

Issues: The issue is to measure Eric’s sustained amount from the capital gain or loss for set off

under ‘Section 108-10 of the ITAA 1997’.

Laws: The relevant laws in this case are provided below:

i. Section 108-20 of the ITAA 1997

ii. Section 108-10 of ITAA 1997

Application:

As per the current situation, it can be said that the loss from the sales of the sound system

will not be considered for set off, as the sound system of the taxpayer is personal asset in nature.

It is stated in ‘Section 108-10 of the ITAA 1997’ that collectable nature of loss is not considered

Answer to Question 1

Issues: The issue is to measure Eric’s sustained amount from the capital gain or loss for set off

under ‘Section 108-10 of the ITAA 1997’.

Laws: The relevant laws in this case are provided below:

i. Section 108-20 of the ITAA 1997

ii. Section 108-10 of ITAA 1997

Application:

As per the current situation, it can be said that the loss from the sales of the sound system

will not be considered for set off, as the sound system of the taxpayer is personal asset in nature.

It is stated in ‘Section 108-10 of the ITAA 1997’ that collectable nature of loss is not considered

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION THEORY, PRACTICE AND LAW

for offset against the ordinary gains and thus, the profit from the sale of the shares will not be

considered for set off (Barnes and Stephens 2012). Again, as per ‘Section 108-10 of the ITAA

1997’, Eric’s profit from the sale of ordinary assets is raised from no assets of the current years.

Thus, the total amount of Eric’s capital gain is $15,000 (Jorgensen 2017).

Conclusion: Thus, it can be concluded that Eric is not able to set off the collectable loss as it is

generated from the ordinary nature of asserts.

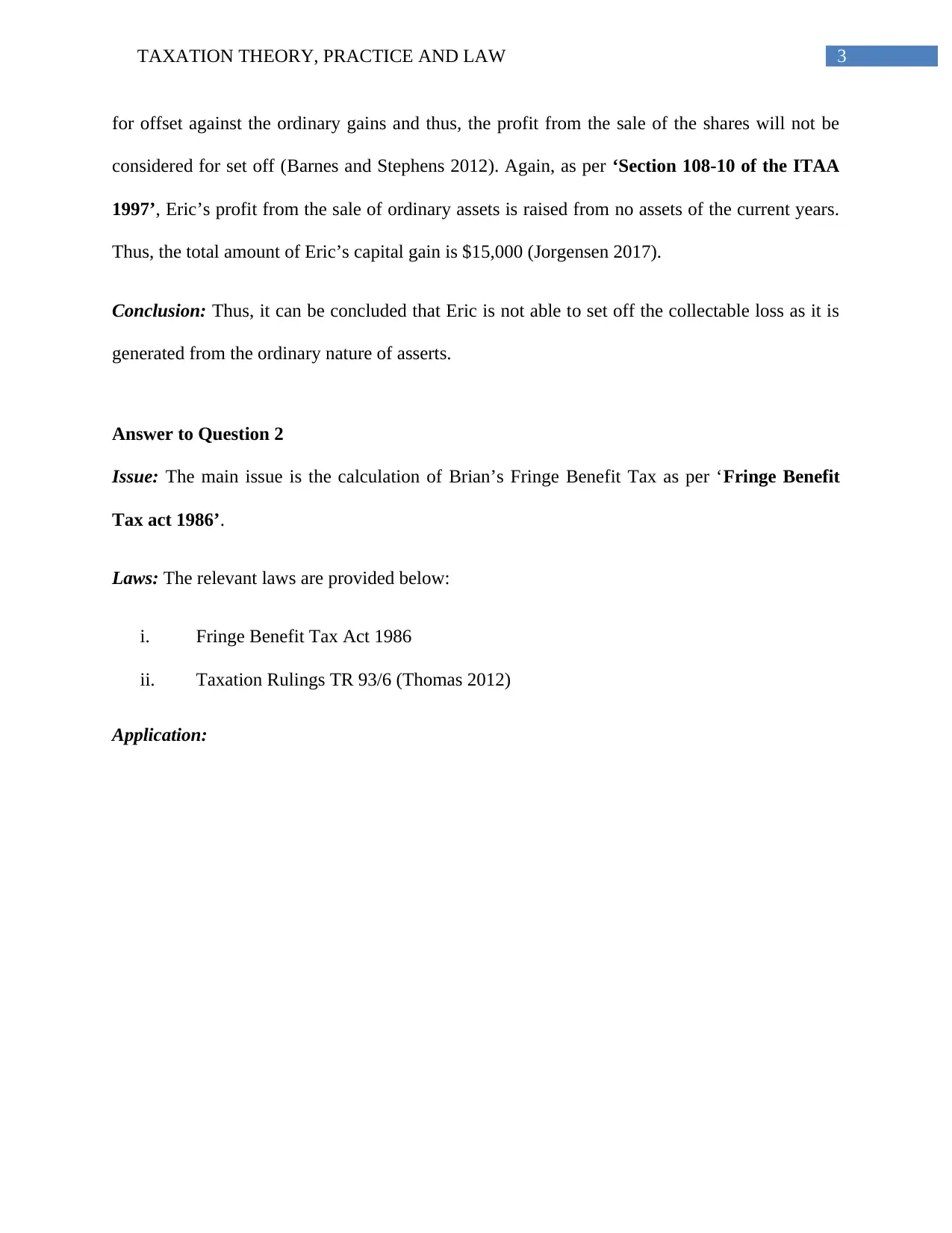

Answer to Question 2

Issue: The main issue is the calculation of Brian’s Fringe Benefit Tax as per ‘Fringe Benefit

Tax act 1986’.

Laws: The relevant laws are provided below:

i. Fringe Benefit Tax Act 1986

ii. Taxation Rulings TR 93/6 (Thomas 2012)

Application:

for offset against the ordinary gains and thus, the profit from the sale of the shares will not be

considered for set off (Barnes and Stephens 2012). Again, as per ‘Section 108-10 of the ITAA

1997’, Eric’s profit from the sale of ordinary assets is raised from no assets of the current years.

Thus, the total amount of Eric’s capital gain is $15,000 (Jorgensen 2017).

Conclusion: Thus, it can be concluded that Eric is not able to set off the collectable loss as it is

generated from the ordinary nature of asserts.

Answer to Question 2

Issue: The main issue is the calculation of Brian’s Fringe Benefit Tax as per ‘Fringe Benefit

Tax act 1986’.

Laws: The relevant laws are provided below:

i. Fringe Benefit Tax Act 1986

ii. Taxation Rulings TR 93/6 (Thomas 2012)

Application:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION THEORY, PRACTICE AND LAW

As per the guidelines of ‘Taxation Rulings of the TR 93/6’, individuals can avails the

opportunity for tax off set on the payments of interests on the loans taken from different kinds of

financial institutes like banks and others (Lignier and Evans 2012). This particular ruling also

provides the customers with the opportunity that there are not any needs for profits derived from

other events for the making of such payments. According to ‘Taxation Rulings of the TR 93/6’,

in case the bank discharges Brian from the payments of interest at the end of the loan tenure,

Brian is not required to pay the tax (Saad 2014).

Conclusion: Thus, based on the above discussion, it can be said that in case the bank instructs

Brian to pay the interest at the end of the year, Brian will not have to pay any kinds of interest to

the bank.

As per the guidelines of ‘Taxation Rulings of the TR 93/6’, individuals can avails the

opportunity for tax off set on the payments of interests on the loans taken from different kinds of

financial institutes like banks and others (Lignier and Evans 2012). This particular ruling also

provides the customers with the opportunity that there are not any needs for profits derived from

other events for the making of such payments. According to ‘Taxation Rulings of the TR 93/6’,

in case the bank discharges Brian from the payments of interest at the end of the loan tenure,

Brian is not required to pay the tax (Saad 2014).

Conclusion: Thus, based on the above discussion, it can be said that in case the bank instructs

Brian to pay the interest at the end of the year, Brian will not have to pay any kinds of interest to

the bank.

5TAXATION THEORY, PRACTICE AND LAW

Answer to Question 3

Issue: In this case, the issue is the distribution of loss sustained by Jack and Jill from the joint

ownership of the rental property.

Laws: The required laws are provided below:

i. FC of T v McDonald

ii. Section 51 of the ITAA 1997

iii. Taxation ruling TR 93/23

Application: ‘Taxation Ruling TR 93/32’ contains the definition and explanation about the

division of profit or loss derived from the property of rent of the joint owners of the same

property (Oats 2012). Apart from this, this particular ruling also provides the explanation about

the position of the co-owners that do not have the responsibility under the continuation of the

defined business activities. The basis of evaluation of Jack and Jill is their assessable position

from the rented property of theirs. In this regard, it needs to be mentioned that Jack will be

eligible for 10% of the business and Jill will be eligible for 90% profit of the business (Devos

2012).

Under section ‘TR 92/32’, joint ownership of rental repertoires is defined as the

partnership for the purpose of income tax (Barkoczy 2016). However, it is not concerned with

the partnership as per the definition of general law. No joint ownership of any business activities

for the purpose of income tax is included in this particular ruling. The administration of the loss

of income from the joint ownership will be done based on allocation of profit and loss of the

partnership. From the provided case study of Jack and Jill, it can be seen that the joint ownership

Answer to Question 3

Issue: In this case, the issue is the distribution of loss sustained by Jack and Jill from the joint

ownership of the rental property.

Laws: The required laws are provided below:

i. FC of T v McDonald

ii. Section 51 of the ITAA 1997

iii. Taxation ruling TR 93/23

Application: ‘Taxation Ruling TR 93/32’ contains the definition and explanation about the

division of profit or loss derived from the property of rent of the joint owners of the same

property (Oats 2012). Apart from this, this particular ruling also provides the explanation about

the position of the co-owners that do not have the responsibility under the continuation of the

defined business activities. The basis of evaluation of Jack and Jill is their assessable position

from the rented property of theirs. In this regard, it needs to be mentioned that Jack will be

eligible for 10% of the business and Jill will be eligible for 90% profit of the business (Devos

2012).

Under section ‘TR 92/32’, joint ownership of rental repertoires is defined as the

partnership for the purpose of income tax (Barkoczy 2016). However, it is not concerned with

the partnership as per the definition of general law. No joint ownership of any business activities

for the purpose of income tax is included in this particular ruling. The administration of the loss

of income from the joint ownership will be done based on allocation of profit and loss of the

partnership. From the provided case study of Jack and Jill, it can be seen that the joint ownership

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION THEORY, PRACTICE AND LAW

develops the foundation of income tax and thus, it will not be considered as the partnership as

per the principles of general law (Saad 2014).

Under ‘Taxation ruling TR 92/32’, it is explained that the joint ownership of the rental

properties will not be considered as partnership as per the regulation of general law (Taylor and

Richardson 2012). The agreement of partnership between Jack and Jill includes either written or

verbal agreement that do not have any effect on the sharing of incomes and losses from that

particular property. As per the agreement, Jack will be eligible for 100% of the loss from the

rental property. In the case of ‘FC of T v McDonald (1987)’, it can be seen that as per the

agreement, Mr. McDonald is entitled for 25% of the profit where Mrs. McDonald will get rest

75% of the profit from the property. Thus, in case of losses, Mr. McDonald has to bear 100% of

the losses from the property. This was done for the advancement of his wife’s income and to

indemnify the amount of losses. In case of Jack and Jill, it is a partnership under the general law

and thus, both jack and Jill need to bear the amount of loss equally (Latimer 2012).

Conclusion: From the above discussion, it can be concluded that it is required for Jack and Jill

need to bear the loss equally. In addition, the partnership between Jack and Jill will not be

considered as general partnership under general law.

Answer to Question 4

One of the major rulings that provide the confirmation of tax evasion is taken as

acceptable as well as legal and this was originated in the case of ‘IRC v Duke Westminster

(1936)’ (Van Weeghel and Emmerink 2013). As per the case, the Duke of Westminster used to

pay the wages of his gardener on weekly basis. After that, he entered into a new contract to

develops the foundation of income tax and thus, it will not be considered as the partnership as

per the principles of general law (Saad 2014).

Under ‘Taxation ruling TR 92/32’, it is explained that the joint ownership of the rental

properties will not be considered as partnership as per the regulation of general law (Taylor and

Richardson 2012). The agreement of partnership between Jack and Jill includes either written or

verbal agreement that do not have any effect on the sharing of incomes and losses from that

particular property. As per the agreement, Jack will be eligible for 100% of the loss from the

rental property. In the case of ‘FC of T v McDonald (1987)’, it can be seen that as per the

agreement, Mr. McDonald is entitled for 25% of the profit where Mrs. McDonald will get rest

75% of the profit from the property. Thus, in case of losses, Mr. McDonald has to bear 100% of

the losses from the property. This was done for the advancement of his wife’s income and to

indemnify the amount of losses. In case of Jack and Jill, it is a partnership under the general law

and thus, both jack and Jill need to bear the amount of loss equally (Latimer 2012).

Conclusion: From the above discussion, it can be concluded that it is required for Jack and Jill

need to bear the loss equally. In addition, the partnership between Jack and Jill will not be

considered as general partnership under general law.

Answer to Question 4

One of the major rulings that provide the confirmation of tax evasion is taken as

acceptable as well as legal and this was originated in the case of ‘IRC v Duke Westminster

(1936)’ (Van Weeghel and Emmerink 2013). As per the case, the Duke of Westminster used to

pay the wages of his gardener on weekly basis. After that, he entered into a new contract to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION THEORY, PRACTICE AND LAW

cancel the existing covenant and to stop the current payment in order to pay an equivalent

amount. However, the gardener was yet to receive the whole amount while Duke enjoyed the

advantage of tax benefits, as due to the new agreement, Duke was able to reduce the status of

their tax liability status. The particular case states that it is the right of each individual to know

his/her tax affairs as under this act, the amount of tax would be lower than other cases. Thus, one

cannot force an individual to pay increased amount of tax (Sceales 2015).

On the application of the fact in the provided case, it can be seen that a person is

successful to tax order in order to obtain the particular result, and then in ingenuity, the person

will be forced to pay the increases amount of tax. The verdict of this particular case states that an

individual has the opportunity to reduce the amount of their tax liabilities as per the agreement of

the law of financial framework (Bardopoulos 2015).

Answer to Question 5

Issue: The issue in this case is related with the assessment of tax from the cutting down of

timbers under ‘Subsection 6 (1) of the ITAA 1997’.

Laws: The required laws are mentioned below:

i. Subsection 6 (1) of the ITAA 1936

ii. McCauley v FC of T

Application: As per the provided case study, it can be seen that Bill is an owner of land that has

many numbers of pine trees. Initially, he took the decision to clear the land in order to gaze

sheep. However, a logging company approached Bill to pay $1000 for every meter of timber of

the pine trees of Bill’s land.

cancel the existing covenant and to stop the current payment in order to pay an equivalent

amount. However, the gardener was yet to receive the whole amount while Duke enjoyed the

advantage of tax benefits, as due to the new agreement, Duke was able to reduce the status of

their tax liability status. The particular case states that it is the right of each individual to know

his/her tax affairs as under this act, the amount of tax would be lower than other cases. Thus, one

cannot force an individual to pay increased amount of tax (Sceales 2015).

On the application of the fact in the provided case, it can be seen that a person is

successful to tax order in order to obtain the particular result, and then in ingenuity, the person

will be forced to pay the increases amount of tax. The verdict of this particular case states that an

individual has the opportunity to reduce the amount of their tax liabilities as per the agreement of

the law of financial framework (Bardopoulos 2015).

Answer to Question 5

Issue: The issue in this case is related with the assessment of tax from the cutting down of

timbers under ‘Subsection 6 (1) of the ITAA 1997’.

Laws: The required laws are mentioned below:

i. Subsection 6 (1) of the ITAA 1936

ii. McCauley v FC of T

Application: As per the provided case study, it can be seen that Bill is an owner of land that has

many numbers of pine trees. Initially, he took the decision to clear the land in order to gaze

sheep. However, a logging company approached Bill to pay $1000 for every meter of timber of

the pine trees of Bill’s land.

8TAXATION THEORY, PRACTICE AND LAW

The taxation regulation under ‘Taxation ruling TR 95/6’ deals the rise in income from

the primary production activities and the forestry activities. This also includes the level or degree

until which the income of the individual from forestry is assessable under income tax. This law is

applicable in both the cases for the individual taxpayers that are involvement in the forestry

activities and primary production from disposing of timbers. As per the explanation in

‘Subsection 6 (1) of the ITAA 1936’, the tax payer’s association with the forestry activities will

be considered as primary production as it has its involvements with the business operations of

the taxpayer (Russell 2016).

According to ‘Subsection 6 (1) of the ITAA 1997’, primary production refers to the

process to plant trees in the process of plantation and the intention behind this is vegetation.

Thus, based on this, it can be said that Bill is a primary producer as he has been engaged in

primary production to tend down the pine trees on his own land. Forest operation refers to the

planting and trending of trees for vegetation and there is not any importance of this fact that the

individual did not originally planted the trees (Russell 2016).

From the provided situation, it can be seen that Bill was not involved in the planting of

the trees. However, his received sums from the selling process of the timbers will be allowable

for the purpose of assessment. In spite of the presence of the fact that the sales amount includes

either fully or partially the portions of the assets having commercial value, the process to tend

the trees needs to be treated as receipts and thus, it will be considered as income under

‘Subsection 36 (1)’.

In the alternative scenario, in case the company paid the taxpayer with a large amount of

$50,000 in order to get the right to cut all the required timbers from Bill’s trees, then the receipt

The taxation regulation under ‘Taxation ruling TR 95/6’ deals the rise in income from

the primary production activities and the forestry activities. This also includes the level or degree

until which the income of the individual from forestry is assessable under income tax. This law is

applicable in both the cases for the individual taxpayers that are involvement in the forestry

activities and primary production from disposing of timbers. As per the explanation in

‘Subsection 6 (1) of the ITAA 1936’, the tax payer’s association with the forestry activities will

be considered as primary production as it has its involvements with the business operations of

the taxpayer (Russell 2016).

According to ‘Subsection 6 (1) of the ITAA 1997’, primary production refers to the

process to plant trees in the process of plantation and the intention behind this is vegetation.

Thus, based on this, it can be said that Bill is a primary producer as he has been engaged in

primary production to tend down the pine trees on his own land. Forest operation refers to the

planting and trending of trees for vegetation and there is not any importance of this fact that the

individual did not originally planted the trees (Russell 2016).

From the provided situation, it can be seen that Bill was not involved in the planting of

the trees. However, his received sums from the selling process of the timbers will be allowable

for the purpose of assessment. In spite of the presence of the fact that the sales amount includes

either fully or partially the portions of the assets having commercial value, the process to tend

the trees needs to be treated as receipts and thus, it will be considered as income under

‘Subsection 36 (1)’.

In the alternative scenario, in case the company paid the taxpayer with a large amount of

$50,000 in order to get the right to cut all the required timbers from Bill’s trees, then the receipt

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION THEORY, PRACTICE AND LAW

received from the logging company would be treated as ‘Royalties’. As per the regulation under

‘Section 26 (f)’, the received royalties from the timber of tending companies needs to be

considered as assessable income and this income needs to be included in the assessable income

of the individual for end of the financial year. Thus, for Bill, the amount of royalties from the

felling of timber needs to be considered to carry on the forestry business operations. In the case

of ‘McCauley v The Federal Commissioner of Taxation’ includes the payments received by

the grantor from the assignment of the rights from timber (Okmark 2014). Thus, based on the

above discussion, it can be said that amount of $50,000 received by Bill at once would be

considered as taxable income for the purpose of income tax under ‘Section 26 (f)’.

Conclusion: From the above discussion, it can be concluded that in the first case, the amount

received by Bill needs to be considered as taxable income for tax assessment. In the second case,

the amount received by Bill needs to be considered as royalties.

received from the logging company would be treated as ‘Royalties’. As per the regulation under

‘Section 26 (f)’, the received royalties from the timber of tending companies needs to be

considered as assessable income and this income needs to be included in the assessable income

of the individual for end of the financial year. Thus, for Bill, the amount of royalties from the

felling of timber needs to be considered to carry on the forestry business operations. In the case

of ‘McCauley v The Federal Commissioner of Taxation’ includes the payments received by

the grantor from the assignment of the rights from timber (Okmark 2014). Thus, based on the

above discussion, it can be said that amount of $50,000 received by Bill at once would be

considered as taxable income for the purpose of income tax under ‘Section 26 (f)’.

Conclusion: From the above discussion, it can be concluded that in the first case, the amount

received by Bill needs to be considered as taxable income for tax assessment. In the second case,

the amount received by Bill needs to be considered as royalties.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION THEORY, PRACTICE AND LAW

References

Bardopoulos, A.M., 2015. Tax Avoidance and Tax Evasion. In eCommerce and the Effects of

Technology on Taxation (pp. 337-341). Springer International Publishing.

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Barnes, J. and Stephens, M., 2012. Capital gains tax basics. Concise Collection of Tax

Fundamentals, A, p.91.

Devos, K., 2012. The impact of tax professionals upon the compliance behaviour of Australian

individual taxpayers. Revenue Law Journal, 22(1), p.31.

Jorgensen, R., 2017. Division 7A structuring: The contortionist revisited. Tax Specialist, 20(3),

p.118.

Latimer, P., 2012. Australian Business Law 2012. CCH Australia Limited.

Lignier, P. and Evans, C., 2012. The rise and rise of tax compliance costs for the small business

sector in Australia.

Oats, L. ed., 2012. Taxation: A fieldwork research handbook. Routledge.

OKMARK, L., 2014. " You Can't Handle the Truth"... Well, the States That Is: The Legality of

State-Imposed Transfer Taxes on Fannie Mae, Freddie Mac, and the Federal Housing Finance

Agency. N. ILL. UL REV. ONLINE J., 5, pp.91-91.

Russell, T., 2016. Trust beneficiaries and exemptions from CGT: Reflections on the Oswal

litigation. Taxation in Australia, 51(6), p.296.

References

Bardopoulos, A.M., 2015. Tax Avoidance and Tax Evasion. In eCommerce and the Effects of

Technology on Taxation (pp. 337-341). Springer International Publishing.

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Barnes, J. and Stephens, M., 2012. Capital gains tax basics. Concise Collection of Tax

Fundamentals, A, p.91.

Devos, K., 2012. The impact of tax professionals upon the compliance behaviour of Australian

individual taxpayers. Revenue Law Journal, 22(1), p.31.

Jorgensen, R., 2017. Division 7A structuring: The contortionist revisited. Tax Specialist, 20(3),

p.118.

Latimer, P., 2012. Australian Business Law 2012. CCH Australia Limited.

Lignier, P. and Evans, C., 2012. The rise and rise of tax compliance costs for the small business

sector in Australia.

Oats, L. ed., 2012. Taxation: A fieldwork research handbook. Routledge.

OKMARK, L., 2014. " You Can't Handle the Truth"... Well, the States That Is: The Legality of

State-Imposed Transfer Taxes on Fannie Mae, Freddie Mac, and the Federal Housing Finance

Agency. N. ILL. UL REV. ONLINE J., 5, pp.91-91.

Russell, T., 2016. Trust beneficiaries and exemptions from CGT: Reflections on the Oswal

litigation. Taxation in Australia, 51(6), p.296.

11TAXATION THEORY, PRACTICE AND LAW

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’ view. Procedia-

Social and Behavioral Sciences, 109, pp.1069-1075.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’ view. Procedia-

Social and Behavioral Sciences, 109, pp.1069-1075.

Sceales, R.W.F., 2015. A review of the trend in the judicial interpretation, and judicial attitudes

towards tax avoidance in the United Kingdom, Australia and South Africa, with reference to the"

declaratory" and" choice" theories of jurisprudence (Doctoral dissertation).

Taylor, G. and Richardson, G., 2012. International corporate tax avoidance practices: evidence

from Australian firms. The International Journal of Accounting, 47(4), pp.469-496.

Thomas, A., 2012. The elasticity of taxable income in New Zealand: Evidence from the 1986 tax

reform. New Zealand Economic Papers, 46(2), pp.159-167.

Van Weeghel, S. and Emmerink, F., 2013. Global Developments and Trends in International

Anti-Avoidance. Bulletin for International Taxation, 67(8), pp.428-435.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’ view. Procedia-

Social and Behavioral Sciences, 109, pp.1069-1075.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’ view. Procedia-

Social and Behavioral Sciences, 109, pp.1069-1075.

Sceales, R.W.F., 2015. A review of the trend in the judicial interpretation, and judicial attitudes

towards tax avoidance in the United Kingdom, Australia and South Africa, with reference to the"

declaratory" and" choice" theories of jurisprudence (Doctoral dissertation).

Taylor, G. and Richardson, G., 2012. International corporate tax avoidance practices: evidence

from Australian firms. The International Journal of Accounting, 47(4), pp.469-496.

Thomas, A., 2012. The elasticity of taxable income in New Zealand: Evidence from the 1986 tax

reform. New Zealand Economic Papers, 46(2), pp.159-167.

Van Weeghel, S. and Emmerink, F., 2013. Global Developments and Trends in International

Anti-Avoidance. Bulletin for International Taxation, 67(8), pp.428-435.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.