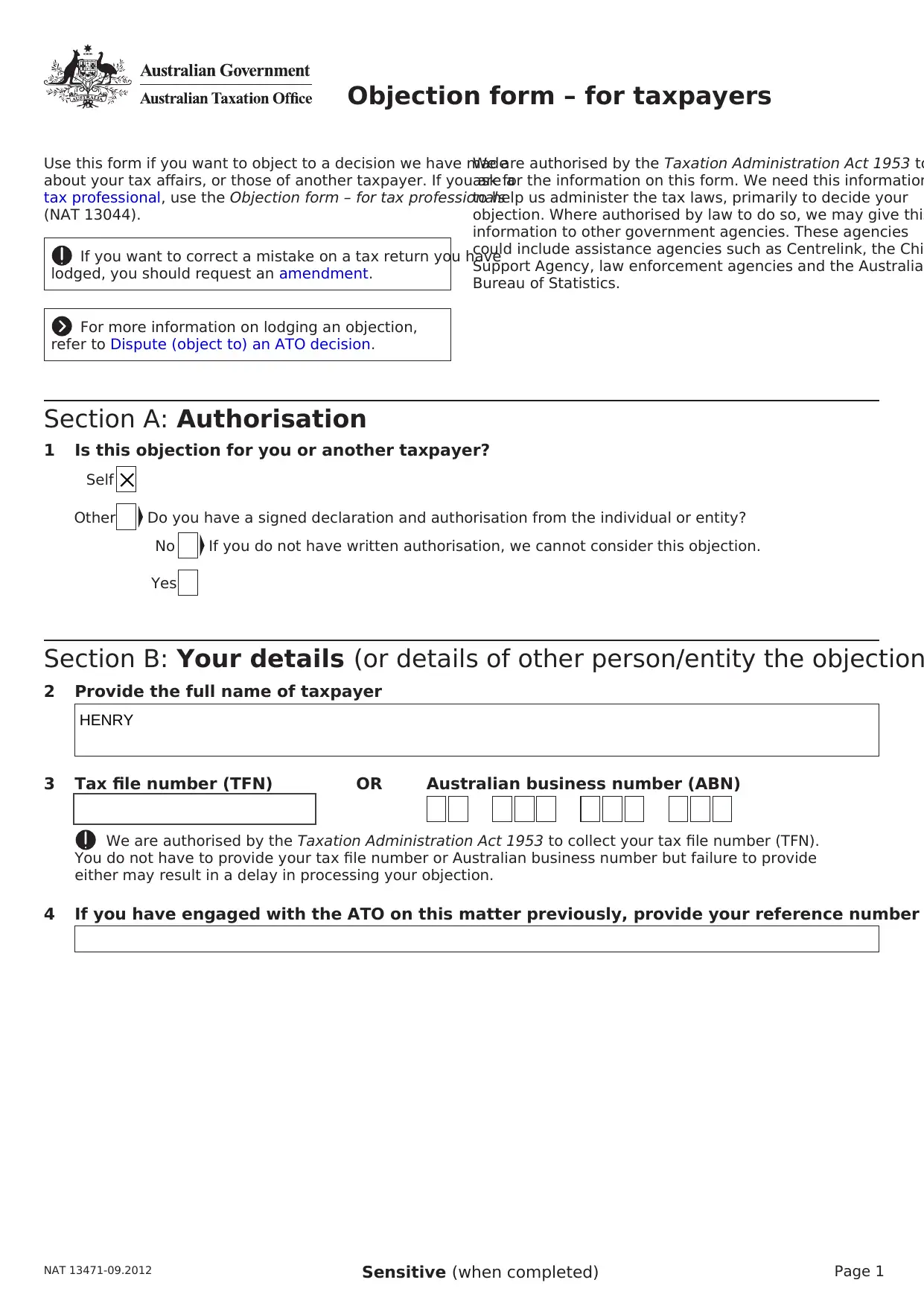

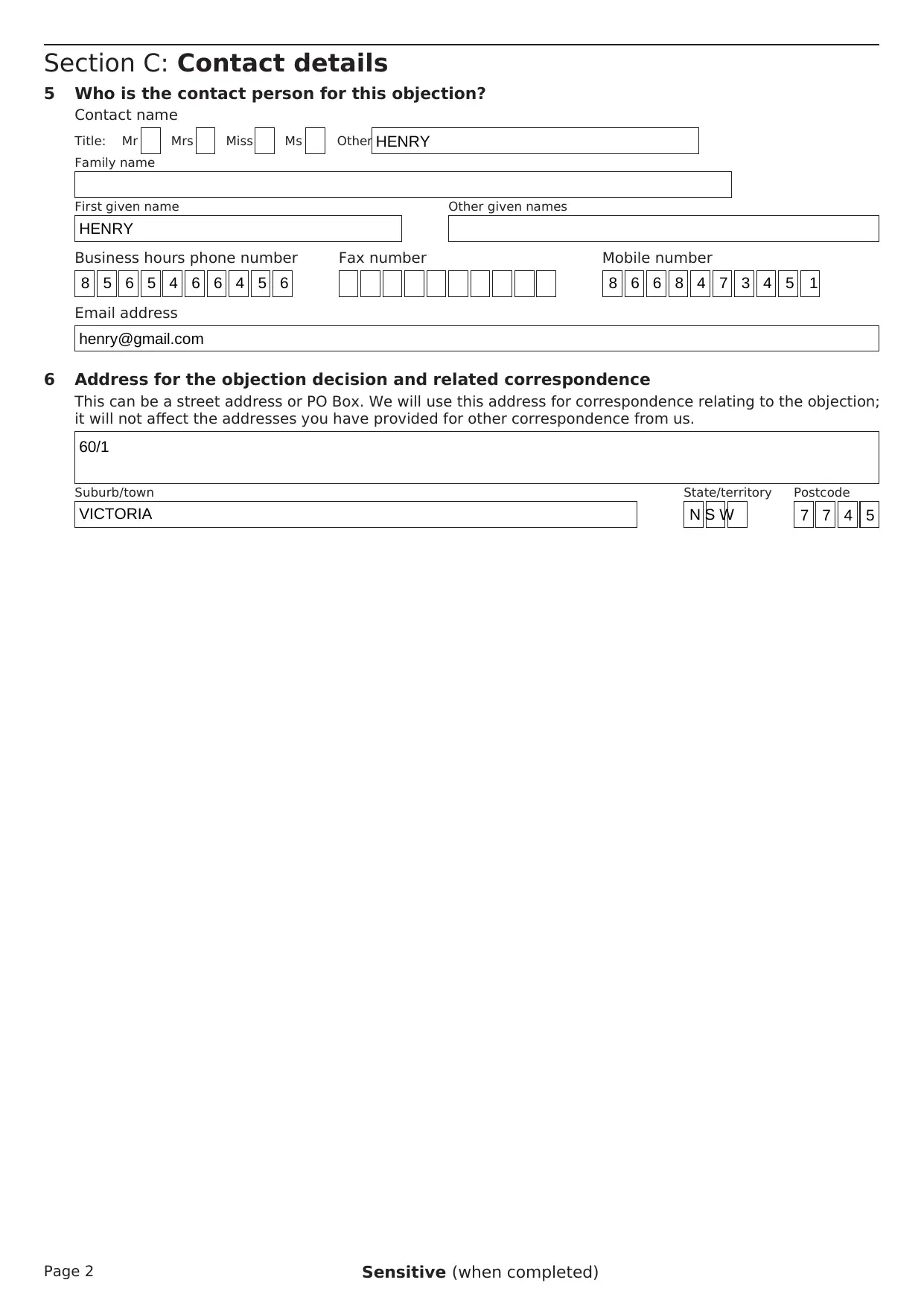

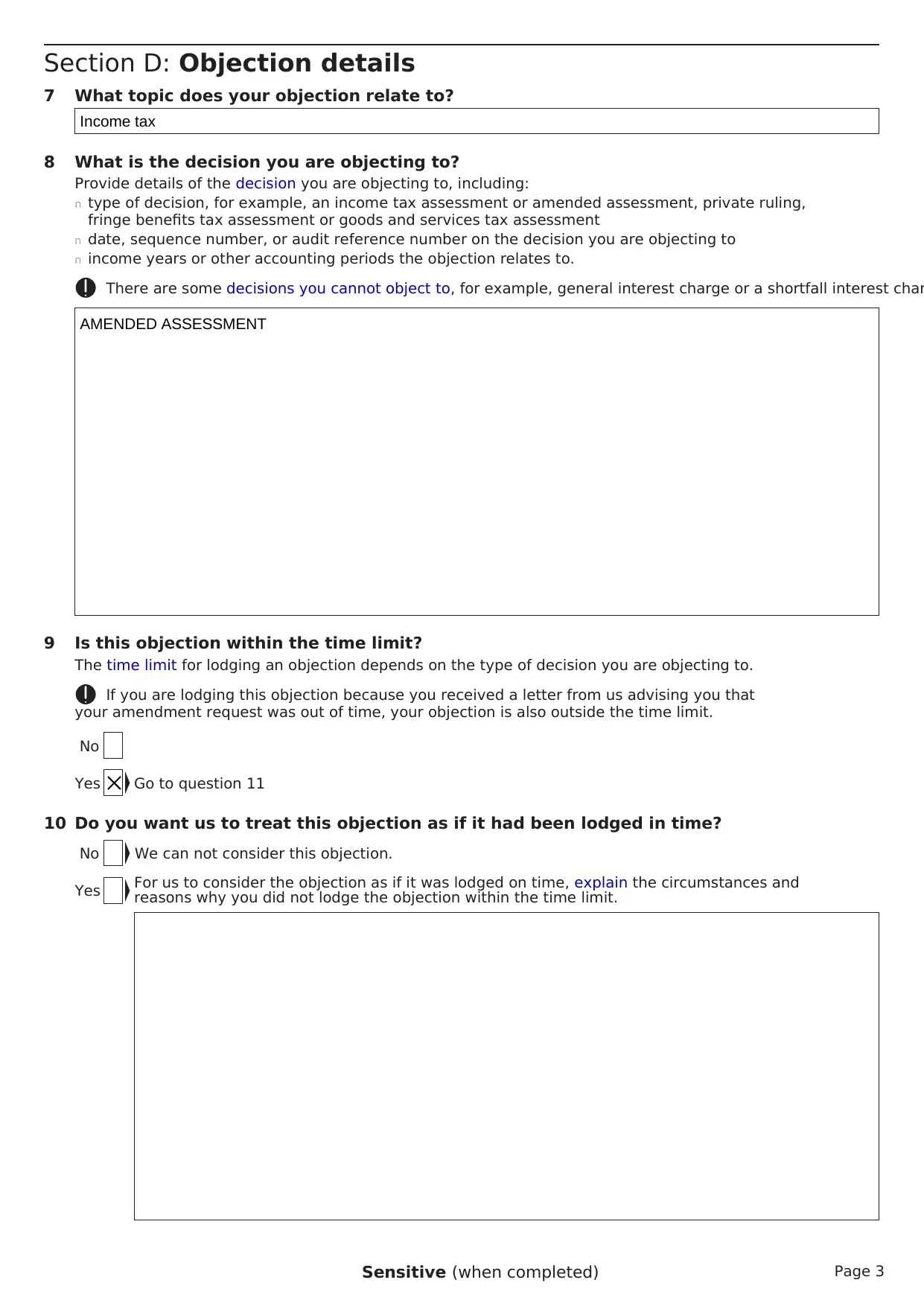

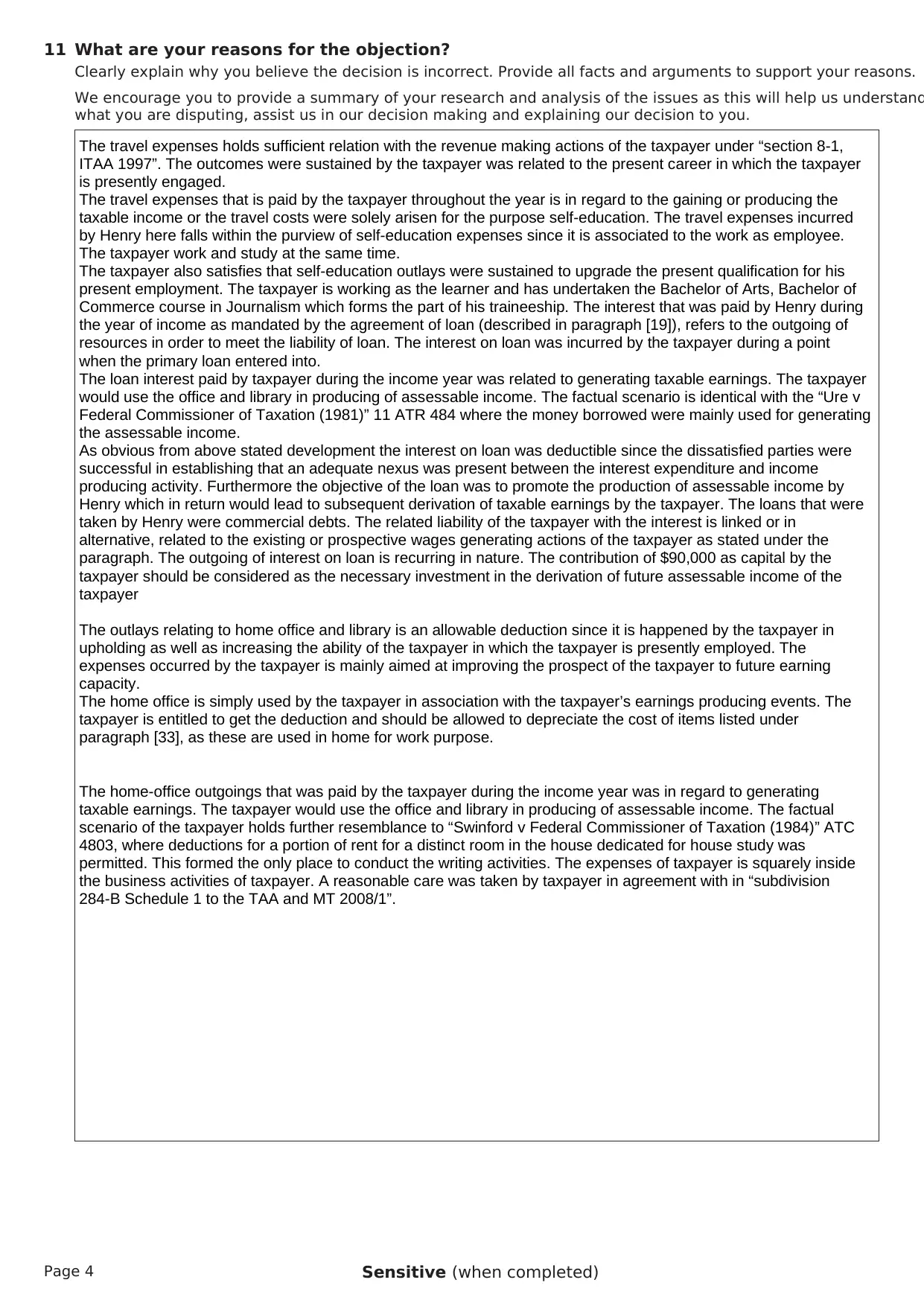

Tax Law Assignment: Objection Form and Letter for Henry's Tax Case

VerifiedAdded on 2022/11/30

|6

|2011

|343

Homework Assignment

AI Summary

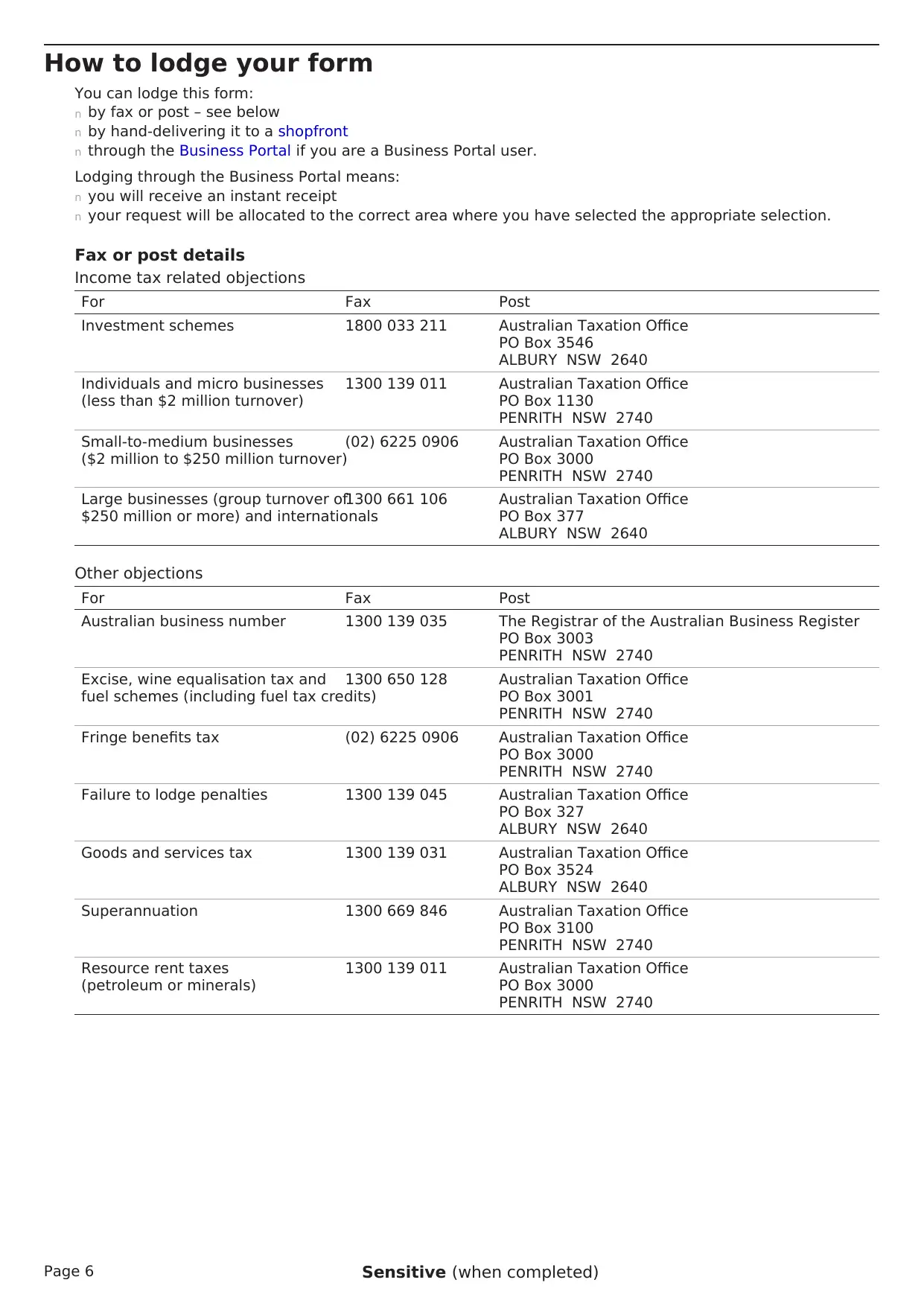

This assignment presents a tax objection case involving a taxpayer named Henry, who is objecting to an amended assessment by the Australian Taxation Office (ATO). The assignment includes a completed objection form detailing Henry's contact information, the decision being objected to, and the reasons for the objection. Henry argues that certain travel expenses, home office expenses, and loan interest should be deductible. The supporting arguments reference relevant sections of the Income Tax Assessment Act 1997 (ITAA 1997) and case law such as "Ure v Federal Commissioner of Taxation (1981)" and "Swinford v Federal Commissioner of Taxation (1984)" to support his claims. The assignment highlights the importance of providing supporting evidence and documentation, and it outlines the process for lodging the objection. The assignment also includes a letter format for communication with the Commissioner of Taxation and provides an overview of the objection process, emphasizing its complexity and the need for a strong legal foundation. The assignment also includes a marking guide that outlines the key elements of the assignment, including the use of the correct objection form, the correct statement of objection grounds, use of relevant legislation and cases, and the quality of the analysis and recommendations.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.