The Impossible Trinity and Taylor Rule for Singapore's Monetary Policy

VerifiedAdded on 2020/06/06

|19

|6037

|47

Essay

AI Summary

This essay critically investigates the effectiveness of the Taylor Rule in Singapore's open economy, addressing the challenges posed by the impossible trinity. It examines the Monetary Authority of Singapore's (MAS) current monetary policy framework, which focuses on maintaining the Singapore dollar's effective exchange rate (S$NEER). The study explores the trilemma, highlighting the trade-offs between exchange rate stability, independent monetary policy, and free capital flows. Applying the Taylor rule in Singapore, the paper assesses whether the MAS should utilize interest rates as an instrument instead of the exchange rate. The research considers the impact of productivity and foreign price shocks, concluding that the Taylor rule may be more effective in certain scenarios. The essay emphasizes that the MAS can leverage high exchange rates to manage interest rates and benefit from foreign capital flows, ensuring an appreciating exchange rate. The study concludes that there is no floating fear for Singapore with the Taylor rule.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

The Impossible Trinity

(Will Taylor Rule be better for Singapore?)

(Will Taylor Rule be better for Singapore?)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Abstract

Monetary policy is regarded as macroeconomic policy wherein the monetary authority

means central bank of the nation makes policies, rules and regulations to control the supply of

money in the country. Monetary Authority of Singapore (MAS) aims at keeping appreciation rate

of Singapore’s dollar effective exchange (S$NEER) rate at 0%. It follows inflation-targeting &

exchange rate focused monetary policy with free flow of capital and domestic interest rate is

determined through foreign interest rate comprising time-varying risk premium. Given an

impossible trinity, MAS can either choose exchange rate or interest rate as an instrument for the

monetary control. Applying the Taylor’s rule in Singapore, MAS needs to charge high rate of

interest so as to control money supply or vice-versa. Thus, the target of the study is to critically

investigate the Taylor’s rule in Singapore’s open economy through secondary analysis. The

finding of the thesis presented that in dominant productivity shocks Taylor’s interest rate rule is

considered as more effective, however, in case of dominant foreign price shocks, exchange rate

rule is preferable. Moreover, inflation significantly response to the import-price inflation shocks

in comparison to the exchange rate. The results concluded that there is no floating fear for the

Singapore with the Taylor rule because with the high exchange rate, MAS can improve policy

rates in order to derive benefits from the foreign flow of capital and assures appreciating

exchange rate in the future.

Monetary policy is regarded as macroeconomic policy wherein the monetary authority

means central bank of the nation makes policies, rules and regulations to control the supply of

money in the country. Monetary Authority of Singapore (MAS) aims at keeping appreciation rate

of Singapore’s dollar effective exchange (S$NEER) rate at 0%. It follows inflation-targeting &

exchange rate focused monetary policy with free flow of capital and domestic interest rate is

determined through foreign interest rate comprising time-varying risk premium. Given an

impossible trinity, MAS can either choose exchange rate or interest rate as an instrument for the

monetary control. Applying the Taylor’s rule in Singapore, MAS needs to charge high rate of

interest so as to control money supply or vice-versa. Thus, the target of the study is to critically

investigate the Taylor’s rule in Singapore’s open economy through secondary analysis. The

finding of the thesis presented that in dominant productivity shocks Taylor’s interest rate rule is

considered as more effective, however, in case of dominant foreign price shocks, exchange rate

rule is preferable. Moreover, inflation significantly response to the import-price inflation shocks

in comparison to the exchange rate. The results concluded that there is no floating fear for the

Singapore with the Taylor rule because with the high exchange rate, MAS can improve policy

rates in order to derive benefits from the foreign flow of capital and assures appreciating

exchange rate in the future.

Table of Contents

PART- I INTRODUCTION............................................................................................................1

Overview of the study..................................................................................................................1

Research aims and objectives......................................................................................................3

Research question........................................................................................................................3

Rationale of the study..................................................................................................................3

Structure of the dissertation.........................................................................................................4

PART – II LITERATURE REVIEW..............................................................................................4

1. Current monetary policy framework of Singapore and impossible trinity concept.................4

2. Application of Taylor’s rule in the monetary policy................................................................6

PART III: CONCLUSION............................................................................................................11

PART –IV REFERENCES............................................................................................................13

PART- I INTRODUCTION............................................................................................................1

Overview of the study..................................................................................................................1

Research aims and objectives......................................................................................................3

Research question........................................................................................................................3

Rationale of the study..................................................................................................................3

Structure of the dissertation.........................................................................................................4

PART – II LITERATURE REVIEW..............................................................................................4

1. Current monetary policy framework of Singapore and impossible trinity concept.................4

2. Application of Taylor’s rule in the monetary policy................................................................6

PART III: CONCLUSION............................................................................................................11

PART –IV REFERENCES............................................................................................................13

Table of Figures

Figure 1 Impossible Trinity........................................................................................................... 2

Figure 2 Mundell’s Impossible Trinity..........................................................................................6

Figure 1 Impossible Trinity........................................................................................................... 2

Figure 2 Mundell’s Impossible Trinity..........................................................................................6

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

PART- I INTRODUCTION

Overview of the study

Monetary policy is a part of macroeconomic strategies wherein the monetary authority

means central bank of the nation makes policies, rules and regulations to control the supply of

money in the country. The target of this is to control high rate of inflation and interest so as to

stabilize price & build trust in economy (Chen and et.al, 2016). In Singapore, central Bank is

responsible to make policies and regulations in regards to control the inflation rate by altering the

interest rate or exchange rate. Its monetary policy covers several aspects i.e. control foreign

exchange rate, open market operations, inflation rate and others. Monetary Authority of

Singapore (MAS) aims at keeping appreciation rate of Singapore’s dollar effective exchange

(S$NEER) rate at 0%. The authority also intervenes in keeping foreign exchange rate stabilized

so as to prevent the possibility of excessive volatility in the exchange rate. The policy considers

domestic rate of interest and monetary supply as an endogenous variables and therefore, money

market operations are carried out in order to ensure sufficient liquid availability. Thus, its

monetary policy is an inflation targeted strategy, in which, policy-makers make policies in order

to control the inflation (Mohan, Patra and Kapur, 2013).

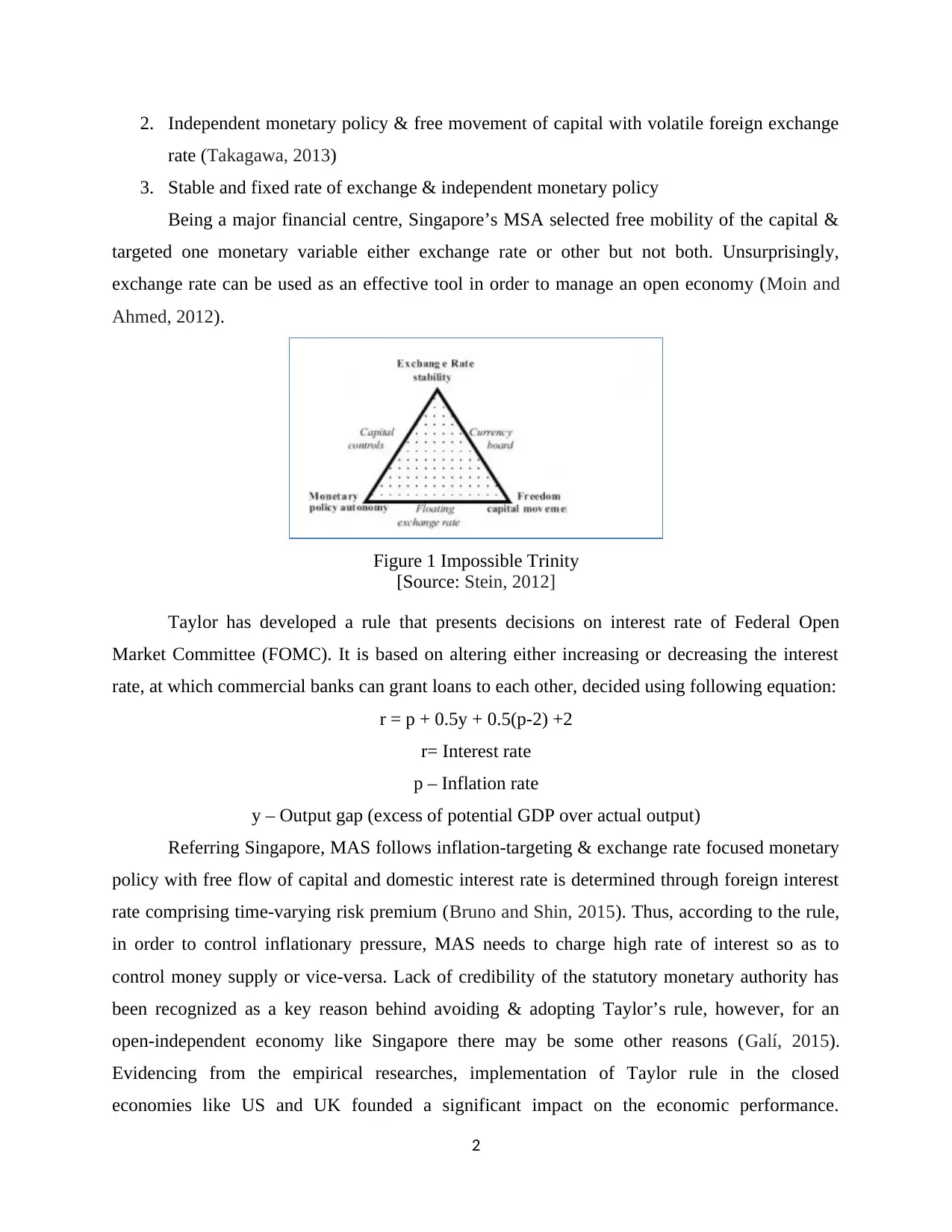

Applying the international economics concept of impossible Trinity, it presents that it is

impossible for every nation to have a fixed FOREX, free movement of capital and independent

monetary policy. Here, free capital flow is regarded as monetary movement for trade &

investment purpose, fixed FOREX rate indicates fixed exchange rate of one currency against the

value of other currency and last one sovereign monetary policy is the process wherein central

bank design policies so as to control the money supply in the nation (Cai and Pitsch, 2014). The

trilemma is also called Unholy Trinity and became popular as Mundell-Fleming model examine

the effectiveness of monetary policy of the country in an open economy with distinctive

exchange rate (Schularick and Taylor, 2012). Considering it in Singapore’s open economy, the

concept believes that it is impossible for the MSA to consider all of these three factors while

designing the monetary policy therefore; there are three choices available to the policymakers

presented below:

1. Stable rate of exchange & free capital flows but not an independent policy

1

Overview of the study

Monetary policy is a part of macroeconomic strategies wherein the monetary authority

means central bank of the nation makes policies, rules and regulations to control the supply of

money in the country. The target of this is to control high rate of inflation and interest so as to

stabilize price & build trust in economy (Chen and et.al, 2016). In Singapore, central Bank is

responsible to make policies and regulations in regards to control the inflation rate by altering the

interest rate or exchange rate. Its monetary policy covers several aspects i.e. control foreign

exchange rate, open market operations, inflation rate and others. Monetary Authority of

Singapore (MAS) aims at keeping appreciation rate of Singapore’s dollar effective exchange

(S$NEER) rate at 0%. The authority also intervenes in keeping foreign exchange rate stabilized

so as to prevent the possibility of excessive volatility in the exchange rate. The policy considers

domestic rate of interest and monetary supply as an endogenous variables and therefore, money

market operations are carried out in order to ensure sufficient liquid availability. Thus, its

monetary policy is an inflation targeted strategy, in which, policy-makers make policies in order

to control the inflation (Mohan, Patra and Kapur, 2013).

Applying the international economics concept of impossible Trinity, it presents that it is

impossible for every nation to have a fixed FOREX, free movement of capital and independent

monetary policy. Here, free capital flow is regarded as monetary movement for trade &

investment purpose, fixed FOREX rate indicates fixed exchange rate of one currency against the

value of other currency and last one sovereign monetary policy is the process wherein central

bank design policies so as to control the money supply in the nation (Cai and Pitsch, 2014). The

trilemma is also called Unholy Trinity and became popular as Mundell-Fleming model examine

the effectiveness of monetary policy of the country in an open economy with distinctive

exchange rate (Schularick and Taylor, 2012). Considering it in Singapore’s open economy, the

concept believes that it is impossible for the MSA to consider all of these three factors while

designing the monetary policy therefore; there are three choices available to the policymakers

presented below:

1. Stable rate of exchange & free capital flows but not an independent policy

1

2. Independent monetary policy & free movement of capital with volatile foreign exchange

rate (Takagawa, 2013)

3. Stable and fixed rate of exchange & independent monetary policy

Being a major financial centre, Singapore’s MSA selected free mobility of the capital &

targeted one monetary variable either exchange rate or other but not both. Unsurprisingly,

exchange rate can be used as an effective tool in order to manage an open economy (Moin and

Ahmed, 2012).

Figure 1 Impossible Trinity

[Source: Stein, 2012]

Taylor has developed a rule that presents decisions on interest rate of Federal Open

Market Committee (FOMC). It is based on altering either increasing or decreasing the interest

rate, at which commercial banks can grant loans to each other, decided using following equation:

r = p + 0.5y + 0.5(p-2) +2

r= Interest rate

p – Inflation rate

y – Output gap (excess of potential GDP over actual output)

Referring Singapore, MAS follows inflation-targeting & exchange rate focused monetary

policy with free flow of capital and domestic interest rate is determined through foreign interest

rate comprising time-varying risk premium (Bruno and Shin, 2015). Thus, according to the rule,

in order to control inflationary pressure, MAS needs to charge high rate of interest so as to

control money supply or vice-versa. Lack of credibility of the statutory monetary authority has

been recognized as a key reason behind avoiding & adopting Taylor’s rule, however, for an

open-independent economy like Singapore there may be some other reasons (Galí, 2015).

Evidencing from the empirical researches, implementation of Taylor rule in the closed

economies like US and UK founded a significant impact on the economic performance.

2

rate (Takagawa, 2013)

3. Stable and fixed rate of exchange & independent monetary policy

Being a major financial centre, Singapore’s MSA selected free mobility of the capital &

targeted one monetary variable either exchange rate or other but not both. Unsurprisingly,

exchange rate can be used as an effective tool in order to manage an open economy (Moin and

Ahmed, 2012).

Figure 1 Impossible Trinity

[Source: Stein, 2012]

Taylor has developed a rule that presents decisions on interest rate of Federal Open

Market Committee (FOMC). It is based on altering either increasing or decreasing the interest

rate, at which commercial banks can grant loans to each other, decided using following equation:

r = p + 0.5y + 0.5(p-2) +2

r= Interest rate

p – Inflation rate

y – Output gap (excess of potential GDP over actual output)

Referring Singapore, MAS follows inflation-targeting & exchange rate focused monetary

policy with free flow of capital and domestic interest rate is determined through foreign interest

rate comprising time-varying risk premium (Bruno and Shin, 2015). Thus, according to the rule,

in order to control inflationary pressure, MAS needs to charge high rate of interest so as to

control money supply or vice-versa. Lack of credibility of the statutory monetary authority has

been recognized as a key reason behind avoiding & adopting Taylor’s rule, however, for an

open-independent economy like Singapore there may be some other reasons (Galí, 2015).

Evidencing from the empirical researches, implementation of Taylor rule in the closed

economies like US and UK founded a significant impact on the economic performance.

2

However, in the open economies, it is still a contrasting discussion. Therefore, the current

research paper investigates that whether Taylor rule will be prove effective or not for the

Singapore. It will make a counter-factual analysis to assess that whether the monetary policy

framework would be more effective by using interest rate as an instrument instead of exchange

rate.

Research aims and objectives

Aim: To critically evaluate the effectiveness of Taylor’s rule in Singapore’s open economy

Objectives:

To explore the current monetary policy framework of Singapore

To examine the complexity of impossible trinity (trilemma) in designing monetary policy

To critical investigate the application of Taylor rule in the Singapore’s monetary policy

To suggest that whether Taylor rule will be better for the Singapore’s open economy or

not

Research question

Q. Will Taylor Rule will be effective or not in designing monetary policy of Singapore?

Rationale of the study

Singapore’s exchange rate targeted monetary policy aims at managing the exchange rate

with the focus on promoting price stability. The policy regime has three characteristics i.e.

managing against currency basket of major trading partners, allowing exchange rate movement

within policy band and reviewing policy with the underlying economic fundamentals (Sanders

and Houghton, 2016). However, given an economic trilemma, Mundell prescribe that MAS can

use any of two, but not all of 3 objectives (stated above) of monetary policy. However,

Aizenman stated that all these follows linear relationship therefore, it make it essential for the

policy makers to make a trade-off in selection two variables out of 3 set of objectives. An

alternative available to the authority is that MAS can utilize interest rate as an instrument

whereas exchange rate can be adjusted to market forces (Moreno, 2012). Thus the main question

is that should Singapore adopts Taylor’s rule and float its currency? Thus, the paper investigated

the characteristic of different policy choices and also examines the application of Taylor rule in

monetary policy of Singapore.

3

research paper investigates that whether Taylor rule will be prove effective or not for the

Singapore. It will make a counter-factual analysis to assess that whether the monetary policy

framework would be more effective by using interest rate as an instrument instead of exchange

rate.

Research aims and objectives

Aim: To critically evaluate the effectiveness of Taylor’s rule in Singapore’s open economy

Objectives:

To explore the current monetary policy framework of Singapore

To examine the complexity of impossible trinity (trilemma) in designing monetary policy

To critical investigate the application of Taylor rule in the Singapore’s monetary policy

To suggest that whether Taylor rule will be better for the Singapore’s open economy or

not

Research question

Q. Will Taylor Rule will be effective or not in designing monetary policy of Singapore?

Rationale of the study

Singapore’s exchange rate targeted monetary policy aims at managing the exchange rate

with the focus on promoting price stability. The policy regime has three characteristics i.e.

managing against currency basket of major trading partners, allowing exchange rate movement

within policy band and reviewing policy with the underlying economic fundamentals (Sanders

and Houghton, 2016). However, given an economic trilemma, Mundell prescribe that MAS can

use any of two, but not all of 3 objectives (stated above) of monetary policy. However,

Aizenman stated that all these follows linear relationship therefore, it make it essential for the

policy makers to make a trade-off in selection two variables out of 3 set of objectives. An

alternative available to the authority is that MAS can utilize interest rate as an instrument

whereas exchange rate can be adjusted to market forces (Moreno, 2012). Thus the main question

is that should Singapore adopts Taylor’s rule and float its currency? Thus, the paper investigated

the characteristic of different policy choices and also examines the application of Taylor rule in

monetary policy of Singapore.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Structure of the dissertation

The dissertation has followed structure outlined here below:

Introduction: This section briefly introduced the subject matter or overview of the

research problem along with the aims and objectives. It also presents the potential

contribution of the investigation and rationale why the current area needs to be

investigated by the scholar.

Literature review: Literature review is a process wherein scholar critically evaluates the

existing knowledge, methodological and theoretical contribution & substantive findings

regarding the research topic. In this regards, researchers uses only the secondary material

sources without conducting any original investigation or experimental work in the chosen

field to gain conceptual knowledge in detail.

Conclusion: It will conclude the findings of the research in summary format to overcome

the research issue investigated by the scholar.

PART – II LITERATURE REVIEW

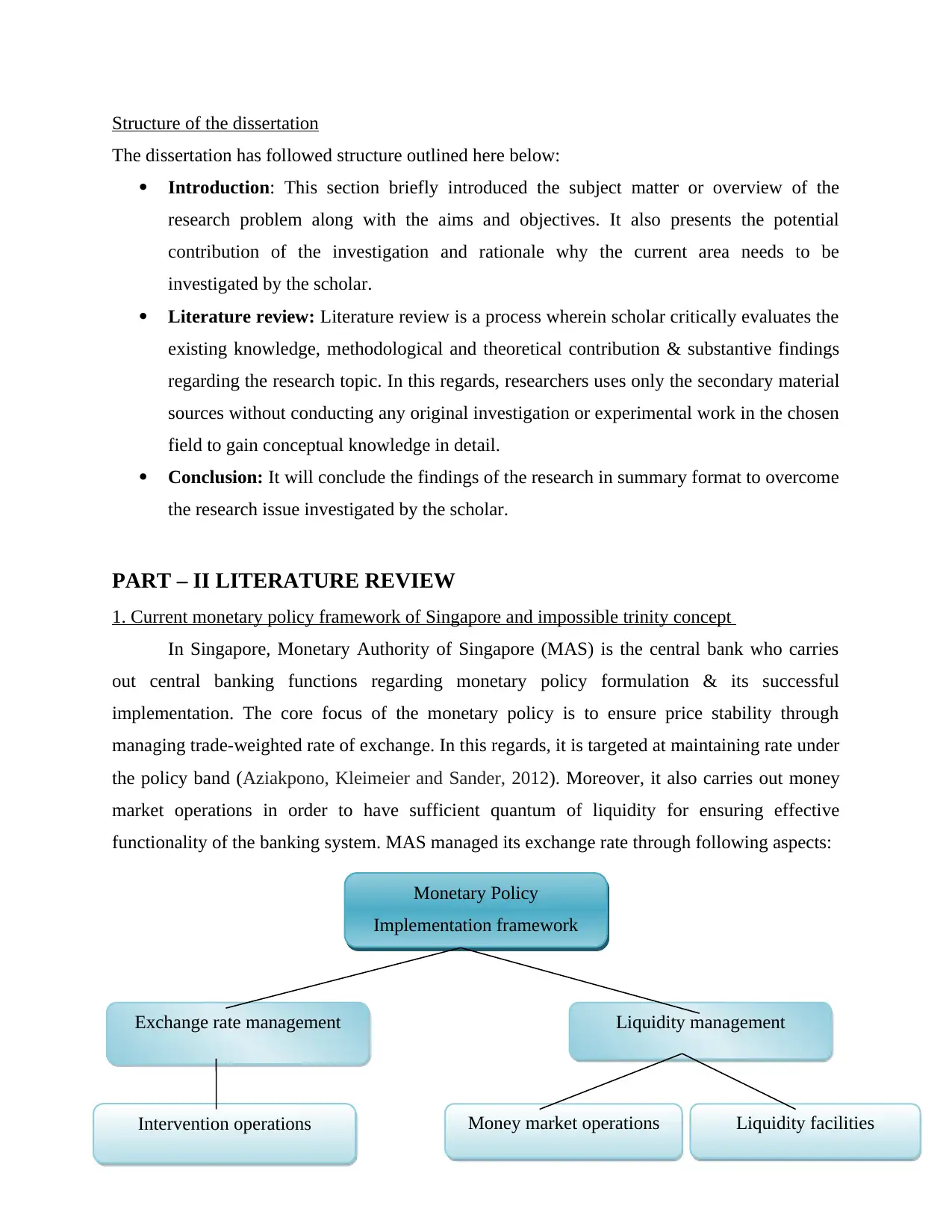

1. Current monetary policy framework of Singapore and impossible trinity concept

In Singapore, Monetary Authority of Singapore (MAS) is the central bank who carries

out central banking functions regarding monetary policy formulation & its successful

implementation. The core focus of the monetary policy is to ensure price stability through

managing trade-weighted rate of exchange. In this regards, it is targeted at maintaining rate under

the policy band (Aziakpono, Kleimeier and Sander, 2012). Moreover, it also carries out money

market operations in order to have sufficient quantum of liquidity for ensuring effective

functionality of the banking system. MAS managed its exchange rate through following aspects:

4

Monetary Policy

Implementation framework

Money market operationsIntervention operations

Liquidity managementExchange rate management

Liquidity facilities

The dissertation has followed structure outlined here below:

Introduction: This section briefly introduced the subject matter or overview of the

research problem along with the aims and objectives. It also presents the potential

contribution of the investigation and rationale why the current area needs to be

investigated by the scholar.

Literature review: Literature review is a process wherein scholar critically evaluates the

existing knowledge, methodological and theoretical contribution & substantive findings

regarding the research topic. In this regards, researchers uses only the secondary material

sources without conducting any original investigation or experimental work in the chosen

field to gain conceptual knowledge in detail.

Conclusion: It will conclude the findings of the research in summary format to overcome

the research issue investigated by the scholar.

PART – II LITERATURE REVIEW

1. Current monetary policy framework of Singapore and impossible trinity concept

In Singapore, Monetary Authority of Singapore (MAS) is the central bank who carries

out central banking functions regarding monetary policy formulation & its successful

implementation. The core focus of the monetary policy is to ensure price stability through

managing trade-weighted rate of exchange. In this regards, it is targeted at maintaining rate under

the policy band (Aziakpono, Kleimeier and Sander, 2012). Moreover, it also carries out money

market operations in order to have sufficient quantum of liquidity for ensuring effective

functionality of the banking system. MAS managed its exchange rate through following aspects:

4

Monetary Policy

Implementation framework

Money market operationsIntervention operations

Liquidity managementExchange rate management

Liquidity facilities

1. Singapore dollar is managed by taking into consideration the currencies of its major

partners in trade & competitors. In this, currencies are assigned with the weights

according to their importance in Singapore’s trade function (Singapore’s Exchange-rate

based monetary policy, 2017).

2. Under the managed floating regime, trade weighted rate of exchange is allowed to

fluctuate but within the limit of policy band that works as a mechanism to accommodate

little fluctuations in the FOREX markets.

3. Regular review of the policy band assures that the policy is going forward in line with the

underlying economic fundamentals (Subbarao, 2013).

Current statistical data reported that in Jan-Feb, 2017, Singapore’s core inflation

excluding the cost of transport & accommodation has been averaged to 1.3% YOY which was

1.2% in the last quarter of preceding year 2016. Exceeding oil prices i.e. electricity, petrol and

other is the main reason behind pickup in inflation. The economy is projected to continues to

expand at the modest pace in the year 2017 and inflation rate has been forecasted to increase

gradually mainly due to exceeding prices of oil (Monetary policy, 2017). On the other hand,

demand-driven inflationary pressure is predicted to restrain and core inflation rate is supposed to

retain at average rate slightly below 2%. MAS targeted at controlling inflationary pressure in the

country through using exchange rate as an instrument. However, applying the Taylor rule,

authority can use interest rate as an alternative means instead of current instrumental exchange

rate.

5

partners in trade & competitors. In this, currencies are assigned with the weights

according to their importance in Singapore’s trade function (Singapore’s Exchange-rate

based monetary policy, 2017).

2. Under the managed floating regime, trade weighted rate of exchange is allowed to

fluctuate but within the limit of policy band that works as a mechanism to accommodate

little fluctuations in the FOREX markets.

3. Regular review of the policy band assures that the policy is going forward in line with the

underlying economic fundamentals (Subbarao, 2013).

Current statistical data reported that in Jan-Feb, 2017, Singapore’s core inflation

excluding the cost of transport & accommodation has been averaged to 1.3% YOY which was

1.2% in the last quarter of preceding year 2016. Exceeding oil prices i.e. electricity, petrol and

other is the main reason behind pickup in inflation. The economy is projected to continues to

expand at the modest pace in the year 2017 and inflation rate has been forecasted to increase

gradually mainly due to exceeding prices of oil (Monetary policy, 2017). On the other hand,

demand-driven inflationary pressure is predicted to restrain and core inflation rate is supposed to

retain at average rate slightly below 2%. MAS targeted at controlling inflationary pressure in the

country through using exchange rate as an instrument. However, applying the Taylor rule,

authority can use interest rate as an alternative means instead of current instrumental exchange

rate.

5

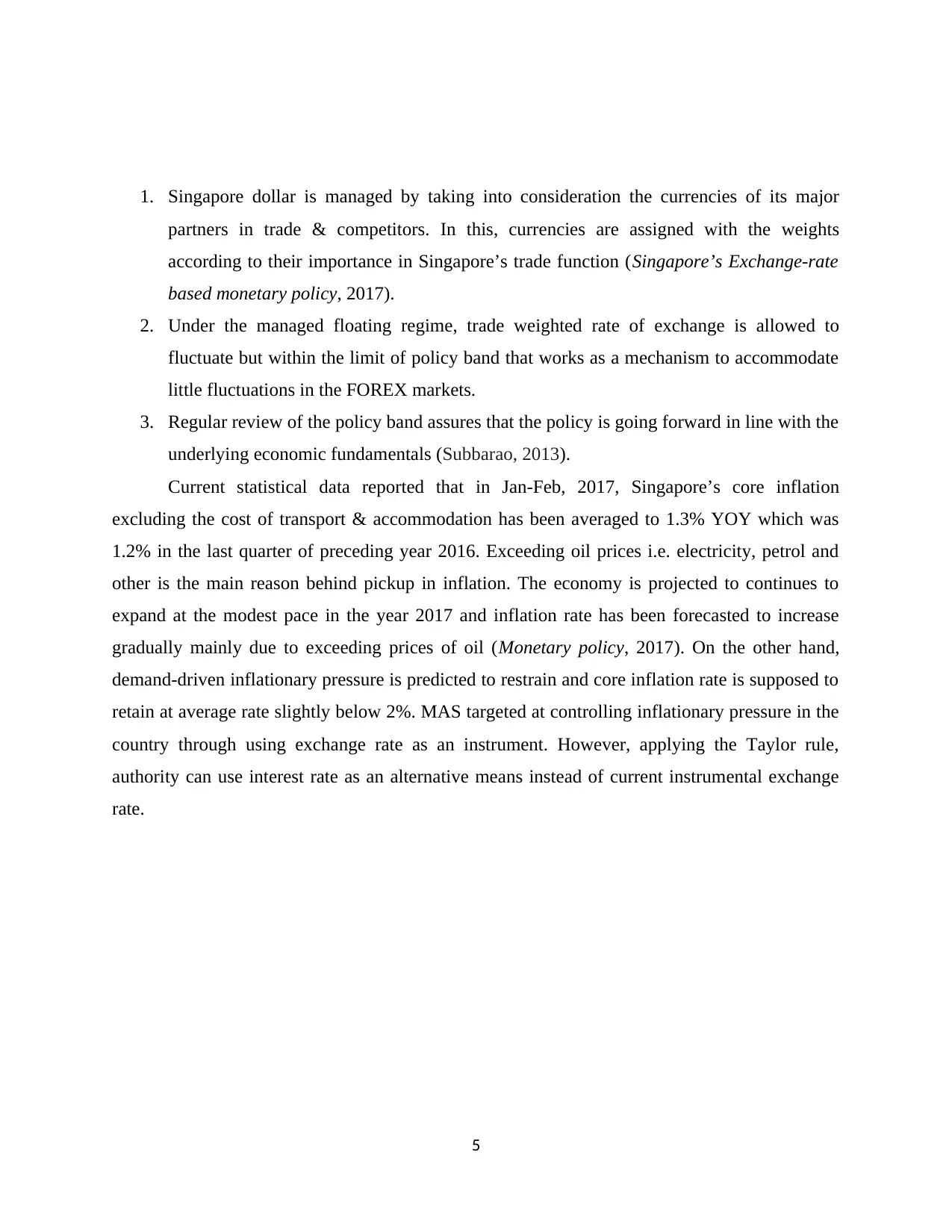

Figure 2 Mundell’s Impossible Trinity

[Source: Rey, 2015]

The above illustrated trilemma presented three sides, that are monetary independence,

financial integration and stability in exchange rate to achieve the monetary policy targets, yet, it

is impossible for the MAS to address all of these. In the study of Aizenman, Chinn and Ito

(2013), it has been founded that targeting an exchange rate is considerably more effective in

comparison to the interest rate as an instrument of macroeconomic fluctuations. However, on the

other side, Taylor’s rule presented a mechanism that can be used by the MAS to reduce high rate

of inflation by altering interest rate by targeting inflation and output gap. Although, it has been

used over last two decades as a dual mandate in order to control price stability and boost

economic sustainability, still, at the same time, the rule has several drawbacks and criticism.

2. Application of Taylor’s rule in the monetary policy

According to views of Gerstenberg and et.al, (2015), Counterfactuals Simulation refers

the flexibility in the rates so that it is very useful because of their flexible nature. When

Singapore’s economy uses the counterfactual simulation it assumes the event or areas which are

already in simulating in nature. It is a force which not only allows but also forces the brain to run

the simulations in desired areas of Singapore. It is useful for the Singapore’s economy because it

is flexible which means it can be simulating anything where it wants. It helps the economy to

discover the hidden opportunities which may be assumed impossible by the country (Neely,

2015).

6

[Source: Rey, 2015]

The above illustrated trilemma presented three sides, that are monetary independence,

financial integration and stability in exchange rate to achieve the monetary policy targets, yet, it

is impossible for the MAS to address all of these. In the study of Aizenman, Chinn and Ito

(2013), it has been founded that targeting an exchange rate is considerably more effective in

comparison to the interest rate as an instrument of macroeconomic fluctuations. However, on the

other side, Taylor’s rule presented a mechanism that can be used by the MAS to reduce high rate

of inflation by altering interest rate by targeting inflation and output gap. Although, it has been

used over last two decades as a dual mandate in order to control price stability and boost

economic sustainability, still, at the same time, the rule has several drawbacks and criticism.

2. Application of Taylor’s rule in the monetary policy

According to views of Gerstenberg and et.al, (2015), Counterfactuals Simulation refers

the flexibility in the rates so that it is very useful because of their flexible nature. When

Singapore’s economy uses the counterfactual simulation it assumes the event or areas which are

already in simulating in nature. It is a force which not only allows but also forces the brain to run

the simulations in desired areas of Singapore. It is useful for the Singapore’s economy because it

is flexible which means it can be simulating anything where it wants. It helps the economy to

discover the hidden opportunities which may be assumed impossible by the country (Neely,

2015).

6

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

As per Bärgman and et.al, (2015), Counterfactual simulations help the economy and

allow finding out the actual figure which is real in nature. It is a concept which is related to

human psychology and tendency to create possible alternative. It also includes all those things

which could never happen in reality. According to He and et.al, (2013), Counterfactual

simulation helps the Singapore’s economy to identify the risk aversion, intention of behaviour. It

also include the goal directed activity and collective action which is beneficial for the economy.

By using the downward counterfactual simulation it could be worst result and people feel a sense

of relief. On the other hand, upward counterfactual thinking, create negative thinking of people

like disappointment which is related to the situation. As per the research in Singapore’s

economy, there are various kinds of effects are contributions are investigated which make great

impact in counterfactual simulation of the economy. As per the Hutchison, Sengupta and Singh

(2012), the result showed that in a last past events people are more concerned and generated with

downward counterfactual. They also examined that manipulating social distance; negative

responses make wrong impact in the country's growth.

Recent research by Aizenman and Ito (2012), looked to determine the given power in the

situation which affect the thought of counterfactual by which such views help to understanding

the future performance. This research also determine that how manipulating the power given a

chance to reflect differently by making effective personal control. According to Federico, Vegh

and Vuletin (2014), counterfactual simulation includes various theories like Norm theory,

rational imagination theory, functional theory and rational counterfactual. By using all these

theories, it helps the Singapore’s economy to achieve their pre-determined target and achieve

their growth. By using the norm theory, Singapore’s economy determines the different outcome

with imaginative manner. On the other hand, functional theory is focus to check the perspectives

of human and their activity by which people can avoid their past blunders. By using rational

imaginative theory, people think alternative possible ways and rational counterfactual theory

helps to maximize the attainment of the desired consequent. As per Pisani-Ferry (2012), norms

and functional theory is taken by the Singapore’s economy so that it will be fruitful to the growth

of the country. It also help to stabilise the monetary policy by accomplishing their pre-determine

targets. As per the given by Taylor's view counterfactual simulation make moderate impact in

their monetary policy which need more improvement so that country can achieve their desire

target in future (Zagst, 2013).

7

allow finding out the actual figure which is real in nature. It is a concept which is related to

human psychology and tendency to create possible alternative. It also includes all those things

which could never happen in reality. According to He and et.al, (2013), Counterfactual

simulation helps the Singapore’s economy to identify the risk aversion, intention of behaviour. It

also include the goal directed activity and collective action which is beneficial for the economy.

By using the downward counterfactual simulation it could be worst result and people feel a sense

of relief. On the other hand, upward counterfactual thinking, create negative thinking of people

like disappointment which is related to the situation. As per the research in Singapore’s

economy, there are various kinds of effects are contributions are investigated which make great

impact in counterfactual simulation of the economy. As per the Hutchison, Sengupta and Singh

(2012), the result showed that in a last past events people are more concerned and generated with

downward counterfactual. They also examined that manipulating social distance; negative

responses make wrong impact in the country's growth.

Recent research by Aizenman and Ito (2012), looked to determine the given power in the

situation which affect the thought of counterfactual by which such views help to understanding

the future performance. This research also determine that how manipulating the power given a

chance to reflect differently by making effective personal control. According to Federico, Vegh

and Vuletin (2014), counterfactual simulation includes various theories like Norm theory,

rational imagination theory, functional theory and rational counterfactual. By using all these

theories, it helps the Singapore’s economy to achieve their pre-determined target and achieve

their growth. By using the norm theory, Singapore’s economy determines the different outcome

with imaginative manner. On the other hand, functional theory is focus to check the perspectives

of human and their activity by which people can avoid their past blunders. By using rational

imaginative theory, people think alternative possible ways and rational counterfactual theory

helps to maximize the attainment of the desired consequent. As per Pisani-Ferry (2012), norms

and functional theory is taken by the Singapore’s economy so that it will be fruitful to the growth

of the country. It also help to stabilise the monetary policy by accomplishing their pre-determine

targets. As per the given by Taylor's view counterfactual simulation make moderate impact in

their monetary policy which need more improvement so that country can achieve their desire

target in future (Zagst, 2013).

7

A recent study conducted by Manogaran and Sek (2016), had investigated Taylor rule in

context to ASEAN5 (Thailand, Singapore, Indonesia, Philippines and Malaysia) using NARDL

(nonlinear augmented distributed lags model & Pooled Mean Group (PMG) method. The

findings of the study presented that in the ASEAN countries, policy reacts asymmetrically to the

exchange rates in the different time period such as short-term and long-term. Still, on the other

side, policy may also react differently from the country to country. Evidencing from the results

of the study, in Thailand, monetary policy framework is designed in such a manner to keep the

exchange rate depreciated as policy shows decline in the interest rate with response to

depreciated exchange rate in the long-run. Unlike this, the other four nations, , Singapore,

Indonesia, Philippines and Malaysia do not reflect any change with the increase or decline in

exchange rate but response with the decrease or increase in long-run period. Referring Malaysia,

the research founded out that there is fear floating exists because it reflects declined in the policy

rate with the appreciated exchange rate therefore; central bank has to implement expansionary

policy so as to boost & promote economic growth. In contrast, other three nations Indonesia,

Singapore and Philippines had founded comfortable without any fear floating behaviour with the

appreciating exchange rate behaviour by improving policy rates in order to derive benefits from

the foreign flow of capital and assures appreciating exchange rate in future.

Besides this, policy behaved differently in response to the output gap & inflation gap

across distinctive countries. Countries with exceeding rate of inflation i.e. Thailand and

Indonesia significantly react with the inflation gap in the long-run whereas Philippines and

Malaysia shows high response with the output gap. It is because their actual output goes beyond

the potential or targeted level. Therefore, central bank keeps down the rate to maintain their

actual output in line with the targeted output to abstain high rate of inflation in long-run. Thus,

the policy reacts asymmetrically hence consider Taylor’s rule as an augmented rule it is because,

all the ASEAN5 reflected effective response with the volatile exchange rate by increasing or

decreasing the policy rates. Majority of the countries monetary policy regime focuses on the

inflation control still they are skeptical to allow fluctuations in the exchange rates due to the

intervention of fear of floating.

However, on the critical note, Basilio (2013), argued that before using Taylor rule,

interest rate sensitiveness of the economy must be checked. In Singapore, its extensive network

of trade relationship with the rapid flow of capital with the liberal policy regime towards FDI

8

context to ASEAN5 (Thailand, Singapore, Indonesia, Philippines and Malaysia) using NARDL

(nonlinear augmented distributed lags model & Pooled Mean Group (PMG) method. The

findings of the study presented that in the ASEAN countries, policy reacts asymmetrically to the

exchange rates in the different time period such as short-term and long-term. Still, on the other

side, policy may also react differently from the country to country. Evidencing from the results

of the study, in Thailand, monetary policy framework is designed in such a manner to keep the

exchange rate depreciated as policy shows decline in the interest rate with response to

depreciated exchange rate in the long-run. Unlike this, the other four nations, , Singapore,

Indonesia, Philippines and Malaysia do not reflect any change with the increase or decline in

exchange rate but response with the decrease or increase in long-run period. Referring Malaysia,

the research founded out that there is fear floating exists because it reflects declined in the policy

rate with the appreciated exchange rate therefore; central bank has to implement expansionary

policy so as to boost & promote economic growth. In contrast, other three nations Indonesia,

Singapore and Philippines had founded comfortable without any fear floating behaviour with the

appreciating exchange rate behaviour by improving policy rates in order to derive benefits from

the foreign flow of capital and assures appreciating exchange rate in future.

Besides this, policy behaved differently in response to the output gap & inflation gap

across distinctive countries. Countries with exceeding rate of inflation i.e. Thailand and

Indonesia significantly react with the inflation gap in the long-run whereas Philippines and

Malaysia shows high response with the output gap. It is because their actual output goes beyond

the potential or targeted level. Therefore, central bank keeps down the rate to maintain their

actual output in line with the targeted output to abstain high rate of inflation in long-run. Thus,

the policy reacts asymmetrically hence consider Taylor’s rule as an augmented rule it is because,

all the ASEAN5 reflected effective response with the volatile exchange rate by increasing or

decreasing the policy rates. Majority of the countries monetary policy regime focuses on the

inflation control still they are skeptical to allow fluctuations in the exchange rates due to the

intervention of fear of floating.

However, on the critical note, Basilio (2013), argued that before using Taylor rule,

interest rate sensitiveness of the economy must be checked. In Singapore, its extensive network

of trade relationship with the rapid flow of capital with the liberal policy regime towards FDI

8

stated that the economy is not very responsive with the fluctuating interest rate. In the

counterfactual experiment, Taylor rule replaces the exchange rate rule, more specifically, when

economy uses exchange rate then domestic rate of interest is determined to satisfy interest parity

whereas when interest rate is managed then exchange rate is founded to do the same.

Study conducted by Chow, Lim and McNelis (2014), performed an Impulse Response

Path analysis of output gap and inflation from the period ranging 1985 to 2009 under actual as

well as counterfactual regime and the result determined that, with response to the productivity

shock, under the exchange rate rule, inflation goes increase, however, it dropped down in Taylor

rule. It is because; productivity shock maximizes the output gap. Since the Taylor’s interest rate

rule respond to the output gaps by increasing the interest rate, inflation rate decline due to the

productivity shocks. Similarly, inflation is also considered as more responsive to import-price

inflation shock in Taylor rule comparatively to the exchange rate. Considering the nature of the

shocks in the economy; impulse response analysis identified that one rule will be more beneficial

over other one so as to stabilize the inflationary pressure. In case of dominant productivity

shocks Taylor’s interest rate rule is considered as more effective, however, in case of dominant

foreign price shocks, exchange rate rule is preferable.

The result of the study showed that welfare-maximizing rule of Taylor that is based on

the lagged interest rate, output gap and inflation minimizes inflationary pressure in productivity

shocks, however, exchange rate depreciation rule reduces the same in export price shocks

(Jiménez and et.al, 2014). Evidencing from the output generated, GDP volatility is founded

more responsive to the export-pricing volatility (74%) in comparison to the productivity (4%)

which suggests Singapore’s monetary authority to use exchange rate as an instrument for the

monetary policy regime instead of Taylor’s rule. Besides this, in the stochastic simulation, the

result showcase that under exchange rate rule, depreciation is less volatile & the interest rate is

considered as more volatile in comparison to the interest-rate based rule. Evidencing from the

outcome, optimal rule delivered zero output gap with low inflation coefficient (1.05) & larger

smoothing coefficient (0.675) in comparison to the corresponding coefficient at 1.72 & 0.145

respectively.

On the critical note, De Brigard, Szpunar and Schacter (2013), pointed out that policy

regime also needs to be examined on the basis of inflation persistence. Asian countries who had

switched to inflation-targeting monetary policy focus with the application of Taylor rule declined

9

counterfactual experiment, Taylor rule replaces the exchange rate rule, more specifically, when

economy uses exchange rate then domestic rate of interest is determined to satisfy interest parity

whereas when interest rate is managed then exchange rate is founded to do the same.

Study conducted by Chow, Lim and McNelis (2014), performed an Impulse Response

Path analysis of output gap and inflation from the period ranging 1985 to 2009 under actual as

well as counterfactual regime and the result determined that, with response to the productivity

shock, under the exchange rate rule, inflation goes increase, however, it dropped down in Taylor

rule. It is because; productivity shock maximizes the output gap. Since the Taylor’s interest rate

rule respond to the output gaps by increasing the interest rate, inflation rate decline due to the

productivity shocks. Similarly, inflation is also considered as more responsive to import-price

inflation shock in Taylor rule comparatively to the exchange rate. Considering the nature of the

shocks in the economy; impulse response analysis identified that one rule will be more beneficial

over other one so as to stabilize the inflationary pressure. In case of dominant productivity

shocks Taylor’s interest rate rule is considered as more effective, however, in case of dominant

foreign price shocks, exchange rate rule is preferable.

The result of the study showed that welfare-maximizing rule of Taylor that is based on

the lagged interest rate, output gap and inflation minimizes inflationary pressure in productivity

shocks, however, exchange rate depreciation rule reduces the same in export price shocks

(Jiménez and et.al, 2014). Evidencing from the output generated, GDP volatility is founded

more responsive to the export-pricing volatility (74%) in comparison to the productivity (4%)

which suggests Singapore’s monetary authority to use exchange rate as an instrument for the

monetary policy regime instead of Taylor’s rule. Besides this, in the stochastic simulation, the

result showcase that under exchange rate rule, depreciation is less volatile & the interest rate is

considered as more volatile in comparison to the interest-rate based rule. Evidencing from the

outcome, optimal rule delivered zero output gap with low inflation coefficient (1.05) & larger

smoothing coefficient (0.675) in comparison to the corresponding coefficient at 1.72 & 0.145

respectively.

On the critical note, De Brigard, Szpunar and Schacter (2013), pointed out that policy

regime also needs to be examined on the basis of inflation persistence. Asian countries who had

switched to inflation-targeting monetary policy focus with the application of Taylor rule declined

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

inflation persistence. According to the results derived through simulation, the study stated that

exchange rate persistent coefficient mean and median was recognized at the lower end of the

actual distribution however the same under the Taylor rule were founded at the upper end. Thus,

the finding clearly presented that monetary policy with the depreciating exchange rate policy had

a comparative advantage over the Taylor rule regime so as to achieve lower inflationary

persistence. The output of the study suggested that there is no reason for the MAS to fear floating

the exchange-rate and using the rule of Taylor to manage their inflation rate. Thus, abandoning

currently used exchange rate regime with the interest rate will indicates more exchange rate

volatility and less fluctuation in the interest-rate.

However, on the other side, Drehmann and Gambacorta (2012), criticized the interest-rate

focused rule of Taylor on the three pointed that are inclusion of exchange rate, its asymmetric

form and foward V/s backward rule. In the first criticism, it is suggested to incorporate exchange

rate in the Taylor rule especially in the emerging economies. Although these are small still very

open in trade hence, these are sensitive to the volatile exchange rate movements and vulnerable

to the external shocks, called fear floating behaviour. Such economies are reluctant to float their

local currency value with the fluctuation in the exchange rate, hence, it is better for such

countries to incorporate exchange rate in the rule to make monetary policy framework more

effective.

It is contradicted by Hofmann and Bogdanova (2012), arguing that monetary policy

shouldn’t include a direct exchange rate because it may results in loss of credibility. The study

opined that there is already an indirect effect of the monetary policy over output and inflation;

therefore, there is no need for the countries to include it in the Taylor rule. Besides this, the rule

follows an assumption of linear relationship however, criticisers disapproved the assumption by

proving asymmetric (non-linear) relationship therefore, the rule cannot be considered as an

effective method. Apart from this, it can be inferred that the rule only pay focus on the

predetermined values of inflation & economic growth in order to formulate the monetary policy,

still, the method provides an inadequate mechanism to predict the future status of the economy at

a current level of inflation & output gap.

10

exchange rate persistent coefficient mean and median was recognized at the lower end of the

actual distribution however the same under the Taylor rule were founded at the upper end. Thus,

the finding clearly presented that monetary policy with the depreciating exchange rate policy had

a comparative advantage over the Taylor rule regime so as to achieve lower inflationary

persistence. The output of the study suggested that there is no reason for the MAS to fear floating

the exchange-rate and using the rule of Taylor to manage their inflation rate. Thus, abandoning

currently used exchange rate regime with the interest rate will indicates more exchange rate

volatility and less fluctuation in the interest-rate.

However, on the other side, Drehmann and Gambacorta (2012), criticized the interest-rate

focused rule of Taylor on the three pointed that are inclusion of exchange rate, its asymmetric

form and foward V/s backward rule. In the first criticism, it is suggested to incorporate exchange

rate in the Taylor rule especially in the emerging economies. Although these are small still very

open in trade hence, these are sensitive to the volatile exchange rate movements and vulnerable

to the external shocks, called fear floating behaviour. Such economies are reluctant to float their

local currency value with the fluctuation in the exchange rate, hence, it is better for such

countries to incorporate exchange rate in the rule to make monetary policy framework more

effective.

It is contradicted by Hofmann and Bogdanova (2012), arguing that monetary policy

shouldn’t include a direct exchange rate because it may results in loss of credibility. The study

opined that there is already an indirect effect of the monetary policy over output and inflation;

therefore, there is no need for the countries to include it in the Taylor rule. Besides this, the rule

follows an assumption of linear relationship however, criticisers disapproved the assumption by

proving asymmetric (non-linear) relationship therefore, the rule cannot be considered as an

effective method. Apart from this, it can be inferred that the rule only pay focus on the

predetermined values of inflation & economic growth in order to formulate the monetary policy,

still, the method provides an inadequate mechanism to predict the future status of the economy at

a current level of inflation & output gap.

10

PART III: CONCLUSION

Based upon the analysis carried in the research, it can be concluded that every country’s

monetary policy’s main focus is to control the rate of inflation through exchange rate control &

interest rate movement. However, taking into account, the impossible trinity index which reveals

that central bank can only use either of any two factors out of monetary independence, financial

integration and stability in exchange rate in their monetary policy regime. In Singapore,

Monetary authority uses exchange rate as an instrument for keeping control over the inflation

rate so as to ensure price stability in the economy. It is because, being a major financial centre,

Singapore’s MSA selected free mobility of the capital & targeted one monetary variable using

exchange rate as a tool for inflation control. Thus, the alternative that is being available to the

MAS is to use interest rate (Taylor rule) as a medium to minimize inflation. MAS allow free

flow of capital under which interest rate is determined by the authority through foreign interest

rate taking into consideration time-varying risk premium. According to the rule, if MAS needs to

control inflationary pressure, then it needs to charge high rate of interest so as to control money

supply or vice-versa.

The findings of various studies conducted earlier, it has been founded that monetary

policy framework reacts distinctively to the output & inflation gaps. The research determined

that in the exchange rate, inflation rate in an economy goes upward with response to the

productivity shocks whereas the same goes decline in Taylor’s interest based rule. It

demonstrates that with dominant productivity shocks Taylor’s interest rate rule is considered as

more effective, however, in case of dominant foreign price shocks, exchange rate rule is

preferable. Likewise, inflation significantly response to the import-price inflation shocks in

comparison to the exchange rate. Besides this, it also has been evaluated that in the exchange

rate based rule, depreciation is comparatively less volatile while interest rate shows high

volatility or opposite under the interest-rate based monetary regime.

However, on the other side, Taylor rule also has been contradicted on the basis of

asymmetrical relationship means non-linear relationship. It also has been criticized on the basis

of interest-rate rule of Taylor on the three pointed that are inclusion of exchange rate, its

asymmetric form and forward V/s backward rule. Moreover, the findings also concluded that

monetary policy regime response differently with the exchange rate movements in different time

duration and in different economies. Focusing on Singapore, it is assessed that its economy has

11

Based upon the analysis carried in the research, it can be concluded that every country’s

monetary policy’s main focus is to control the rate of inflation through exchange rate control &

interest rate movement. However, taking into account, the impossible trinity index which reveals

that central bank can only use either of any two factors out of monetary independence, financial

integration and stability in exchange rate in their monetary policy regime. In Singapore,

Monetary authority uses exchange rate as an instrument for keeping control over the inflation

rate so as to ensure price stability in the economy. It is because, being a major financial centre,

Singapore’s MSA selected free mobility of the capital & targeted one monetary variable using

exchange rate as a tool for inflation control. Thus, the alternative that is being available to the

MAS is to use interest rate (Taylor rule) as a medium to minimize inflation. MAS allow free

flow of capital under which interest rate is determined by the authority through foreign interest

rate taking into consideration time-varying risk premium. According to the rule, if MAS needs to

control inflationary pressure, then it needs to charge high rate of interest so as to control money

supply or vice-versa.

The findings of various studies conducted earlier, it has been founded that monetary

policy framework reacts distinctively to the output & inflation gaps. The research determined

that in the exchange rate, inflation rate in an economy goes upward with response to the

productivity shocks whereas the same goes decline in Taylor’s interest based rule. It

demonstrates that with dominant productivity shocks Taylor’s interest rate rule is considered as

more effective, however, in case of dominant foreign price shocks, exchange rate rule is

preferable. Likewise, inflation significantly response to the import-price inflation shocks in

comparison to the exchange rate. Besides this, it also has been evaluated that in the exchange

rate based rule, depreciation is comparatively less volatile while interest rate shows high

volatility or opposite under the interest-rate based monetary regime.

However, on the other side, Taylor rule also has been contradicted on the basis of

asymmetrical relationship means non-linear relationship. It also has been criticized on the basis

of interest-rate rule of Taylor on the three pointed that are inclusion of exchange rate, its

asymmetric form and forward V/s backward rule. Moreover, the findings also concluded that

monetary policy regime response differently with the exchange rate movements in different time

duration and in different economies. Focusing on Singapore, it is assessed that its economy has

11

no floating fear with the Taylor rule. It is because, with the appreciating exchange rate

behaviour, MAS will improve policy rates in order to derive benefits from the foreign flow of

capital and assures appreciating exchange rate in future. Pointing out inflation persistence, the

studies showed that monetary policy framework of the nation with the depreciating rate of

exchange has certain advantage over interest rate based rule to control inflation rate. Thus, there

is no reason for the Singapore’s open economy to fear floating the exchange-rate and using the

rule of Taylor to manage their inflation rate. Abandoning currently used exchange rate regime

with the interest rate will indicates more exchange rate volatility and less fluctuation in the

interest-rate.

Thus, from the research, it becomes clear that it might be better for the Singapore to

apply Taylor rule to control inflation in case of dominant productivity shocks. However,

currently applied exchange rate is founded as a better choice for the monetary authority in case

of dominant foreign price shocks.

12

behaviour, MAS will improve policy rates in order to derive benefits from the foreign flow of

capital and assures appreciating exchange rate in future. Pointing out inflation persistence, the

studies showed that monetary policy framework of the nation with the depreciating rate of

exchange has certain advantage over interest rate based rule to control inflation rate. Thus, there

is no reason for the Singapore’s open economy to fear floating the exchange-rate and using the

rule of Taylor to manage their inflation rate. Abandoning currently used exchange rate regime

with the interest rate will indicates more exchange rate volatility and less fluctuation in the

interest-rate.

Thus, from the research, it becomes clear that it might be better for the Singapore to

apply Taylor rule to control inflation in case of dominant productivity shocks. However,

currently applied exchange rate is founded as a better choice for the monetary authority in case

of dominant foreign price shocks.

12

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

PART –IV REFERENCES

Books and Journals

Aizenman, J. and Ito, H., 2012. Trilemma policy convergence patterns and output volatility. The

North American Journal of Economics and Finance.23(3). pp.269-285.

Aizenman, J., Chinn, M. D. and Ito, H., 2013. The “impossible trinity” hypothesis in an era of

global imbalances: Measurement and testing. Review of International Economics. 21(3).

pp.447-458.

Aziakpono, M. J., Kleimeier, S. and Sander, H., 2012. Banking market integration in the SADC

countries: evidence from interest rate analyses.Applied Economics.44(29). pp.3857-3876.

Bärgman, J. and et.al, 2015. How does glance behavior influence crash and injury risk? A ‘what-

if’counterfactual simulation using crashes and near-crashes from SHRP2.Transportation

Research Part F: Traffic Psychology and Behaviour. 35. pp.152-169.

Basilio, J. R., 2013. Empirics of Monetary Policy Rules: The Taylor Rule in Different

Countries (Doctoral dissertation, University of Illinois at Chicago).

Bruno, V. and Shin, H. S., 2015. Capital flows and the risk-taking channel of monetary

policy. Journal of Monetary Economics. 71. pp.119-132.

Cai, L. and Pitsch, H., 2014. Mechanism optimization based on reaction rate rules. Combustion

and Flame. 161(2). pp.405-415.

Chen, Q., Filardo, A., He, D. and Zhu, F., 2016. Financial crisis, US unconventional monetary

policy and international spillovers. Journal of International Money and Finance. 67.

pp.62-81.

Chow, H. K., Lim, G. C. and McNelis, P. D., 2014. Monetary regime choice in Singapore:

Would a Taylor rule outperform exchange-rate management?.Journal of Asian

Economics. 30. pp.63-81.

De Brigard, F., Szpunar, K. K. and Schacter, D. L., 2013. Coming to grips with the past: Effect

of repeated simulation on the perceived plausibility of episodic counterfactual

thoughts. Psychological Science. 24(7). pp.1329-1334.

Drehmann, M. and Gambacorta, L., 2012. The effects of countercyclical capital buffers on bank

lending. Applied Economics Letters. 19(7). pp.603-608.

13

Books and Journals

Aizenman, J. and Ito, H., 2012. Trilemma policy convergence patterns and output volatility. The

North American Journal of Economics and Finance.23(3). pp.269-285.

Aizenman, J., Chinn, M. D. and Ito, H., 2013. The “impossible trinity” hypothesis in an era of

global imbalances: Measurement and testing. Review of International Economics. 21(3).

pp.447-458.

Aziakpono, M. J., Kleimeier, S. and Sander, H., 2012. Banking market integration in the SADC

countries: evidence from interest rate analyses.Applied Economics.44(29). pp.3857-3876.

Bärgman, J. and et.al, 2015. How does glance behavior influence crash and injury risk? A ‘what-

if’counterfactual simulation using crashes and near-crashes from SHRP2.Transportation

Research Part F: Traffic Psychology and Behaviour. 35. pp.152-169.

Basilio, J. R., 2013. Empirics of Monetary Policy Rules: The Taylor Rule in Different

Countries (Doctoral dissertation, University of Illinois at Chicago).

Bruno, V. and Shin, H. S., 2015. Capital flows and the risk-taking channel of monetary

policy. Journal of Monetary Economics. 71. pp.119-132.

Cai, L. and Pitsch, H., 2014. Mechanism optimization based on reaction rate rules. Combustion

and Flame. 161(2). pp.405-415.

Chen, Q., Filardo, A., He, D. and Zhu, F., 2016. Financial crisis, US unconventional monetary

policy and international spillovers. Journal of International Money and Finance. 67.

pp.62-81.

Chow, H. K., Lim, G. C. and McNelis, P. D., 2014. Monetary regime choice in Singapore:

Would a Taylor rule outperform exchange-rate management?.Journal of Asian

Economics. 30. pp.63-81.

De Brigard, F., Szpunar, K. K. and Schacter, D. L., 2013. Coming to grips with the past: Effect

of repeated simulation on the perceived plausibility of episodic counterfactual

thoughts. Psychological Science. 24(7). pp.1329-1334.

Drehmann, M. and Gambacorta, L., 2012. The effects of countercyclical capital buffers on bank

lending. Applied Economics Letters. 19(7). pp.603-608.

13

Federico, P., Vegh, C. A. and Vuletin, G., 2014. Reserve requirement policy over the business

cycle (No. w20612). National Bureau of Economic Research.

Galí, J., 2015. Monetary policy, inflation, and the business cycle: an introduction to the new

Keynesian framework and its applications. Princeton University Press.

Gerstenberg, T. and et.al, 2015. How, whether, why: Causal judgments as counterfactual

contrasts. InCogSci.

He, J. and et.al, 2013. A counterfactual scenario simulation approach for assessing the impact of

farmland preservation policies on urban sprawl and food security in a major grain-

producing area of China. Applied Geography. 37. pp.127-138.

Hofmann, B. and Bogdanova, B., 2012. Taylor Rules and Monetary Policy: A Global'Great

Deviation’?

Hutchison, M., Sengupta, R. and Singh, N., 2012. India’s trilemma: financial liberalisation,

exchange rates and monetary policy. The World Economy.35(1). pp.3-18.

Jiménez, G. and et.al, 2014. Hazardous Times for Monetary Policy: What Do Twenty‐Three

Million Bank Loans Say About the Effects of Monetary Policy on Credit Risk‐

Taking?. Econometrica. 82(2). pp.463-505.

Mohan, R., Patra, M. D. and Kapur, M., 2013. Currency internationalization and reforms in the

architecture of the international monetary system: managing the impossible trinity.

Moin, K. I. and Ahmed, D. Q. B., 2012. Use of data mining in banking.International Journal of

Engineering Research and Applications. 2(2). pp.738-742.

Moreno, R., 2012, December. Exchange rates and monetary policy in Singapore and Hong Kong.

In Monetary Policy in Pacific Basin Countries: Papers Presented at a Conference

Sponsored by the Federal Reserve Bank of San Francisco (p. 173). Springer Science &

Business Media.

Neely, C.J., 2015. Unconventional monetary policy had large international effects. Journal of

Banking & Finance. 52. pp.101-111.

Pisani-Ferry, J., 2012. The euro crisis and the new impossible trinity (No. 2012/01). Bruegel

Policy Contribution.

Rey, H., 2015. Dilemma not trilemma: the global financial cycle and monetary policy

independence (No. w21162). National Bureau of Economic Research.

14

cycle (No. w20612). National Bureau of Economic Research.

Galí, J., 2015. Monetary policy, inflation, and the business cycle: an introduction to the new

Keynesian framework and its applications. Princeton University Press.

Gerstenberg, T. and et.al, 2015. How, whether, why: Causal judgments as counterfactual

contrasts. InCogSci.

He, J. and et.al, 2013. A counterfactual scenario simulation approach for assessing the impact of

farmland preservation policies on urban sprawl and food security in a major grain-

producing area of China. Applied Geography. 37. pp.127-138.

Hofmann, B. and Bogdanova, B., 2012. Taylor Rules and Monetary Policy: A Global'Great

Deviation’?

Hutchison, M., Sengupta, R. and Singh, N., 2012. India’s trilemma: financial liberalisation,

exchange rates and monetary policy. The World Economy.35(1). pp.3-18.

Jiménez, G. and et.al, 2014. Hazardous Times for Monetary Policy: What Do Twenty‐Three

Million Bank Loans Say About the Effects of Monetary Policy on Credit Risk‐

Taking?. Econometrica. 82(2). pp.463-505.

Mohan, R., Patra, M. D. and Kapur, M., 2013. Currency internationalization and reforms in the

architecture of the international monetary system: managing the impossible trinity.

Moin, K. I. and Ahmed, D. Q. B., 2012. Use of data mining in banking.International Journal of

Engineering Research and Applications. 2(2). pp.738-742.

Moreno, R., 2012, December. Exchange rates and monetary policy in Singapore and Hong Kong.

In Monetary Policy in Pacific Basin Countries: Papers Presented at a Conference

Sponsored by the Federal Reserve Bank of San Francisco (p. 173). Springer Science &

Business Media.

Neely, C.J., 2015. Unconventional monetary policy had large international effects. Journal of

Banking & Finance. 52. pp.101-111.

Pisani-Ferry, J., 2012. The euro crisis and the new impossible trinity (No. 2012/01). Bruegel

Policy Contribution.

Rey, H., 2015. Dilemma not trilemma: the global financial cycle and monetary policy

independence (No. w21162). National Bureau of Economic Research.

14

Sanders, D. and Houghton, D. P., 2016. Losing an empire, finding a role: British foreign policy

since 1945. Palgrave Macmillan.

Schularick, M. and Taylor, A. M., 2012. Credit booms gone bust: monetary policy, leverage

cycles, and financial crises, 1870–2008. The American Economic Review. 102(2). pp.1029-

1061.

Stein, J. C., 2012. Monetary policy as financial stability regulation. The Quarterly Journal of

Economics. 127(1). pp.57-95.

Subbarao, D., 2013. Central banking in emerging economies-emerging challenges. Speech at the

European Economics and Finanacial Centre, London, 17.

Takagawa, I., 2013. 14 An empirical analysis of the “impossible trinity”.Exchange rates, capital

flows and policy. 30. pp.319.

Zagst, R., 2013. Interest-rate management. Springer Science & Business Media.

Online

Manogaran, L. and Sek, K. S., 2016. Can Taylor Rule be a good presentation of Monetary Policy

functions for ASEAN5? [Online]. Available through: <

http://www.indjst.org/index.php/indjst/article/view/109305/77041>. [Accessed on 27th

June 2017].

Monetary policy. 2017. [Online]. Available through: < http://www.sgs.gov.sg/The-SGS-

Market/Monetary-Policy.aspx>. [Accessed on 27th June 2017].

Singapore’s Exchange-rate based monetary policy. 2017. [Online]. Available through: <

http://www.mas.gov.sg/~/media/MAS/Monetary%20Policy%20and%20Economics/

Monetary%20Policy/MP%20Framework/Singapores%20Exchange%20Ratebased

%20Monetary%20Policy.pdf>. [Accessed on 27th June 2017].

15

since 1945. Palgrave Macmillan.

Schularick, M. and Taylor, A. M., 2012. Credit booms gone bust: monetary policy, leverage

cycles, and financial crises, 1870–2008. The American Economic Review. 102(2). pp.1029-

1061.

Stein, J. C., 2012. Monetary policy as financial stability regulation. The Quarterly Journal of

Economics. 127(1). pp.57-95.

Subbarao, D., 2013. Central banking in emerging economies-emerging challenges. Speech at the

European Economics and Finanacial Centre, London, 17.

Takagawa, I., 2013. 14 An empirical analysis of the “impossible trinity”.Exchange rates, capital

flows and policy. 30. pp.319.

Zagst, R., 2013. Interest-rate management. Springer Science & Business Media.

Online

Manogaran, L. and Sek, K. S., 2016. Can Taylor Rule be a good presentation of Monetary Policy

functions for ASEAN5? [Online]. Available through: <

http://www.indjst.org/index.php/indjst/article/view/109305/77041>. [Accessed on 27th

June 2017].

Monetary policy. 2017. [Online]. Available through: < http://www.sgs.gov.sg/The-SGS-

Market/Monetary-Policy.aspx>. [Accessed on 27th June 2017].

Singapore’s Exchange-rate based monetary policy. 2017. [Online]. Available through: <

http://www.mas.gov.sg/~/media/MAS/Monetary%20Policy%20and%20Economics/

Monetary%20Policy/MP%20Framework/Singapores%20Exchange%20Ratebased

%20Monetary%20Policy.pdf>. [Accessed on 27th June 2017].

15

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.