Audit Report on Trunkey Creek Wines Ltd: Risk & Ratio Analysis

VerifiedAdded on 2023/06/09

|18

|4452

|202

Report

AI Summary

This report provides an analysis of the audit risks associated with Trunkey Creek Wines Limited (TCW), focusing on key accounts such as accounts receivable, investments, property assets, and marketing expenses. It uses ratio analysis to assess the company's financial performance and identifies potential areas of material misstatement due to error or fraud. The report also evaluates the effectiveness of TCW's internal controls in ensuring operational efficiency and compliance with organizational objectives. Key performance indicators, including return on equity, return on assets, gross margin, and days in inventory, are analyzed to provide a comprehensive overview of TCW's financial health and potential business risks. The analysis includes a review of both audited historical data and unaudited projections to identify trends and potential areas of concern for the auditor.

Running head: AUDITING THEORY AND PRACTICE

Auditing theory and practice

Name of the Student:

Name of the University:

Auditing theory and practice

Name of the Student:

Name of the University:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING THEORY AND PRACTICE

Executive summary

The paper discusses about the risk of audit that refers to the issue that is faced by the auditor

while detecting the material misstatement is to be detected in this section. This may occur due to

error or fraud. The best way to analyze the business risks is to conduct a ratio analysis that would

help in obtaining a quick indication of the performance of the firm in several key areas. It would

help the management to pinpoint the strength and weaknesses from with various initiatives and

strategies can be formed. The chosen company of TCW has been analyzed in the following

report. On the other internal control that refers to the assurance of organizations objectives in the

operational efficiency and effectiveness has also been checked for the company.

Executive summary

The paper discusses about the risk of audit that refers to the issue that is faced by the auditor

while detecting the material misstatement is to be detected in this section. This may occur due to

error or fraud. The best way to analyze the business risks is to conduct a ratio analysis that would

help in obtaining a quick indication of the performance of the firm in several key areas. It would

help the management to pinpoint the strength and weaknesses from with various initiatives and

strategies can be formed. The chosen company of TCW has been analyzed in the following

report. On the other internal control that refers to the assurance of organizations objectives in the

operational efficiency and effectiveness has also been checked for the company.

2AUDITING THEORY AND PRACTICE

Table of Contents

Answer to Question 1A...................................................................................................................3

Answer to Question 1B....................................................................................................................6

Answer to question 2A..................................................................................................................10

Answer to Question 2B..................................................................................................................11

Referemces....................................................................................................................................13

Table of Contents

Answer to Question 1A...................................................................................................................3

Answer to Question 1B....................................................................................................................6

Answer to question 2A..................................................................................................................10

Answer to Question 2B..................................................................................................................11

Referemces....................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING THEORY AND PRACTICE

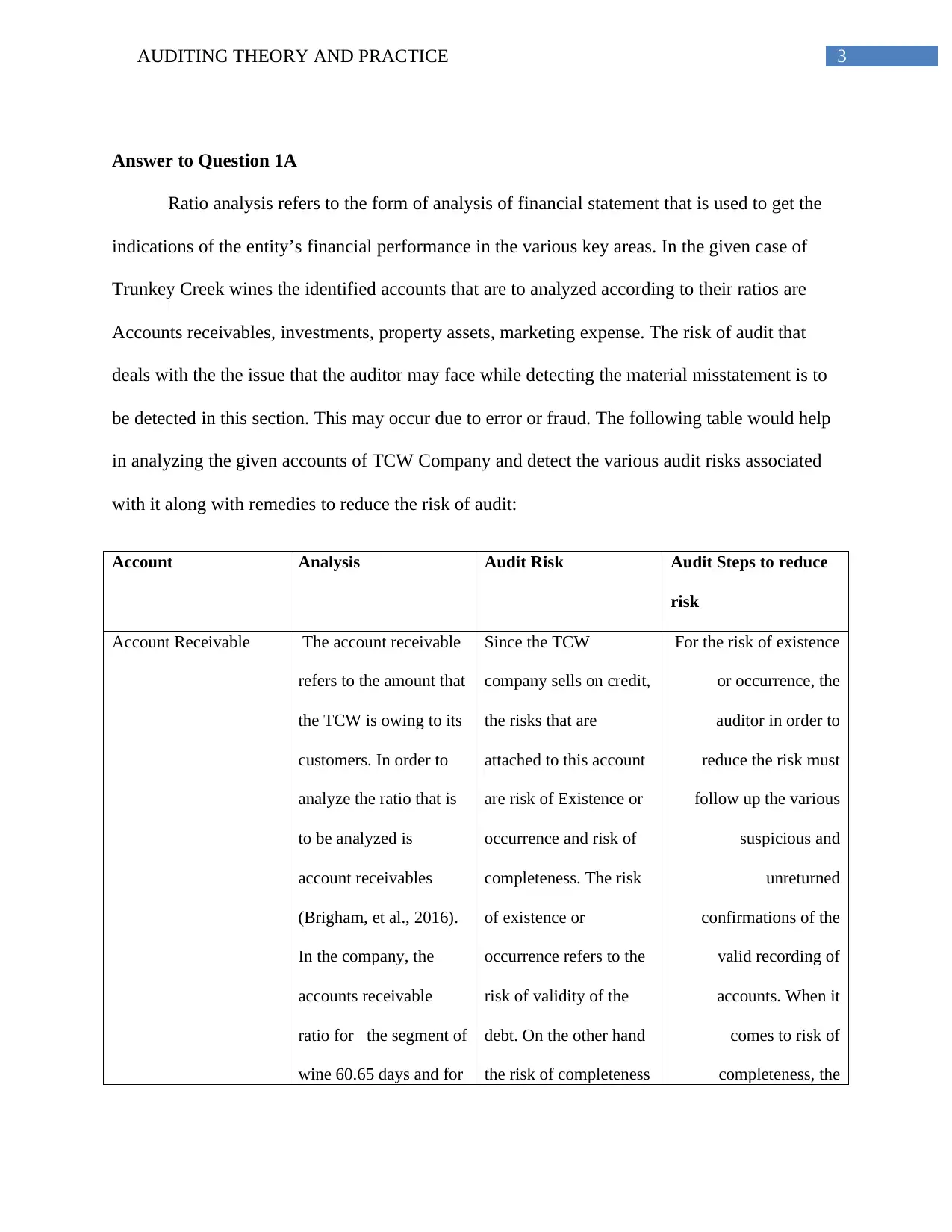

Answer to Question 1A

Ratio analysis refers to the form of analysis of financial statement that is used to get the

indications of the entity’s financial performance in the various key areas. In the given case of

Trunkey Creek wines the identified accounts that are to analyzed according to their ratios are

Accounts receivables, investments, property assets, marketing expense. The risk of audit that

deals with the the issue that the auditor may face while detecting the material misstatement is to

be detected in this section. This may occur due to error or fraud. The following table would help

in analyzing the given accounts of TCW Company and detect the various audit risks associated

with it along with remedies to reduce the risk of audit:

Account Analysis Audit Risk Audit Steps to reduce

risk

Account Receivable The account receivable

refers to the amount that

the TCW is owing to its

customers. In order to

analyze the ratio that is

to be analyzed is

account receivables

(Brigham, et al., 2016).

In the company, the

accounts receivable

ratio for the segment of

wine 60.65 days and for

Since the TCW

company sells on credit,

the risks that are

attached to this account

are risk of Existence or

occurrence and risk of

completeness. The risk

of existence or

occurrence refers to the

risk of validity of the

debt. On the other hand

the risk of completeness

For the risk of existence

or occurrence, the

auditor in order to

reduce the risk must

follow up the various

suspicious and

unreturned

confirmations of the

valid recording of

accounts. When it

comes to risk of

completeness, the

Answer to Question 1A

Ratio analysis refers to the form of analysis of financial statement that is used to get the

indications of the entity’s financial performance in the various key areas. In the given case of

Trunkey Creek wines the identified accounts that are to analyzed according to their ratios are

Accounts receivables, investments, property assets, marketing expense. The risk of audit that

deals with the the issue that the auditor may face while detecting the material misstatement is to

be detected in this section. This may occur due to error or fraud. The following table would help

in analyzing the given accounts of TCW Company and detect the various audit risks associated

with it along with remedies to reduce the risk of audit:

Account Analysis Audit Risk Audit Steps to reduce

risk

Account Receivable The account receivable

refers to the amount that

the TCW is owing to its

customers. In order to

analyze the ratio that is

to be analyzed is

account receivables

(Brigham, et al., 2016).

In the company, the

accounts receivable

ratio for the segment of

wine 60.65 days and for

Since the TCW

company sells on credit,

the risks that are

attached to this account

are risk of Existence or

occurrence and risk of

completeness. The risk

of existence or

occurrence refers to the

risk of validity of the

debt. On the other hand

the risk of completeness

For the risk of existence

or occurrence, the

auditor in order to

reduce the risk must

follow up the various

suspicious and

unreturned

confirmations of the

valid recording of

accounts. When it

comes to risk of

completeness, the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING THEORY AND PRACTICE

beef is 36 days. This

reflects the number of

days that an average

customer invoice

remains outstanding.

is the risk of the

incomplete record

auditor must assess all

the proceeds of sales

and gain comfort on the

ability of the company’s

process of transactions.

Investment The investment can be

analyzed by the ratio of

the number of times the

interest is earned on

investment (Yee, Sujan,

James & Leung, 2017).

In the year, 2016 the

interest received was

8.10 and in the year

2017 it was 7.51, it can

be said that the

investment for the TCW

has been increased. The

debt to equity ratio also

represents the

investment risk of the

company, higher the

ratio higher is the risk

associated to investment

(Louwers, et al., 2015).

In case the risk is high,

it reflects a substantial

obligation to the

investors who requires

scheduled payments.

This would alarm the

company, as this would

affect the working

capital. There exists

additionally an inherent

risk of material

misstatement in this

context.

The auditor in this case

may obtain evidence

about the investment

carried at cost value or

fair value as disclosed in

the financial statement.

They must also

recognize the

approaches for

determining the fair

value as per GAAP

(Generally Accepted

Accounting Principles).

Property assets In order to analyze the The risk that is It is the job of the

beef is 36 days. This

reflects the number of

days that an average

customer invoice

remains outstanding.

is the risk of the

incomplete record

auditor must assess all

the proceeds of sales

and gain comfort on the

ability of the company’s

process of transactions.

Investment The investment can be

analyzed by the ratio of

the number of times the

interest is earned on

investment (Yee, Sujan,

James & Leung, 2017).

In the year, 2016 the

interest received was

8.10 and in the year

2017 it was 7.51, it can

be said that the

investment for the TCW

has been increased. The

debt to equity ratio also

represents the

investment risk of the

company, higher the

ratio higher is the risk

associated to investment

(Louwers, et al., 2015).

In case the risk is high,

it reflects a substantial

obligation to the

investors who requires

scheduled payments.

This would alarm the

company, as this would

affect the working

capital. There exists

additionally an inherent

risk of material

misstatement in this

context.

The auditor in this case

may obtain evidence

about the investment

carried at cost value or

fair value as disclosed in

the financial statement.

They must also

recognize the

approaches for

determining the fair

value as per GAAP

(Generally Accepted

Accounting Principles).

Property assets In order to analyze the The risk that is It is the job of the

5AUDITING THEORY AND PRACTICE

audit risk when it comes

to property assets, the

ratio return on

production assets of

both segment of wine

and beef of the company

is to be analyzed. From

the given information, it

can be identified that the

return on beef

production asset for the

year 2017 has been

increased to -0.82%

from -3.45% that was in

2016.

associated with the

recording of the

property assets includes

correct cost basis

recording and

complexity in valuation

of the assets (Feng, et

al., 2014).

auditor to examine

whether the TCW has

capitalized all the cost

related to the purchase

of the assets along with

the record of all the

maintenance and repairs

of the assets. In addition

to that the auditor must

reduce the complexity

of the record of the

assets and make it more

fairly straightforward in

order to avoid gap in the

audit process and

accounting process.

Marketing Expense Marketing expense % of

total S & A expenses of

the company of will

represent the analysis

marketing expenses of

the TCW company. The

audited ratio for the year

2017 is 17.89% that has

been increased from

15.2% from the year

The risks involved in

the audit of the

marketing expense ratio

are the risk of

understatement, risk of

duplicate payment and

risk of inappropriate

vendors (Griffiths,

2016). There are also

other risks of control of

The steps of mitigating

the risk rekated to the

audit of the marketing

expense for the auditor

are to conduct a

reasonable check on the

records regularly along

with timely processing

of the expenses. As a

part of internal control

audit risk when it comes

to property assets, the

ratio return on

production assets of

both segment of wine

and beef of the company

is to be analyzed. From

the given information, it

can be identified that the

return on beef

production asset for the

year 2017 has been

increased to -0.82%

from -3.45% that was in

2016.

associated with the

recording of the

property assets includes

correct cost basis

recording and

complexity in valuation

of the assets (Feng, et

al., 2014).

auditor to examine

whether the TCW has

capitalized all the cost

related to the purchase

of the assets along with

the record of all the

maintenance and repairs

of the assets. In addition

to that the auditor must

reduce the complexity

of the record of the

assets and make it more

fairly straightforward in

order to avoid gap in the

audit process and

accounting process.

Marketing Expense Marketing expense % of

total S & A expenses of

the company of will

represent the analysis

marketing expenses of

the TCW company. The

audited ratio for the year

2017 is 17.89% that has

been increased from

15.2% from the year

The risks involved in

the audit of the

marketing expense ratio

are the risk of

understatement, risk of

duplicate payment and

risk of inappropriate

vendors (Griffiths,

2016). There are also

other risks of control of

The steps of mitigating

the risk rekated to the

audit of the marketing

expense for the auditor

are to conduct a

reasonable check on the

records regularly along

with timely processing

of the expenses. As a

part of internal control

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING THEORY AND PRACTICE

2016. the accounting in this

context.

audit, the auditor must

also verify the vendors

on a regular basis to

avoid the fraudulent

practices.

Answer to Question 1B

The business risk refers to the risk that is related to the income variance of the company.

Since the company of TCW has a relatively stable income over the time, they can easily predict

the utility bills of the customers within a certain range. The best way to analyze the business

risks is to conduct a ratio analysis that would help in obtaining a quick indication of the

performance of the firm in several key areas (Hoskin, Fizzell, & Cherry, 2014). It would help the

management to pinpoint the strength and weaknesses from with various initiatives and strategies

can be formed. In the company of TCW the ratio that are given and has to be analyzed are as

follows:

Return on equity: The return on equity is the method to analyze the profitability that

measures that amount if profit TCW would generate with each dollar of shareholders

equity. Return on equity for the year of 2017 has been increased to 17.5 from 15.5 that

were in 2016.however it has been assumed that the return on equity would decrease to

10.80 in 2018 as per unaudited records of TCW.

Return on beef production assets: The return on production assets refers to the power

of production and measurement of profit with the total assets invested in business. In the

given case, production refers to the beef production of the TCW. The percentage of return

2016. the accounting in this

context.

audit, the auditor must

also verify the vendors

on a regular basis to

avoid the fraudulent

practices.

Answer to Question 1B

The business risk refers to the risk that is related to the income variance of the company.

Since the company of TCW has a relatively stable income over the time, they can easily predict

the utility bills of the customers within a certain range. The best way to analyze the business

risks is to conduct a ratio analysis that would help in obtaining a quick indication of the

performance of the firm in several key areas (Hoskin, Fizzell, & Cherry, 2014). It would help the

management to pinpoint the strength and weaknesses from with various initiatives and strategies

can be formed. In the company of TCW the ratio that are given and has to be analyzed are as

follows:

Return on equity: The return on equity is the method to analyze the profitability that

measures that amount if profit TCW would generate with each dollar of shareholders

equity. Return on equity for the year of 2017 has been increased to 17.5 from 15.5 that

were in 2016.however it has been assumed that the return on equity would decrease to

10.80 in 2018 as per unaudited records of TCW.

Return on beef production assets: The return on production assets refers to the power

of production and measurement of profit with the total assets invested in business. In the

given case, production refers to the beef production of the TCW. The percentage of return

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING THEORY AND PRACTICE

on beef production assets has increased from -3.45 in 2016 to 0.82 in 2017. Howver as

per unaided records it has been assumed that the return on beef production asset would

increase to 1.67 in 2018.

Return on grape and wine production assets: The return on grape and wine production

assets similarly represents the power of production and measurement of profit with the

total assets invested in business (Newton et al., 2015). In the given case, production refers

to the grape and vine production of the TCW. In TCW the percentage return on grape and

wine production asset in 2016 was 16.2 that decreased to 14.5 in 2017. The unaudited

return that has been assumed is less than the previous two years that is 12.2.

Gross margin: The gross profit margin refers to the TCWs total revenue sales less its

cost of goods that are sold divided by the total sales (Weygandt, Kimmel & Kieso, 2015).

This measures total percent of the sales that the TCW retains after incurring the various

direct cost connected with manufacture the products, namely, beef and vine. If the

percentage is high, the company can retain the dollar of sales. The gross margin of TCW

was highest in 2016 that was 31.76 that decreased to 14.5 in 2017; the assumed gross

margin is reduced to 12.2 in 2018. This suggests that TCW could now able to retain more

dollars of sales.

Marketing expense over S/A expenses: The marketing expenses refers to the percentage

of money that has been spent out of the profit from the total of selling and administrative

expenses in order to enhance the sales (Jóhannesdóttir, et al., 2018). This is an indirect

cost. As per audited records of 2017 and 2016, the percentage of marketing expense has

been decreasing from 2016 amounting to 15.2 to 17.89 in 2017. it has been predicted as

per the unaudited record that the marketing expense ratio is to be increased to 23.67

on beef production assets has increased from -3.45 in 2016 to 0.82 in 2017. Howver as

per unaided records it has been assumed that the return on beef production asset would

increase to 1.67 in 2018.

Return on grape and wine production assets: The return on grape and wine production

assets similarly represents the power of production and measurement of profit with the

total assets invested in business (Newton et al., 2015). In the given case, production refers

to the grape and vine production of the TCW. In TCW the percentage return on grape and

wine production asset in 2016 was 16.2 that decreased to 14.5 in 2017. The unaudited

return that has been assumed is less than the previous two years that is 12.2.

Gross margin: The gross profit margin refers to the TCWs total revenue sales less its

cost of goods that are sold divided by the total sales (Weygandt, Kimmel & Kieso, 2015).

This measures total percent of the sales that the TCW retains after incurring the various

direct cost connected with manufacture the products, namely, beef and vine. If the

percentage is high, the company can retain the dollar of sales. The gross margin of TCW

was highest in 2016 that was 31.76 that decreased to 14.5 in 2017; the assumed gross

margin is reduced to 12.2 in 2018. This suggests that TCW could now able to retain more

dollars of sales.

Marketing expense over S/A expenses: The marketing expenses refers to the percentage

of money that has been spent out of the profit from the total of selling and administrative

expenses in order to enhance the sales (Jóhannesdóttir, et al., 2018). This is an indirect

cost. As per audited records of 2017 and 2016, the percentage of marketing expense has

been decreasing from 2016 amounting to 15.2 to 17.89 in 2017. it has been predicted as

per the unaudited record that the marketing expense ratio is to be increased to 23.67

8AUDITING THEORY AND PRACTICE

Times interest earned: The times to interest earned refers to the coverage ratio that

measures the ability of the company to honor the payment if debt. In case the interest

coverage ratio is less than one that means that, the company is not earning enough cash

from the various operations (Scarborough,2016). The interest earned is decreasing in the

company of TCW that represents that there is not much earning of cash. In 2017 the

interest earned was 7.51; in 2016 was 8.10 and the assumed and unaudited interest for

2018 was 6.67.

Days in inventory (wine): The days sales represents the number of days it took for

selling its stocks during a period that is specified. In this case, the inventory refers to the

production of the wine. In case of wine, the days of inventory for 2016 was 460, in 2017

was 423 and in case of the unaudited record the number of days is 367.

Days in accounts receivables (wine): The days in accounts receivables refers to the

average number of days that TCW would need to collect the payments on the goods that

are sold. If the numbers of days are higher, it indicates that there is a problem in the

collection and pressure in the cash flows (Hoskin, Fizzell, & Cherry, 2014). In case the

numbers of days are less, there is a strict policy of credit that may lessen down the high

sales revenue. In this case, the goods refer to the wine production of TCW. The days of

account receivable for wine was 53.24 in 2016, 60.65 in 2017 and the unaudited record

are 50.2.

Days in accounts receivables (beef): Similarly, the days in accounts receivables of the

beef production refers to number of days required for collecting the payments on the sale

of beef from the company (Khelil, Hussainey & Noubbigh, 2016). The days of account

receivable for beef was 24 in 2016, 36 in 2017 and the unaudited record are 57.

Times interest earned: The times to interest earned refers to the coverage ratio that

measures the ability of the company to honor the payment if debt. In case the interest

coverage ratio is less than one that means that, the company is not earning enough cash

from the various operations (Scarborough,2016). The interest earned is decreasing in the

company of TCW that represents that there is not much earning of cash. In 2017 the

interest earned was 7.51; in 2016 was 8.10 and the assumed and unaudited interest for

2018 was 6.67.

Days in inventory (wine): The days sales represents the number of days it took for

selling its stocks during a period that is specified. In this case, the inventory refers to the

production of the wine. In case of wine, the days of inventory for 2016 was 460, in 2017

was 423 and in case of the unaudited record the number of days is 367.

Days in accounts receivables (wine): The days in accounts receivables refers to the

average number of days that TCW would need to collect the payments on the goods that

are sold. If the numbers of days are higher, it indicates that there is a problem in the

collection and pressure in the cash flows (Hoskin, Fizzell, & Cherry, 2014). In case the

numbers of days are less, there is a strict policy of credit that may lessen down the high

sales revenue. In this case, the goods refer to the wine production of TCW. The days of

account receivable for wine was 53.24 in 2016, 60.65 in 2017 and the unaudited record

are 50.2.

Days in accounts receivables (beef): Similarly, the days in accounts receivables of the

beef production refers to number of days required for collecting the payments on the sale

of beef from the company (Khelil, Hussainey & Noubbigh, 2016). The days of account

receivable for beef was 24 in 2016, 36 in 2017 and the unaudited record are 57.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING THEORY AND PRACTICE

Current ratio: The current ratio refers to the liquidity ratio that helps in measuring the

company’s ability to cope up with the obligations both short-term and long term. It

calculated by dividing the total assets and liability of the company. In the given case the

total assets refers to both liquid and liquid assets of the company of TCW. The current

ratio was 2.66 in 2016, 2.54 in 2017 and the unaudited record is 2.80.

Quick asset ratio: The quick ratio or the acid -test ratio refers to the current assets that

can be easily converted into cash without any decrease in the value (Pizzini, Lin &

Ziegenfuss, 2014). The current ratio was 1.20 in 2016, 1.15 in 2017 and the unaudited

record is 1.18.

Debts to equity ratio: The ratio of debt to equity refers financial ratio that is calculated

to shows the relative proportion of shareholders debt and equity to finance the assets

relative to the value of shareholders equity (Cheng, Felix & Indjejikian, 2018). Debt to

equity ratio was 0.67 in 2016, 0.63 in 2017 and the unaudited record is 0.54.

From the above analysis of the ratio, different types of risks has been identified, Business

risk refers to the chance of not receiving a return on the investment. In case of the chosen

company of TCW the identified risk are:

Strategic risk: The strategic risk is the risk that results from operating within a specific

industry at a specific time that can take place from change in the technology or change in the

preference of the consumers (Martin, Sanders & Scalan, 2014). In case of TCW, they deal

with wines and beef therefore, the risk related to strategy is much less. However, there has

been installation of new IT system that may give rise to some risk.

Current ratio: The current ratio refers to the liquidity ratio that helps in measuring the

company’s ability to cope up with the obligations both short-term and long term. It

calculated by dividing the total assets and liability of the company. In the given case the

total assets refers to both liquid and liquid assets of the company of TCW. The current

ratio was 2.66 in 2016, 2.54 in 2017 and the unaudited record is 2.80.

Quick asset ratio: The quick ratio or the acid -test ratio refers to the current assets that

can be easily converted into cash without any decrease in the value (Pizzini, Lin &

Ziegenfuss, 2014). The current ratio was 1.20 in 2016, 1.15 in 2017 and the unaudited

record is 1.18.

Debts to equity ratio: The ratio of debt to equity refers financial ratio that is calculated

to shows the relative proportion of shareholders debt and equity to finance the assets

relative to the value of shareholders equity (Cheng, Felix & Indjejikian, 2018). Debt to

equity ratio was 0.67 in 2016, 0.63 in 2017 and the unaudited record is 0.54.

From the above analysis of the ratio, different types of risks has been identified, Business

risk refers to the chance of not receiving a return on the investment. In case of the chosen

company of TCW the identified risk are:

Strategic risk: The strategic risk is the risk that results from operating within a specific

industry at a specific time that can take place from change in the technology or change in the

preference of the consumers (Martin, Sanders & Scalan, 2014). In case of TCW, they deal

with wines and beef therefore, the risk related to strategy is much less. However, there has

been installation of new IT system that may give rise to some risk.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING THEORY AND PRACTICE

Compliance risk: The risks that are associated with compliance refers to bureaucratic or

legislative regulations that the company may follow (Kraft, 2014). In case of TCW since

there exist a sound internal control, the risk related to compliance is less.

Financial risk: The risk related to financial loss is known as financial risk. In case of TCW,

there can take place a huge financial risk due to the adaptation of new IT system (Tayeh, Al-

Jarrah, & Tarhini, 2015). Moreover, the three of the segment of grapes, wines and beef may

encounter of loss of fiancé.

Operational risk: The operational risk is the risk that takes due to internal failures that

comes out from the business operations (Duff, et al., 2017). This can also takes place from

unforeseen external events. Since in TCW operates in both wine and beef the operational risk

is high.

Reputational risk: The reputational risk refers to that risk that takes place due to the

anticipation of losing the reputation of the company or negative publicity (Minnis &

Sutherland, 2017). The reputational risk is also high in case of the company of TCW since it

operates in more than two sectors.

Answer to question 2A

Internal control refers to the assurance of organizations objectives in the operational

efficiency and effectiveness. It is system of verification of whether the financial reporting

compliance with the regulations, laws and policies.

Compliance risk: The risks that are associated with compliance refers to bureaucratic or

legislative regulations that the company may follow (Kraft, 2014). In case of TCW since

there exist a sound internal control, the risk related to compliance is less.

Financial risk: The risk related to financial loss is known as financial risk. In case of TCW,

there can take place a huge financial risk due to the adaptation of new IT system (Tayeh, Al-

Jarrah, & Tarhini, 2015). Moreover, the three of the segment of grapes, wines and beef may

encounter of loss of fiancé.

Operational risk: The operational risk is the risk that takes due to internal failures that

comes out from the business operations (Duff, et al., 2017). This can also takes place from

unforeseen external events. Since in TCW operates in both wine and beef the operational risk

is high.

Reputational risk: The reputational risk refers to that risk that takes place due to the

anticipation of losing the reputation of the company or negative publicity (Minnis &

Sutherland, 2017). The reputational risk is also high in case of the company of TCW since it

operates in more than two sectors.

Answer to question 2A

Internal control refers to the assurance of organizations objectives in the operational

efficiency and effectiveness. It is system of verification of whether the financial reporting

compliance with the regulations, laws and policies.

11AUDITING THEORY AND PRACTICE

Internal control in the given company of TCW is the process that is affected by the

management of the company, board of trustees and other various people who are responsible for

providing the reasonable assurance for the attainment the objectives of the following –

Complying with laws and regulations that are applicable

The various operations effectiveness and Efficiency

Financial reporting reliability

In TCW the elements of internal control are taken in consideration as per the of the

standard guidelines, if –

There is proper approval of the procedures has been followed for the capital expenses

Proper insurance coverage has been provided for the assets exposure.

The calculation of the Depreciation is provided and done properly for each period

The salvage value and the useful life has neen properly determined

In the enterprise of TCW, the organization takes in hand the business profitability not

just as the function of the revenue but also for proper resources management. The identified

internal controls are:

Effective control Risk alleviated Test of Control

Controlling environment The risk that is alleviated while

controlling the environment of

TCW is the operational risk,

and the reputational risk.

The test of control refers to the

check of the moral values,

managerial skills, honesty of the

employees working and the

direction of the company.

Risk assessment In this system of control, the Risk assessment refers to the

Internal control in the given company of TCW is the process that is affected by the

management of the company, board of trustees and other various people who are responsible for

providing the reasonable assurance for the attainment the objectives of the following –

Complying with laws and regulations that are applicable

The various operations effectiveness and Efficiency

Financial reporting reliability

In TCW the elements of internal control are taken in consideration as per the of the

standard guidelines, if –

There is proper approval of the procedures has been followed for the capital expenses

Proper insurance coverage has been provided for the assets exposure.

The calculation of the Depreciation is provided and done properly for each period

The salvage value and the useful life has neen properly determined

In the enterprise of TCW, the organization takes in hand the business profitability not

just as the function of the revenue but also for proper resources management. The identified

internal controls are:

Effective control Risk alleviated Test of Control

Controlling environment The risk that is alleviated while

controlling the environment of

TCW is the operational risk,

and the reputational risk.

The test of control refers to the

check of the moral values,

managerial skills, honesty of the

employees working and the

direction of the company.

Risk assessment In this system of control, the Risk assessment refers to the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.