Managerial Accounting Report: TDABC Implementation for ADCO

VerifiedAdded on 2020/05/16

|11

|2867

|236

Report

AI Summary

This report provides a comprehensive analysis of managerial accounting, focusing on different costing methods and their applications. It begins with an introduction to the importance of cost management for businesses of all sizes, followed by a detailed description of Time-Driven Activity-Based Costing (TDABC) and its key features. The report then compares TDABC with Activity-Based Costing (ABC) and traditional costing methods, highlighting their differences and advantages. A case study of ADCO Construction is presented, evaluating the suitability of TDABC for the firm and suggesting implementation strategies. The report concludes with a summary of the key findings, emphasizing the benefits of TDABC as a superior costing mechanism. The report utilizes information from various academic sources to support the analysis.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Name of the student

Name of the University

Author note

Managerial Accounting

Name of the student

Name of the University

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGERIAL ACCOUNTING

Table of Contents

Introduction:....................................................................................................................................2

Description of the client’s firm:.......................................................................................................2

Description regarding TDABC and its features:.............................................................................3

Difference among traditional costing mechanism, TDABC and ABC:..........................................6

Suitability check of TDABC for firm’s clients:..............................................................................7

Conclusion:......................................................................................................................................8

Reference:........................................................................................................................................9

Table of Contents

Introduction:....................................................................................................................................2

Description of the client’s firm:.......................................................................................................2

Description regarding TDABC and its features:.............................................................................3

Difference among traditional costing mechanism, TDABC and ABC:..........................................6

Suitability check of TDABC for firm’s clients:..............................................................................7

Conclusion:......................................................................................................................................8

Reference:........................................................................................................................................9

2MANAGERIAL ACCOUNTING

Introduction:

With rise in competition among the firms, it has been highly essential for the managers to

understand the importance of cost for their firms irrespective of its size. Whether it is a big

multinational organisation or a small firm, it is important to understand the costing method

(Hemmer and Labro 2016). Main goal of understanding the costing is to provide proper

information regarding the internal decision-making and provide much needed outlook for the

control and planning purpose of the firm (Cooper 2017). Besides this, knowledge regarding

costing aids the mangers to assess the alteration in the market scenario and trace out changes in

trade. This report considers the TDABC method of costing and highlights its various

importances. Besides this, an overview regarding different methods of costing that include ABC

and traditional method of costing will be given in this analysis. Along with this, the report will

try to draw difference between TDABC, traditional costing system and ABC method of costing.

Moving further, the report will highlight the suitability of TDABC in the ADCO construction

and provide details regarding implementation of TDABC in the firm.

Description of the client’s firm:

The ADCO Construction is one of the leading construction companies of Australia that

has been serving national project since 1972 (Adcoconstruct.com.au, 2018). According to the

words of ADCO Construction, until 2017, the company has served almost 3,500 completed

projects and it is valued at $10 billion. With its annual revenue figure of $1 billion and almost

600 employees, ADCO is one of the top 50 private organisations of Australia. Main service of

the brand lies in the construction industry and its high level of resources enable the firm to

remain aligned with the latest techniques of construction. Besides this, the firm is well known for

its practical utilisation of materials and products that provides the firm efficiency, which is at par

Introduction:

With rise in competition among the firms, it has been highly essential for the managers to

understand the importance of cost for their firms irrespective of its size. Whether it is a big

multinational organisation or a small firm, it is important to understand the costing method

(Hemmer and Labro 2016). Main goal of understanding the costing is to provide proper

information regarding the internal decision-making and provide much needed outlook for the

control and planning purpose of the firm (Cooper 2017). Besides this, knowledge regarding

costing aids the mangers to assess the alteration in the market scenario and trace out changes in

trade. This report considers the TDABC method of costing and highlights its various

importances. Besides this, an overview regarding different methods of costing that include ABC

and traditional method of costing will be given in this analysis. Along with this, the report will

try to draw difference between TDABC, traditional costing system and ABC method of costing.

Moving further, the report will highlight the suitability of TDABC in the ADCO construction

and provide details regarding implementation of TDABC in the firm.

Description of the client’s firm:

The ADCO Construction is one of the leading construction companies of Australia that

has been serving national project since 1972 (Adcoconstruct.com.au, 2018). According to the

words of ADCO Construction, until 2017, the company has served almost 3,500 completed

projects and it is valued at $10 billion. With its annual revenue figure of $1 billion and almost

600 employees, ADCO is one of the top 50 private organisations of Australia. Main service of

the brand lies in the construction industry and its high level of resources enable the firm to

remain aligned with the latest techniques of construction. Besides this, the firm is well known for

its practical utilisation of materials and products that provides the firm efficiency, which is at par

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGERIAL ACCOUNTING

with the commercial manner. Continued success of the ADCO Construction has enabled the firm

to find its customer from blue chip base of client that comprise state, federal and local

government agencies (Adcoconstruct.com.au, 2018). Besides this, the firm has served various

institutional and private corporate with their service of construction, making the firm a market

leader in the construction industry. The firm has wide base of 580 to 600 direct employees and

40% of them are engaged in operation with the firm for more than 7 years

(Adcoconstruct.com.au, 2018). With their efficient allocation of human capital and resource

allocation, turnover rate is lower than its competitors that have lead the firm to a better goodwill.

ADCO Construction guarantees delivery to their clients, according to the manager of the firm,

which has been gained through combination of unique techniques, skilled labour and idea of

costing.

Description regarding TDABC and its features:

Until 1984, firms used to prefer traditional method for costing, however scenario changed

when Activity Based Costing (ABC) came into action. Traditional mechanism of costing was

introduced during 1920, and it used to consider only three costing parameters, which are

materials, labour and overhead (Weygandt, Kimmel. and Kieso 2015). However, with change in

market scenario and economy of business, traditional costing mechanism started to become

complex and traditional accounting failed to calculate the overheads. By the time of 1984, firms

started to utilize distorted information regarding orders, customers, products and profitability that

has crippled the standard method of accounting. Thus, during 1984, a new mechanism of costing

was introduced, which was known as the ABC (Plank 2018).

Activity Based Costing mechanism was presented as the completed method of costing

that not only addresses the pitfalls of the traditional methods moreover enable the mangers to

with the commercial manner. Continued success of the ADCO Construction has enabled the firm

to find its customer from blue chip base of client that comprise state, federal and local

government agencies (Adcoconstruct.com.au, 2018). Besides this, the firm has served various

institutional and private corporate with their service of construction, making the firm a market

leader in the construction industry. The firm has wide base of 580 to 600 direct employees and

40% of them are engaged in operation with the firm for more than 7 years

(Adcoconstruct.com.au, 2018). With their efficient allocation of human capital and resource

allocation, turnover rate is lower than its competitors that have lead the firm to a better goodwill.

ADCO Construction guarantees delivery to their clients, according to the manager of the firm,

which has been gained through combination of unique techniques, skilled labour and idea of

costing.

Description regarding TDABC and its features:

Until 1984, firms used to prefer traditional method for costing, however scenario changed

when Activity Based Costing (ABC) came into action. Traditional mechanism of costing was

introduced during 1920, and it used to consider only three costing parameters, which are

materials, labour and overhead (Weygandt, Kimmel. and Kieso 2015). However, with change in

market scenario and economy of business, traditional costing mechanism started to become

complex and traditional accounting failed to calculate the overheads. By the time of 1984, firms

started to utilize distorted information regarding orders, customers, products and profitability that

has crippled the standard method of accounting. Thus, during 1984, a new mechanism of costing

was introduced, which was known as the ABC (Plank 2018).

Activity Based Costing mechanism was presented as the completed method of costing

that not only addresses the pitfalls of the traditional methods moreover enable the mangers to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGERIAL ACCOUNTING

customize it depending upon the requirement of the present scenario. However, many firms

rejected it due to various complications leading to search for another model of costing that

addresses the drawback of the ABC mechanism. According to the Prasad (2014)Major reasons

for rejecting the ABC model were its organisational and behavioural resistance. Besides this, the

ABC model was intricate to sustain, hard to customize according to the need and expensive to

introduce in the firm. It need rigorous survey and interviewing of the employees that makes it

complex and expensive to be implemented in the firms. Moreover, if any customization required,

then reinter viewing and resurvey need to be done, making it complex. Success came in 2004,

when one of the initiator of ABC model, Kaplan, brings in another new mechanism of costing,

which is known as the Time Driven Activity based Costing (TDABC) (Kaplan 2014). According

to him, TDABC is more accurate, elegant and simplified approach for costing. Besides this,

TDABC is cost effective mechanism of costing and it aids the firm to customize the model

deepening upon the requirement.

TDABC offers better information regarding the earnings of the firms and it accurately

demonstrates the frequency of profit. Utilizing the cost difference among the customers who

have higher demand along with complex client preference than those who have lower demand

along easy customer preference, TDABC highlights accurate result of profitability of the firms

(Afonso and Santana 2016). Simplifying the process of costing compared to the ABC method

was one of the main reasons for bringing in the TDABC and it successfully does so. This new

model of costing does not require any surveying or interviewing for resource allocation for the

activities of the firm before inserting them into the cost objectives; instead, TDABC model using

a comprehensive framework, assigns the cost of resources directly toward the cost objectives.

Utilizing two set of factors TDABC calculates the costing details of a firm and enables the

customize it depending upon the requirement of the present scenario. However, many firms

rejected it due to various complications leading to search for another model of costing that

addresses the drawback of the ABC mechanism. According to the Prasad (2014)Major reasons

for rejecting the ABC model were its organisational and behavioural resistance. Besides this, the

ABC model was intricate to sustain, hard to customize according to the need and expensive to

introduce in the firm. It need rigorous survey and interviewing of the employees that makes it

complex and expensive to be implemented in the firms. Moreover, if any customization required,

then reinter viewing and resurvey need to be done, making it complex. Success came in 2004,

when one of the initiator of ABC model, Kaplan, brings in another new mechanism of costing,

which is known as the Time Driven Activity based Costing (TDABC) (Kaplan 2014). According

to him, TDABC is more accurate, elegant and simplified approach for costing. Besides this,

TDABC is cost effective mechanism of costing and it aids the firm to customize the model

deepening upon the requirement.

TDABC offers better information regarding the earnings of the firms and it accurately

demonstrates the frequency of profit. Utilizing the cost difference among the customers who

have higher demand along with complex client preference than those who have lower demand

along easy customer preference, TDABC highlights accurate result of profitability of the firms

(Afonso and Santana 2016). Simplifying the process of costing compared to the ABC method

was one of the main reasons for bringing in the TDABC and it successfully does so. This new

model of costing does not require any surveying or interviewing for resource allocation for the

activities of the firm before inserting them into the cost objectives; instead, TDABC model using

a comprehensive framework, assigns the cost of resources directly toward the cost objectives.

Utilizing two set of factors TDABC calculates the costing details of a firm and enables the

5MANAGERIAL ACCOUNTING

managers to assess their optimal outcome, profitability and various other factors that affects the

firms business. Two factors of computing TDABC are as follows (Stouthuysen et al. 2014):

1. Rather than using the information from survey and interview, it computes the cost of

resource supplying

2. TDABC utilizes the Capacity Cost Rate in order to bring in departmental costs into the

computation of cost through estimation of resource capacity for demand.

Using the time requirement for performing an activity, TDABC is highly efficient to

recognize the cost of every unit including the cost of allocation. Various features of the TDABC

are as follows (AhmadPour and AzimiMoghadam 2016):

It is a complete strategic model, which is fast, easy to build and inexpensive in nature

This model successfully identifies the opportunities for capacity management and process

efficiencies

One of the best features of this model is that it can be customized and updated easily

depending upon the requirement of the firm

The model is based on the individual customer orders, suppliers, process and

transactions, thus it is efficient and effective for cost calculation of the firm

This model allows forecasting demand of resources that permit the companies to frame

their budget and trace out ideal level of output utilizing the database technologies and

application software

TDABC integrate Enterprise Resource Planning (ERP) information though an efficient

way and enables the TDABC to become a vibrant system for Customer Relationship

Management

managers to assess their optimal outcome, profitability and various other factors that affects the

firms business. Two factors of computing TDABC are as follows (Stouthuysen et al. 2014):

1. Rather than using the information from survey and interview, it computes the cost of

resource supplying

2. TDABC utilizes the Capacity Cost Rate in order to bring in departmental costs into the

computation of cost through estimation of resource capacity for demand.

Using the time requirement for performing an activity, TDABC is highly efficient to

recognize the cost of every unit including the cost of allocation. Various features of the TDABC

are as follows (AhmadPour and AzimiMoghadam 2016):

It is a complete strategic model, which is fast, easy to build and inexpensive in nature

This model successfully identifies the opportunities for capacity management and process

efficiencies

One of the best features of this model is that it can be customized and updated easily

depending upon the requirement of the firm

The model is based on the individual customer orders, suppliers, process and

transactions, thus it is efficient and effective for cost calculation of the firm

This model allows forecasting demand of resources that permit the companies to frame

their budget and trace out ideal level of output utilizing the database technologies and

application software

TDABC integrate Enterprise Resource Planning (ERP) information though an efficient

way and enables the TDABC to become a vibrant system for Customer Relationship

Management

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGERIAL ACCOUNTING

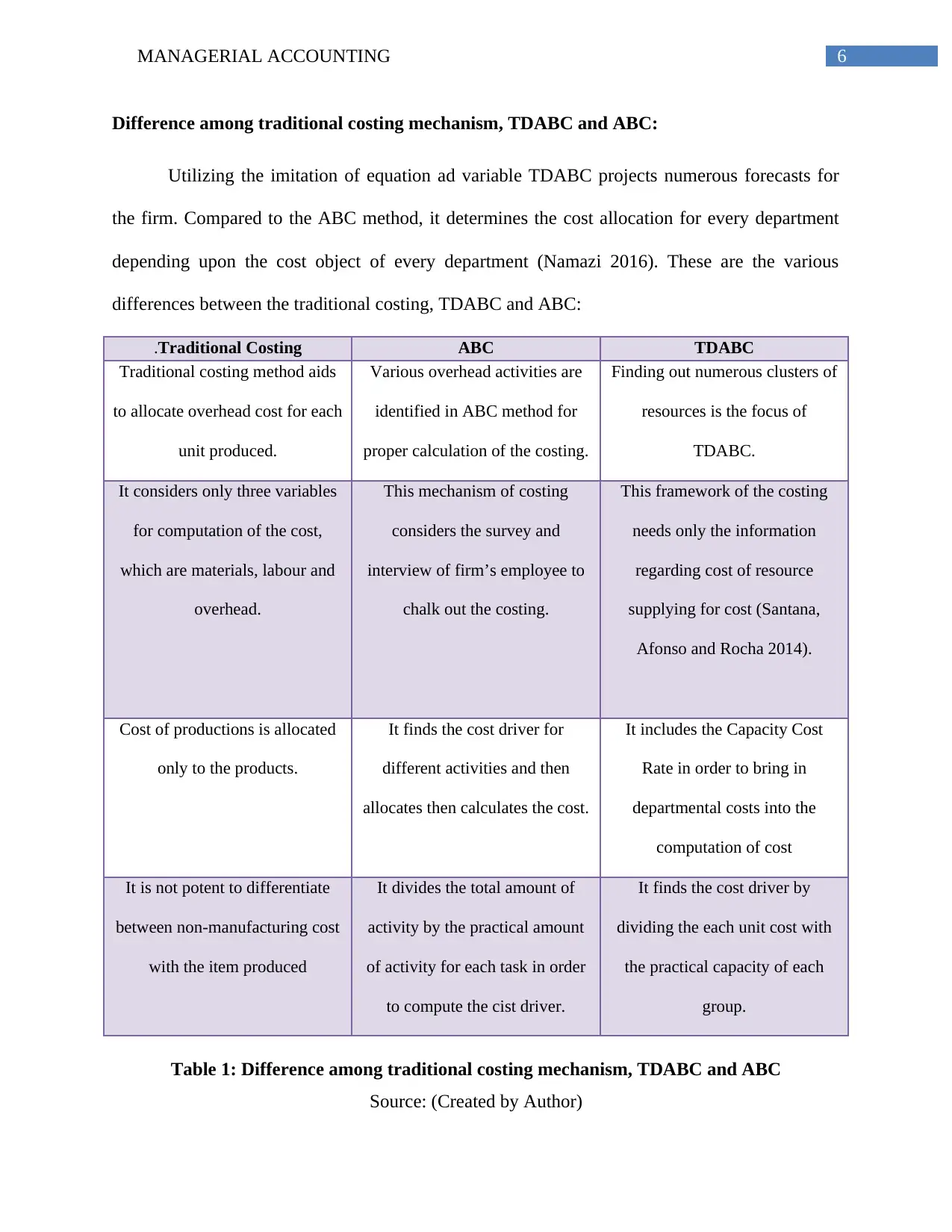

Difference among traditional costing mechanism, TDABC and ABC:

Utilizing the imitation of equation ad variable TDABC projects numerous forecasts for

the firm. Compared to the ABC method, it determines the cost allocation for every department

depending upon the cost object of every department (Namazi 2016). These are the various

differences between the traditional costing, TDABC and ABC:

.Traditional Costing ABC TDABC

Traditional costing method aids

to allocate overhead cost for each

unit produced.

Various overhead activities are

identified in ABC method for

proper calculation of the costing.

Finding out numerous clusters of

resources is the focus of

TDABC.

It considers only three variables

for computation of the cost,

which are materials, labour and

overhead.

This mechanism of costing

considers the survey and

interview of firm’s employee to

chalk out the costing.

This framework of the costing

needs only the information

regarding cost of resource

supplying for cost (Santana,

Afonso and Rocha 2014).

Cost of productions is allocated

only to the products.

It finds the cost driver for

different activities and then

allocates then calculates the cost.

It includes the Capacity Cost

Rate in order to bring in

departmental costs into the

computation of cost

It is not potent to differentiate

between non-manufacturing cost

with the item produced

It divides the total amount of

activity by the practical amount

of activity for each task in order

to compute the cist driver.

It finds the cost driver by

dividing the each unit cost with

the practical capacity of each

group.

Table 1: Difference among traditional costing mechanism, TDABC and ABC

Source: (Created by Author)

Difference among traditional costing mechanism, TDABC and ABC:

Utilizing the imitation of equation ad variable TDABC projects numerous forecasts for

the firm. Compared to the ABC method, it determines the cost allocation for every department

depending upon the cost object of every department (Namazi 2016). These are the various

differences between the traditional costing, TDABC and ABC:

.Traditional Costing ABC TDABC

Traditional costing method aids

to allocate overhead cost for each

unit produced.

Various overhead activities are

identified in ABC method for

proper calculation of the costing.

Finding out numerous clusters of

resources is the focus of

TDABC.

It considers only three variables

for computation of the cost,

which are materials, labour and

overhead.

This mechanism of costing

considers the survey and

interview of firm’s employee to

chalk out the costing.

This framework of the costing

needs only the information

regarding cost of resource

supplying for cost (Santana,

Afonso and Rocha 2014).

Cost of productions is allocated

only to the products.

It finds the cost driver for

different activities and then

allocates then calculates the cost.

It includes the Capacity Cost

Rate in order to bring in

departmental costs into the

computation of cost

It is not potent to differentiate

between non-manufacturing cost

with the item produced

It divides the total amount of

activity by the practical amount

of activity for each task in order

to compute the cist driver.

It finds the cost driver by

dividing the each unit cost with

the practical capacity of each

group.

Table 1: Difference among traditional costing mechanism, TDABC and ABC

Source: (Created by Author)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGERIAL ACCOUNTING

Traditional mechanism of costing was introduced way back during 1920s and uses direct

labour hours for deciding the costing overheads for manufacturing of each product. However, it

fails to differentiate between the non-manufacturing cost and the manufacturing cost that makes

it unable for the customizations. One the other hand, new mechanism of TDABC aids the firm to

measure effectiveness in production of the goods and services of the firm. According to the

Gunasekaran, Williams and McGaughey 2015, TDABC requires time projection for the process

in order to process the customer orders and it does not mandatorily follow the principal of

traditional accounting system, where customer cost need to be equal with the projected cost.

Suitability check of TDABC for firm’s clients:

Utilizing the traditional framework of costing for the ADCO Construction the firm can

distribute the cost of its resources towards the activities before sending them toward the cost

objects. One of the important consideration need to look out in this regard is that the TDABC

mechanism will be beneficial for the firm because it uses smart framework for the estimation of

the profit (Todorovic 2014) . TDABC uses Cost Capacity Rate for finding the resource cost by

utilizing the demand of the resources, which will help the ADCO Construction in time estimation

for customer order process. Moreover, it would aid the firm to have a watch on the variations in

the market and alert the firm regarding the projection of storage, capital and production

requirement (Namazi 2016). Additionally it would help the firm to sustain in its business

ventures proving it better sustainability.

Thus from the above analysis it can be stated that if the ADCO Construction used the

TDBAC framework, then it would help the firm to have better profitability and smooth

transformation of its business from ABC to TDABC (Hoozee and Hansen 2014). Smart

framework of the TDABC would be beneficial for the firm to upgrade and customize the

Traditional mechanism of costing was introduced way back during 1920s and uses direct

labour hours for deciding the costing overheads for manufacturing of each product. However, it

fails to differentiate between the non-manufacturing cost and the manufacturing cost that makes

it unable for the customizations. One the other hand, new mechanism of TDABC aids the firm to

measure effectiveness in production of the goods and services of the firm. According to the

Gunasekaran, Williams and McGaughey 2015, TDABC requires time projection for the process

in order to process the customer orders and it does not mandatorily follow the principal of

traditional accounting system, where customer cost need to be equal with the projected cost.

Suitability check of TDABC for firm’s clients:

Utilizing the traditional framework of costing for the ADCO Construction the firm can

distribute the cost of its resources towards the activities before sending them toward the cost

objects. One of the important consideration need to look out in this regard is that the TDABC

mechanism will be beneficial for the firm because it uses smart framework for the estimation of

the profit (Todorovic 2014) . TDABC uses Cost Capacity Rate for finding the resource cost by

utilizing the demand of the resources, which will help the ADCO Construction in time estimation

for customer order process. Moreover, it would aid the firm to have a watch on the variations in

the market and alert the firm regarding the projection of storage, capital and production

requirement (Namazi 2016). Additionally it would help the firm to sustain in its business

ventures proving it better sustainability.

Thus from the above analysis it can be stated that if the ADCO Construction used the

TDBAC framework, then it would help the firm to have better profitability and smooth

transformation of its business from ABC to TDABC (Hoozee and Hansen 2014). Smart

framework of the TDABC would be beneficial for the firm to upgrade and customize the

8MANAGERIAL ACCOUNTING

accounting mechanism for the firm and enable it to forecast the demand properly. Additional

benefits of utilizing the TDABC for the ADCO Construction is that it if the firm uses TDABC,

then it would cost less for accounting because it does not require any survey and interviewing of

the employee of various departments and enhance the ERP (Ai-Min et al. 2016). Moreover, it is

also required to highlight that being a flexible framework of costing; it would enable the firm to

customize the model for further alteration in future depending upon the requirement.

Conclusion:

The report has analyzed the various aspects of TDABC and compared it with the ABC

and the traditional mechanism of auditing. From the comparison, it has been found that TDABC

is far more superior and complete mechanism of costing calculation. It not only simple and

inexpensive, moreover it aids the firms to forecast their demand and make budgetary framework

accordingly. This report was meant to analyze if an organisation like ADCO Construction imply

TDABC into its framework, then how would be the suitability of this implementation. The report

has found that TDABC, being the easiest framework of costing, would be highly beneficial for

the firm. TDABC model will help the firm to avoid costly mechanism of costing and saves lot of

time on behalf of this computation. Moreover, the report has found that TDABC will help the

managers of the ADCO Construction, to overcome the problems related to their CRM and ERP

system. Though TDABC analyzes the historical data, however, it can effectively determine the

future trend and help the firm like ADCO Construction to forecast their future. To conclude, it

can be said that, TDABC is a complete mechanism of costing and if the ADCO Construction

implement it in its framework, then it would help the firm to become more successful with its

ventures by utilizing the cost effective mechanism of costing and forecasting.

accounting mechanism for the firm and enable it to forecast the demand properly. Additional

benefits of utilizing the TDABC for the ADCO Construction is that it if the firm uses TDABC,

then it would cost less for accounting because it does not require any survey and interviewing of

the employee of various departments and enhance the ERP (Ai-Min et al. 2016). Moreover, it is

also required to highlight that being a flexible framework of costing; it would enable the firm to

customize the model for further alteration in future depending upon the requirement.

Conclusion:

The report has analyzed the various aspects of TDABC and compared it with the ABC

and the traditional mechanism of auditing. From the comparison, it has been found that TDABC

is far more superior and complete mechanism of costing calculation. It not only simple and

inexpensive, moreover it aids the firms to forecast their demand and make budgetary framework

accordingly. This report was meant to analyze if an organisation like ADCO Construction imply

TDABC into its framework, then how would be the suitability of this implementation. The report

has found that TDABC, being the easiest framework of costing, would be highly beneficial for

the firm. TDABC model will help the firm to avoid costly mechanism of costing and saves lot of

time on behalf of this computation. Moreover, the report has found that TDABC will help the

managers of the ADCO Construction, to overcome the problems related to their CRM and ERP

system. Though TDABC analyzes the historical data, however, it can effectively determine the

future trend and help the firm like ADCO Construction to forecast their future. To conclude, it

can be said that, TDABC is a complete mechanism of costing and if the ADCO Construction

implement it in its framework, then it would help the firm to become more successful with its

ventures by utilizing the cost effective mechanism of costing and forecasting.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGERIAL ACCOUNTING

Reference:

Adcoconstruct.com.au. (2018). Overview | ADCO. [online] Available at:

http://www.adcoconstruct.com.au/about-us/overview/ [Accessed 25 Jan. 2018].

Adcoconstruct.com.au. (2018). Projects | ADCO. [online] Available at:

http://www.adcoconstruct.com.au/projects/ [Accessed 25 Jan. 2018].

AhmadPour, J. and AzimiMoghadam, A., 2016. Identifying operational improvements during the

design process of costing system based on time-driven ABC (TDABC)(The role of staff public

participation and leadership style). Bulletin de la Société Royale des Sciences de Liège, 85,

pp.999-1016.

Ai-Min, D.E.N.G., Hong, L.I. and Hao, T.I.A.N., 2016. Based on the Cloud ERP and TDABC

for the SMEs’ Logistics Cost Accounting. DEStech Transactions on Engineering and

Technology Research, (sste).

Cooper, R., 2017. Target costing and value engineering. Routledge.

Gunasekaran, A., Williams, H.J. and McGaughey, R.E., 2015. Performance measurement and

costing system in new enterprise. Technovation, 25(5), pp.523-533.

Hemmer, T. and Labro, E., 2016. Productions and Operations Management & Management

Accounting.

Hoozée, S. and Hansen, S., 2014. A comparison of activity-based costing and time-driven

activity-based costing. Journal of Management Accounting Research.

Kaplan, R.S., 2014. Improving value with TDABC. Healthcare Financial Management, 68(6),

pp.76-84.

Namazi, M., 2016. Time-driven activity-based costing: Theory, applications and

limitations. Iranian Journal of Management Studies, 9(3), p.457.

Reference:

Adcoconstruct.com.au. (2018). Overview | ADCO. [online] Available at:

http://www.adcoconstruct.com.au/about-us/overview/ [Accessed 25 Jan. 2018].

Adcoconstruct.com.au. (2018). Projects | ADCO. [online] Available at:

http://www.adcoconstruct.com.au/projects/ [Accessed 25 Jan. 2018].

AhmadPour, J. and AzimiMoghadam, A., 2016. Identifying operational improvements during the

design process of costing system based on time-driven ABC (TDABC)(The role of staff public

participation and leadership style). Bulletin de la Société Royale des Sciences de Liège, 85,

pp.999-1016.

Ai-Min, D.E.N.G., Hong, L.I. and Hao, T.I.A.N., 2016. Based on the Cloud ERP and TDABC

for the SMEs’ Logistics Cost Accounting. DEStech Transactions on Engineering and

Technology Research, (sste).

Cooper, R., 2017. Target costing and value engineering. Routledge.

Gunasekaran, A., Williams, H.J. and McGaughey, R.E., 2015. Performance measurement and

costing system in new enterprise. Technovation, 25(5), pp.523-533.

Hemmer, T. and Labro, E., 2016. Productions and Operations Management & Management

Accounting.

Hoozée, S. and Hansen, S., 2014. A comparison of activity-based costing and time-driven

activity-based costing. Journal of Management Accounting Research.

Kaplan, R.S., 2014. Improving value with TDABC. Healthcare Financial Management, 68(6),

pp.76-84.

Namazi, M., 2016. Time-driven activity-based costing: Theory, applications and

limitations. Iranian Journal of Management Studies, 9(3), p.457.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGERIAL ACCOUNTING

Plank, P., 2018. Introduction. In Price and Product-Mix Decisions Under Different Cost

Systems (pp. 1-5). Springer Gabler, Wiesbaden.

Prasad, A.D., 2014. Must Make Cost & Management Accounting Key to Building National

Competitiveness. The MA Journal, 49(8), pp.9-10.

Prasad, A.D., 2014. Must Make Cost & Management Accounting Key to Building National

Competitiveness. The MA Journal, 49(8), pp.9-10.

Santana, A., Afonso, P. and ROCHA, A., 2014. Activity Based Costing and Time-Driven

Activity Based Costing: Towards an Integrated Approach. In ICOPEV-2nd International

Conference on Project Evaluation, Guimarães/PT.

Stouthuysen, K., Schierhout, K., Roodhooft, F. and Reusen, E., 2014. Time-driven activity-based

costing for public services. Public Money & Management, 34(4), pp.289-296.

Todorovic, M., 2014. Key Aspects of Building and Application of Time Equations in Costs

Calculation.

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2015. Financial & Managerial Accounting. John

Wiley & Sons.

Plank, P., 2018. Introduction. In Price and Product-Mix Decisions Under Different Cost

Systems (pp. 1-5). Springer Gabler, Wiesbaden.

Prasad, A.D., 2014. Must Make Cost & Management Accounting Key to Building National

Competitiveness. The MA Journal, 49(8), pp.9-10.

Prasad, A.D., 2014. Must Make Cost & Management Accounting Key to Building National

Competitiveness. The MA Journal, 49(8), pp.9-10.

Santana, A., Afonso, P. and ROCHA, A., 2014. Activity Based Costing and Time-Driven

Activity Based Costing: Towards an Integrated Approach. In ICOPEV-2nd International

Conference on Project Evaluation, Guimarães/PT.

Stouthuysen, K., Schierhout, K., Roodhooft, F. and Reusen, E., 2014. Time-driven activity-based

costing for public services. Public Money & Management, 34(4), pp.289-296.

Todorovic, M., 2014. Key Aspects of Building and Application of Time Equations in Costs

Calculation.

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2015. Financial & Managerial Accounting. John

Wiley & Sons.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.